The question of “where to pay taxes” has evolved from a simple logistical query into a complex strategic consideration for individuals and business owners alike. In an era defined by remote work, globalized trade, and digital entrepreneurship, understanding your fiscal residency and the appropriate channels for settlement is the cornerstone of sound financial management. Whether you are a salaried employee, a freelancer with a burgeoning side hustle, or a corporate entity scaling across borders, navigating the tax landscape requires more than just knowing a deadline; it requires a deep understanding of jurisdictional rules and the financial tools available to streamline the process.

This guide explores the multifaceted nature of tax obligations, focusing on the “where” from both a geographical and a platform-based perspective, ensuring your personal and business finances remain compliant while optimizing for long-term growth.

Understanding Jurisdictional Obligations: Determining Your Tax Home

Before clicking “pay” on a digital portal, you must first identify which governing body has the legal right to tax your income. This is known as establishing your “tax home” or tax residency. For most, this is straightforward—it is the place where you live and work. However, for the modern professional, this has become increasingly nuanced.

Resident vs. Non-Resident Tax Status

Most countries operate on a residency-based tax system. If you spend more than 183 days in a particular jurisdiction, you are typically deemed a tax resident, making you liable for taxes on your global income in that location. However, the United States is a notable exception, practicing citizenship-based taxation. This means U.S. citizens must report income to the IRS regardless of where they reside globally.

Distinguishing between resident and non-resident status is vital for financial planning. Non-residents are often only taxed on income sourced within that specific country (e.g., rental income from a property located there), whereas residents face a much broader net. Misidentifying your status can lead to double taxation or significant legal penalties.

The Impact of Remote Work and Digital Nomadism

The rise of the “digital nomad” has forced a total re-evaluation of where taxes are paid. If you are a resident of Florida but spend six months working from a co-working space in Portugal, where do you owe money? “Nexus” is the legal term for a connection between a taxpayer and a jurisdiction.

For remote workers, nexus is usually established where the work is physically performed. This can lead to “multi-state” or “multi-national” filing requirements. From a personal finance perspective, this necessitates meticulous record-keeping. You must track your days spent in different regions to ensure you are paying the correct amount to the correct local authority, preventing future audits and ensuring you take advantage of any available tax treaties.

Digital Platforms and Modern Payment Portals: Navigating the “Where” Online

Once you have identified your obligations, the next hurdle is the physical act of payment. Gone are the days of mailing paper checks as the primary method. Modern financial tools have digitized the process, offering more security and better tracking for your personal ledgers.

Direct Government Portals and Electronic Systems

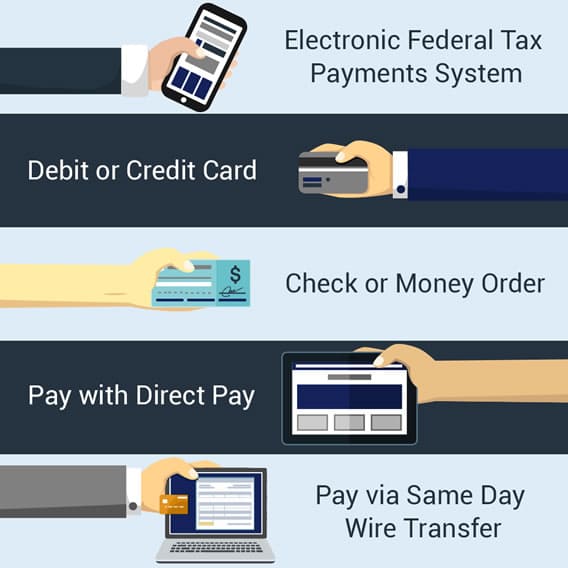

For federal obligations in the United States, the IRS provides “Direct Pay,” a secure service to pay your individual tax bill or estimated tax directly from your checking or savings account at no cost. This is the gold standard for personal finance management because it provides an immediate confirmation number, which is essential for your financial records.

For businesses, the Electronic Federal Tax Payment System (EFTPS) is the mandatory route for many. It is a more robust system designed to handle payroll taxes, corporate income taxes, and excise taxes. Leveraging these direct government portals is the safest way to ensure funds are credited correctly without the intervention of third-party processors who might charge convenience fees.

Integrating Tax Payments with Financial Management Software

For those managing multiple income streams or small businesses, the “where” is often integrated directly into their accounting ecosystem. Platforms like QuickBooks, Xero, or specialized tax software allow users to calculate their liabilities and, in many cases, initiate the payment directly through an integrated e-file system.

