Choosing the “best” credit card can often feel like navigating a labyrinth, especially when confronted with the extensive and highly competitive portfolio offered by a financial giant like Chase. With a myriad of options catering to diverse spending habits, financial goals, and credit profiles, identifying the single “best” card is a deeply personal quest. What’s optimal for a frequent international traveler might be entirely unsuitable for a budget-conscious cash-back enthusiast or a burgeoning small business owner.

Chase, renowned for its robust Ultimate Rewards program, generous sign-up bonuses, and a suite of travel and consumer protections, consistently ranks among the top issuers. Their cards promise not just convenience, but also significant value through points, miles, and cash back. However, unlocking this value requires a strategic approach, beginning with a thorough understanding of your own financial landscape. This guide aims to demystify Chase’s offerings, helping you pinpoint the ideal card — or combination of cards — that aligns perfectly with your lifestyle and financial aspirations, ultimately empowering you to maximize your rewards and financial well-being.

Understanding Your Financial Profile and Spending Habits

Before diving into the specifics of Chase’s impressive card lineup, the most crucial first step is to conduct an honest assessment of your own financial habits and objectives. This self-evaluation will serve as your compass, guiding you toward cards that genuinely deliver value rather than just attractive marketing.

Identifying Your Primary Spending Categories

Credit cards are designed to reward specific types of spending. A card might offer accelerated rewards on dining, travel, groceries, gas, or even rotating categories. Take a moment to review your last three to six months of expenditures. Are you primarily:

- A Traveler? Do you spend significantly on flights, hotels, car rentals, and international purchases? Travel-focused cards often provide the highest return on these categories, alongside valuable perks like lounge access and travel insurance.

- A Diner or Grocery Shopper? Many cards offer bonus points or cash back for restaurant meals, food delivery, and supermarket purchases.

- A General Spender? If your spending is diversified with no dominant category, a flat-rate cash back or points card might be more suitable, ensuring you earn rewards on every dollar spent.

- A Business Owner? Business expenses like internet, phone services, shipping, and office supplies often have dedicated bonus categories on small business cards.

Understanding where your money consistently goes is paramount to selecting a card that rewards your natural spending patterns without forcing you to alter them unnecessarily.

Evaluating Your Credit Score and Eligibility

Your credit score is a critical gatekeeper for premium credit card offerings. Chase cards typically require good to excellent credit (generally FICO scores of 670 and above) for their most rewarding products like the Sapphire series or Ink Business Preferred.

- Excellent Credit (740-850): Opens the door to virtually all premium travel and rewards cards with the best benefits and lowest interest rates.

- Good Credit (670-739): Still provides access to a wide range of strong rewards cards, though some top-tier options might be out of reach.

- Fair Credit (580-669): You might need to start with cards designed for building credit, such as secured cards or basic offerings like the Chase Freedom Rise℠, before graduating to more rewarding options.

Beyond the score itself, Chase has a notorious “5/24 Rule,” which generally means they will deny applications if you’ve opened five or more personal credit cards (from any issuer, not just Chase) in the past 24 months. Understanding your current credit landscape and this specific rule is vital for a successful application.

Defining Your Financial Goals

What do you want your credit card to do for you? Your objective will heavily influence your choice:

- Maximizing Travel Rewards: If your dream is to fly first class or stay in luxury hotels for free, cards that earn transferable points (like Chase Ultimate Rewards) are ideal.

- Earning Cash Back: For those who prefer direct savings or dislike the complexity of travel redemptions, a robust cash back card offers tangible value.

- Building or Rebuilding Credit: If you’re new to credit or working to improve your score, cards with simpler structures, lower limits, and a focus on responsible usage are key.

- Transferring a Balance: If you have high-interest debt, a card offering a 0% APR introductory period on balance transfers could provide significant relief.

- Managing Business Expenses: Small business owners need cards that separate personal and business spending, offer specific business rewards, and provide tools for expense tracking.

Clarifying these goals will significantly narrow down the vast array of options, making your decision-making process much more straightforward.

Top Chase Credit Cards for Diverse Needs

Chase’s credit card portfolio is designed to cater to a broad spectrum of consumers and businesses. Here’s a breakdown of their leading cards, categorized by their primary strengths and target users.

For the Savvy Traveler: Chase Sapphire Preferred® Card & Chase Sapphire Reserve®

These two cards are the cornerstones of Chase’s travel rewards program, offering premium benefits and the highly versatile Ultimate Rewards points.

