For businesses operating in the United States, managing payroll and tax obligations is a cornerstone of financial compliance. Among the myriad forms employers must contend with, Form 941, the Employer’s Quarterly Federal Tax Return, stands out as a critical document. It is used to report income taxes, Social Security tax, or Medicare tax withheld from employee paychecks, as well as the employer’s share of Social Security and Medicare taxes. Accurately completing and timely submitting this form, along with any due payments, is not just a regulatory requirement but a fundamental aspect of sound business finance.

Navigating the complexities of federal tax submissions can be daunting, especially when it comes to identifying the correct recipient for your payment. A single misstep can lead to penalties, interest, and unnecessary administrative burdens. This guide aims to demystify the process, offering a detailed roadmap for employers to ensure their Form 941 and associated payments reach the Internal Revenue Service (IRS) promptly and accurately, safeguarding their financial standing and compliance.

Understanding Form 941: The Employer’s Quarterly Federal Tax Return

Before delving into the logistics of where and how to send your payments, it’s crucial to grasp the fundamental nature and importance of Form 941 itself. This understanding forms the bedrock of effective payroll tax management.

What is Form 941?

Form 941 is a federal tax document that nearly every employer in the U.S. must file each quarter. It serves as a comprehensive report detailing the wages paid, tips reported, federal income tax withheld, and both the employer and employee portions of Social Security and Medicare taxes (FICA taxes). These taxes are critical for funding Social Security benefits, Medicare, and various government programs. The form helps the IRS track employer tax liabilities and ensure that businesses are fulfilling their obligation to withhold and remit these funds on behalf of their employees. It reconciles the total tax liability for the quarter with the deposits made throughout that quarter.

Who Needs to File?

Generally, if you pay wages to one or more employees, you are an employer and must file Form 941 quarterly. This applies to most businesses, including corporations, partnerships, and sole proprietors who have employees. There are a few exceptions:

- Seasonal employers: If you hire employees for only a portion of the year, you’ll file for the quarters you pay wages.

- Employers of household employees: These typically file Schedule H (Form 1040).

- Employers of farm employees: These generally file Form 943, Employer’s Annual Federal Tax Return for Agricultural Employees.

- Businesses with no employees: If you are a sole proprietor with no employees, you typically don’t file Form 941 for yourself.

- Businesses that ceased operations: If you stopped paying wages and closed your business, you’ll file a final Form 941 and indicate it as such.

Understanding whether your business falls under the filing requirement is the first step towards robust financial compliance.

Key Information Reported on Form 941

Form 941 requires employers to provide detailed figures for the quarter. This includes:

- Number of employees who received wages, tips, or other compensation.

- Total wages, tips, and other compensation subject to federal income tax withholding.

- Federal income tax withheld from wages, tips, and other compensation.

- Taxable Social Security wages and tips (and the resulting tax).

- Taxable Medicare wages and tips (and the resulting tax).

- Additional Medicare tax withholding.

- Current quarter’s adjustments for fractions of cents, sick pay, tips, and group-term life insurance.

- Total tax liability for the quarter.

- Total deposits made for the quarter.

The accuracy of this data is paramount, as discrepancies can trigger IRS inquiries, audits, or penalties, directly impacting a business’s financial health.

