Navigating the landscape of higher education financing is one of the most significant financial decisions a student or parent will ever make. With the rising costs of tuition, room, and board, understanding exactly where to get student loans—and how to evaluate them—is essential for long-term financial health. The “where” of student loans is generally split into two primary camps: the federal government and private financial institutions. Choosing the right source requires a deep dive into interest rates, repayment flexibility, and borrower protections.

1. The Foundation of Student Financing: Federal Student Loans

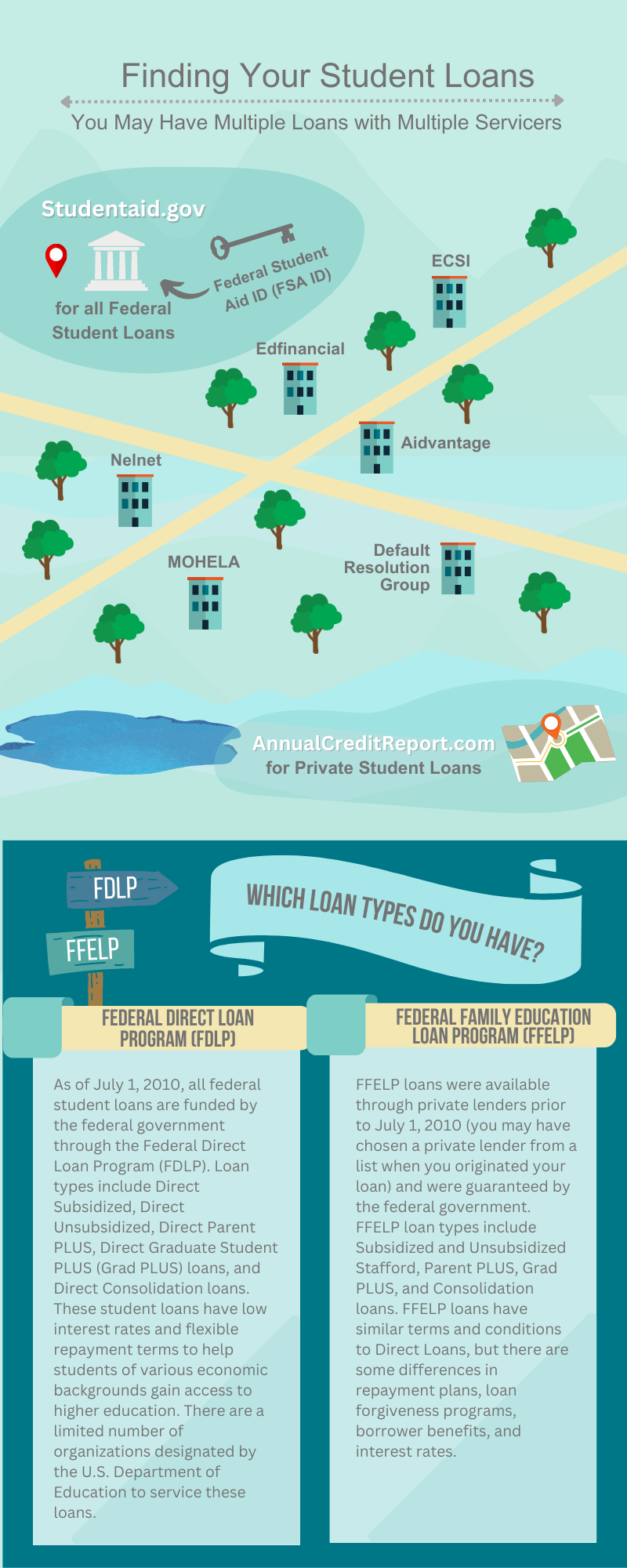

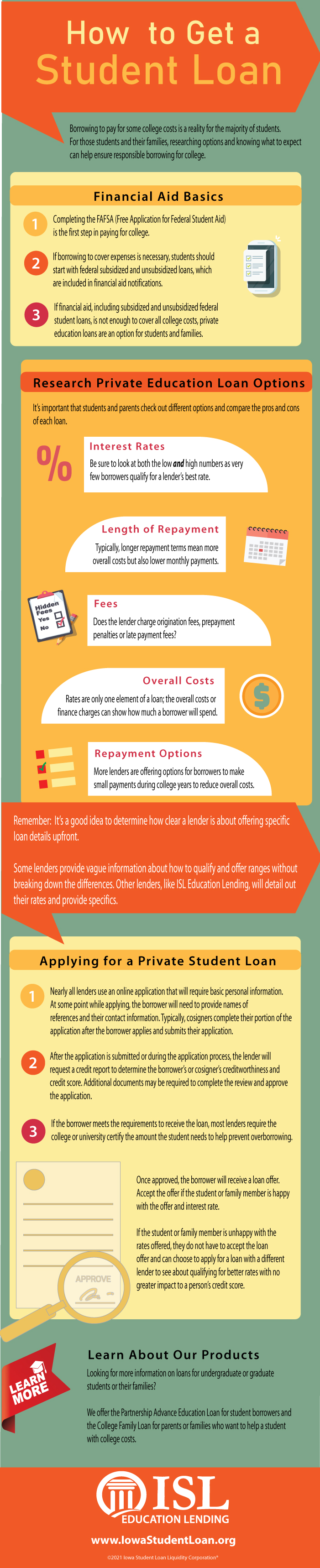

Before exploring private markets, the first destination for any borrower should be the U.S. Department of Education. Federal student loans are funded by the government and offer unique benefits that private lenders rarely match, such as income-driven repayment plans and potential loan forgiveness.

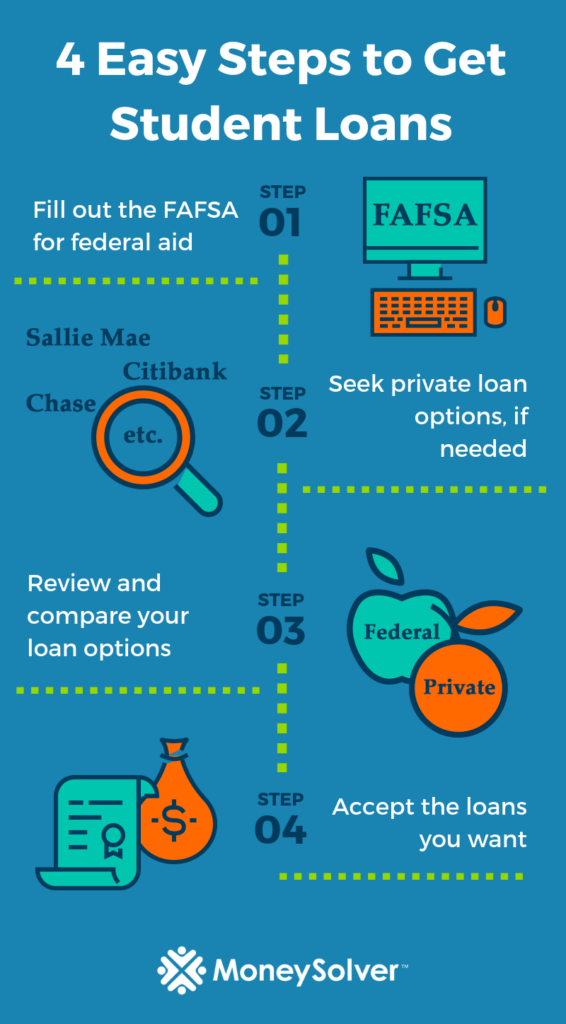

The Critical Role of the FAFSA

To access federal loans, the journey begins with the Free Application for Federal Student Aid (FAFSA). This document assesses your or your family’s financial strength and determines your eligibility for various types of federal aid. It is the gatekeeper not only for loans but also for grants and work-study programs that do not need to be repaid.

Direct Subsidized vs. Unsubsidized Loans

