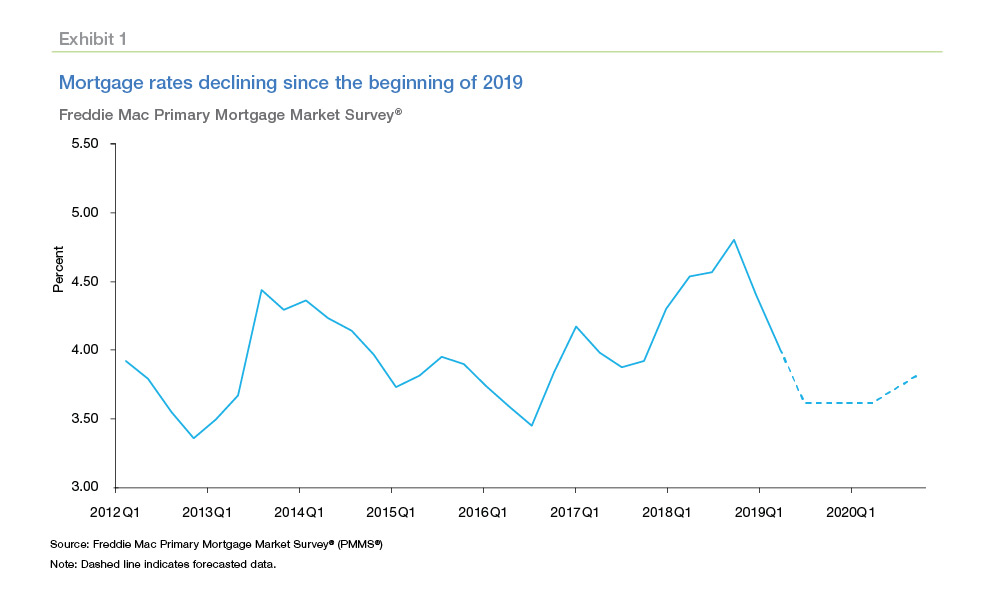

The year 2020 will forever be etched in history for many reasons, not least among them the unprecedented plunge in mortgage rates to historic lows. As the world grappled with a global pandemic, financial markets responded with a series of dramatic shifts, creating an environment where borrowing money to buy or refinance a home became remarkably cheap. This phenomenon wasn’t accidental; it was the direct result of an extraordinary combination of aggressive monetary policy, profound economic uncertainty, and unique market dynamics that collectively reshaped the landscape of homeownership and personal finance. Understanding the forces at play offers critical insights into the intricate workings of the economy and the powerful tools available to central banks in times of crisis.

The Federal Reserve’s Aggressive Response to the Pandemic

At the heart of 2020’s low mortgage rates was the swift and decisive action taken by the U.S. Federal Reserve. Faced with an economic shutdown of a scale not seen in generations, the Fed moved with an urgency aimed at preventing a complete financial collapse and stimulating recovery.

Cutting the Federal Funds Rate to Near Zero

One of the Fed’s primary tools for influencing the economy is the federal funds rate, the target rate for overnight lending between banks. In March 2020, as the economic impact of COVID-19 became starkly clear, the Federal Reserve executed two emergency rate cuts, slashing the federal funds rate from a range of 1.50-1.75% down to a new range of 0.00-0.25%. This move signaled the Fed’s commitment to providing maximum support to the economy. While the federal funds rate doesn’t directly dictate long-term mortgage rates, it sets the baseline for borrowing costs across the financial system. Lower short-term rates generally translate to lower costs for banks to fund their operations, which, in turn, can trickle down to consumer loan products, including adjustable-rate mortgages and indirectly, fixed-rate mortgages. The immediate psychological impact on markets was also significant, reassuring investors and consumers that cheap money would be readily available.