Navigating Payment Methods for Form 941

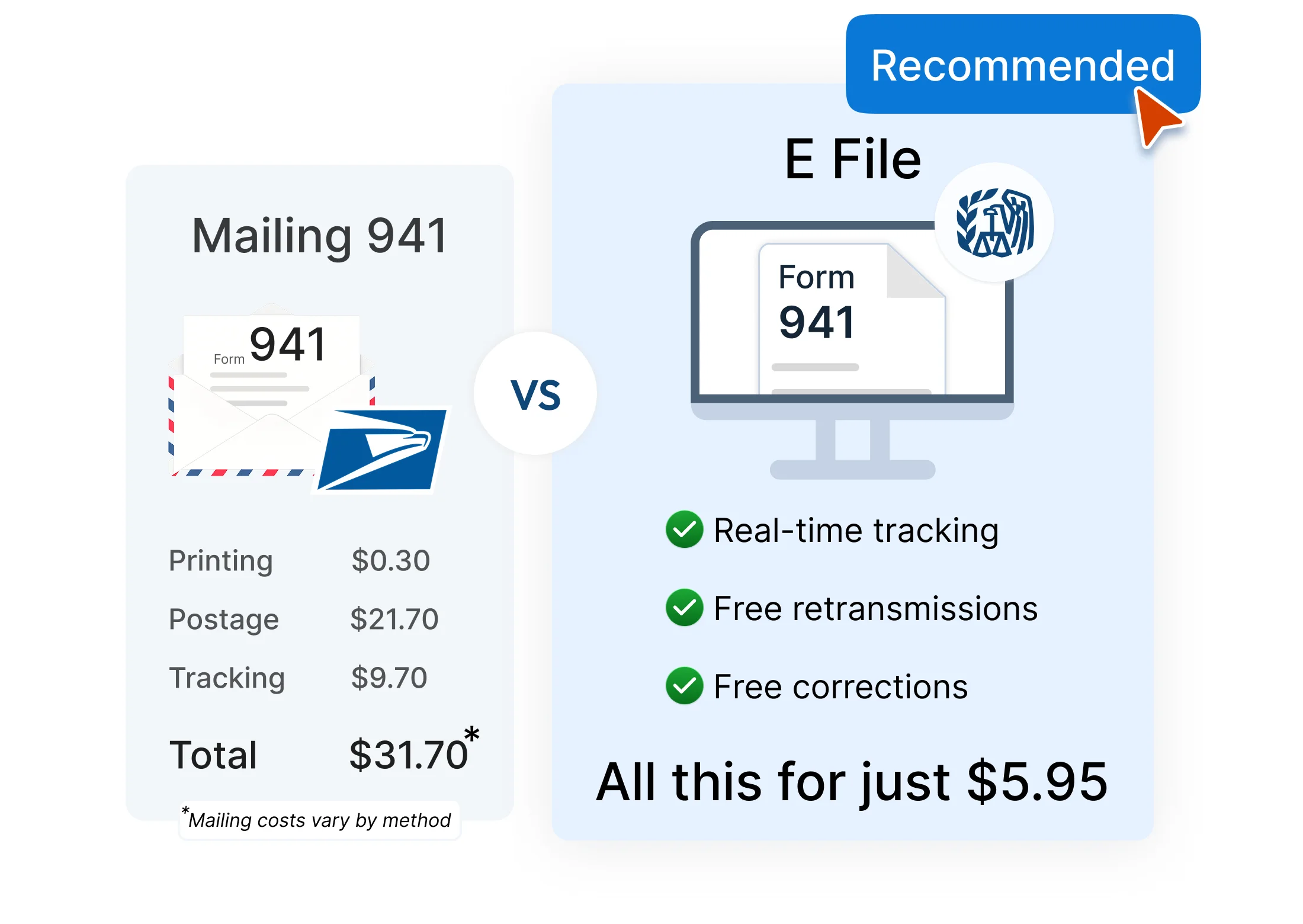

Once Form 941 is prepared, the next critical step is to ensure that any associated payment reaches the IRS correctly. The IRS strongly encourages electronic payment, but mail options still exist under specific circumstances. Choosing the right method based on your business’s needs and compliance requirements is vital.

Electronic Funds Transfer (EFTPS): The Preferred Method

The Electronic Federal Tax Payment System (EEFTPS) is the IRS’s primary method for receiving federal tax payments. For most employers, EFTPS is not just preferred but mandatory. If your total federal tax deposits were over $200,000 in a prior calendar year, or if you expect your annual tax liability to be over $200,000, you must use EFTPS. Even if your liability is lower, the convenience, speed, and security of EFTPS make it the recommended choice.

Benefits of EFTPS:

- Convenience: Payments can be scheduled 24/7 online or by phone.

- Accuracy: Reduces errors associated with manual processing.

- Security: Eliminates the risk of lost or stolen checks.

- Proof of Payment: Provides an immediate confirmation number.

To use EFTPS, you must first enroll on the official EFTPS website (www.eftps.gov). This process can take several business days, so it’s essential to enroll well in advance of your first payment due date. Once enrolled, you can schedule payments, view payment history, and manage your tax accounts. Most payroll software solutions also integrate directly with EFTPS, streamlining the payment process.

