Navigating the labyrinthine world of home buying can be daunting, but one of the most crucial initial steps, and often the most empowering, is securing a pre-approval for a home loan. This isn’t just a bureaucratic hurdle; it’s a strategic financial maneuver that provides clarity, credibility, and a significant advantage in a competitive housing market. For many prospective homeowners, the question isn’t just how to get pre-approved, but more importantly, where to turn for this essential financial green light. Understanding the landscape of lenders and the nuances of the pre-approval process can make all the difference between a smooth journey to homeownership and one fraught with uncertainty.

Understanding Home Loan Pre-Approval: Why It Matters

Before diving into the “where,” it’s critical to grasp the “why.” Pre-approval is a formal commitment from a lender, contingent on certain conditions, to lend you a specific amount of money. It’s a powerful tool that transforms you from a casual browser into a serious buyer.

Differentiating Pre-Qualification vs. Pre-Approval

It’s common for first-time buyers to confuse pre-qualification with pre-approval, but the two are distinct. Pre-qualification is an informal estimate of how much you might be able to borrow, based on a brief conversation or questionnaire about your income, debts, and assets. It involves no credit check and carries no weight in an offer.

Pre-approval, on the other hand, is a much more rigorous process. It involves a detailed review of your financial history, including a hard credit inquiry, verification of income and assets, and an assessment of your debt-to-income ratio. The result is a pre-approval letter, a document that states the maximum loan amount you qualify for, often specifying the loan type and potential interest rate. This letter is gold in the housing market.

The Strategic Advantages of Being Pre-Approved

Possessing a pre-approval letter offers several undeniable advantages:

- Clarity on Affordability: It provides a realistic budget, allowing you to focus your home search on properties you can genuinely afford, saving time and preventing disappointment.

- Enhanced Buyer Credibility: When you make an offer on a home, a pre-approval letter signals to sellers that you are a serious, qualified buyer capable of securing financing. In multiple-offer situations, this can give you a significant edge over buyers who are not yet pre-approved.

- Faster Closing Process: Since much of the financial vetting has already occurred, the mortgage process can move more quickly once you find a home, potentially leading to a smoother closing.

- Negotiating Power: Knowing your financial limits allows you to negotiate with confidence, understanding precisely what you can commit to.

