Choosing the right tax preparation software is more than just selecting a tool; it’s a strategic financial decision that can significantly impact your annual tax outcome. For millions, TurboTax stands out as a popular choice, offering a range of versions designed to cater to diverse financial situations. However, with multiple options, pinpointing “which version of TurboTax do I need” can feel like navigating a maze. This article will guide you through the financial considerations necessary to make an informed choice, ensuring you optimize your deductions, comply with tax laws, and achieve financial peace of mind.

Understanding Your Tax Landscape: The Foundation of Choice

Before diving into TurboTax’s specific offerings, the most crucial first step is to accurately assess your own financial landscape. Your income sources, deductions, credits, and overall financial complexity are the primary drivers in determining the ideal software version for your needs.

Basic Filers: Simplicity for W-2 Employees

Many individuals fall into the category of “basic filers.” This typically includes:

- Individuals or couples filing jointly with primarily W-2 income: Your employer reports your wages and withheld taxes on a W-2 form.

- Taking the standard deduction: You don’t have enough itemized deductions (like mortgage interest or significant medical expenses) to exceed the standard deduction threshold.

- No complex investment income: Your financial activities are limited to basic savings interest (reported on a 1099-INT) or perhaps a few simple dividends (1099-DIV).

- No self-employment income or business expenses: You don’t run a side hustle, freelance, or own a small business that generates 1099-NEC income.

