Understanding the various components of a check is a fundamental aspect of managing personal and business finances effectively. In an increasingly digital world, physical checks still play a significant role, and accurately identifying their key elements, such as the routing number, is crucial for secure and efficient financial transactions. For anyone navigating direct deposits, automated bill payments, or linking financial accounts, knowing precisely where to locate and how to utilize the routing number is an essential piece of financial literacy.

Decoding Your Check: The Essentials of a Routing Number

A check is more than just a piece of paper; it’s a financial instrument that authorizes a payment from your bank account to another individual or entity. Each check is replete with critical numerical sequences, each serving a distinct purpose in the financial ecosystem. Misunderstanding these numbers can lead to delayed transactions, returned payments, or even security risks. Among these vital identifiers, the routing number stands out as a cornerstone for virtually all electronic fund transfers.

The Anatomy of a Personal Check

Before zeroing in on the routing number, it’s beneficial to understand the typical layout of a personal or business check. Starting from the top, you’ll usually find the account holder’s name and address. Below that, on the right, is the date line, followed by the payee line (“Pay to the order of”). The numeric and written amounts are prominently displayed, along with a memo line for notes. The signature line authenticates the payment. However, the most critical information for processing lies at the bottom of the check.

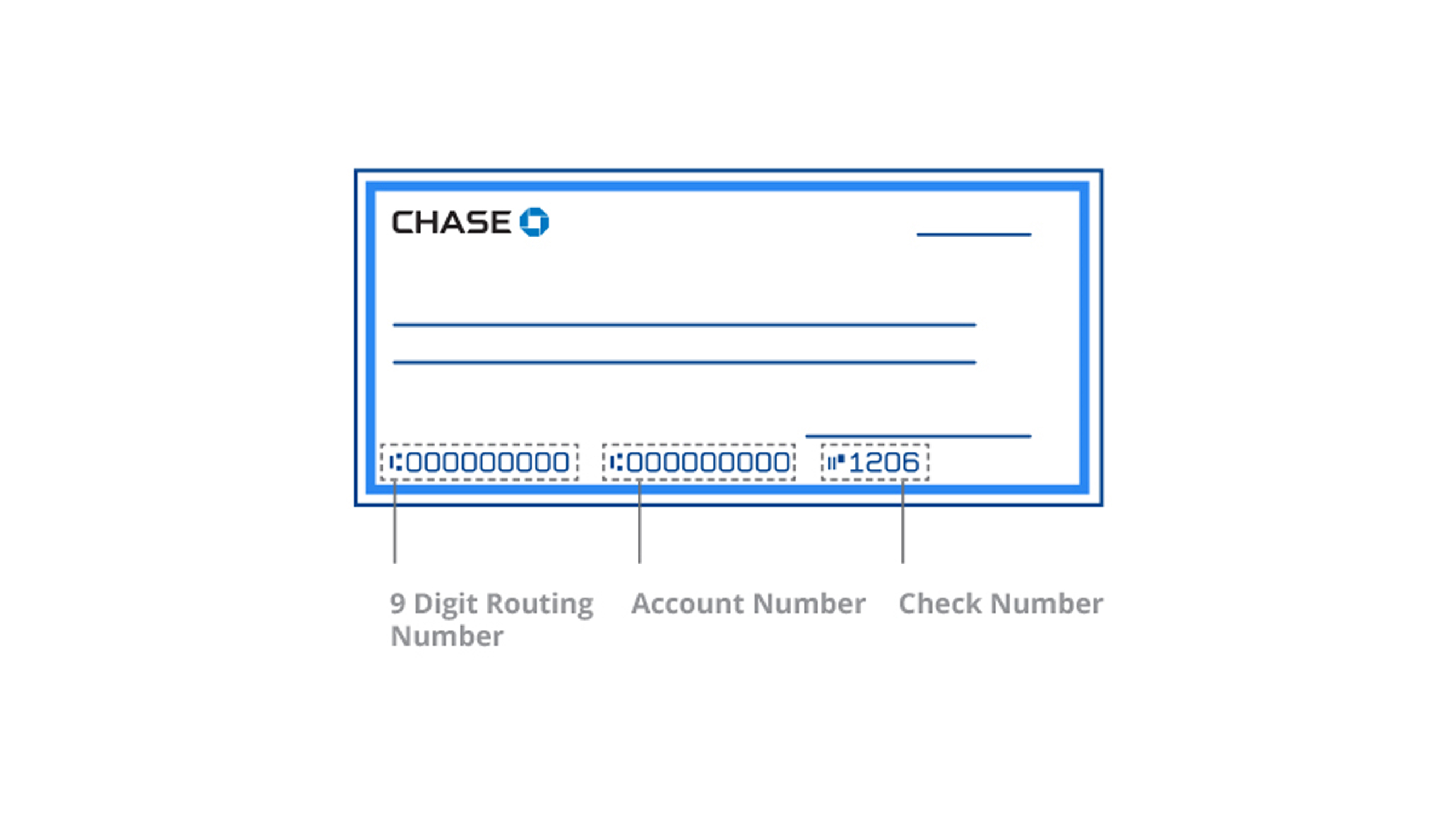

The bottom strip of a check is often called the Magnetic Ink Character Recognition (MICR) line. This special area contains a series of numbers printed in magnetic ink, which allows for rapid, automated processing by financial institutions. This line typically consists of three distinct sets of numbers: the routing number, the account number, and the check number. Understanding the order and function of these ensures you can confidently handle any transaction requiring this information.

Beyond the Basics: Why Each Number Matters

Each numerical sequence on a check serves a unique, critical function. The check number, usually found in the top right corner and also as the last set of numbers on the MICR line, simply identifies that specific check within your series. The account number, typically nestled in the middle of the MICR line, uniquely identifies your individual bank account. However, it is the routing number that dictates where funds should be directed, acting as the digital address for your financial institution itself. Without the correct routing number, funds cannot be directed to or from the appropriate bank, regardless of the accuracy of the account number. This makes accurate identification not just helpful, but absolutely mandatory for financial operations ranging from setting up payroll direct deposits to making online payments.

The Routing Number Revealed: Location and Identification

The routing number, formally known as the ABA Routing Transit Number, is a nine-digit code that identifies your specific financial institution within the United States. Its primary purpose is to ensure that funds transfer correctly between different banks during transactions like direct deposits, wire transfers, and automated clearing house (ACH) payments. Knowing exactly where to find this number on your check is paramount for a wide array of financial activities.

The ABA Routing Transit Number: A Unique Identifier