Quantitative Easing and Mortgage-Backed Securities Purchases

Beyond adjusting the benchmark interest rate, the Federal Reserve also reactivated and significantly expanded its quantitative easing (QE) program. This involved purchasing vast quantities of government bonds and, crucially for mortgage rates, mortgage-backed securities (MBS). Mortgage-backed securities are investment products that bundle together hundreds or thousands of individual home loans. By buying these securities, the Fed achieved several critical objectives. Firstly, it injected massive amounts of liquidity into the financial system, ensuring banks had ample funds to lend. Secondly, and more directly, by creating robust demand for MBS, the Fed effectively lowered their yields. Since the yield on MBS is closely tied to the interest rates offered on new mortgages, this direct intervention had a powerful downward pull on mortgage rates across the board. The Fed committed to purchasing “unlimited” amounts of MBS and Treasury bonds, a commitment that signaled an open-ended willingness to keep long-term interest rates low for as long as necessary to support economic stability. This unprecedented level of intervention provided a direct subsidy to the mortgage market, making home loans cheaper than ever.

Forward Guidance and Market Confidence

Another key component of the Fed’s strategy was “forward guidance.” Through public statements, press conferences, and economic projections, the Federal Reserve communicated its intention to keep interest rates low for an extended period, even after the economy began to recover. This commitment provided markets with a high degree of certainty about future monetary policy, influencing long-term interest rate expectations. When investors and lenders believe that short-term rates will remain low for years, they are more willing to lend at lower long-term rates today. This forward guidance helped to anchor mortgage rates at their historic lows, giving homeowners and prospective buyers confidence that these favorable borrowing conditions would persist.

Economic Uncertainty and Flight to Safety

While the Fed’s actions were the primary driver, the broader economic climate of intense uncertainty also played a significant, complementary role in pushing mortgage rates down.

Global Economic Downturn and Risk Aversion

The COVID-19 pandemic triggered an abrupt and severe global economic downturn. Lockdowns, supply chain disruptions, and widespread job losses created an environment of extreme risk aversion among investors. When the economic outlook is bleak and future earnings are uncertain, investors tend to shy away from riskier assets like stocks and corporate bonds. Instead, they seek “safe haven” investments – assets perceived to be very low risk, even if they offer modest returns.

Impact on Bond Yields

One of the most prominent safe haven assets is U.S. Treasury bonds. In times of crisis, there is a surge in demand for these government-backed securities, considered among the safest investments in the world. As demand for Treasuries soared in 2020, their prices went up, and consequently, their yields – which move inversely to prices – fell dramatically. Long-term mortgage rates are heavily influenced by the yield on the 10-year Treasury bond, serving as a benchmark for where the market prices long-term debt. As the 10-year Treasury yield plummeted to historic lows (even briefly dipping below 0.50% at one point), it naturally pulled fixed mortgage rates down with it. The combination of strong demand for safety and the Fed’s bond-buying spree created a powerful downward force on these critical benchmark yields.

Lender Dynamics and Market Factors

Even with the Fed’s aggressive posture and a flight to safety, the actual execution of low mortgage rates also depended on the capacity and behavior of individual lenders and the broader mortgage market.

Increased Demand for Refinancing

The sudden drop in rates unleashed an unprecedented wave of refinancing activity. Millions of homeowners seized the opportunity to lower their monthly payments, shorten their loan terms, or tap into accumulated home equity. This surge in demand created a highly competitive environment among mortgage lenders. While lenders were inundated with applications, the sheer volume meant they could still maintain profitability even with narrower margins on individual loans. The competition for market share among lenders contributed to keeping rates sharp, as each institution vied for a piece of the burgeoning refinance pie.

Mortgage Market Liquidity and Investor Appetite

Despite the initial shock to financial markets in early 2020, the mortgage market quickly stabilized, largely thanks to the Federal Reserve’s interventions. The Fed’s commitment to buying MBS ensured there was always a buyer for these securities, providing crucial liquidity to lenders. This allowed mortgage originators to confidently lend money knowing they could sell the loans into the secondary market. Furthermore, strong investor appetite for stable, government-backed assets like agency MBS (those guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae) persisted, further supporting liquidity. In a world of negative interest rates in some developed economies and volatile stock markets, U.S. mortgage-backed securities offered relatively attractive yields with the implicit or explicit backing of the U.S. government, making them appealing to a wide range of institutional investors.

