Securing a home loan is a monumental financial decision, and for eligible service members, veterans, and surviving spouses, the VA home loan program offers unparalleled advantages. Among these, competitive interest rates frequently stand out as a primary benefit. However, the question of “who has the best VA home loan rates” isn’t straightforward, as rates are dynamic and influenced by a myriad of factors. This guide delves into understanding VA loan rates, navigating the lender landscape, and empowering borrowers to secure the most favorable terms for their unique financial situation.

Understanding the VA Home Loan Advantage

The VA home loan program, backed by the U.S. Department of Veterans Affairs, is designed to help eligible individuals achieve homeownership with significant benefits not typically available through conventional mortgages. At its core, the VA guarantees a portion of the loan, which substantially reduces the risk for lenders. This government backing is the foundation for many of the program’s attractive features.

Key benefits that directly or indirectly contribute to securing competitive rates include:

- No Down Payment Requirement: For most eligible borrowers, a down payment is not required, making homeownership accessible even without substantial savings.

- No Private Mortgage Insurance (PMI): Unlike conventional loans with less than a 20% down payment, VA loans do not require PMI, which can save borrowers hundreds of dollars per month and significantly reduce the overall cost of the loan over its lifetime.

- Competitive Interest Rates: Due to the VA guarantee, lenders face less risk, often enabling them to offer lower interest rates compared to conventional and even FHA loans. This is a cornerstone of the program’s financial appeal.

- Limited Closing Costs: The VA limits the closing costs lenders can charge to borrowers, further protecting the borrower’s finances.

- Assumability: VA loans can often be assumed by another eligible borrower, a unique feature that can be advantageous in certain market conditions.

While the VA sets the broad guidelines for these loans, it does not set the interest rates. Instead, individual lenders determine their own rates, leading to variations in what different institutions offer. This decentralization necessitates diligent research and comparison shopping to truly uncover the “best” rate available at any given time.

Decoding VA Loan Rates: What Influences Them?

Determining the “best” VA home loan rate is complex because the rate you receive is a product of both broad economic forces and specific factors related to the lender and your individual financial profile. Understanding these influences is crucial for strategic rate shopping.

Macroeconomic and Market Conditions

- Federal Reserve Policy: Actions by the Federal Reserve, particularly regarding the federal funds rate, influence broader interest rates across the economy, including mortgage rates. While the fed funds rate isn’t directly tied to mortgage rates, it impacts the cost of borrowing for banks, which in turn affects their lending rates.

- Inflation: Concerns about inflation often lead to higher interest rates as lenders seek to maintain the purchasing power of their returns.

- Economic Outlook: A strong economy can sometimes lead to higher rates as demand for money increases, while economic uncertainty might push rates down as investors seek the stability of government-backed securities.

- Mortgage-Backed Securities (MBS) Market: Mortgage rates are primarily driven by the performance of the MBS market. These are investments made up of thousands of mortgages, and their value fluctuates based on investor demand. Lenders sell their loans into this market, and its performance directly impacts the rates they offer.

Lender-Specific Factors

- Lender Overlays: While the VA sets minimum standards, individual lenders often impose stricter requirements, known as “overlays.” These can include higher credit score minimums or lower debt-to-income (DTI) ratio requirements. Lenders with stricter overlays might offer slightly lower rates because they perceive less risk.

- Profit Margins and Operational Costs: Every lender operates with different cost structures and profit objectives. A highly efficient lender might be able to offer more competitive rates than one with higher overhead.

- Volume and Specialization: Lenders who specialize in VA loans and process a high volume often have more streamlined operations and deep expertise, which can sometimes translate into better rates or a smoother process.

Borrower-Specific Factors

- Credit Score: A higher credit score signals lower risk to lenders, almost always resulting in access to lower interest rates. Lenders typically view scores above 740 as excellent.

- Debt-to-Income (DTI) Ratio: This ratio compares your monthly debt payments to your gross monthly income. A lower DTI indicates that you can more comfortably manage additional debt, making you a less risky borrower.

- Loan Term: A 15-year VA loan typically carries a lower interest rate than a 30-year VA loan because the lender’s money is returned more quickly.

- Discount Points: Borrowers can pay “discount points” upfront to “buy down” their interest rate. Each point usually costs 1% of the loan amount and can reduce the interest rate by a certain fraction, though the exact reduction varies by lender and market conditions.

- Property Type and Location: While less impactful for VA loans than conventional, certain property types or highly competitive markets can sometimes subtly influence rates or lender offerings.

Navigating the Lender Landscape for Optimal Rates

Finding the “best” VA loan rate isn’t about identifying a single, universally superior lender; it’s about identifying the best lender for you at a specific moment in time. The VA loan market is competitive, with a diverse array of lenders vying for your business.