Every bank and credit union in the U.S. has at least one unique routing number assigned by the American Bankers Association (ABA). Larger financial institutions might have multiple routing numbers, often specific to different regions or types of transactions (e.g., one for ACH transactions, another for wire transfers). While this can occasionally lead to confusion, the routing number printed on your personal checks is almost always the correct one for standard electronic transactions. It acts as a digital postcode for your bank, directing incoming and outgoing funds to the right financial institution before the account number then specifies the individual account.

Visual Guide: Pinpointing the Routing Number

On a standard check, the routing number is consistently found at the bottom, usually as the first set of nine digits in the MICR line, typically enclosed by a special transit symbol on both ends. This symbol, resembling a colon or a small box, helps processing machines correctly identify the start and end of the routing number. It’s crucial to look for this specific nine-digit sequence. For instance, if the MICR line reads [Transit Symbol] 123456789 [Transit Symbol] 0001234567 [Transit Symbol] 101, then 123456789 would be your routing number. The subsequent number would be your account number, and the final number would be the check number.

While the routing number’s placement is largely standardized, it’s always wise to double-check. If you have any doubts, or if your check layout deviates from the norm, you can also find your bank’s routing number by logging into your online banking portal, checking your bank statements, or contacting your financial institution directly. This ensures accuracy, particularly when dealing with large sums or critical payments.

Common Misconceptions: Don’t Confuse It

A frequent mistake is confusing the routing number with other numbers on the check. Some checks might include a bank’s internal branch number or a memo field that could be mistaken for the routing number. Always remember these key distinguishing features:

- Nine Digits: A U.S. routing number is always nine digits long.

- MICR Line: It is part of the magnetic ink character recognition line at the very bottom of the check.

- Position: It is almost always the first set of numbers on that MICR line, bracketed by specific transit symbols.

Avoid using numbers from deposit slips, as these sometimes feature a routing number specific to a particular branch or a different type of transaction, which might not be suitable for general electronic fund transfers. For definitive accuracy, always refer to a printed check or your official bank resources.

The Critical Role of the Routing Number in Financial Transactions

The routing number is far more than just a string of digits; it is the backbone of the entire electronic payment system in the United States. Its accurate use facilitates a multitude of essential financial operations, making it indispensable for personal money management and business finance alike. Without this identifier, the seamless flow of money between different financial institutions would grind to a halt.

Facilitating Electronic Fund Transfers (EFTs)

Electronic Fund Transfers (EFTs) encompass a broad range of digital payment methods, and the routing number is central to almost all of them. When you send money online, pay bills through your bank’s portal, or conduct any transaction that moves money electronically from one bank to another, the routing number ensures the funds arrive at the correct destination bank. This system underpins the efficiency and speed of modern banking, allowing for rapid movement of capital that was once only possible through physical checks and lengthy clearing processes. For individuals, this means faster access to funds; for businesses, it translates to improved cash flow and operational efficiency.