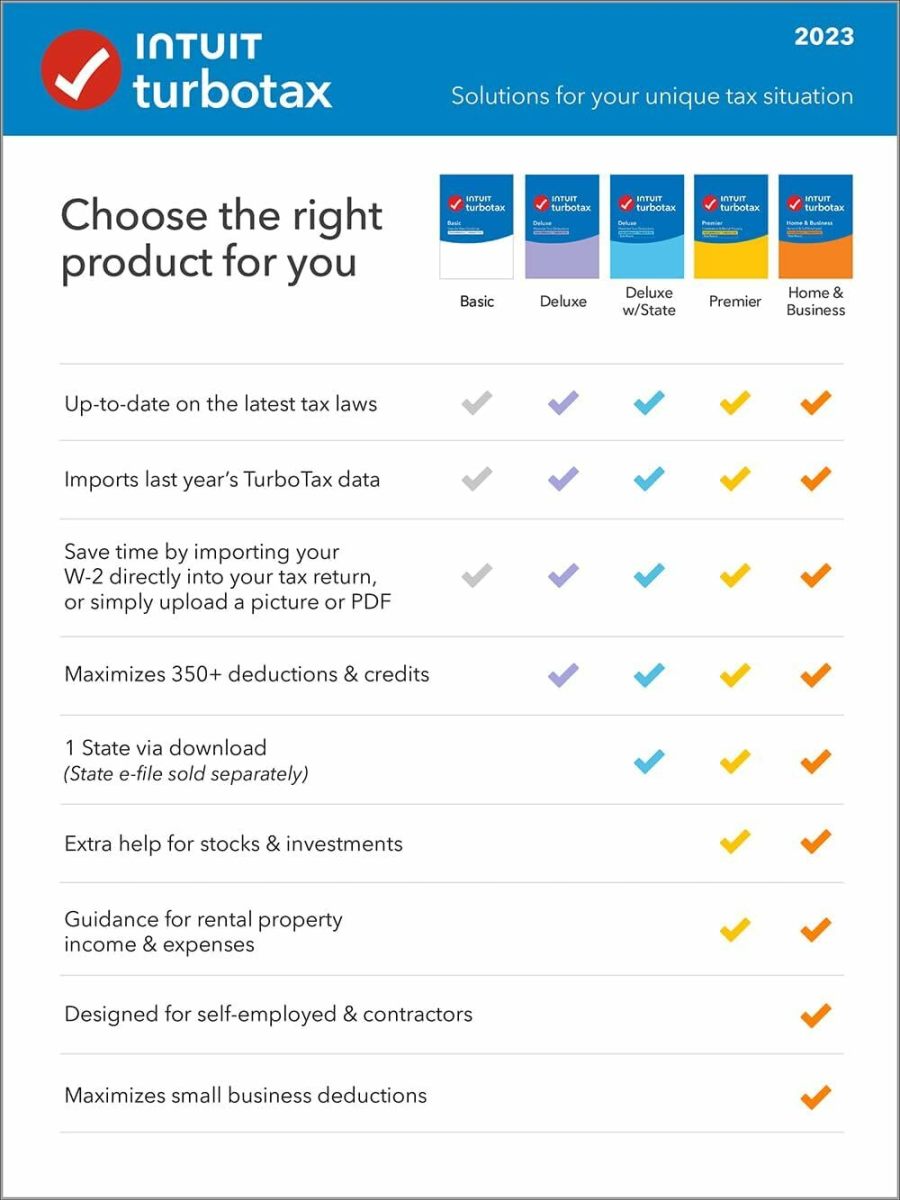

For basic filers, the TurboTax Free Edition (or similar entry-level offerings from other providers) is often sufficient. It handles federal and often state tax returns for simple scenarios, ensuring you meet your basic obligations without incurring unnecessary costs. The financial goal here is compliance with minimal expenditure.

Growing Complexity: When Life Changes Your Taxes

Life events and increasing financial sophistication often introduce layers of complexity that necessitate a more robust tax solution. This mid-tier complexity might include:

- Itemized deductions: You’ve purchased a home, making you eligible for mortgage interest deductions (1098), or you have significant state and local taxes (SALT), charitable contributions, or medical expenses that collectively exceed the standard deduction. Opting to itemize requires more detailed tracking and reporting.

- Dependents, child tax credits, and education credits: Having children opens up eligibility for valuable tax credits like the Child Tax Credit, Credit for Other Dependents, or various education credits (e.g., American Opportunity Tax Credit, Lifetime Learning Credit). These require specific forms and calculations.

- Simple investment income: Beyond basic interest and dividends, you might have capital gains or losses from selling stocks or mutual funds (1099-B). While not as complex as day trading, these transactions need accurate reporting.

- Retirement contributions: You contribute to a traditional IRA or 401(k) and might be eligible for deductions or credits related to these savings.

For these scenarios, TurboTax Deluxe is typically the recommended choice. It’s designed to help you find and maximize various deductions and credits, ensuring you don’t leave money on the table due to increased financial activity. The added financial insights and guidance make the modest cost a worthwhile investment for optimizing your refund.

Beyond the Basics: Tailoring TurboTax to Diverse Financial Lives

As your financial journey becomes more intricate, specialized versions of TurboTax become essential. These editions are built to handle the unique reporting requirements and optimization strategies for specific income streams and asset classes.

The Self-Employed and Small Business Owners: Specialized Needs

For the entrepreneurial spirit, tax preparation takes on a whole new dimension. Self-employed individuals, freelancers, and small business owners (sole proprietors, independent contractors) face unique financial reporting challenges:

- Schedule C (Profit or Loss from Business): This form is central to reporting income and expenses for most sole proprietorships and single-member LLCs. It requires meticulous tracking of revenue and deductible business expenses.

- Business expenses and home office deductions: Identifying and accurately deducting everything from office supplies and travel to health insurance premiums and home office expenses (if applicable) is critical for minimizing taxable income.

- Quarterly estimated taxes: Unlike W-2 employees, self-employed individuals are responsible for paying estimated taxes throughout the year to cover their income tax and self-employment taxes (Social Security and Medicare). Underpayment penalties can be significant if not managed correctly.

- Handling 1099 income and expenses: You’ll likely receive 1099-NEC forms for non-employee compensation, requiring careful matching with your recorded income and expenses.

TurboTax Self-Employed is the go-to version here. It provides robust guidance for Schedule C, helps categorize business expenses, assists with calculating estimated taxes, and even connects to popular accounting software to streamline data import. The financial benefit comes from its specialized tools designed to maximize legitimate business deductions and ensure compliance with complex self-employment tax rules.

