The dream of homeownership has long been a cornerstone of personal financial stability. However, over the past few years, prospective buyers have faced a starkly different reality than those who purchased homes during the previous decade. The era of the 3% mortgage is, for the foreseeable future, a relic of the past. Today’s borrowers are grappling with rates that have reached levels not seen in two decades, fundamentally altering the landscape of personal finance and real estate investment.

To understand why mortgage rates are so high, one must look beyond the local real estate office and into the complex machinery of global economics, central bank policy, and the inner workings of the bond market. While high rates can feel like a personal obstacle, they are the result of deliberate systemic shifts intended to stabilize a volatile economy.

1. The Federal Reserve and the Battle Against Inflation

The most direct influence on the upward trajectory of mortgage rates is the Federal Reserve’s monetary policy. While the Fed does not “set” mortgage rates, its control over the federal funds rate creates a ripple effect that dictates the cost of borrowing across the entire financial spectrum.

The Mandate to Combat Inflation

Following the global pandemic, a combination of supply chain disruptions, massive fiscal stimulus, and pent-up consumer demand led to the highest inflation rates in forty years. When the prices of goods and services rise too quickly, the purchasing power of the dollar erodes. To cool the economy and bring inflation back down to its 2% target, the Federal Reserve began a series of aggressive interest rate hikes. By making it more expensive for banks to borrow money, the Fed successfully throttled the flow of cheap capital, which naturally forced mortgage lenders to raise their own rates to maintain profitability.

The Shift from Quantitative Easing to Quantitative Tightening

During the 2008 financial crisis and again during the 2020 pandemic, the Federal Reserve engaged in “Quantitative Easing” (QE). This involved the central bank buying trillions of dollars in government bonds and mortgage-backed securities (MBS). This massive demand kept interest rates artificially low. Recently, the Fed shifted to “Quantitative Tightening” (QT), allowing these assets to roll off its balance sheet without replacing them. With the Fed no longer acting as a primary buyer, the supply of mortgage-backed securities in the open market has increased, causing prices to drop and yields—and consequently mortgage rates—to rise.

The Psychological Impact on Lenders

Mortgage lenders are not just looking at the current federal funds rate; they are looking at where the Fed expects to be in six months or two years. If the Federal Reserve signals that it will keep rates “higher for longer” to ensure inflation is fully extinguished, lenders price that expectation into their current mortgage offerings. This forward-looking sentiment is a primary reason why mortgage rates often climb even before the Fed officially announces a rate hike.