Spreads and Profit Margins

While overall rates were low, there were moments in 2020 where the “spread” – the difference between mortgage rates and benchmark Treasury yields – actually widened. This widening often occurred when lenders were overwhelmed by application volume. They might slightly increase rates or add fees to manage their capacity, slowing down the influx of new business. Mortgage originators, facing staffing challenges and backlogs, sometimes priced loans higher to control demand and ensure they could process existing applications efficiently. However, these temporary increases were usually limited and did not derail the overall downward trend driven by the Fed and market fundamentals. As lenders adapted and hired more staff, spreads typically tightened again, allowing mortgage rates to reflect the underlying low-rate environment more closely.

The Broader Economic and Social Impact

The sustained period of ultra-low mortgage rates in 2020 had profound effects, both intended and unintended, on the U.S. economy and society.

Housing Market Boom and Affordability Concerns

Perhaps the most visible impact was on the housing market. Low mortgage rates drastically improved affordability for many, allowing buyers to purchase more expensive homes or obtain lower monthly payments. This fueled a surge in homebuyer demand, even amidst a pandemic. Coupled with already low inventory levels, this demand-side shock led to rapid home price appreciation across much of the country. While beneficial for existing homeowners who saw their equity grow, it simultaneously exacerbated affordability challenges for first-time buyers and those in lower income brackets, making homeownership seem more out of reach for some, despite the cheap financing.

Stimulating Economic Activity

The primary goal of the Fed’s actions was to stimulate economic activity. By making borrowing cheaper, the hope was to encourage both consumers and businesses to spend and invest, thereby supporting recovery from the pandemic-induced recession. Lower mortgage payments freed up disposable income for homeowners, potentially leading to increased consumption. Furthermore, a robust housing market has significant ripple effects throughout the economy, supporting industries from construction and real estate services to home furnishings and appliances, all contributing to job creation and GDP growth.

Wealth Creation and Disparities

The period of low rates significantly contributed to wealth creation for existing homeowners. Those who refinanced locked in lower payments and saved thousands over the life of their loans. Those who didn’t refinance still benefited from rising home equity. However, this wealth effect was not evenly distributed. Communities with lower homeownership rates or less access to credit did not benefit as much, potentially widening existing wealth disparities. The boom, while a boon for many, highlighted the uneven distribution of financial advantages in the economy.

Looking Back: A Unique Economic Moment

The conditions that led to historically low mortgage rates in 2020 were truly exceptional, marking a unique chapter in economic history.

The Unprecedented Nature of the 2020 Response

The speed and scale of the Federal Reserve’s intervention in 2020 were virtually unprecedented outside of major wars or the Great Depression. The use of quantitative easing on such a massive scale, combined with near-zero interest rates and explicit forward guidance, represented a powerful and coordinated effort to stabilize a rapidly deteriorating economy. This was not a typical economic downturn; it required an equally atypical response.

Long-Term Implications for Monetary Policy

The experience of 2020 provided valuable lessons for central banks regarding the effectiveness of unconventional monetary policies in extreme crises. While successful in preventing a deeper collapse and supporting recovery, it also initiated a period of extended low rates that contributed to inflation pressures later on, and highlighted the challenges of eventually unwinding such accommodative policies without disrupting markets. The strategies deployed in 2020 will likely be studied and debated by economists and policymakers for decades to come, shaping future responses to economic shocks.

In conclusion, the historically low mortgage rates of 2020 were a complex interplay of aggressive central bank intervention, a global flight to safety amidst unprecedented economic uncertainty, and the resulting dynamics of lender competition and market liquidity. While offering immense benefits to many homeowners and providing a crucial economic stimulus during a dark period, these rates also contributed to a red-hot housing market with long-term implications for affordability and wealth distribution. The year served as a powerful reminder of how interconnected global events, monetary policy, and individual financial decisions truly are.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.