Investors and Real Estate Holders: Maximizing Returns and Minimizing Tax Burdens

Individuals with significant investment portfolios or rental properties face specific tax considerations aimed at accurately reporting gains, losses, and income, while also leveraging available deductions.

- Capital gains and losses from stocks, mutual funds, crypto: If you actively trade stocks, manage a diversified portfolio with multiple sales, or engage in cryptocurrency transactions, you’ll have numerous 1099-B forms. Reporting short-term vs. long-term gains/losses, and potentially carrying forward capital losses, requires careful handling.

- Rental property income and deductions (Schedule E): Owning rental property involves reporting rental income and deducting expenses like mortgage interest, property taxes, depreciation, repairs, and maintenance. This generates a Schedule E (Supplemental Income and Loss) form.

- K-1 forms from partnerships or S-corps: If you’re an investor in a partnership or an S-corporation, you’ll receive a Schedule K-1, which reports your share of the entity’s income, losses, and deductions. These forms can be complex to interpret and input.

For these situations, TurboTax Premier or Self-Employed (which often includes Premier features) is usually necessary. These versions are equipped to handle a wide array of investment forms, calculate depreciation for rental properties, and guide you through the intricacies of various investment tax rules, helping to optimize your after-tax returns.

Tax Planning for Unique Situations: Advanced Financial Scenarios

Certain financial profiles involve highly specialized tax situations that demand the highest level of software capability or even professional assistance. While TurboTax’s most advanced versions can handle many of these, some might nudge you towards a tax professional.

- Alternative Minimum Tax (AMT): This parallel tax system can impact higher-income earners or those with certain deductions, requiring additional calculations to determine if you owe AMT.

- Employee stock options (ESOPs, RSUs): The taxation of stock options and restricted stock units can be complex, involving different tax treatments for grant, vesting, and exercise dates.

- Foreign income or assets: If you have income from foreign sources, own foreign bank accounts (requiring FBAR filing), or have other foreign financial assets, you face specific reporting obligations.

- Estate or trust income: If you are a beneficiary of an estate or trust, you may receive a K-1 form that reports your share of income, requiring accurate input.

While TurboTax’s higher-tier products often include features for these advanced scenarios, it’s prudent to consider if the complexity warrants seeking advice from a tax professional (CPA or Enrolled Agent) who can provide personalized guidance and strategic tax planning. The financial risk of misfiling in these complex areas can be substantial, making professional advice a valuable investment.

Weighing Cost vs. Value: A Financial Investment in Accuracy

The decision of which TurboTax version to choose also involves a clear financial cost-benefit analysis. While the free options are tempting, the potential for missed deductions or errors with an inadequate version can far outweigh the savings on the software itself.

The Price Tag of Peace of Mind: Understanding Version Costs

TurboTax offers various tiers, each with its own price structure:

- Free vs. Paid tiers: The Free Edition covers basic W-2 filing, but as soon as you have itemized deductions, investments, or self-employment income, you’ll need to upgrade to a paid version (Deluxe, Premier, Self-Employed).

- State filing fees: Often, the free federal filing comes with a separate charge for state tax returns, even with the free federal edition. Paid federal versions typically charge extra for state filing as well.

- Add-on services: TurboTax offers additional services like “Audit Defense” (which provides representation if you’re audited) or “Live Full Service” (where a tax expert reviews or prepares your return). These come at an extra cost but offer a layer of financial security.

It’s crucial to factor in all these costs when evaluating your total tax preparation expenditure. Don’t just look at the initial price of the federal software.

The ROI of Choosing Wisely: Preventing Errors and Maximizing Savings

The “Return on Investment” of selecting the appropriate TurboTax version is multifaceted:

- Potential for missed deductions/credits: A simpler version might not prompt you for all the deductions and credits you’re eligible for, especially if you have itemized deductions, business expenses, or investment losses. The money you save on the software could be dwarfed by the refund you miss out on.

- Avoiding penalties and interest from incorrect filings: Using the wrong version or making errors due to a lack of guidance can lead to miscalculations, which in turn can result in underpayment penalties, interest charges from the IRS, or even an audit. The cost of these penalties far exceeds the price of an upgraded software version.

