In recent fiscal policy discussions, the proposal to eliminate federal income taxes on tipped wages has moved from a fringe idea to a central campaign pillar. While the concept of “No Tax on Tips” appears to be a straightforward win for service industry workers, its rejection or skepticism by various policymakers, including many Democrats and economic analysts, is rooted in complex financial theories and budgetary concerns. To understand why this proposal faces significant opposition, one must look past the populist appeal and examine the underlying impacts on the federal tax base, social safety nets, and the broader landscape of tax equity.

The debate is not merely political; it is a fundamental disagreement over how to best structure the American economy to support low-to-middle-income earners while maintaining a sustainable fiscal trajectory.

The Fiscal Impact of Eliminating Taxes on Tipped Income

The primary concern for any major change to the internal revenue code is the “price tag”—the total amount of federal revenue lost over a standard ten-year budget window. From a strictly financial perspective, removing taxes on tips creates a significant hole in the federal budget that must be accounted for through either spending cuts or increased borrowing.

Federal Revenue and the Budget Deficit

According to non-partisan groups like the Committee for a Responsible Federal Budget (CRFB), exempting tips from federal income and payroll taxes could reduce federal revenue by $150 billion to $250 billion over a decade. In an era of high interest rates and a mounting national debt, fiscal conservatives and budget-conscious Democrats alike express concern about further eroding the tax base. The loss of revenue isn’t just a number on a spreadsheet; it represents funds that would otherwise be allocated to infrastructure, education, or debt servicing. For many, the financial trade-off is seen as inefficient, as the benefits are concentrated in a specific sector rather than distributed across the entire low-wage workforce.

The Long-term Cost to Social Security and Medicare

One of the most nuanced financial arguments against the “No Tax on Tips” proposal involves the future solvency of social insurance programs. Social Security benefits are calculated based on a worker’s lifetime “covered earnings”—the income on which they paid payroll taxes. If tips are no longer considered taxable income, they may no longer be reported as part of the worker’s earnings history.

For a career server or bartender, this could lead to a significantly lower Social Security check upon retirement. Furthermore, the Medicare Trust Fund relies heavily on payroll tax contributions. By carving out a segment of the labor market and exempting their income from these taxes, the proposal could inadvertently hasten the insolvency of these critical financial safety nets, leaving the very workers it intends to help more vulnerable in their senior years.

Why Policy Experts Raise Concerns Over Tax Equity and Fairness

In the world of tax policy, “horizontal equity” is a gold standard. This principle suggests that individuals in similar economic circumstances should pay similar amounts in taxes. The “No Tax on Tips” proposal creates a sharp departure from this principle, creating winners and losers based on the type of work performed rather than the amount of money earned.

The Disparity Between Tipped and Non-Tipped Low-Wage Earners

Consider two workers: one is a server at a high-end restaurant who earns $40,000 a year, including $20,000 in tips. The other is a warehouse worker or a retail clerk who earns $40,000 in straight hourly wages. Under a “No Tax on Tips” regime, the server would pay significantly less in taxes than the warehouse worker, despite having the exact same gross income.

This creates a financial distortion in the labor market. From a personal finance perspective, it incentivizes workers to flock to tipped positions, potentially leaving other essential low-wage sectors—like childcare, elder care, and logistics—with even greater labor shortages. Critics argue that tax policy should not pick “favorite” industries, but should instead provide broad relief through mechanisms like the standard deduction or adjusted tax brackets.

Potential for Tax Sheltering and Corporate Loopholes

One of the most significant risks highlighted by financial analysts is the potential for “income reclassification.” If tips become tax-free, there is a massive financial incentive for high earners to restructure their compensation. While the proposal is aimed at waiters and hair stylists, tax lawyers are notoriously adept at finding ways to exploit such exemptions.

