In the complex landscape of personal finance, insurance stands as a fundamental pillar of protection, safeguarding individuals and families against unforeseen financial setbacks. From auto accidents and home damage to medical emergencies and premature death, insurance policies provide a crucial safety net. However, the cost of these essential protections can represent a significant portion of a household’s budget, leading many to ask the perennial question: “Who has the cheapest insurance?”

The pursuit of the most affordable insurance is a savvy financial goal, but it’s important to understand that “cheapest” doesn’t always equate to “best value.” The true aim is to find comprehensive coverage at the most competitive price, ensuring adequate protection without overspending. This guide delves into the intricate world of insurance pricing, offering actionable strategies and insights to help you navigate the market, identify cost-saving opportunities, and ultimately secure the coverage you need at a price you can afford, all while remaining firmly within the domain of personal finance and money management.

Understanding the Fundamentals of Insurance Pricing

Before embarking on the quest for the cheapest insurance, it’s crucial to grasp the underlying factors that insurers use to determine premiums. Insurance is, at its core, an assessment of risk. The higher the perceived risk you present, the higher your premium will likely be. Understanding these variables empowers you to take steps that can potentially lower your costs.

Personal Demographics and Risk Profiles

Your personal profile is a significant determinant of your insurance rates. For auto insurance, factors like age, driving record, gender (in some states), marital status, and even credit score (where permitted by law) play a role. Younger, less experienced drivers typically face higher premiums, as do those with a history of accidents or traffic violations. Similarly, for health insurance, age, location, and health status are key, while life insurance premiums are heavily influenced by age, health, lifestyle, and family medical history. Insurers use vast actuarial data to correlate these demographic points with the likelihood of a claim. Maintaining a clean record, managing your health, and even improving your credit score can, over time, positively impact your rates.

Coverage Levels and Deductibles

The extent of your coverage directly impacts your premium. Generally, more extensive coverage—such as full coverage auto insurance versus liability-only, or a health plan with a broader network and lower out-of-pocket maximums—will cost more. The deductible, which is the amount you pay out-of-pocket before your insurance coverage kicks in, is another critical factor. Opting for a higher deductible typically results in a lower premium, as you are agreeing to bear a larger initial financial responsibility in the event of a claim. This is a strategic decision that requires careful consideration: while a higher deductible saves money upfront, it necessitates having sufficient savings to cover that amount if a claim arises.

Vehicle Type, Property Characteristics, or Health Status

Specific assets or personal health conditions also influence pricing. For auto insurance, the make, model, year, safety features, and even the theft rate of your vehicle can affect your premium. A luxury sports car will almost always cost more to insure than an older, safer sedan. For homeowners insurance, factors like the age and construction of your home, its proximity to fire hydrants and fire stations, crime rates in your neighborhood, and specific protective measures (e.g., alarm systems, storm shutters) are all considered. In health insurance, pre-existing conditions and the overall health of the applicant are central to pricing, though regulations under the Affordable Care Act have significantly altered how these are factored for individual and small group plans.

