In the intricate landscape of finance, numbers tell a story, and often, that story is best understood through proportions. The seemingly simple question of “which is more, 2/3 or 3/4?” serves as an excellent microcosm for countless financial dilemmas. Are you allocating two-thirds of your income to necessities or three-quarters? Is one investment returning 2/3 of its potential, while another is yielding 3/4? These aren’t just abstract numbers; they represent tangible portions of your wealth, income, or opportunity. Mastering the comparison of such fractions is not merely about mathematical prowess; it’s about cultivating financial acumen that empowers you to make informed, strategic choices, ensuring you always choose the financially superior option.

The Foundation of Financial Comparison: Understanding Proportions

At its core, finance is about managing resources, and resource management inherently involves understanding parts of a whole. Whether it’s a budget, a portfolio, or a market, every financial entity can be broken down into proportional segments. The ability to correctly interpret and compare these segments is paramount to navigating the complexities of the financial world.

Deciphering Fractions in a Financial Context

Fractions are ubiquitous in finance, often appearing as percentages, ratios, or direct allocations. For instance, when a financial advisor discusses allocating “a significant portion” of your portfolio to a certain asset class, they are implicitly referring to a fraction or percentage. Similarly, a discount of “one-third off” is a direct fractional representation.

Let’s consider our primary example: 2/3 versus 3/4.

- 2/3 represents two out of three equal parts of a whole. In financial terms, this could mean 66.67% of your savings, two-thirds of a company’s shares, or two dollars for every three spent.

- 3/4 represents three out of four equal parts of a whole. Financially, this translates to 75% of your available credit, three-quarters of your investment capital, or three successes out of four attempts.

The subtle difference between 66.67% and 75% might seem minor in isolation, but when applied to large sums of money—be it a multi-million dollar investment fund or a lifetime’s earnings—that seemingly small gap can translate into hundreds of thousands, if not millions, of dollars in gains or losses. Understanding this percentage difference is the first step towards making financially intelligent decisions.

Why Small Differences Matter in Large Sums

The power of compound interest, the impact of varying interest rates, or the long-term effect of incremental savings all underscore why even minute fractional differences are crucial. Consider two investment opportunities: Investment A promises to return 2/3 of its principal annually, while Investment B promises 3/4. While neither scenario is realistic for annual returns, let’s use it as an illustrative example. Over a single year on a $100,000 investment:

- Investment A returns $66,666.67 (2/3 of $100,000).

- Investment B returns $75,000.00 (3/4 of $100,000).

The difference of $8,333.33 in one year is substantial. Extrapolate this over decades, with compounding returns, and the gap becomes astronomical. This highlights that discerning “which is more” is not just an academic exercise but a critical determinant of financial success. Whether it’s optimizing a business budget, maximizing personal savings, or evaluating complex financial instruments, the ability to pinpoint the greater proportion is non-negotiable.

Practical Methods for Comparing Financial Fractions

To accurately determine which fraction is larger—2/3 or 3/4—we can employ several straightforward mathematical methods. These techniques are not only useful for this specific comparison but are universally applicable to any financial scenario requiring proportional evaluation.

Method 1: Finding a Common Denominator for Clarity

One of the most intuitive ways to compare fractions is to express them with a common denominator. This allows for a direct comparison of their numerators, making it immediately clear which fraction represents a larger portion of the whole.

To compare 2/3 and 3/4:

- Identify the denominators: 3 and 4.

- Find the least common multiple (LCM) of the denominators: The LCM of 3 and 4 is 12.

- Convert each fraction to an equivalent fraction with the new common denominator:

- For 2/3: To get a denominator of 12, we multiply 3 by 4. Therefore, we must also multiply the numerator (2) by 4. So, 2/3 becomes (2 * 4) / (3 * 4) = 8/12.

- For 3/4: To get a denominator of 12, we multiply 4 by 3. Therefore, we must also multiply the numerator (3) by 3. So, 3/4 becomes (3 * 3) / (4 * 3) = 9/12.

- Compare the new numerators: Now we are comparing 8/12 and 9/12. Since 9 is greater than 8, it is clear that 9/12 is greater than 8/12.

Conclusion: 3/4 is greater than 2/3.

In financial analysis, this method is invaluable when comparing different investment products with varying fee structures, evaluating different equity stakes in a company, or even understanding different tax brackets represented as fractions of income. By bringing disparate figures to a common base, you gain immediate clarity.