- Chase Sapphire Preferred® Card: Often considered the entry point into premium travel rewards, the Preferred offers 2x points on travel and dining, and 3x points on online grocery purchases, select streaming services, and Peloton purchases (through March 2025). Points are worth 25% more when redeemed for travel through Chase Ultimate Rewards, or can be transferred 1:1 to numerous airline and hotel partners (e.g., United, Southwest, Hyatt, Marriott) for potentially even greater value. It comes with a modest annual fee (currently $95) offset by a $50 annual hotel credit and strong travel protections. This card is excellent for those who travel a few times a year and want significant rewards without a hefty annual fee.

- Chase Sapphire Reserve®: The Reserve is the premium big sibling, targeting frequent travelers and those seeking luxury perks. It earns 3x points on travel and dining (after the $300 travel credit is applied), and 10x points on hotels and rental cars booked through Chase Travel. Points are worth 50% more when redeemed for travel through Chase Ultimate Rewards, making each point effectively 1.5 cents. Its annual fee (currently $550) is significantly mitigated by a $300 annual travel credit, Priority Pass Select lounge access, TSA PreCheck/Global Entry credit, and comprehensive travel insurance. For those who travel extensively and can fully utilize its premium benefits, the Reserve often provides outsized value.

For Maximum Cash Back Earners: Chase Freedom Unlimited® & Chase Freedom Flex℠

These two cards are fantastic no-annual-fee options for earning cash back, which can also be converted to Ultimate Rewards points if paired with a Sapphire card.

- Chase Freedom Unlimited®: This card offers a straightforward earning structure: 1.5% cash back (or 1.5x points) on all eligible purchases, plus 5% on travel purchased through Chase Travel, and 3% on dining and drugstore purchases. Its simplicity and consistent earning rate on all spending make it an excellent choice for everyday expenses where bonus categories don’t apply.

- Chase Freedom Flex℠: The Flex introduces a dynamic rewards structure, offering 5% cash back (or 5x points) on up to $1,500 in combined purchases in rotating bonus categories each quarter (e.g., gas stations, groceries, Amazon.com). It also offers 5% on travel purchased through Chase Travel, 3% on dining and drugstore purchases, and 1% on all other purchases. This card is perfect for strategic spenders who don’t mind activating quarterly categories to maximize their earnings.

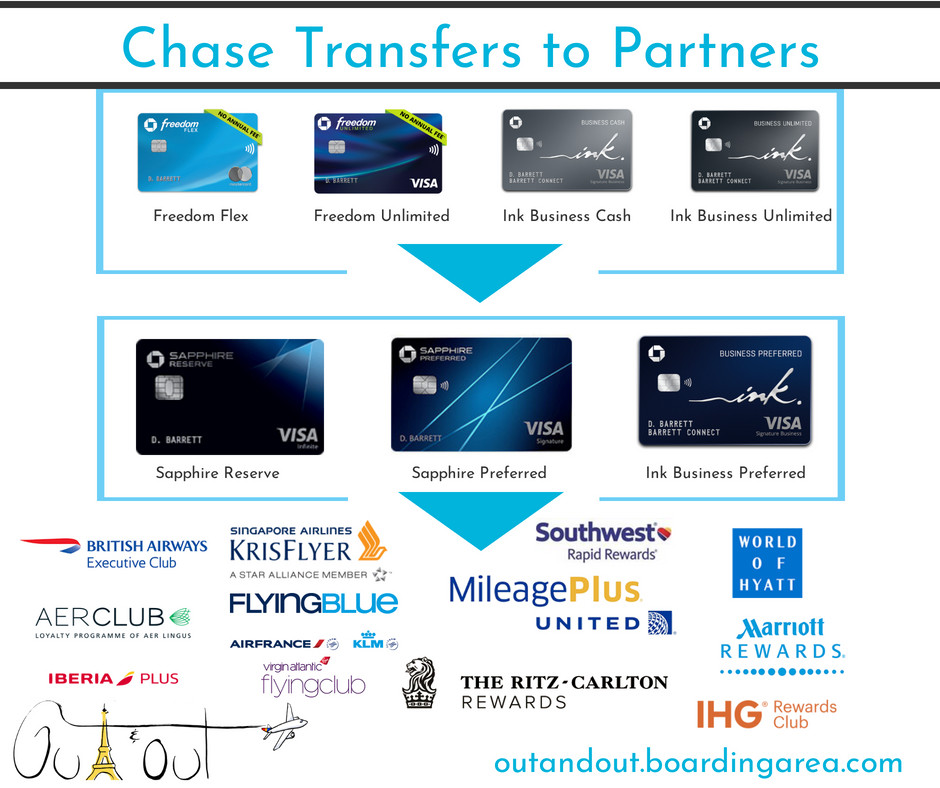

Both Freedom cards are excellent standalone cash back options, but their true power is unleashed when combined with a Sapphire card, allowing you to convert your cash back to transferable Ultimate Rewards points.