2. The Influence of the 10-Year Treasury Yield

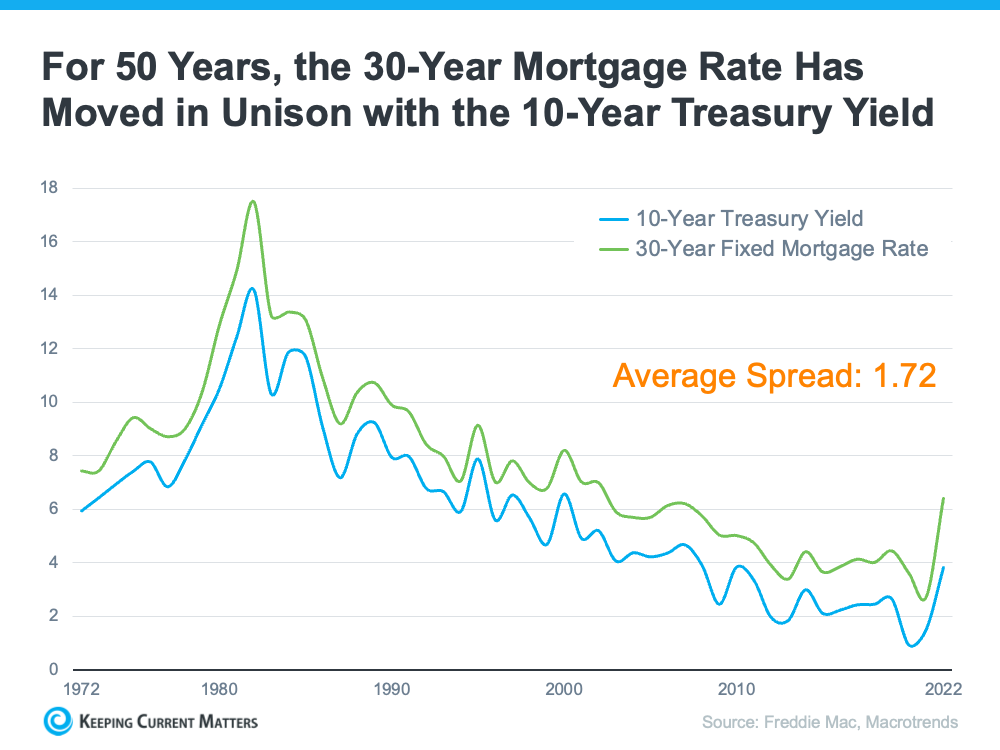

In the world of personal finance, there is no stronger correlation than the one between the 30-year fixed-rate mortgage and the yield on the 10-year U.S. Treasury note. While they are different financial instruments, they compete for the same type of investor.

Why Mortgages Follow Bonds

Investors who want “safe” long-term returns usually look at government bonds. Because a 30-year mortgage is also a long-term debt instrument, investors view it as an alternative to the 10-year Treasury bond (most mortgages are paid off or refinanced within 10 years, making the 10-year Treasury a better benchmark than the 30-year Treasury). To attract investors to buy mortgage debt instead of “risk-free” government debt, mortgage rates must offer a higher yield to compensate for the additional risk. As the yield on the 10-year Treasury rises due to economic uncertainty or high government spending, mortgage rates must follow suit to remain competitive.

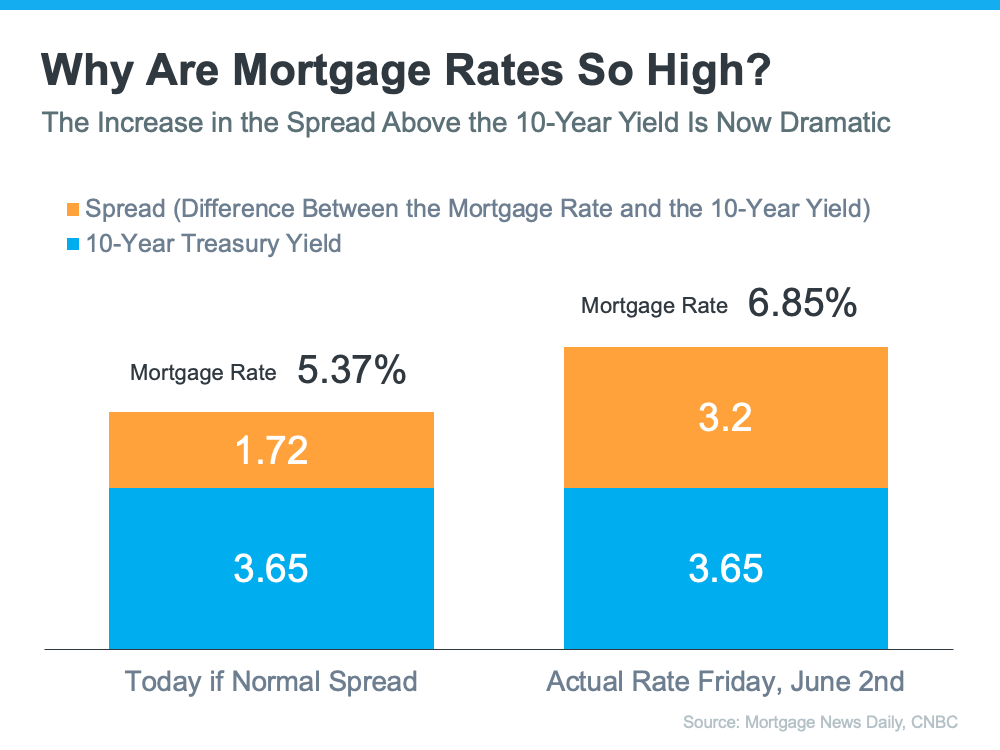

The Concept of the “Spread”

The “spread” is the difference between the 10-year Treasury yield and the 30-year fixed mortgage rate. Historically, this spread has hovered around 1.5 to 2 percentage points. However, in recent years, this spread has widened significantly, often exceeding 3 percentage points. This widening occurs when there is high volatility in the market. Lenders are unsure about future interest rate paths, so they add a “risk premium” to the rates they offer consumers. This explains why mortgage rates can remain stubbornly high even on days when Treasury yields might take a slight dip.