This integration is a powerful financial tool. By syncing your bank accounts with your tax software, you can see a real-time estimate of what you owe throughout the year. This prevents the “tax season shock” and allows for better cash flow management, ensuring that the money you “pay” at the end of the year has been strategically set aside in interest-bearing accounts until the moment it is due.

Strategic Financial Management for Small Businesses and Freelancers

For those in the “Money” niche—freelancers, entrepreneurs, and side-hustlers—paying taxes is not a once-a-year event. It is a quarterly responsibility that requires a proactive financial strategy.

Estimating and Paying Quarterly Taxes

The IRS and many state authorities operate on a “pay-as-you-go” basis. If you expect to owe more than $1,000 in taxes for the year, you are generally required to make quarterly estimated payments. This changes the “where” from a single annual destination to a recurring line item in your business budget.

Using Form 1040-ES, freelancers must calculate their expected adjusted gross income, taxable income, taxes, deductions, and credits for the year. Strategically, it is often wise to pay slightly more than the “safe harbor” amount (usually 100% or 110% of last year’s tax) to avoid underpayment penalties. Paying these through the online portals mentioned earlier ensures that your business credit remains unsullied and your financial compliance is airtight.

High-Yield Accounts for Tax Reserves

A sophisticated approach to paying taxes involves “The Sinking Fund” method. Instead of letting tax money sit in a primary business checking account where it might be accidentally spent on operational costs, savvy financial managers move 20–30% of every incoming payment into a dedicated high-yield savings account (HYSA).

By doing this, the money earns interest for you until the quarterly deadline arrives. In this scenario, “where you pay from” becomes just as important as “where you pay to.” Using a high-yield account for your tax reserves turns a liability into a small, interest-generating asset during the holding period.

Navigating International Tax Obligations and Global Compliance

As businesses expand and individuals invest in foreign markets, the question of where to pay taxes extends beyond national borders. This requires an understanding of international law and specialized financial instruments.

Double Taxation Agreements (DTAs)

To prevent taxpayers from paying income tax twice on the same earnings, many countries have entered into Double Taxation Agreements. If you are an investor receiving dividends from a foreign corporation, or a consultant working for a firm in London while based in New York, these treaties determine which country has the primary taxing right.

From a wealth-management perspective, leveraging DTAs is essential. It usually involves filing a “Tax Residency Certificate” from your home country to the foreign entity to ensure taxes are withheld at a reduced rate or not at all. Knowing “where” the treaty places the burden allows you to keep more of your hard-earned capital.

Value Added Tax (VAT) and Digital Sales Tax

For those involved in online income and e-commerce, the “where” involves the location of the customer, not just the business. Many jurisdictions now require digital sellers to collect and remit Value Added Tax (VAT) or Goods and Services Tax (GST) based on the buyer’s location.

This has led to the rise of “Merchant of Record” services. These are financial tools that handle the tax collection and remittance on behalf of the business. By using a Merchant of Record, a business owner offloads the complex task of figuring out where to pay sales taxes in 50 different countries, allowing them to focus on scaling their brand and increasing their profit margins.

Leveraging Professional Services and Financial Tools for Accuracy

The final piece of the puzzle in determining where and how much to pay is the human and technological element. Financial literacy involves knowing when to automate and when to consult an expert.

The Role of Certified Public Accountants (CPAs)

While software can handle the “where” for basic filings, a CPA or tax strategist is invaluable for complex financial structures. They provide insight into “where” you can legally avoid taxes through credits, deductions, and strategic entities like S-Corps or LLCs. A professional can look at your entire financial portfolio—investments, real estate, and business income—to ensure that the money you pay is the absolute legal minimum, rather than a penny more.

Tax Software vs. Manual Filing

For the vast majority of personal finance needs, tax software has rendered manual filing obsolete. These tools act as a bridge between your bank accounts and the government portals. They provide a logical flow, asking questions that help identify “where” you might have hidden tax liabilities or benefits, such as student loan interest or home office deductions.

In conclusion, “where to pay taxes” is a question that encompasses your physical location, your digital presence, and your strategic financial choices. By utilizing direct government payment portals, maintaining dedicated tax reserves in high-yield accounts, and understanding the nuances of nexus and international treaties, you can transform tax compliance from a stressful annual chore into a streamlined component of your broader financial success. Proper tax management is not just about following the law; it is about protecting your liquidity and ensuring the long-term health of your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.