In the intricate world of personal finance, understanding the fundamental components of your banking operations is paramount. Among the most crucial pieces of information for any account holder are the routing number and the account number. These unique identifiers are not merely random digits; they are the bedrock upon which countless financial transactions are built, from setting up direct deposits to paying bills online and initiating wire transfers. Yet, despite their importance, many individuals might find themselves momentarily puzzled when asked to locate these numbers, especially if they infrequently use physical checks.

This comprehensive guide aims to demystify the structure of a check, revealing precisely where these vital numbers reside and explaining their distinct roles. More than just a simple “where to look,” we’ll delve into why these numbers are indispensable for managing your money effectively, explore alternative ways to access them, and underscore the critical importance of safeguarding this sensitive financial information. By the end, you’ll not only know exactly where to find your routing and account numbers but also possess a deeper understanding of their significance in your personal financial landscape.

Deconstructing the Check: A Visual Guide to Your Financial Identifiers

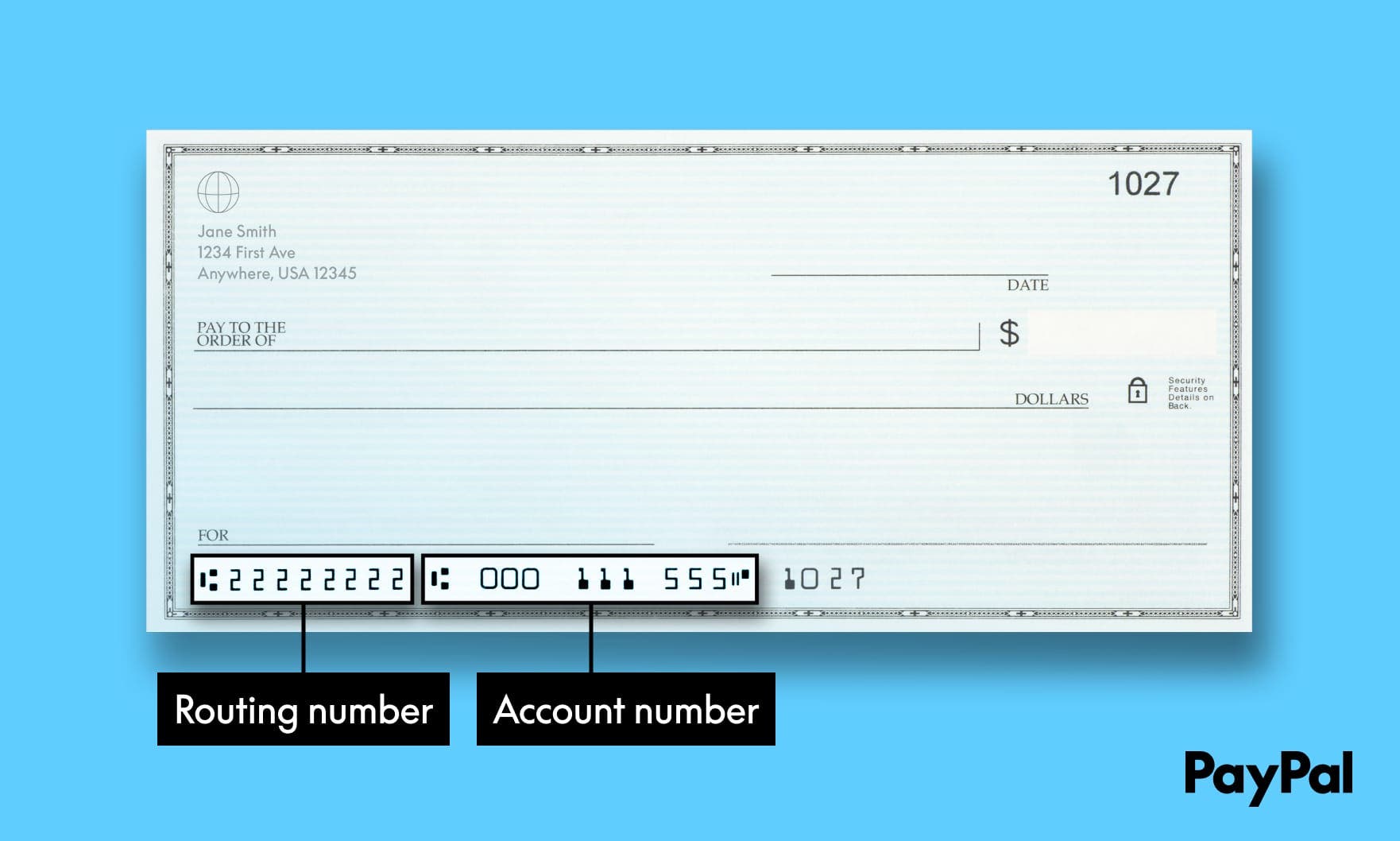

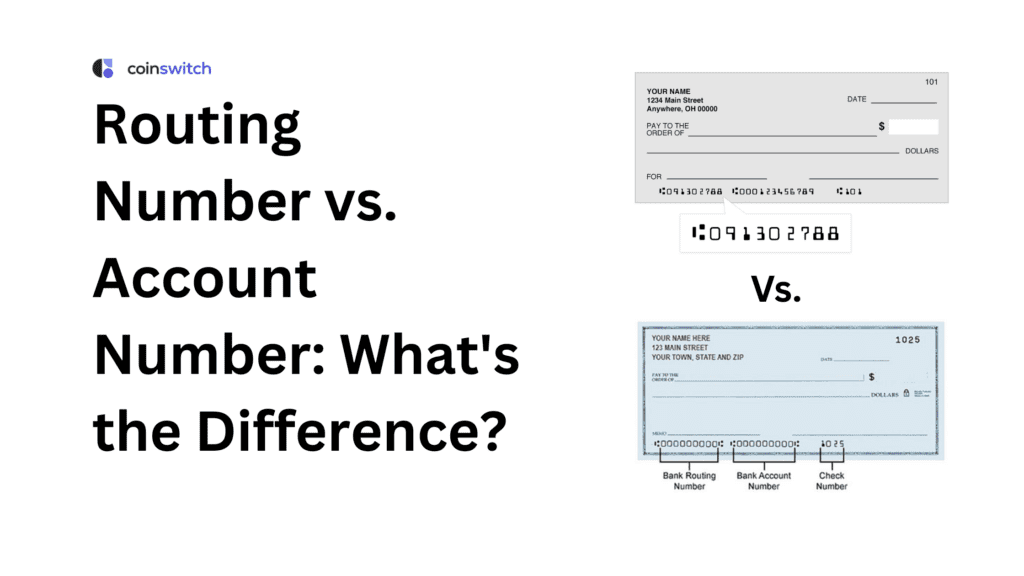

A physical check, though increasingly less common in daily transactions, remains a powerful instrument in banking. It’s a carefully structured document, each section serving a specific purpose. At the bottom of every check lies a sequence of magnetic ink characters, known as the Magnetic Ink Character Recognition (MICR) line. This line is specifically designed for automated processing by banks and contains the three most important identifiers: the routing number, the account number, and the check number. Understanding the placement and purpose of each can save you time and prevent errors in financial transactions.

The Routing Number: Your Bank’s Identity

The routing number is arguably the most public-facing of the three critical numbers on a check, primarily because it identifies your specific financial institution and its location within the U.S. banking system. This nine-digit code acts like a unique postal code for your bank, directing funds to the correct financial institution for processing.

Where to Find It: On most standard U.S. checks, the routing number is the first set of nine digits located at the bottom-left corner of the check, within the MICR line. It’s often enclosed by a colon-like symbol on either side.

What It Means: Officially known as an American Bankers Association (ABA) routing transit number, it was initially created in 1910 to process paper checks. Today, it facilitates a wide array of electronic transactions, including Automated Clearing House (ACH) payments like direct deposits and automatic bill payments, as well as wire transfers. It’s crucial to understand that while the routing number on your check is valid for most standard transactions, some banks may have a different routing number specifically for wire transfers. Always verify with your bank if you are initiating a wire transfer, as using the wrong one could delay or misdirect funds.