Global Demand for U.S. Debt

The U.S. Treasury market is global. When other countries’ central banks raise their own interest rates, or when foreign investors find better returns elsewhere, the demand for U.S. Treasuries may fluctuate. If demand for U.S. debt falls, the government must offer higher interest rates to attract buyers. These higher rates on government debt create a baseline that pushes all other consumer interest rates—including mortgages—higher.

3. The Secondary Market and Mortgage-Backed Securities (MBS)

To understand the cost of a mortgage, one must understand that your local bank rarely keeps your loan on its books for the full 30 years. Instead, loans are packaged into Mortgage-Backed Securities (MBS) and sold to investors on Wall Street.

Investor Appetite for Risk and Return

The price of an MBS is determined by how much investors are willing to pay for the stream of interest payments the mortgage generates. When inflation is high, the “fixed” return of a mortgage becomes less attractive because the future dollars paid back will have less purchasing power. To make these securities attractive to institutional investors (like pension funds and insurance companies), the interest rates on the underlying mortgages must be high enough to outperform inflation and account for the risk of default.

The Prepayment Risk Factor

When interest rates are volatile, investors face “prepayment risk.” If rates were to drop suddenly, many homeowners would refinance, paying off their high-interest loans early. This is bad for investors who wanted to collect high interest for years. To compensate for the possibility that the loan might be “called” or refinanced away, investors demand a higher initial interest rate. This uncertainty in the secondary market directly translates to higher costs for the individual homebuyer.

Liquidity Constraints in the Housing Market

The secondary market thrives on liquidity—the ease with which securities can be bought and sold. In a high-rate environment, the volume of new mortgages being issued drops significantly. This lower volume can lead to “thin” trading in the MBS market, which increases volatility. Higher volatility leads to higher yields, creating a cycle where high rates contribute to further rate increases by making the market less efficient.

4. Strategies for Navigating a High-Rate Environment

While the macroeconomic forces driving rates are outside the control of the individual, there are several financial strategies that savvy investors and prospective homeowners can use to mitigate the impact of high borrowing costs.

Prioritizing Credit Health and Loan-to-Value Ratios

In a low-rate environment, the difference between a “good” and “excellent” credit score might only be a fraction of a percent. In a high-rate environment, that gap widens. Lenders become much more conservative when capital is expensive. Focusing on debt-to-income (DTI) ratios and maximizing credit scores can help a borrower move from a “standard” rate to the “prime” rate, saving tens of thousands of dollars over the life of the loan.

Exploring Alternative Loan Products

The 30-year fixed-rate mortgage is the gold standard for stability, but it is also the most expensive during rate peaks. Some borrowers are turning toward Adjustable-Rate Mortgages (ARMs), which offer a lower introductory rate for 5, 7, or 10 years. The logic here is a financial bet: that rates will decrease in the future, allowing the borrower to refinance into a fixed-rate loan before the ARM adjusts upward. Additionally, “buydowns”—where the seller or buyer pays an upfront fee to lower the interest rate for the first few years—have become a popular tool in contract negotiations.

The Role of Larger Down Payments

In an era of 3% rates, the opportunity cost of putting more money down on a house was high; that cash could often earn more in the stock market. At 7% or 8%, the math changes. Putting more money down reduces the principal balance and the total interest paid, effectively providing a “guaranteed return” equal to the mortgage rate. For those with the capital, increasing the down payment is one of the most effective ways to combat the erosion of purchasing power caused by high rates.

The Long-Term Financial Outlook

The current high-rate environment is a stark reminder that the “cheap money” era of the 2010s was the exception, not the rule. Historically, mortgage rates have often hovered in the 6% to 8% range. While the transition from record-low rates to current levels has been painful for the housing market, it represents a “normalization” of the financial system.

High mortgage rates are a tool being used to rebalance an overheated economy. By slowing down the housing market, the Federal Reserve aims to reduce the “wealth effect” that fuels inflation, eventually leading to a more stable price environment for all goods and services. For the individual, the key to navigating this period lies in disciplined financial planning, a deep understanding of market indicators like the 10-year Treasury, and the patience to wait for the eventual stabilization of the spread between government debt and consumer loans. Understanding why rates are high doesn’t lower the monthly payment, but it does empower the consumer to make more informed, strategic decisions in a complex financial world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.