For undergraduate students, federal loans are categorized into two main types. Direct Subsidized Loans are available to students with demonstrated financial need. The most significant advantage here is that the government pays the interest while you are in school at least half-time. Direct Unsubsidized Loans, on the other hand, are available to all students regardless of need, but interest begins accruing as soon as the loan is disbursed.

PLUS Loans for Parents and Graduate Students

If the standard undergraduate limits are not enough to cover the cost of attendance, the government offers PLUS loans. These are available to the parents of dependent undergraduate students (Parent PLUS) and to graduate or professional students (Grad PLUS). Unlike standard direct loans, PLUS loans require a basic credit check, and they typically carry higher interest rates and origination fees.

2. Exploring the Private Market: Banks and Online Lenders

When federal loan limits are reached or if a borrower does not qualify for federal aid, the private sector offers a variety of alternatives. Private student loans are issued by banks, credit unions, and specialized online lenders. Unlike federal loans, these are strictly credit-based, meaning your credit score and income (or those of a cosigner) will dictate your interest rate and approval.

Traditional National Banks

Many large-scale commercial banks offer student loan products. These institutions often provide the comfort of a well-established brand and the convenience of managing your student loans alongside your checking or savings accounts. However, because these are profit-driven entities, their interest rates may be higher for those without pristine credit, and their repayment flexibility is often more rigid than federal options.