Types of VA Lenders

- Large National Banks: These institutions often have vast resources, a wide array of loan products, and established brand recognition. They might offer competitive rates due to their high volume, but service can sometimes be less personalized.

- Dedicated VA Lenders/Mortgage Companies: Many companies specialize exclusively in VA loans or have robust VA loan departments. Their expertise often means a smoother process, knowledgeable loan officers, and highly competitive rates tailored for the VA market. They understand the nuances of VA eligibility and guidelines deeply.

- Credit Unions and Community Banks: These smaller, often locally focused institutions can sometimes offer personalized service and competitive rates, especially for their members. However, their VA loan volume might be lower, and their internal overlays could sometimes be stricter than national lenders.

- Mortgage Brokers: A mortgage broker doesn’t lend money themselves but acts as an intermediary, working with multiple lenders to find the best rate and terms for you. They can be invaluable for accessing a wide range of options without directly contacting each lender.

The Imperative of Shopping Around

The single most effective strategy for securing the best VA home loan rate is to shop around. Obtaining quotes from at least three to five different lenders on the same day is paramount. Even a slight difference in the interest rate can translate into thousands of dollars saved over the life of a 30-year mortgage.

When comparing offers:

- Get Personalized Loan Estimates: Don’t just rely on advertised rates or general quotes. Request an official Loan Estimate from each lender, which is a standardized form detailing the interest rate, monthly payment, closing costs, and other loan terms. This allows for a true “apples-to-apples” comparison.

- Ensure Consistent Information: Provide each lender with the exact same information (credit score estimate, loan amount, property value, etc.) to ensure the quotes are truly comparable.

- Focus on the APR, Not Just the Interest Rate: While the interest rate is critical, the Annual Percentage Rate (APR) provides a more comprehensive picture of the loan’s cost, as it includes certain fees and discount points in addition to the interest rate.

Strategies for Securing Your Best VA Loan Rate

Beyond simply shopping around, several proactive steps can significantly improve your chances of securing the lowest possible VA home loan rate.

Enhance Your Financial Profile

- Improve Your Credit Score: Prioritize paying bills on time, keeping credit utilization low, and addressing any errors on your credit report well in advance of applying. A higher score directly translates to lower perceived risk and better rates.

- Reduce Your Debt-to-Income (DTI) Ratio: Pay down existing debts, especially high-interest credit card balances. A lower DTI indicates greater financial stability and capacity to handle mortgage payments.

- Build Your Savings: While a down payment isn’t required for VA loans, having robust savings (reserves) can demonstrate financial strength to lenders, even if not directly reflected in the rate.

Understand Loan Options and Terms

- Consider Discount Points: Evaluate whether paying discount points to “buy down” your interest rate makes financial sense for your situation. If you plan to stay in the home for a long time, the long-term savings might outweigh the upfront cost. Calculate the “break-even point” to determine its value.

- Choose the Right Loan Term: A 15-year loan typically has a lower interest rate than a 30-year loan. While the monthly payments will be higher, the total interest paid over the life of the loan will be substantially less.

- Get Pre-Approved, Not Just Pre-Qualified: A pre-approval involves a more thorough review of your financial standing and provides a stronger indication of what you can borrow, often at a specific rate. This also strengthens your position when making an offer on a home.

Engage Effectively with Lenders

- Be Prepared: Have all necessary financial documents (pay stubs, tax returns, bank statements, Certificate of Eligibility) ready. A swift and organized application process can help lock in a favorable rate before market shifts.

- Ask About Rate Locks: Once you’ve found a rate you like, ask the lender about locking it in. Understand the lock period (e.g., 30, 45, 60 days) and any associated fees or conditions. A rate lock protects you if market rates rise during your home buying process.

- Leverage Lender Competition: Politely inform lenders that you are shopping around. This can sometimes encourage them to offer their most competitive terms to earn your business.

Beyond the Rate: Fees, Service, and the Full Picture

While the interest rate is undeniably a critical component, it’s not the sole factor in determining the overall cost and value of a VA home loan. A holistic perspective is essential for making the best financial decision.

Understanding the True Cost

- Annual Percentage Rate (APR): As mentioned, the APR provides a more accurate representation of the total cost of the loan by incorporating the interest rate along with certain fees and charges. Always compare APRs when evaluating loan offers.

- Closing Costs: These are fees paid at the closing of the loan. While VA loans limit certain closing costs for borrowers, others remain. These can include appraisal fees, title insurance, recording fees, and attorney fees. Ensure you understand all line items on your Loan Estimate.