For Growing Businesses: Chase Ink Business Preferred® & Ink Business Cash® Credit Card

Chase offers a powerful suite of business credit cards under the Ink brand, designed to help small business owners manage expenses and earn rewards tailored to business needs.

- Ink Business Preferred® Credit Card: This is the premium business travel card, offering 3x points per dollar on the first $150,000 spent annually in combined categories like travel, shipping, internet, cable, phone services, and advertising purchases made with social media sites and search engines. It also provides cell phone protection and 1:1 point transfers to airline and hotel partners. With an annual fee of $95, it’s a strong choice for businesses with significant operational spending.

- Ink Business Cash® Credit Card: A no-annual-fee powerhouse for everyday business expenses, the Ink Business Cash offers 5% cash back (or 5x points) on the first $25,000 spent annually in combined purchases at office supply stores and on internet, cable, and phone services. It also earns 2% cash back (or 2x points) on the first $25,000 spent annually in combined purchases at gas stations and restaurants. This card is ideal for businesses with high fixed costs in these specific categories.

- Ink Business Unlimited® Credit Card: This card provides a simple 1.5% cash back (or 1.5x points) on all eligible business purchases, with no annual fee. It’s a great option for businesses with diversified spending that prefer a flat rewards rate.

Similar to the personal Freedom cards, the Ink Cash and Ink Unlimited truly shine when paired with an Ink Business Preferred or personal Sapphire card, allowing the accumulated cash back to be converted into valuable, transferable Ultimate Rewards points.

For Building Credit or Balance Transfers: Chase Slate Edge℠ & Chase Freedom Rise℠

While not primary rewards cards, these options serve crucial financial needs, particularly for those looking to improve their credit health or manage existing debt.

- Chase Slate Edge℠: This card is primarily designed for balance transfers, often featuring an introductory 0% APR period on new purchases and balance transfers. It has no annual fee and provides tools to help you improve your credit score, such as automatic credit line reviews. While it doesn’t offer a rewards program, its value lies in helping consumers consolidate debt and save on interest.

- Chase Freedom Rise℠: Geared towards individuals new to credit or looking to rebuild their credit, the Freedom Rise offers a pathway to establishing a positive credit history. It typically requires a bank account with Chase to apply and offers 1.5% cash back on all purchases, making it a simple, no-annual-fee option for those starting their credit journey responsibly.

Optimizing Your Rewards Strategy with the “Chase Trifecta”

For those committed to maximizing their credit card rewards, the concept of the “Chase Trifecta” is a game-changer. This strategy involves combining specific Chase cards to unlock their full synergistic potential.

The Synergistic Power of Combining Cards

The “Trifecta” typically involves pairing one premium Sapphire card (Preferred or Reserve) with the Chase Freedom Unlimited® and the Chase Freedom Flex℠ (or potentially an Ink Business card if you’re a business owner).

- Sapphire Card (e.g., Reserve): Acts as the “hub” for point redemption, allowing you to transfer points to airline/hotel partners and providing the bonus redemption value for travel through the Chase portal (e.g., 1.5 cents per point with Reserve). It also covers premium travel benefits.

- Freedom Flex℠: Maximizes earnings in rotating 5% cash back categories.

- Freedom Unlimited®: Ensures a solid 1.5% cash back (or 1.5x points) on all non-bonus spending, plus 3% on dining/drugstores and 5% on Chase travel.

By strategically using these cards, you can earn accelerated points in various categories (5x on rotating, 3x on dining/drugstores, 1.5x on everything else) and then pool all these points into your Sapphire account. Once pooled, all points gain the Sapphire card’s higher redemption value (e.g., 1.5 cents each for travel with the Reserve) and become eligible for 1:1 transfers to Chase’s valuable travel partners. This strategy transforms what would be simple cash back into highly flexible and valuable travel points.

Maximizing Point Transfers and Redemptions

The true magic of the Ultimate Rewards program lies in its flexibility. While redeeming points for cash back or gift cards offers a baseline value (usually 1 cent per point), the highest value is typically found through:

- Transferring to Travel Partners: Chase partners with major airlines (e.g., United, Southwest, British Airways, Virgin Atlantic) and hotel chains (e.g., Hyatt, Marriott, IHG). Transferring points to these partners during a promotion or for high-value redemptions (like business class flights or luxury hotel stays) can yield significantly more than 1.5 cents per point – often 2 cents or more. This requires some research and flexibility but can result in incredible travel experiences for minimal cost.

- Booking Travel Through the Chase Travel Portal: For simpler travel bookings, using your Sapphire card to book directly through Chase’s portal provides an immediate value boost (25% more with Preferred, 50% more with Reserve), without the complexity of partner transfers.