Location, Location, Location

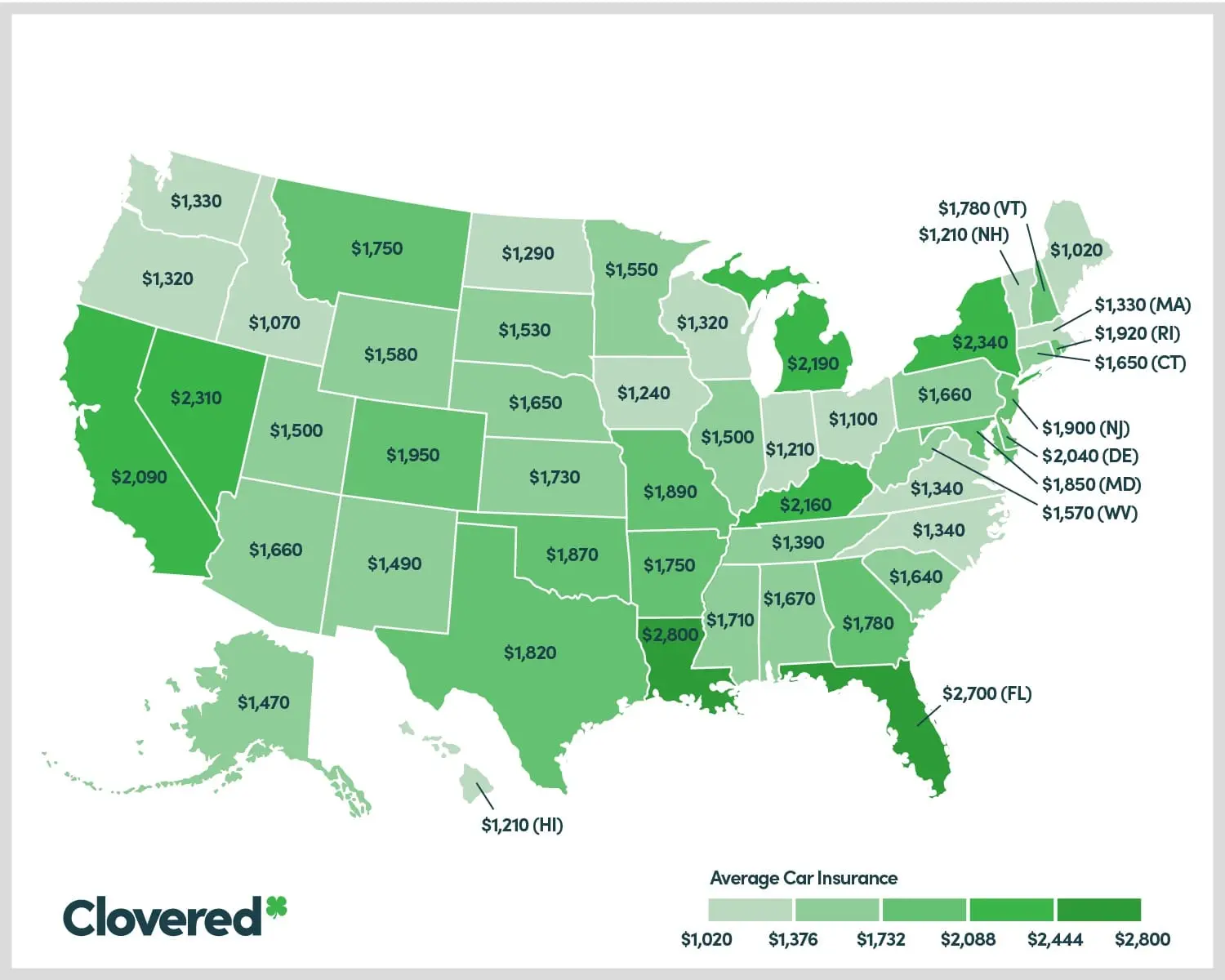

Where you live can have a profound impact on your insurance costs across nearly all types of policies. For auto insurance, urban areas with higher traffic density, crime rates, and greater likelihood of accidents often have higher premiums than rural areas. Similarly, homeowners insurance rates vary significantly by region, driven by factors such as susceptibility to natural disasters (hurricanes, earthquakes, wildfires), crime rates, and the cost of repairs in that specific area. Even health insurance premiums can differ based on geographical location, reflecting variations in healthcare costs and competition among providers.

Strategies for Finding the Most Affordable Insurance

While some pricing factors are beyond your immediate control, numerous actionable strategies can help you significantly reduce your insurance costs without compromising essential protection. The key lies in being proactive, informed, and diligent in your search.

Comparison Shopping: The Power of Multiple Quotes

This is arguably the single most effective strategy for finding the cheapest insurance. Insurers use proprietary algorithms and varying risk assessments, meaning the same coverage can have wildly different prices from one provider to another. Don’t settle for the first quote you receive. Obtain quotes from at least three to five different insurance companies, including national carriers, regional providers, and even lesser-known online insurers. Utilize online comparison websites, which can quickly generate multiple quotes, but also consider contacting independent insurance agents who can shop around on your behalf with various carriers. This simple act of comparison shopping can often reveal savings of hundreds, if not thousands, of dollars annually.