Direct Deposits and Automated Payments

Perhaps the most common and impactful uses of the routing number for most individuals are direct deposits and automated payments.

- Direct Deposit: Whether it’s your paycheck, government benefits, or a refund, direct deposit relies on your routing number and account number to electronically send funds directly into your bank account. This eliminates the need for physical checks, speeds up access to funds, and enhances security by reducing the risk of lost or stolen checks. For employers and businesses, offering direct deposit is a key administrative efficiency, reducing printing and mailing costs while boosting employee satisfaction.

- Automated Bill Payments: Setting up recurring payments for utilities, mortgage, rent, or loan installments often requires your bank’s routing number. This allows creditors to automatically debit your account on specified dates, ensuring timely payments, avoiding late fees, and simplifying personal financial management. For businesses, automated payments are vital for managing subscriptions, services, and regular vendor payments, streamlining their accounts payable processes.

These automated processes reduce human error, save time, and provide a predictable financial rhythm, all made possible by the routing number correctly identifying your financial institution.

Wire Transfers and International Transactions

While direct deposits and ACH payments are standard, the routing number also plays a vital role in more complex transactions such as wire transfers. When you need to send funds quickly and securely, often domestically, a wire transfer is employed. These transactions typically require the recipient’s bank routing number, along with their account number and name, to ensure the money reaches the correct bank without delay.

For international transactions, the routing number often works in conjunction with other identifiers, such as the SWIFT/BIC code (Society for Worldwide Interbank Financial Telecommunication / Bank Identifier Code) for international banks. While the routing number primarily identifies U.S. banks, it can be a part of the broader information required when sending or receiving money across borders, especially when a U.S. bank is an intermediary in the transaction chain. Understanding these distinctions is critical for anyone involved in global commerce or sending remittances internationally, directly impacting the speed, cost, and success rate of cross-border money movement.

Safeguarding Your Financial Information: Best Practices

Given the routing number’s central role in accessing and moving funds, protecting this information is a critical component of personal and business financial security. While it is not as sensitive as your full account number or PIN, its misuse in conjunction with other details can lead to fraudulent activities. Therefore, understanding when and how to share it, and leveraging digital tools for verification, are essential best practices.

When to Share and When to Protect

It’s important to differentiate between necessary sharing and unnecessary exposure. You will need to provide your routing number for legitimate purposes such as:

- Setting up direct deposit with your employer.

- Authorizing automated bill payments.

- Linking external bank accounts (e.g., to investment platforms, payment apps).

- Setting up or receiving wire transfers.

- Paying taxes or other government fees directly from your bank account.

In these scenarios, you are typically providing it to trusted entities or secure platforms. However, you should exercise caution:

- Never share your routing number (or any financial information) in response to unsolicited emails, texts, or calls. Scammers often try to phish for this data.

- Be wary of requests for this information on insecure websites or through unencrypted channels. Always ensure you are on a legitimate and secure website (look for ‘https://’ and a padlock symbol).

- Shred old checks or financial documents that contain your routing and account numbers before discarding them.

While a routing number alone cannot completely compromise your account, it is a key piece of information. When combined with your account number and personal details, it can be exploited. Therefore, prudent protection is always advisable.

Digital Alternatives for Routing Number Retrieval

In today’s digital age, relying solely on physical checks to find your routing number is often unnecessary and sometimes inconvenient. Most financial institutions offer several secure digital alternatives:

- Online Banking Portal: Logging into your bank’s official website or mobile app is typically the safest and most reliable method. Most banks display your routing number and account number prominently on your account summary page or within a “Account Details” or “Direct Deposit Information” section.

- Bank Statements: Both paper and electronic bank statements usually list your account number and the bank’s routing number.

- Contact Your Bank: If all else fails, a quick call to your bank’s customer service line can provide you with the correct routing number. Ensure you verify their identity and use official contact numbers.

Leveraging these digital tools not only provides convenience but also reduces the risk associated with handling physical checks or misreading the MICR line.

Proactive Measures for Financial Security

Beyond understanding your routing number, adopting a broader strategy for financial security is paramount. This includes:

- Regularly monitoring your bank statements and transaction history for any unauthorized activity.

- Setting up transaction alerts with your bank to be notified of any unusual activity.

- Using strong, unique passwords for all your online banking and financial accounts.

- Enabling two-factor authentication (2FA) wherever possible.

- Being vigilant against phishing scams that attempt to trick you into revealing personal and financial information.

- Keeping your operating systems and financial software updated to benefit from the latest security patches.

By consistently applying these proactive measures, individuals and businesses can significantly reduce their vulnerability to fraud and maintain robust control over their financial assets, ensuring that their understanding of elements like the routing number contributes to, rather than detracts from, their overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.