By understanding how to earn, pool, and then strategically redeem your Ultimate Rewards points, you can unlock incredible value, turning your everyday spending into memorable experiences or significant savings.

Key Factors to Consider Before Applying

Once you’ve identified potential Chase credit cards that align with your profile, it’s crucial to consider a few final practicalities before submitting an application. Responsible credit card management is just as important as strategic card selection.

Annual Fees vs. Benefits

Many of Chase’s most rewarding cards come with an annual fee. While these fees might seem daunting, it’s essential to perform a cost-benefit analysis.

- Premium Cards (e.g., Sapphire Reserve): A high annual fee (e.g., $550) can be well worth it if you fully utilize benefits like the $300 travel credit, lounge access, TSA PreCheck/Global Entry, and premium travel insurance. If these benefits aren’t regularly used, a lower-fee option might be better.

- Mid-Tier Cards (e.g., Sapphire Preferred): A moderate fee (e.g., $95) is often easily offset by the annual hotel credit, increased redemption value, and primary car rental insurance.

- No Annual Fee Cards (e.g., Freedom cards, Ink Cash): These are excellent choices if you prefer not to pay a fee, or if the benefits of a higher-fee card don’t justify the cost for your spending habits.

Never pay an annual fee for benefits you won’t use. The “best” card isn’t always the one with the most perks, but the one whose perks you genuinely leverage.

Sign-Up Bonuses and Minimum Spend Requirements

Chase is known for offering substantial sign-up bonuses, which can provide a significant boost to your points or cash back balance right from the start. However, these bonuses typically require you to spend a certain amount within a specified timeframe (e.g., $4,000 in the first three months).

- Plan your spending: Ensure you can comfortably meet the minimum spend requirement through your regular expenses without going into debt or making unnecessary purchases.

- Time your applications: If you’re considering multiple cards, strategize your applications to ensure you can meet all minimum spend requirements without overlap or undue financial pressure.

A large sign-up bonus is a powerful incentive, but it should never lead to overspending.

APR, Fees, and Other Terms

While the focus is often on rewards, understanding the fundamental terms and conditions of your credit card is paramount.

- Annual Percentage Rate (APR): Credit cards are primarily designed for convenience and rewards, not carrying a balance. Always aim to pay your statement balance in full each month to avoid incurring high-interest charges, which will quickly negate any rewards earned.

- Late Payment Fees: Missing a payment can result in fees and damage to your credit score. Set up automatic payments or reminders.

- Foreign Transaction Fees: If you travel internationally, ensure your chosen card (like the Sapphire cards or some Ink cards) has no foreign transaction fees, as these can quickly add up.

- Cash Advance Fees: Avoid cash advances, as they typically come with high fees and immediate, high-interest rates.

Always read the cardmember agreement carefully to understand all terms, conditions, and fees associated with your chosen card.

The Chase 5/24 Rule

As mentioned earlier, Chase has a strict application rule: if you have opened 5 or more personal credit cards from any issuer in the past 24 months, your application for most Chase cards will likely be denied.

- Check your credit report: Before applying, check your credit report to see how many new accounts you’ve opened recently.

- Prioritize Chase cards: If you are under 5/24, and have a strong interest in Chase’s Ultimate Rewards program, it’s often advisable to apply for desired Chase cards first before opening cards from other issuers.

- Exceptions: Some business cards might not count towards your personal 5/24 count, though you still need to be under the limit to get them.

Understanding and adhering to the 5/24 rule is crucial for anyone serious about building a long-term relationship with Chase and maximizing their Ultimate Rewards strategy.

Conclusion

Ultimately, the “best” Chase credit card is not a universal truth but a tailored solution. It’s the card—or combination of cards—that meticulously aligns with your unique financial behavior, spending categories, credit standing, and overarching financial objectives. Whether you are a globetrotting adventurer, a meticulous budgeter chasing every cash back dollar, or a shrewd business owner streamlining expenses, Chase has a product designed with your needs in mind.

The journey begins with introspection: rigorously assess where your money goes, what you hope to achieve, and what your credit profile allows. Then, arm yourself with knowledge of Chase’s diverse offerings, from the premium travel perks of the Sapphire cards to the targeted cash back of the Freedom and Ink series, and even the credit-building support of the Slate Edge or Freedom Rise. By strategically selecting and responsibly managing your Chase credit cards, you’re not just choosing a piece of plastic; you’re adopting a powerful financial tool that can significantly enhance your rewards, savings, and overall financial journey. Choose wisely, spend responsibly, and unlock the full potential of your Chase credit card experience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.