The Account Number: Your Unique Identifier

While the routing number identifies your bank, the account number points directly to your specific account within that bank. This is your personal identifier, distinguishing your funds from every other customer’s funds at the same institution.

Where to Find It: The account number is typically the second set of numbers in the MICR line, positioned to the right of the routing number. Its length can vary significantly, usually ranging from 10 to 12 digits, but sometimes shorter or longer depending on the bank.

What It Means: This number is unique to your individual checking account. Every transaction that debits or credits your account will utilize this number. It is the most sensitive piece of information on your check, as it directly links to your funds. When setting up direct deposit, automatic payments, or needing to provide your bank details for various financial services, this is the number, along with your routing number, that you will provide. Accuracy here is paramount, as a single incorrect digit can lead to funds being deposited into the wrong account or payments failing entirely.

The Check Number: Tracking Your Transactions

Though not always required for digital transactions, the check number plays an important role in tracking and record-keeping for both you and your bank.

Where to Find It: The check number is typically the third set of numbers in the MICR line, located to the right of your account number, often at the far right. You’ll also find this number printed prominently in the top right corner of the check.

What It Means: This sequential number allows you to keep track of individual checks you’ve written, making reconciliation of your bank statements much easier. Each check in your checkbook will have a unique, sequential number. When you write a check, you typically record this number in your check register along with the payee and amount, providing a clear audit trail for your expenditures.

Why These Numbers Matter: Essential Use Cases in Personal Finance

Understanding where to find your routing and account numbers is just the first step; knowing why they are so critical to various financial operations is equally important. These numbers are the keys to unlocking seamless money management, enabling everything from receiving your salary to paying your mortgage.

Setting Up Direct Deposit

One of the most common and beneficial uses of your routing and account numbers is for direct deposit. Whether it’s your salary, government benefits, or tax refunds, direct deposit ensures that funds are transferred electronically and directly into your bank account, bypassing physical checks and manual deposits. To set this up, your employer or the paying entity will typically require both your bank’s routing number and your specific account number to ensure the funds reach the correct destination quickly and securely. This system is not only convenient but also enhances financial security by reducing the risk of lost or stolen checks.