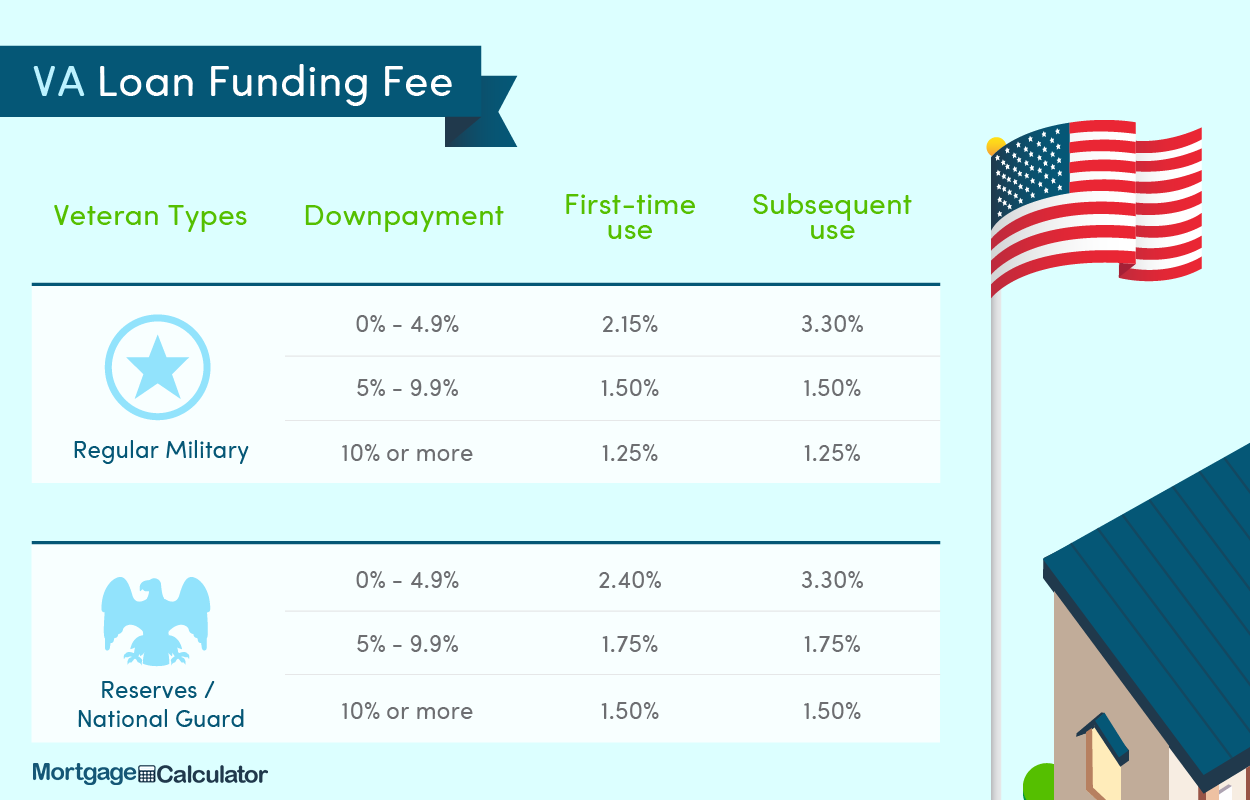

- VA Funding Fee: This is a one-time mandatory fee paid directly to the VA to help offset the cost of the program. It varies based on your service type, loan amount, and whether it’s your first time using the VA loan benefit. It can often be financed into the loan, increasing your total loan amount but not requiring cash upfront. Certain veterans (e.g., those receiving VA compensation for service-connected disabilities) are exempt from this fee.

- Escrow Accounts: Most VA loans require an escrow account for property taxes and homeowner’s insurance premiums. While not a loan fee, it impacts your monthly payment, so understanding its calculation is important.

The Value of Lender Service and Expertise

A slightly higher interest rate from a lender with exceptional service and deep VA expertise might be a better value than a rock-bottom rate from a slow, unresponsive, or inexperienced lender.

- Responsiveness and Communication: The home buying process can be stressful. A lender who communicates clearly, responds promptly to questions, and keeps you informed throughout the process can significantly reduce that stress.

- VA Loan Expertise: Lenders who specialize in VA loans are more likely to understand the unique aspects of the program, navigate potential complexities, and process your loan efficiently. Inexperienced lenders can cause delays or errors that jeopardize your home purchase.

- Transparency: A good lender will be transparent about all fees, terms, and conditions, ensuring there are no surprises at closing.

- Post-Closing Support: Consider what kind of support the lender offers after your loan closes. Will they be available for questions about your mortgage payments, escrow, or refinancing options down the line?

Ultimately, the “best” VA home loan rate comes from a combination of diligent preparation, strategic shopping, and selecting a lender that not only offers competitive terms but also provides the expertise and service necessary for a smooth and successful homeownership journey. By focusing on your financial profile, comparing comprehensive Loan Estimates, and considering the full package beyond just the interest rate, you can empower yourself to secure the most advantageous VA loan for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.