Bundling Policies for Discounts

Many insurance companies offer significant discounts when you purchase multiple policies from them. This is often referred to as a “multi-policy discount” or “bundling.” For example, combining your auto and homeowners insurance with the same provider can lead to substantial savings on both premiums. Some insurers also offer discounts for bundling auto with renters, life, or even umbrella policies. Always inquire about bundling options and compare the bundled price against individual policies from different carriers, as sometimes a seemingly good bundle might still be more expensive than separate policies from different “cheapest” providers.

Leveraging Discounts: From Good Driver to Multi-Policy

Beyond bundling, a myriad of other discounts are available, and it pays to ask your agent or review your policy details carefully. Common discounts include:

- Good Driver/Accident-Free: For those with a clean driving record over several years.

- Good Student: For young drivers who maintain a certain GPA.

- Defensive Driving Course: Completing an approved safety course can often lower auto premiums.

- Anti-Theft Devices: For vehicles equipped with alarms or tracking systems.

- Safety Features: Cars with advanced safety features (e.g., automatic emergency braking, lane-keeping assist).

- Home Security Systems: For homes with monitored alarms or sprinkler systems.

- Loyalty/Longevity: For remaining with the same insurer for an extended period.

- Payment Options: Discounts for paying premiums annually or setting up automatic payments.

- Low Mileage: For drivers who don’t drive frequently.

- Occupational/Affinity Group: Some employers, professional organizations, or alumni associations partner with insurers for group discounts.

Always ask your insurance provider for a comprehensive list of all available discounts and ensure you are taking advantage of every one for which you qualify.

Optimizing Your Coverage: When Less Can Be More (Carefully)

While never advisable to skimp on essential coverage, there are instances where optimizing your policy can lead to savings.

- Increasing Your Deductible: As discussed, a higher deductible lowers your premium. If you have a robust emergency fund, taking on more initial risk can be a smart financial move.

- Dropping Unnecessary Coverage: For older vehicles with low market value, collision and comprehensive coverage might become economically impractical. If your car is only worth a few thousand dollars, paying hundreds in premiums for collision might not make sense, especially if your deductible is high.

- Reviewing Life Insurance Needs: Life insurance requirements change over time. As your children become independent or your mortgage is paid off, you might need less coverage, allowing you to opt for a less expensive policy or term.

- Adjusting Health Plan Tiers: For health insurance, carefully assess your typical medical usage. If you are generally healthy, a higher-deductible health plan (HDHP) coupled with a Health Savings Account (HSA) can offer significant premium savings and tax advantages, though it requires readiness for higher out-of-pocket costs if serious illness strikes.

This optimization must be approached with caution. The goal is to reduce cost without exposing yourself to catastrophic financial risk. Always ensure you retain adequate coverage for genuine “what if” scenarios.

Navigating Different Types of Insurance

The search for the “cheapest” insurance requires a nuanced approach, as specific considerations apply to different types of policies.

Auto Insurance: Driving Down Costs

Beyond comparison shopping and discounts, consider your driving habits. Maintaining a clean driving record is paramount. Some insurers offer telematics programs (usage-based insurance) where a device in your car or a smartphone app monitors your driving behavior (speed, braking, mileage). Safe drivers can receive substantial discounts through these programs. Also, if you work from home or have a short commute, inquire about low-mileage discounts.

Homeowners/Renters Insurance: Protecting Your Dwelling Affordably

For homeowners, improvements that mitigate risk, such as upgrading an old roof, installing impact-resistant windows, or reinforcing your home against specific natural disasters, can lead to lower premiums. Renters insurance is often very inexpensive, but essential for protecting personal belongings. Don’t overlook this crucial coverage, especially as it frequently qualifies for bundling discounts.