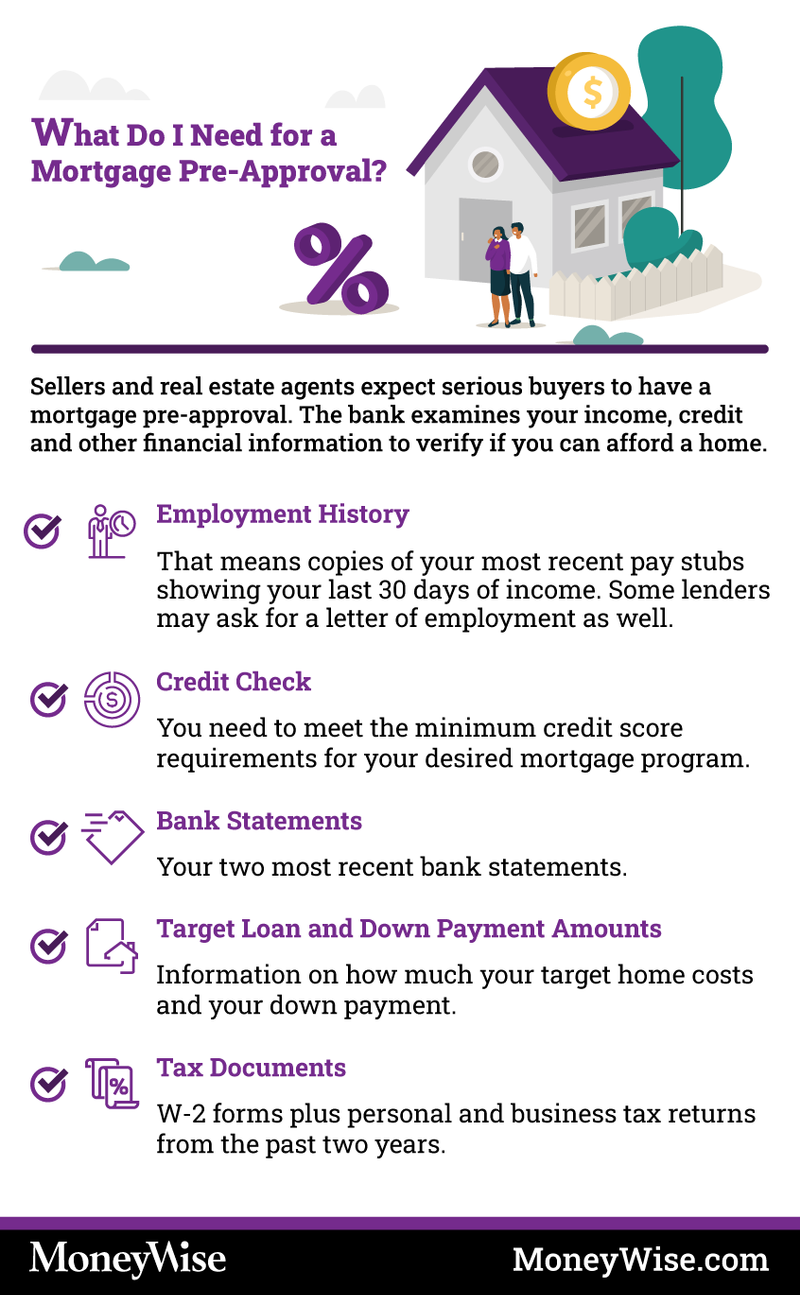

Key Documents Required for Pre-Approval

To streamline the process, gather these documents in advance:

- Identification: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs (last 30-60 days), W-2 forms (last two years), tax returns (last two years if self-employed or complex income).

- Proof of Assets: Bank statements (last two months for checking/savings), investment account statements.

- Credit History Information: While the lender will pull your credit report, having an idea of your score and any major debts can be helpful.

- Debt Information: Statements for credit cards, auto loans, student loans, or any other outstanding debts.

Navigating the Landscape of Pre-Approval Lenders

The financial industry offers a diverse array of lenders, each with its own advantages and disadvantages. Choosing the right one depends on your specific financial situation, preferences, and priorities.

Traditional Banks and Credit Unions

These are the financial institutions most people are familiar with. Large national banks (e.g., Chase, Bank of America, Wells Fargo) offer a wide range of mortgage products, competitive rates, and the convenience of in-person service and established relationships if you’re already a customer. Regional and local banks often provide more personalized service and may be more flexible with borrowers who have unique financial circumstances.

Credit unions operate as not-for-profit organizations, often resulting in lower fees and potentially better interest rates for their members. They are known for their customer-centric approach and willingness to work closely with borrowers. However, you typically need to be a member to secure a loan, which involves meeting certain eligibility criteria.

Pros: Established reputation, in-person support, existing customer relationships can simplify process, diverse product offerings.

Cons: Potentially slower processing times, less flexibility on underwriting for non-standard cases, may not always have the absolute lowest rates.

Online Mortgage Lenders and Brokers

The digital age has brought forth a new breed of lenders specializing in online applications and processing. Companies like Rocket Mortgage (Quicken Loans), Better Mortgage, and LoanDepot offer streamlined digital experiences, often promising faster approvals and competitive rates due to lower overheads. They cater to tech-savvy borrowers comfortable managing their application entirely online.

Mortgage brokers, whether online or traditional, act as intermediaries. They don’t lend money themselves but work with multiple lenders to find the best loan product and rate for you. They can be invaluable if you have a complex financial situation, are looking for a niche product, or want someone to shop around on your behalf.

Pros: Often faster processing, competitive rates, convenient online experience, broad product selection (brokers).

Cons: Less personalized service (direct online lenders), reliance on technology, potential for overwhelming communication if working with multiple brokers.

Direct Lenders vs. Mortgage Brokers: Which is Right for You?

The choice between a direct lender (a bank, credit union, or online lender that originates and funds loans directly) and a mortgage broker largely depends on your comfort level and needs.

- Direct Lender: Choose a direct lender if you prefer a single point of contact, want to build a direct relationship with the institution, or have a straightforward financial profile that fits standard lending criteria. You’ll work directly with their loan officers and their specific product offerings.

- Mortgage Broker: Opt for a mortgage broker if you value personalized advice, have a unique financial situation (e.g., self-employed, fluctuating income), or want someone to compare rates and terms from multiple lenders on your behalf. A good broker can save you time and potentially money by finding a deal you might not discover on your own.

The Pre-Approval Process: A Step-by-Step Guide

Once you’ve decided on the type of lender, the pre-approval process itself follows a predictable path. Being prepared for each stage will expedite your journey.

Gathering Your Financial Documentation

As outlined earlier, having all your financial documents organized and readily accessible is the first critical step. This includes proof of income, assets, debts, and identification. The more organized you are, the smoother and faster the lender can process your application. Create a digital folder and a physical one for copies.

