Every great business idea, no matter how revolutionary or impactful, faces a common hurdle: securing the necessary capital to transform vision into reality. The journey from a nascent concept to a thriving enterprise is almost invariably paved with financial needs, from seed funding for development to growth capital for scaling. Understanding who gives loans for great business ideas is not just about identifying potential lenders; it’s about navigating a complex financial ecosystem to find the perfect match for your specific venture, stage of growth, and risk profile. This article delves into the diverse landscape of funding sources, offering insights into how entrepreneurs can access the capital they need to build the next big thing.

Understanding the Landscape of Business Funding

The quest for business funding can feel like navigating a maze, with myriad options, each with its own set of requirements, benefits, and drawbacks. For an entrepreneur with a “great business idea,” the initial step is to comprehend this landscape, categorizing the types of financing available and identifying which might be most suitable.

The Entrepreneurial Dilemma: Idea vs. Capital

A brilliant idea is the cornerstone of any successful business, but it’s rarely enough on its own. Capital acts as the fuel, enabling research and development, market entry, operational scaling, and talent acquisition. Many promising ventures falter not due to a lack of innovation or market demand, but due to an inability to bridge the financial gap between conception and commercial viability. This dilemma underscores the critical importance of understanding where and how to secure loans and investments. Entrepreneurs often underestimate the time and effort required to raise capital, mistakenly believing that a compelling idea alone will attract investors. In reality, a well-structured plan, a clear articulation of market opportunity, and a solid financial projection are equally vital.

Beyond Traditional Banking: A Broader View

When most people think of business loans, traditional banks often come to mind first. While banks remain a significant source of funding, especially for established businesses, the funding landscape has dramatically expanded and diversified. Today, entrepreneurs have access to a rich tapestry of financial instruments and institutions, ranging from government-backed programs and online lenders to venture capitalists and crowdfunding platforms. This diversification means that even businesses that might not meet stringent traditional bank criteria can find viable funding pathways. The key is to look beyond the conventional and explore the full spectrum of options, understanding that each type of lender or investor has a unique appetite for risk, return expectations, and areas of focus.

Traditional Lenders: The Bedrock of Business Finance

For many years, traditional financial institutions like banks were the primary, if not sole, recourse for businesses seeking external capital. They remain a crucial component of the funding ecosystem, particularly for businesses with established track records or robust collateral.

Commercial Banks and Credit Unions

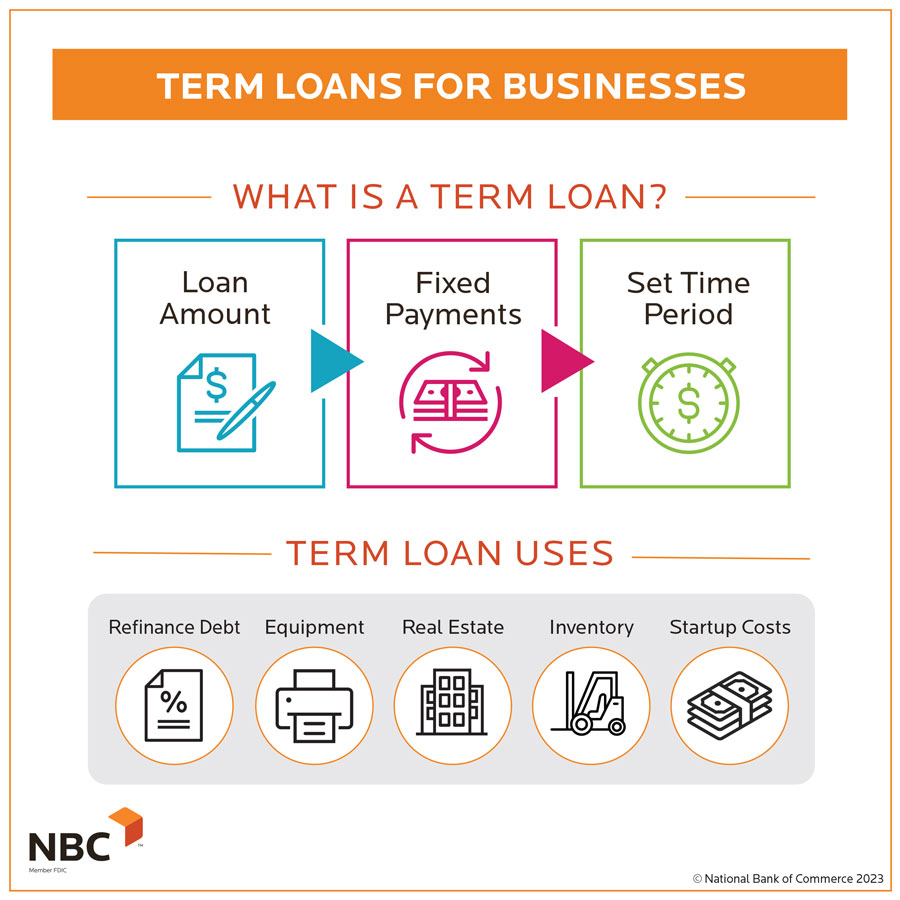

Commercial banks and credit unions offer a variety of loan products tailored for businesses, ranging from term loans for equipment purchases and real estate to lines of credit for working capital. These institutions typically prefer to lend to businesses with a proven operational history, strong credit scores, and sufficient collateral. Their lending decisions are often based on a thorough analysis of the business’s financial statements, cash flow projections, and the entrepreneur’s personal credit history. While the application process can be rigorous and time-consuming, the benefits include competitive interest rates, structured repayment schedules, and the opportunity to build a long-term banking relationship. Credit unions, often community-focused, may offer more flexible terms or a more personal touch, especially for smaller local businesses.