- The value of expert guidance: Higher tiers of TurboTax often include access to tax experts (either on-demand or as part of a review service). This “human in the loop” can provide invaluable peace of mind, ensuring accuracy and helping you navigate trickier financial situations. Consider this as a more affordable alternative to a full-service CPA, offering a good balance of cost and expert assurance.

View the software cost as an investment in accuracy and optimization. A slightly higher outlay for the right version can lead to a significantly larger refund or reduced tax liability, along with the invaluable benefit of confidence in your filing.

Making Your Final Decision: A Strategic Financial Approach

With a clear understanding of your financial situation and the various TurboTax versions, you can now approach your final decision strategically.

Assessing Your Financial Year: A Pre-Filing Checklist

Before you even open TurboTax, take a systematic approach to gather your financial information:

- Gather all income statements: This includes W-2s from employers, 1099-NEC for freelance income, 1099-MISC, 1099-INT, 1099-DIV, 1099-B for investments, Schedule K-1s, and any other income documentation.

- Compile deduction documentation: Collect receipts for charitable contributions, medical expenses, property tax statements, mortgage interest statements (1098), student loan interest (1098-E), tuition statements (1098-T), and detailed records of business expenses.

- Review past tax returns: Looking at your previous year’s return can provide a good benchmark. Have your income sources changed significantly? Did you have new deductions or credits this year? This helps identify new complexities.

Once you have a comprehensive picture of your financial year, matching it to TurboTax’s feature sets will be much clearer.

Leveraging TurboTax Features for Financial Advantage

TurboTax isn’t just a form filler; its integrated tools can offer significant financial advantages:

- Import capabilities: Many versions allow you to directly import W-2 information from employers and even investment data from participating financial institutions. This reduces data entry errors and saves time.

- Deduction finders and tax credit optimizers: TurboTax is designed to ask targeted questions to help you uncover every possible deduction and credit, ensuring you don’t miss out on financial benefits due to oversight.

- Audit support and guarantee features: Many TurboTax versions offer audit support, which can include guidance and assistance if you receive an IRS inquiry. Some even offer an “accuracy guarantee” that covers penalties and interest if their software causes a calculation error. These features provide a valuable financial safety net.

Beyond TurboTax: When Professional Financial Advice is Prudent

While TurboTax is an incredibly powerful tool for self-preparation, there are financial situations where DIY solutions reach their limits, and professional expertise becomes invaluable.

Recognizing When DIY Reaches Its Limit

Consider seeking professional help if you encounter:

- Extremely complex financial situations: This could include being involved in multiple partnerships, complex international tax issues, or unusual investment structures.

- Major life events with significant tax implications: A death in the family, a large inheritance, a major divorce settlement, or establishing a complex trust can have profound and intricate tax consequences best handled by an expert.

- Starting a complex business structure: Moving beyond a sole proprietorship to an S-corp or C-corp, or dealing with multi-state business operations, often warrants professional guidance from the outset.

In these scenarios, the financial cost of a professional tax preparer is often justified by the expertise in navigating complex regulations, ensuring compliance, and optimizing your overall financial strategy.

The Role of a CPA or Enrolled Agent in Your Financial Strategy

A Certified Public Accountant (CPA) or Enrolled Agent (EA) offers a level of personalized service that software cannot replicate:

- Personalized advice and tax planning: They can provide strategic advice tailored to your unique financial goals, not just report historical data. This includes year-round tax planning to minimize future liabilities.

- Representation before the IRS: If you’re audited, a CPA or EA can represent you, significantly reducing your stress and potentially achieving a better outcome.

- Long-term financial strategy integration: They can integrate your tax planning with your broader financial planning, investment strategies, and estate planning, offering a holistic approach to your wealth.

Ultimately, the question “which version of TurboTax do I need” boils down to a thorough assessment of your financial complexity and a strategic balancing of cost, convenience, and the imperative for accuracy. By understanding your unique tax profile and leveraging the appropriate software tools, you can confidently navigate tax season, optimize your financial position, and ensure compliance with the least amount of stress.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.