Making Payments by Mail: When and How

While EFTPS is the standard, there are limited scenarios where mailing a payment with Form 941 is permissible. Generally, you can mail a check or money order only if your total tax liability for the current quarter (or annual liability if filing annually for other forms) is less than $2,500, and you did not incur a $100,000 next-day deposit obligation during the quarter. However, even if you meet this threshold, the IRS always encourages electronic payment.

If you must mail your payment, it is crucial to follow specific guidelines:

- Do not staple or attach your payment to Form 941. The IRS uses automated processing equipment that can be damaged by staples.

- Make your check or money order payable to the “United States Treasury.”

- Write your employer identification number (EIN), “Form 941,” and the tax period on your payment. For example, “EIN: XX-XXXXXXX, Form 941, Q1 20XX.” This ensures your payment is correctly credited to your account.

- Include Form 941-V, Payment Voucher. This voucher helps the IRS process your mailed payment correctly. It should be detached from your Form 941 package and sent with your check or money order.

Remember, mailing payments carries inherent risks, including potential delays, loss, or misdirection, which could result in late payment penalties.

Deposit Schedules: Understanding Your Obligation

Beyond choosing a payment method, employers must understand their federal tax deposit schedule, which dictates when payments are due. There are two main schedules:

- Monthly Deposit Schedule: If your total tax liability for the lookback period (a 12-month period ending June 30 of the prior year) was $50,000 or less, you are a monthly depositor. You must deposit your tax by the 15th day of the next month.

- Semiweekly Deposit Schedule: If your total tax liability for the lookback period was more than $50,000, you are a semiweekly depositor. If your payday is Wednesday, Thursday, or Friday, deposit the tax by the following Wednesday. If your payday is Saturday, Sunday, Monday, or Tuesday, deposit the tax by the following Friday.

Failure to follow the correct deposit schedule can result in substantial penalties, even if the taxes are paid by the Form 941 due date. Your payroll system or tax professional can help determine your correct deposit schedule.

Identifying the Correct Mailing Address for Form 941

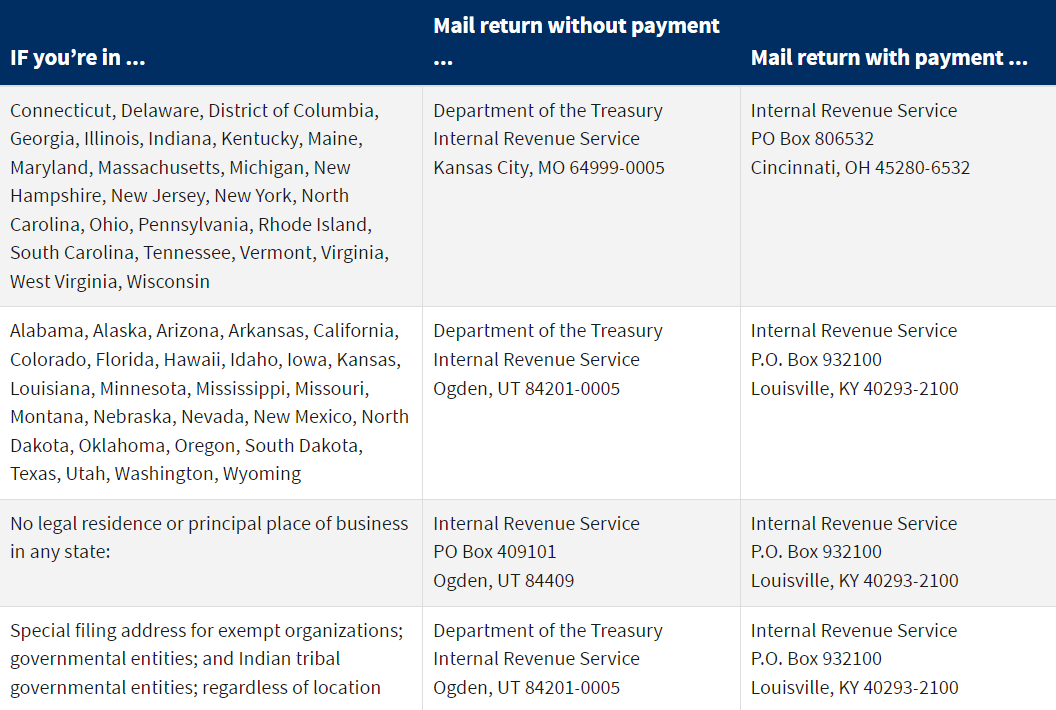

For the rare instances where mailing is permissible, knowing the exact IRS address is paramount. The IRS maintains several processing centers across the country, and the correct address for mailing Form 941 with payment depends on your business’s physical location and whether you are including a payment.