Submitting Your Application and Authorizing Credit Checks

With your documents in hand, you’ll complete a mortgage application, either online or with a loan officer. This application details your personal information, employment history, financial assets, and liabilities. At this stage, you’ll also authorize the lender to pull your credit report. This “hard inquiry” will temporarily ding your credit score by a few points, but the impact is usually minor and short-lived. It’s important to do all your rate shopping within a short window (typically 14-45 days, depending on the scoring model) to have multiple hard inquiries count as one for credit scoring purposes.

Receiving Your Pre-Approval Letter and Understanding Its Terms

If your financial profile meets the lender’s criteria, you will receive a pre-approval letter. This letter will clearly state:

- The maximum loan amount you qualify for.

- The type of loan (e.g., FHA, VA, Conventional).

- The estimated interest rate (though this is subject to change until you lock it in).

- Any specific conditions or contingencies for the final loan approval.

Crucially, read this letter carefully. Understand its expiration date (typically 60-90 days) and any fine print. This letter is your financial passport to the housing market.

Optimizing Your Financial Profile for Pre-Approval Success

Before even applying, there are proactive steps you can take to strengthen your financial standing and increase your chances of securing a favorable pre-approval.

Boosting Your Credit Score

Your credit score is a primary determinant of loan eligibility and interest rates. Lenders look for FICO scores, generally preferring 620+ for conventional loans, higher for the best rates. To improve your score:

- Pay Bills on Time: Payment history is the most significant factor.

- Reduce Credit Card Debt: Lowering your credit utilization ratio (amount of credit used vs. available) can significantly boost your score.

- Avoid New Debt: Don’t open new credit lines or make major purchases (like a new car) while applying for a mortgage.

- Check Your Credit Report: Dispute any errors with all three major credit bureaus (Equifax, Experian, TransUnion).

Managing Your Debt-to-Income (DTI) Ratio

Lenders use your DTI ratio to assess your ability to manage monthly payments and repay debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer a DTI of 43% or lower, though some programs allow for higher. To improve your DTI:

- Pay Down Existing Debts: Focus on credit cards and personal loans.

- Increase Income: If feasible, consider a side hustle or negotiate a raise.

- Avoid Taking on New Debt: This goes hand-in-hand with boosting your credit score.

Building a Strong Down Payment and Reserve Funds

While a 20% down payment is ideal to avoid Private Mortgage Insurance (PMI) on conventional loans, many loan programs allow for much lower down payments (e.g., 3.5% for FHA, 0% for VA/USDA). Regardless, having a solid down payment reduces the loan amount, lowers your monthly payments, and demonstrates financial responsibility.

Additionally, lenders like to see reserve funds—money left in savings after your down payment and closing costs. This indicates you have a financial cushion for unexpected expenses, making you a less risky borrower. Aim for at least 2-3 months of mortgage payments in reserves.

What to Do After Receiving Pre-Approval

Receiving your pre-approval letter is a major milestone, but the journey isn’t over. Strategic actions post-pre-approval are key to a successful home purchase.

Understanding the Validity Period

Remember, your pre-approval letter isn’t eternal. It typically expires after 60 to 90 days. This is because your financial situation can change, and interest rates fluctuate. If you haven’t found a home by then, you’ll need to re-apply, which means providing updated financial documents and potentially another hard credit inquiry. Keep track of this date and communicate with your lender if you anticipate needing an extension.

Shopping for Your Home with Confidence

With your pre-approval in hand, you can now confidently shop for homes within your approved budget. This clarity allows you to be more decisive and make strong offers, knowing your financial backing is solid. Share your pre-approval letter with your real estate agent so they can guide your search effectively and present you as a serious buyer to sellers.

Maintaining Financial Discipline Until Closing

The period between pre-approval and closing is critical. Any significant changes to your financial profile can jeopardize your final loan approval. Do NOT:

- Make large purchases: Avoid buying a new car, furniture, or making any big-ticket purchases on credit.

- Open new credit accounts: This can lower your credit score and change your DTI.

- Close existing credit accounts: While seemingly counterintuitive, closing old accounts can negatively impact your credit history length and utilization ratio.

- Change jobs: A change in employment, especially to a different field or with a probation period, can raise red flags for lenders.

- Make large, unexplained deposits: Lenders need to source all large deposits to ensure they aren’t undisclosed loans.

Stay in constant communication with your lender and real estate agent. If any financial changes are unavoidable, discuss them immediately to understand the potential implications.

In conclusion, securing a home loan pre-approval is an indispensable first step in the homeownership journey. By understanding where to seek pre-approval, preparing meticulously, and maintaining financial discipline, prospective homeowners can navigate the process with confidence, transforming the dream of owning a home into a tangible reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.