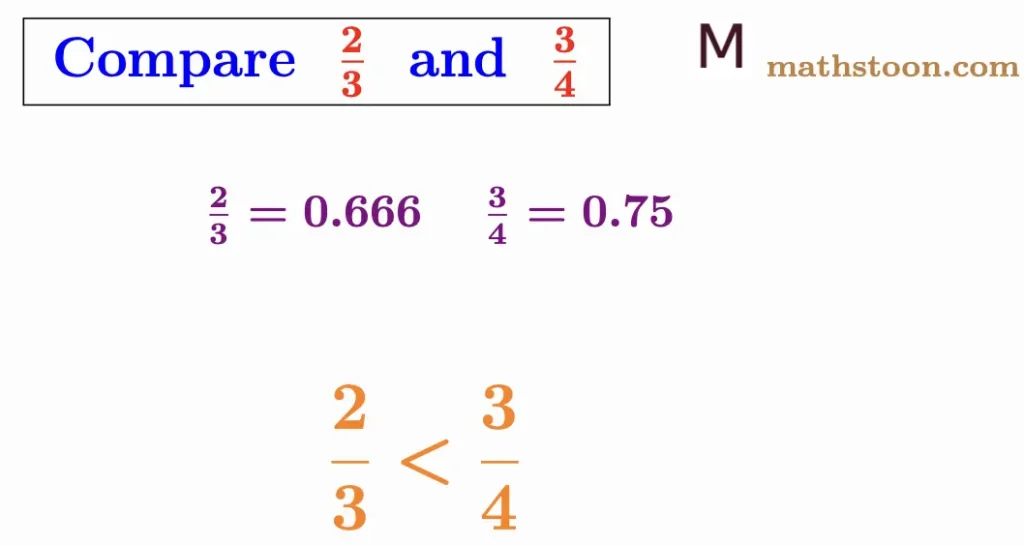

Method 2: Converting to Decimals for Swift Analysis

For those who prefer working with decimals and percentages, converting fractions is a quick and efficient way to compare them. This method is particularly useful in finance, where percentages are a standard language for expressing rates, returns, and allocations.

To compare 2/3 and 3/4:

- Divide the numerator by the denominator for each fraction:

- For 2/3: 2 ÷ 3 ≈ 0.6667 (often rounded to two or four decimal places for financial calculations).

- For 3/4: 3 ÷ 4 = 0.75.

- Compare the decimal values: 0.75 is clearly greater than 0.6667.

Conclusion: 3/4 is greater than 2/3.

Converting to decimals immediately gives you the percentage equivalent (0.6667 = 66.67%; 0.75 = 75%), which is how most financial data is presented. This method is excellent for quick comparisons in real-time trading, budgeting on the fly, or interpreting financial reports where percentages are abundant.

Method 3: Cross-Multiplication for Quick Verification

Cross-multiplication offers a rapid way to compare two fractions without explicitly finding a common denominator or converting to decimals. While perhaps less intuitive for some, it’s a powerful shortcut once mastered.

To compare 2/3 and 3/4:

- Multiply the numerator of the first fraction by the denominator of the second fraction: 2 * 4 = 8.

- Multiply the numerator of the second fraction by the denominator of the first fraction: 3 * 3 = 9.

- Compare the products: The first product (8) corresponds to the first fraction (2/3), and the second product (9) corresponds to the second fraction (3/4). Since 9 is greater than 8, the second fraction (3/4) is greater.

Conclusion: 3/4 is greater than 2/3.

This method is particularly useful when you need a swift comparison and are dealing with numerous fractional figures, such as in competitive bidding scenarios, comparing relative performance metrics across different entities, or quickly verifying figures in a financial spreadsheet.

Applying Proportional Thinking to Personal Finance

The ability to compare proportions like 2/3 and 3/4 transcends theoretical math problems; it directly influences effective personal financial management. From daily spending to long-term wealth building, proportional thinking is a cornerstone.

Budgeting and Expense Allocation: The 50/30/20 Rule and Beyond

Budgeting is fundamentally about allocating proportions of your income. Popular rules like the 50/30/20 rule (50% for needs, 30% for wants, 20% for savings/debt repayment) are direct applications of fractional allocation. But what if you’re evaluating a financial plan that suggests allocating 2/3 of your income to living expenses versus another plan suggesting 3/4? Knowing that 3/4 is a larger slice means that the latter plan demands a greater proportion of your income for living, potentially leaving less for savings or discretionary spending. This crucial comparison helps you choose a budget that aligns with your financial goals and comfort level.