SBA-Backed Loans: Government Support for Small Businesses

The U.S. Small Business Administration (SBA) doesn’t lend money directly to businesses; instead, it guarantees a portion of loans made by commercial lenders, significantly reducing the risk for banks and making them more willing to lend to small businesses that might not otherwise qualify. SBA-backed loans, such as the popular 7(a) loan program and CDC/504 loans for major assets, are designed to stimulate economic growth by supporting small businesses. They often come with lower down payments, longer repayment terms, and competitive interest rates compared to conventional bank loans. Eligibility criteria focus on the business’s size, its ability to repay, and its purpose for the loan. These loans are an excellent option for startups and small businesses with great ideas but limited collateral or operating history, provided they meet the SBA’s specific requirements.

Advantages and Disadvantages of Traditional Loans

Advantages: Traditional loans typically offer lower interest rates, particularly for well-qualified borrowers, and predictable repayment schedules, making financial planning easier. They also help establish business credit, which is vital for future financing. The established nature of these institutions can provide a sense of security and legitimacy.

Disadvantages: The stringent eligibility requirements, often including collateral and a strong operating history, can be a significant barrier for startups and businesses with innovative but untested ideas. The application process can be lengthy, and rejection rates are relatively high for new or high-risk ventures. This makes them less accessible for early-stage “great business ideas” that are still proving their concept.

Alternative Funding Sources: Innovation in Capital Access

The digital revolution and evolving financial markets have given rise to a new generation of lenders and funding mechanisms, offering more flexible and often faster access to capital. These alternative sources are frequently better suited for startups and innovative business ideas that might not fit the traditional lending mold.

Online Lenders and Fintech Platforms

Online lenders have disrupted the traditional banking model by leveraging technology to streamline the loan application and approval process. Platforms like OnDeck, Kabbage (now part of American Express), and Funding Circle offer a range of products, including short-term loans, lines of credit, and merchant cash advances. Their appeal lies in speed and convenience: applications can often be completed online in minutes, with funding decisions made within hours or days. They typically have less stringent credit requirements than traditional banks, making them accessible to a broader spectrum of businesses, including those with limited operating history. However, this accessibility often comes with higher interest rates and shorter repayment periods, so it’s crucial for entrepreneurs to carefully evaluate the total cost of borrowing.

Peer-to-Peer (P2P) Lending

Peer-to-peer lending platforms connect individual investors directly with businesses seeking loans, bypassing traditional financial intermediaries. Platforms like Prosper and LendingClub allow multiple individuals to fund a portion of a business loan, diversifying risk for investors and potentially offering more favorable terms for borrowers. For businesses with great ideas but a lack of traditional collateral, P2P lending can be an attractive option, as lenders often consider the business’s potential and the entrepreneur’s story more heavily. The process can be quicker than traditional bank loans, and the terms can be more flexible, though interest rates vary widely based on the perceived risk of the borrower.

Microlenders: Empowering Underserved Entrepreneurs

Microlenders specialize in providing small loans (microloans) to entrepreneurs and small businesses, often those in underserved communities or those who struggle to access capital from traditional sources. Organizations like Kiva and Accion focus on economic empowerment, offering not just financial capital but also business training and support. These loans are typically small, ranging from a few hundred to tens of thousands of dollars, and are ideal for very early-stage startups, sole proprietorships, or businesses with innovative ideas that require minimal initial capital. Microlenders often have more lenient eligibility criteria and a mission-driven approach, making them a compassionate and accessible option for many aspiring entrepreneurs.

Equity-Based Funding: Sharing the Vision and the Risk

For high-growth potential businesses, particularly those in technology or with scalable models, equity-based funding offers significant capital in exchange for a share of ownership. This path is less about “loans” and more about “investment,” where investors become partners in the business’s success and risk.

Angel Investors: Mentorship and Money

Angel investors are affluent individuals who provide capital for business startups, usually in exchange for convertible debt or ownership equity. They are often experienced entrepreneurs or business executives who not only provide financial backing but also invaluable mentorship, industry contacts, and strategic guidance. Angel investors typically invest earlier than venture capital firms, often in seed or early-stage rounds, making them an ideal source for great business ideas that are still in their formative stages. Finding angel investors usually involves networking, referrals, and pitching at startup events. While they offer vital capital and expertise, entrepreneurs must be prepared to give up a portion of their company and navigate a potentially less formal investment process.