Could a consultant “tip” their firm instead of paying a service fee? Could high-level executives receive a “discretionary tip” for performance instead of a taxable bonus? Without incredibly stringent (and difficult to enforce) regulations, this policy could become a “Trojan Horse” for tax avoidance among the wealthy, further draining the Treasury and shifting the tax burden onto those with traditional W-2 wages.

Operational Challenges for Businesses and the Financial Sector

Beyond the macro-economic impact, the practical application of a “No Tax on Tips” policy presents a logistical nightmare for small business owners and payroll departments. The financial infrastructure of the United States service industry is currently built around the reporting and withholding of tipped income.

Payroll Complexity and Compliance Issues

Currently, employers are required to track tips to ensure they are meeting minimum wage requirements via the “tip credit.” If tips are removed from the federal tax equation, the reporting requirements don’t necessarily disappear, but they become bifurcated. Payroll software would need to be entirely redesigned to handle income that is subject to state tax but not federal tax, or subject to one type of payroll tax but not another.

For small businesses, this increased administrative burden translates to higher accounting costs. Furthermore, it creates a new “audit frontier” for the IRS. Ensuring that reported tips are genuine and not a way to hide under-the-table wages would require a level of oversight that could lead to more frequent and intrusive audits for small business owners in the hospitality sector.

The Impact on Consumer Behavior and Service Industry Pricing

From a business finance perspective, the proposal could lead to “tip inflation.” If employers know that tips are tax-free, they may feel empowered to lower base wages (where legal) or freeze wage growth, encouraging workers to rely even more heavily on customer generosity. This shifts the financial burden of labor costs from the business to the consumer.

Moreover, as “tip fatigue” grows among consumers, a policy that explicitly prioritizes tips could backfire. If customers feel that tipping has become a government-mandated tax-evasion scheme for the service industry, they may reduce their tipping percentages, ultimately leaving workers with less take-home pay than they had under the previous taxable system.

Alternative Financial Strategies for Supporting Service Workers

The opposition to “No Tax on Tips” is rarely an opposition to helping low-income workers; rather, it is often a preference for more stable and equitable financial mechanisms. Policy experts and many Democrats argue that there are more efficient ways to put money back into the pockets of the working class.

Raising the Minimum Wage vs. Tax Incentives

A common counter-proposal is the elimination of the “subminimum wage” for tipped workers and a significant increase in the federal minimum wage. Financially, this provides a more stable and predictable income for workers. Unlike tips, which fluctuate based on the day of the week, the weather, or a customer’s mood, a higher base wage ensures a consistent cash flow. This consistency is vital for workers trying to qualify for mortgages or auto loans, as lenders often view stable hourly wages more favorably than fluctuating tip income.

Expanding the Earned Income Tax Credit (EITC)