State-Specific IRS Mailing Addresses (General Rules)

The IRS publishes specific mailing addresses for Form 941 based on the state where your principal business, office, or agency is located. These addresses are subject to change, so always consult the latest IRS instructions for Form 941 (available on www.irs.gov) before mailing.

As a general guideline, the IRS differentiates between addresses for:

- Form 941 with a payment.

- Form 941 without a payment.

If you are mailing a payment, you must use the address designated for payments, which typically goes to a lockbox facility designed for secure payment processing. Sending a payment to an address for forms without payment can significantly delay processing and may lead to penalties.

Example (Illustrative – ALWAYS check current IRS instructions):

- For states like Connecticut, Delaware, District of Columbia, Florida, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin:

- With Payment: Internal Revenue Service, P.O. Box [Specific Box Number], [City, State]

- Without Payment: Department of the Treasury, Internal Revenue Service, [City, State, Zip]

- For states like Alabama, Arizona, Arkansas, California, Colorado, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming:

- With Payment: Internal Revenue Service, P.O. Box [Specific Box Number], [City, State]

- Without Payment: Department of the Treasury, Internal Revenue Service, [City, State, Zip]

It is critical to re-emphasize that these are illustrative examples. The IRS updates its addresses periodically, and referring to the most current Form 941 instructions (typically IRS Publication 15, Circular E, or the Form 941 instructions directly) is the only reliable way to get the correct address for your specific situation.

Special Circumstances: No Payment, Exempt Organizations

- No Payment: If you are filing Form 941 but have no payment due (e.g., you’ve already made all your deposits via EFTPS), you will send your form to a different IRS address than if you were including a payment. These addresses are typically standard IRS service centers.

- Exempt Organizations and Government Entities: While most employers use the standard Form 941, certain tax-exempt organizations and governmental entities may have specific instructions or addresses. Always verify.

Importance of Using the Most Current Address

Using an outdated address is a common error that can lead to significant headaches. Mailed payments or forms sent to the wrong address can be delayed, lost, or returned, potentially resulting in late filing or payment penalties. Always download the current year’s Form 941 instructions from the IRS website (irs.gov) to ensure you have the most up-to-date information for both the form itself and the mailing addresses. This simple diligence can save your business from considerable financial repercussions.

Deadlines, Penalties, and Best Practices for Timely Filing

Beyond understanding what and where to send, knowing when to send is equally critical. Missed deadlines and inadequate attention to detail can trigger a cascade of financial penalties, impacting a business’s bottom line.

Quarterly Filing Deadlines

Form 941 is filed quarterly, with specific due dates for each period:

- Quarter 1 (January 1 – March 31): Due April 30

- Quarter 2 (April 1 – June 30): Due July 31

- Quarter 3 (July 1 – September 30): Due October 31

- Quarter 4 (October 1 – December 31): Due January 31 of the next year

If a due date falls on a weekend or legal holiday, the deadline shifts to the next business day. It’s important to note that these are filing deadlines for the form. Deposit deadlines for taxes withheld are often much earlier, as discussed in the deposit schedules section.

Consequences of Late Filing or Payment

The IRS imposes strict penalties for non-compliance. These can include:

- Failure to File Penalty: A penalty of 5% of the unpaid tax for each month or part of a month that a return is late, capped at 25% of your unpaid tax.

- Failure to Pay Penalty: A penalty of 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25%. This penalty applies even if you file on time but don’t pay.

- Failure to Deposit Penalty: This is often the most significant penalty for employers. It ranges from 2% to 15% depending on how late the deposit is made relative to the required deposit date. If you fail to follow your specific deposit schedule (monthly vs. semiweekly), this penalty will apply even if you pay the full amount by the Form 941 filing deadline.