Investment Portfolio Diversification: Weighting Your Assets

Diversification involves distributing your investments across various asset classes (stocks, bonds, real estate, etc.) in specific proportions to manage risk and optimize returns. An investment strategy might propose allocating 2/3 of your equity portfolio to large-cap stocks and 1/3 to small-cap. Another might suggest 3/4 to large-cap and 1/4 to small-cap. Understanding that 3/4 represents a greater concentration allows you to assess the risk profile more accurately. A higher proportion in a certain asset class means greater exposure to its particular risks and rewards. Accurately comparing these fractions ensures your portfolio reflects your true risk tolerance and investment objectives.

Evaluating Returns and Discounts: Maximizing Your Financial Gains

Whether you’re looking at a discount during a sale (e.g., “up to 2/3 off selected items” vs. “3/4 off all clearance”) or comparing investment returns, the ability to discern the larger fraction is vital. A discount of 3/4 is significantly better than 2/3, representing a 75% saving compared to 66.67%. Similarly, understanding that one investment fund generated 3/4 of the market average return while another only managed 2/3 can guide your decisions towards more profitable ventures.

Business Finance and Strategic Resource Allocation

In the corporate world, the stakes are often higher, and the impact of proportional thinking can be felt across operational efficiency, market positioning, and ultimate profitability. Businesses constantly make decisions based on ratios and fractions.

Project Funding and Resource Prioritization

Companies frequently allocate capital and resources across multiple projects. If Project A requires 2/3 of the available budget, and Project B requires 3/4, a finance manager instantly knows that Project B is a more significant draw on resources. This understanding informs strategic decisions regarding project prioritization, staffing, and potential outsourcing. Making the wrong proportional allocation can lead to resource depletion in critical areas or an inability to fund high-potential initiatives.

Market Share and Performance Metrics

Market share is often expressed as a fraction or percentage of the total market. If a company holds 2/3 of the market share in one region but only 3/4 in another, it indicates that while both are dominant positions, the latter has a slightly stronger foothold. Comparing these fractions helps in understanding competitive landscapes, identifying growth opportunities, and setting realistic targets. Similarly, performance metrics—like the proportion of successful sales conversions (e.g., 2/3 success rate vs. 3/4 success rate)—guide marketing and sales strategies.

Profit Margins and Cost-Benefit Analysis

Profit margins (net profit as a fraction of revenue) and cost-benefit ratios are crucial for assessing the financial health and viability of a business. A product with a 3/4 profit margin is far more lucrative than one with a 2/3 margin, indicating more efficient operations or better pricing strategies. In cost-benefit analysis, comparing the fractional benefits to the fractional costs of a new initiative ensures that the investment is worthwhile. A project yielding 3/4 benefit for every unit of cost is preferable to one yielding only 2/3.

The Long-Term Impact of Fractional Differences

The seemingly small difference between 2/3 and 3/4, when compounded over time, can lead to profoundly divergent financial outcomes. This emphasizes the importance of consistent, accurate proportional reasoning in all financial decisions.

Compounding Returns: The Power of Persistent Proportions

The magic of compounding interest means that consistent, even slightly higher, returns can lead to exponential wealth growth. If one investment consistently yields 3/4 of a benchmark return while another yields 2/3, the cumulative difference over decades can be staggering, illustrating the true power of persistent, superior proportions. This principle applies not only to investment returns but also to savings rates and debt reduction. A higher fractional saving rate, maintained consistently, leads to substantially greater wealth accumulation.

Risk Management: Assessing Your Exposure

Understanding proportions is critical for effective risk management. If your financial exposure to a single volatile asset is 3/4 of your total liquid assets compared to another individual whose exposure is 2/3, you are significantly more vulnerable to market fluctuations. Being able to quantify and compare these risks through fractional analysis allows for more prudent decision-making and better portfolio protection strategies.

Building Financial Literacy for Sustainable Wealth

Ultimately, the ability to confidently answer “which is more, 2/3 or 3/4?” within a financial context is a testament to strong financial literacy. This skill set empowers individuals and businesses to:

- Optimize resource allocation: Ensuring every dollar is working as hard as possible.

- Make informed comparisons: From investment products to loan offers.

- Project future outcomes: Understanding the long-term implications of current choices.

- Identify opportunities and mitigate risks: Spotting the better deal or the greater vulnerability.

In conclusion, while the question “which is more 2/3 or 3/4?” might appear simple, its answer holds significant weight in the financial world. The practical methods for comparison – common denominators, decimal conversion, and cross-multiplication – are more than just mathematical tools; they are essential instruments for navigating the complexities of personal and business finance. By embracing and applying proportional thinking, individuals and organizations can gain a clearer understanding of their financial position, make more strategic decisions, and ultimately, pave the way for sustainable financial growth and prosperity. The knowledge that 3/4 is indeed greater than 2/3 is a small but powerful piece of wisdom that underpins a vast array of critical financial calculations and choices.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.