Health Insurance: Decoding Affordability in Healthcare

The landscape of health insurance affordability is complex, heavily influenced by government regulations. Explore options through the Affordable Care Act (ACA) marketplace, where you may qualify for subsidies (premium tax credits) based on your income, making comprehensive plans significantly more affordable. Consider different plan types (HMO, PPO, EPO, POS) and metallic tiers (Bronze, Silver, Gold, Platinum) based on your health needs and financial situation. For those who are generally healthy, high-deductible health plans with an HSA can be a cost-effective choice due to lower premiums and tax benefits.

Life Insurance: Securing Futures Without Breaking the Bank

Term life insurance is generally the most affordable option, providing coverage for a specific period (e.g., 10, 20, 30 years). It offers a straightforward death benefit without complex cash value components, making it ideal for covering specific financial obligations like a mortgage or providing for dependents during their formative years. Whole life or universal life policies are significantly more expensive due to their savings/investment components and lifelong coverage. Prioritize term life for pure protection needs if affordability is a primary concern. The younger and healthier you are when you purchase, the lower your premiums will be.

The Long-Term Perspective: Beyond Just “Cheapest”

While finding the cheapest premium is a commendable financial goal, it’s vital to consider the broader picture. Insurance is a long-term commitment, and the true value of a policy often extends beyond its price tag.

The Importance of Insurer Reliability and Customer Service

A low premium is meaningless if your insurer is unreliable when it comes time to file a claim. Research an insurer’s financial strength ratings from agencies like A.M. Best or Standard & Poor’s. Check customer reviews and complaint ratios with organizations like the National Association of Insurance Commissioners (NAIC) or the Better Business Bureau. A company with a strong reputation for fair claim handling and excellent customer service might be worth a slightly higher premium. The stress of a major loss is compounded if your insurance company is unresponsive or difficult to work with.

Regular Policy Reviews and Adjustments

Your life changes, and so should your insurance. Annually review all your policies to ensure your coverage still meets your needs and that you’re getting the best possible rates. A new car, a home renovation, a marriage, or a new job could all warrant a policy adjustment. Don’t wait for renewal notices; be proactive. A simple phone call to your agent or a quick online comparison can unveil new discounts or better rates.

Understanding Policy Exclusions and Limitations

Always read the fine print. The cheapest policy might come with significant exclusions or limitations that could leave you vulnerable. For example, a homeowners policy might exclude flood or earthquake damage, requiring separate policies. A health plan might have a very restricted network of doctors. Ensure you fully understand what is and isn’t covered, and don’t assume broad protection based solely on a low premium. Clarity on coverage is a cornerstone of responsible financial planning.

Leveraging Financial Tools and Resources

The digital age has revolutionized the process of finding and comparing insurance, providing consumers with powerful tools to make informed decisions.

Online Comparison Websites and Aggregators

Websites like Policygenius, Insurify, or The Zebra allow you to enter your information once and receive multiple quotes from various carriers almost instantly. While these tools are incredibly convenient, remember that they might not include every insurer, especially smaller regional ones. Use them as a starting point, but consider supplementary research.

Independent Insurance Agents: Your Personal Shoppers

Unlike captive agents who work for a single insurance company, independent agents work with multiple carriers. They can shop around on your behalf, providing unbiased recommendations and helping you compare different policies and discounts. They can also offer personalized advice, explain complex policy terms, and assist with the claims process. Their expertise can be invaluable, especially for complex insurance needs.

Financial Planners and Advisors

For those with more intricate financial situations, a certified financial planner can integrate your insurance strategy into your broader financial plan. They can help assess your overall risk tolerance, identify potential coverage gaps, and recommend optimal insurance solutions that align with your long-term financial goals and budget.

In conclusion, finding the “cheapest” insurance is not about blindly picking the lowest number. It’s about a strategic, informed approach to personal finance that balances cost with adequate protection. By understanding pricing factors, actively seeking out discounts, regularly reviewing your policies, and leveraging available resources, you can confidently navigate the insurance market and secure the best value for your hard-earned money, ensuring your financial well-being is robustly protected.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.