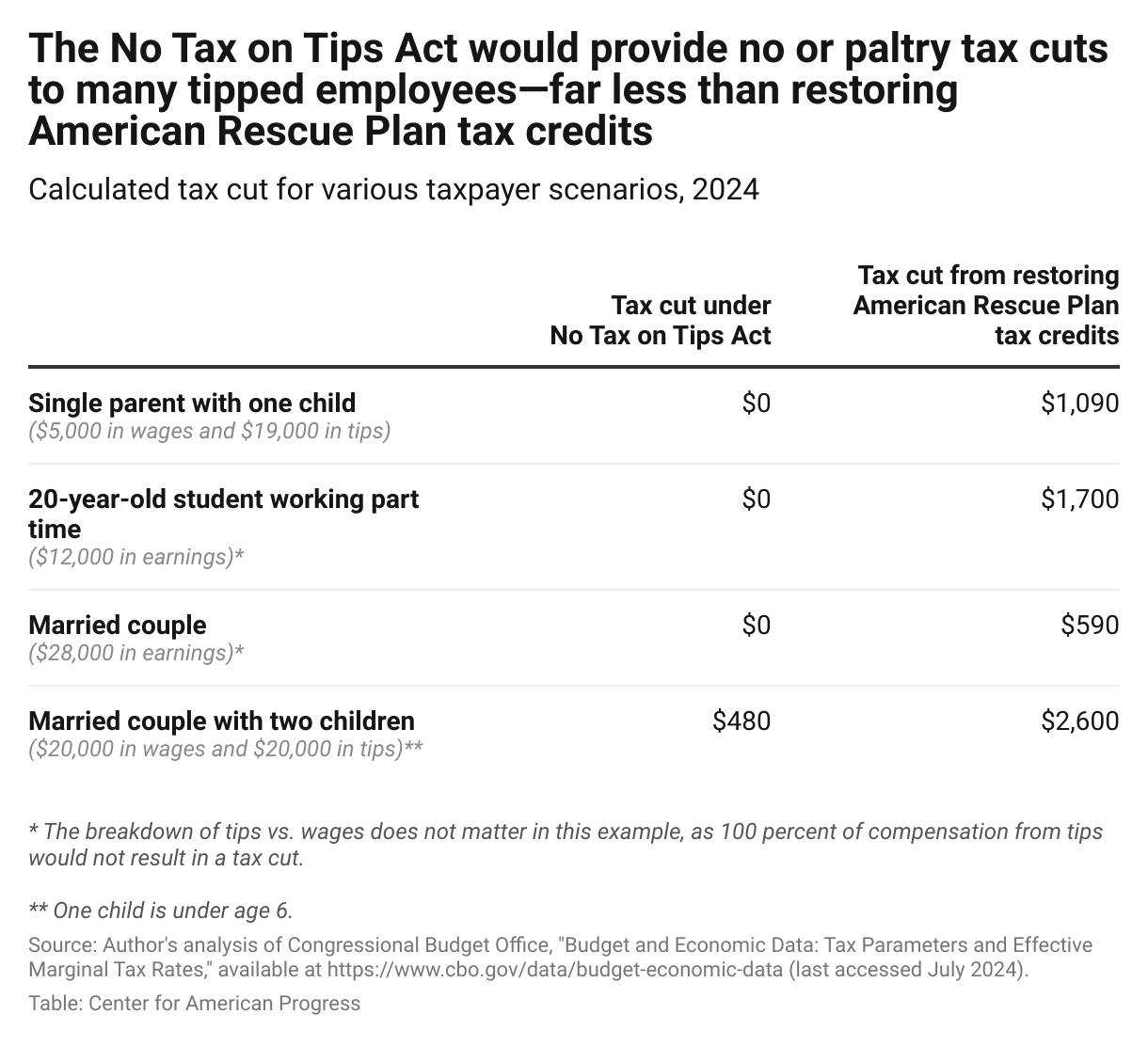

Another financial tool frequently cited is the Earned Income Tax Credit (EITC). Unlike a tip exemption, which only benefits those in specific roles, an expansion of the EITC provides a direct financial boost to all low-income households. The EITC is widely considered one of the most effective anti-poverty tools in the U.S. tax code because it encourages work and is “refundable,” meaning workers can receive money back even if they owe $0 in taxes. From a policy standpoint, expanding the EITC is seen as a “cleaner” financial move that avoids the distortionary effects and loophole risks associated with exempting tips.

Conclusion: The Financial Future of the Service Economy

While “No Tax on Tips” is a compelling slogan that addresses the immediate financial pressures felt by millions of Americans, the reasons for voting against or opposing it are grounded in a desire for fiscal stability and tax fairness. The financial reality is that such a policy could weaken the social safety net, create vast inequities between different types of low-wage labor, and open the door for significant tax avoidance by those at the top of the income bracket.

For the service industry worker, the most effective path toward financial security likely involves a combination of higher base wages, a robust social safety net, and broad-based tax relief that doesn’t depend on the whims of a customer’s tipping habits. As the debate continues, the focus must remain on creating a tax system that is both simple to navigate and equitable for every person who collects a paycheck, regardless of whether that check comes in the form of an hourly wage or a gratuity left on a table.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.