FinTech and Online-Only Lenders

The last decade has seen a surge in financial technology (FinTech) companies specializing in student lending. These platforms often use proprietary algorithms to assess creditworthiness, sometimes looking beyond just a FICO score to consider a student’s major or future earning potential. Online lenders are known for streamlined application processes, competitive fixed and variable rates, and lower overhead costs, which they often pass on to the borrower in the form of lower fees.

Specialized Lenders for Graduate Professionals

Some private lenders cater specifically to high-earning potential fields, such as law, medicine, or MBA programs. These lenders understand the specific career trajectories of these professions and may offer tailored repayment terms, such as lower payments during residency or clerkships, making them a niche but valuable “where” for professional students.

3. Community-Based Options: Credit Unions and State Agencies

Beyond the major national players, there are localized and membership-based sources for student loans that frequently offer more personalized service and competitive rates.

The Credit Union Advantage

Credit unions are member-owned, non-profit cooperatives. Because they do not have to answer to shareholders, they often provide lower interest rates on loans compared to commercial banks. Many credit unions offer “private student loan” products designed to fill the gap left by federal aid. To access these, you usually need to meet membership requirements, which could be based on your location, employer, or school.

State-Sponsored Education Agencies

Many states have their own higher education authorities or non-profit agencies that offer student loan programs. These agencies are designed to help residents or students attending schools within that state. State-based loans often feature fixed interest rates that are competitive with federal PLUS loans and sometimes include “bridge” funding options for students who need a small amount of capital to finish their final semester.

Institutional Loans from Universities

In some cases, the “where” is the school itself. Some colleges and universities have their own endowment-funded loan programs. These are typically reserved for students who have exhausted all other options. While they can be a lifesaver, it is important to scrutinize the terms, as these loans may not have the same deferment or forbearance options as federal or major private loans.

4. Key Metrics for Comparing Loan Providers

Identifying where to get student loans is only half the battle; the other half is evaluating which source offers the most sustainable financial terms. When comparing lenders, a borrower must look past the monthly payment and analyze the total cost of the debt.

Fixed vs. Variable Interest Rates

Federal loans always offer fixed interest rates, meaning the rate remains the same for the life of the loan. Private lenders, however, often offer a choice between fixed and variable rates. A variable rate might start lower than a fixed rate, but it can fluctuate based on market conditions, potentially increasing your monthly obligation significantly over time. For long-term debt like a student loan, fixed rates are generally considered the safer bet for financial planning.

Understanding APR and Origination Fees

The Annual Percentage Rate (APR) is a more accurate measure of the cost of a loan than the interest rate alone, as it includes fees. Some lenders, particularly for federal PLUS loans or certain private products, charge an “origination fee”—a percentage of the loan amount taken off the top. If one lender offers a 5% interest rate with a 4% fee and another offers a 5.5% rate with no fee, the latter may actually be cheaper in the long run.

Repayment Terms and Grace Periods

The “grace period” is the amount of time you have after graduation before you must start making full payments. While federal loans typically offer a six-month grace period, private lenders vary wildly. Some require interest-only payments while you are in school, while others allow full deferment. Additionally, look for “co-signer release” options in private loans, which allow the primary borrower to take full responsibility for the loan after making a certain number of on-time payments, thereby protecting the co-signer’s credit.

5. Strategic Alternatives to Minimize Loan Reliance

Before finalizing any loan agreement, it is prudent to explore sources of capital that do not involve debt. The best “where” for funding is always a source that doesn’t require repayment.

Maximize Grants and Scholarships

Every dollar found in grants or scholarships is a dollar you don’t have to borrow at interest. Beyond the federal Pell Grant, look for “merit-based” scholarships from the university or “niche” scholarships from private organizations. These can be based on anything from ethnic background and religious affiliation to specific hobbies or intended career paths.

Employer Assistance and Tuition Reimbursement

For those working while in school, or for graduate students already in the workforce, employer assistance is a powerful tool. Many companies offer tuition reimbursement programs (up to $5,250 per year tax-free in the U.S.) as a fringe benefit. This can significantly reduce the total amount of student loans needed.

Refinancing as a Post-Graduation Strategy

The lender you choose today doesn’t have to be your lender forever. Once you graduate and secure a stable income, you may qualify for student loan refinancing. This involves taking out a new loan with a private lender at a lower interest rate to pay off your existing federal or private loans. While this can save thousands in interest, be aware that refinancing federal loans into a private loan means giving up federal protections like income-driven repayment and forgiveness programs.

In conclusion, knowing where to get student loans involves a tiered approach: start with the federal government to secure protections and lower-cost subsidized options, then look to reputable private lenders or credit unions to bridge any remaining gaps. By carefully comparing interest rates, fees, and repayment terms, you can finance your education without compromising your future financial stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.