Venture Capital Firms: Fueling High-Growth Startups

Venture Capital (VC) firms manage funds raised from institutional investors and high-net-worth individuals, which they then invest in startups and small businesses with exceptional growth potential. VCs typically invest larger sums than angel investors and are looking for disruptive technologies, scalable business models, and significant market opportunities. They often take an active role in their portfolio companies, providing strategic direction, operational support, and access to a vast network. Securing VC funding is highly competitive, requiring a compelling business plan, a strong management team, a proven concept (even if early-stage), and a clear exit strategy for investors. For truly great, high-potential business ideas, VC funding can provide the immense capital needed to scale rapidly and dominate a market.

Crowdfunding: Leveraging the Power of the Crowd

Crowdfunding platforms allow businesses to raise money from a large number of individuals, typically via the internet. There are several models:

- Reward-based crowdfunding (e.g., Kickstarter, Indiegogo): Individuals pledge money in exchange for a product, service, or experience once the business successfully launches. This is excellent for validating market demand and securing pre-orders for innovative products.

- Equity crowdfunding (e.g., SeedInvest, StartEngine): Individuals invest in a company in exchange for equity, allowing everyday investors to participate in startup growth, traditionally reserved for accredited investors. This democratizes access to investment capital for entrepreneurs.

- Debt crowdfunding (e.g., Funding Circle for businesses): Similar to P2P lending, individuals lend money to a business with the expectation of repayment with interest.

Crowdfunding can be a powerful way to not only raise capital but also to build a community around a business idea, gain market validation, and generate early buzz. It’s particularly effective for consumer-facing products or services with a strong narrative.

Specialized Loans and Grants: Niche Opportunities

Beyond the general categories, there are specific funding mechanisms designed for particular assets, industries, or purposes, as well as non-repayable grants.

Equipment Financing and Invoice Factoring

- Equipment Financing: This type of loan is specifically used to purchase business equipment. The equipment itself often serves as collateral, making it easier to secure than general business loans. It’s ideal for businesses needing machinery, vehicles, or technology without tying up other assets.

- Invoice Factoring (Accounts Receivable Financing): Businesses sell their outstanding invoices (accounts receivable) to a third party (a “factor”) at a discount in exchange for immediate cash. This is not a loan but a way to improve cash flow by converting future receivables into present working capital. It’s particularly useful for businesses with long payment cycles or those needing quick access to funds.

Government Grants: Non-Dilutive Funding

Government agencies at federal, state, and local levels, as well as some foundations, offer grants to businesses and organizations pursuing specific objectives, such as research and development in critical sectors, promoting innovation, or addressing social challenges. Unlike loans or equity investments, grants do not require repayment or give up ownership. They are highly competitive and often have very specific criteria, but for businesses whose ideas align with a grant’s mission (e.g., green technology, medical breakthroughs, educational initiatives), they represent an invaluable source of non-dilutive funding.

Industry-Specific Funds and Programs

Many industries have specialized funds, accelerators, or incubators that provide capital, mentorship, and resources to startups within their niche. For example, biotech startups might access grants from NIH, while software companies might find support from tech accelerators. These programs often come with robust networks and expert guidance, making them highly attractive for businesses operating in specialized fields. It requires diligent research to identify such opportunities relevant to a particular business idea.

Preparing Your Business for Funding: The Investor’s Perspective

Regardless of the source, securing funding for a great business idea requires meticulous preparation and a deep understanding of what lenders and investors are looking for.

Developing a Robust Business Plan

A comprehensive business plan is the cornerstone of any funding application. It should clearly articulate your business concept, market analysis, competitive landscape, operational strategy, management team, and financial projections. This document serves as your blueprint, demonstrating the viability and potential of your idea. Lenders and investors use it to assess risk, potential returns, and your capability as an entrepreneur. A great idea needs a great plan to convince others of its potential.

Understanding Your Financial Projections

Beyond historical financial data (if available), future financial projections are critical. This includes detailed forecasts for revenue, expenses, cash flow, and profitability. These projections should be realistic, well-substantiated, and demonstrate a clear path to profitability and return on investment for equity investors or repayment capacity for lenders. Be prepared to defend your assumptions and show sensitivity analysis for various scenarios.

Building a Strong Pitch and a Competent Team

Finally, a great business idea needs to be effectively communicated. Develop a compelling pitch that succinctly explains your vision, market opportunity, solution, and team. Investors invest in people as much as ideas. A strong, experienced, and passionate management team instills confidence that the business can execute its plan and overcome challenges. Highlight the expertise and track record of your key personnel, demonstrating that your team has what it takes to turn a great idea into a resounding success.

In conclusion, “who give loans for great business ideas” is not a singular entity but a vibrant, multifaceted ecosystem of financial players. From traditional banks and government-backed programs to innovative online lenders, angel investors, venture capitalists, and the power of the crowd, entrepreneurs today have an unprecedented array of options. The key to unlocking this capital lies in thorough preparation, strategic alignment with the right funding source, and a compelling articulation of your business’s potential. With the right approach, even the most ambitious business ideas can secure the financing needed to flourish and transform the future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.