- Interest: In addition to penalties, interest may be charged on underpayments from the date the tax was due until it is paid in full.

These penalties accumulate rapidly, underscoring the necessity of diligent and timely compliance.

Best Practices for Ensuring Compliance

To mitigate risks and ensure smooth tax operations, employers should adopt several best practices:

- Automate Payroll: Utilize robust payroll software that calculates withholdings, tracks deposits, and generates Form 941 accurately. Many systems can also automate EFTPS payments.

- Maintain Accurate Records: Keep meticulous records of all wages paid, taxes withheld, and tax deposits made. This includes payroll journals, bank statements, and EFTPS confirmation numbers.

- Stay Informed: Regularly review IRS publications and updates regarding payroll taxes. Tax laws can change, and staying current is vital.

- Set Reminders: Implement a system of reminders for deposit deadlines and Form 941 filing deadlines. Calendar alerts, email notifications, or integrated payroll software features can be invaluable.

- Reconcile Quarterly: Before filing Form 941, reconcile your payroll records with your general ledger and the total deposits made. This helps catch discrepancies early.

- Plan for Contingencies: Have a plan for tax compliance even if key personnel are unavailable. Cross-training staff or having a trusted external advisor can prevent last-minute crises.

Leveraging Financial Tools and Professional Help

Managing payroll taxes can be complex, especially for growing businesses. Fortunately, a range of financial tools and professional services exist to streamline the process and ensure compliance, ultimately contributing to better business finance management.

Payroll Software Integration

Modern payroll software is arguably the most powerful tool for managing Form 941 and associated payments. Solutions like QuickBooks Payroll, Gusto, ADP, or Paychex offer comprehensive features:

- Automated Calculation: Accurately calculate federal income tax, Social Security, and Medicare withholdings based on current tax tables.

- Deposit Reminders and Automation: Many systems track your deposit schedule and can initiate EFTPS payments directly or provide clear reminders.

- Form Generation: Automatically populate Form 941 with all necessary data, minimizing manual entry errors.

- Record Keeping: Maintain digital records of all payroll activity, making it easy to reconcile and audit.

Investing in a reliable payroll system can significantly reduce the administrative burden and enhance accuracy, allowing business owners to focus on core operations.

The Role of Accountants and Tax Professionals

For businesses with intricate payroll structures, high employee turnover, or simply a desire for expert oversight, engaging an accountant or tax professional is a prudent financial decision. These professionals can:

- Determine Correct Deposit Schedules: Ensure your business adheres to the correct monthly or semiweekly deposit schedule.

- Prepare and File Form 941: Accurately complete and file your Form 941, including any necessary adjustments.

- Manage EFTPS Payments: Handle or oversee your federal tax payments through EFTPS.

- Represent Your Business: Act as a liaison with the IRS in case of inquiries, audits, or notices.

- Offer Strategic Advice: Provide insights on tax planning, employee benefits, and other financial strategies that impact payroll.

The cost of professional services is often outweighed by the value of peace of mind, penalty avoidance, and the opportunity to optimize your financial operations.

Keeping Meticulous Records

Regardless of whether you use software, a professional, or manage everything yourself, maintaining meticulous records is non-negotiable. This includes:

- Copies of all filed Forms 941.

- Records of all federal tax deposits (EFTPS confirmation numbers, cancelled checks, bank statements).

- Employee wage and withholding records.

- Correspondence with the IRS.

These records should be kept for at least four years from the date the tax was due or paid, whichever is later, as they are essential for audits, responding to IRS notices, and historical financial analysis. Proper record-keeping is a foundational element of sound business finance and tax compliance.

In conclusion, understanding where to send Form 941 with payment is a crucial aspect of business finance. While electronic payments via EFTPS are the standard and preferred method, knowing the specific mailing addresses and adhering to strict IRS guidelines for physical mail remains essential for scenarios where it’s permitted. By prioritizing accurate preparation, timely submission, leveraging appropriate financial tools, and, when necessary, seeking professional guidance, employers can confidently navigate their quarterly payroll tax obligations, ensuring compliance and maintaining a healthy financial standing. Always refer to the most current IRS instructions and publications for the definitive guidance applicable to your business.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.