Making Online Bill Payments

In today’s digital age, online bill payment is a cornerstone of efficient personal finance. Many service providers, utility companies, and lenders offer options to pay bills directly from your bank account. This often involves providing your routing and account numbers to authorize recurring or one-time electronic withdrawals. This method streamlines your monthly obligations, helps avoid late fees, and provides a clear digital record of transactions, making budgeting and financial tracking much simpler.

Initiating Wire Transfers

Wire transfers are a fast and reliable way to send funds, especially for large amounts or international transactions. Unlike ACH payments which can take a few business days, wire transfers are often processed within hours. When initiating a wire transfer, you will almost always need the recipient’s bank’s routing number and their account number. As mentioned earlier, it’s crucial to confirm the specific wire transfer routing number with your bank, as it can sometimes differ from the standard routing number printed on your checks. Accuracy is paramount here, as wire transfers are often irreversible.

ACH Payments and Electronic Fund Transfers (EFTs)

Beyond direct deposit and online bill payments, your routing and account numbers facilitate a broader category of transactions known as ACH payments or Electronic Fund Transfers (EFTs). This encompasses various electronic money movements, from sending money to friends via peer-to-peer payment apps (often linking to your bank account) to making investments or contributing to savings accounts. These numbers are the backbone of the electronic financial system, enabling a vast network of digital transactions that keep the economy moving.

Ordering New Checks

Paradoxically, even when ordering new checks, you’ll need to provide your bank’s routing number and your account number to the check printing company. This ensures that the new checks are correctly pre-printed with your specific banking information, ready for use. This process underscores the foundational role these numbers play in identifying your bank and your individual account.

Beyond the Physical Check: Alternative Ways to Find Your Numbers

While your physical check is the most straightforward place to find these numbers, situations arise where you might not have a check handy. Fortunately, modern banking offers several convenient alternatives to access your routing and account numbers without needing a paper check.

Online Banking Portals

Virtually all financial institutions provide robust online banking platforms. Once you log in to your account, you can typically find your routing and account numbers displayed prominently on your account summary page, or within a section dedicated to account details, statements, or direct deposit information. Many banks also offer a dedicated “Direct Deposit Form” or “Account Information” section that explicitly lists these numbers for easy reference. This is often the quickest and most accessible method.

Bank Statements

Your monthly bank statements, whether physical or electronic, are another reliable source for your account and routing numbers. The account number is always clearly listed at the top of the statement, identifying the account it pertains to. The routing number, while not always as prominently displayed as on a check, is typically found near your bank’s address or in the fine print regarding electronic transfers or direct deposit instructions. Keep past statements accessible, perhaps digitally archived, for quick reference.

Mobile Banking Apps

In an increasingly mobile-first world, banking apps have become indispensable. Most major bank apps allow you to view your account details, including your routing and account numbers, directly on your smartphone or tablet. After logging in securely, navigate to your account details or settings section. Some apps even have a dedicated “Direct Deposit Info” button that instantly pulls up the necessary details. Always ensure you are using the official app from your bank and not a third-party application.

Contacting Your Bank Directly

If all else fails, or if you prefer a direct human interaction, you can always contact your bank. Customer service representatives can securely provide you with your routing and account numbers after verifying your identity. You can typically reach them via phone, through a secure message within your online banking portal, or by visiting a local branch in person. This method is particularly useful if you have multiple accounts and need to confirm which set of numbers corresponds to a specific account.

Safeguarding Your Financial Information: A Top Priority

Knowing where to find your routing and account numbers is essential, but understanding the importance of protecting them is even more critical. These numbers, especially when combined, can be used to access your funds or initiate unauthorized transactions. Vigilance and smart security practices are paramount in today’s digital financial landscape.

The Risks of Sharing Too Freely

While necessary for legitimate transactions, indiscriminately sharing your routing and account numbers can expose you to risks. If these numbers fall into the wrong hands, they could potentially be used for fraudulent activities, such as creating fake checks, making unauthorized withdrawals, or setting up unauthorized direct debits. While banks have robust fraud protection, prevention is always better than cure. Be cautious about who you provide this information to and ensure the request comes from a legitimate source.

Best Practices for Security

- Shred Old Checks: Before discarding old checkbooks or voided checks, always shred them to prevent sensitive information from being retrieved.

- Secure Online Access: Use strong, unique passwords for your online banking and mobile apps. Enable two-factor authentication (2FA) whenever possible for an added layer of security.

- Verify Requests: If someone asks for your routing and account numbers, verify their legitimacy. Be wary of unsolicited emails, calls, or texts asking for this information, as they could be phishing attempts.

- Monitor Your Accounts: Regularly review your bank statements and transaction history for any unauthorized activity. Report suspicious transactions to your bank immediately.

- Use Secure Websites: When entering financial information online, ensure the website address begins with “https://” (indicating a secure connection) and look for a padlock icon in your browser’s address bar.

What to Do If Your Checkbook is Lost or Stolen

Losing your checkbook or having it stolen can be a distressing experience, as it directly exposes your routing and account numbers. If this happens:

- Contact Your Bank Immediately: Report the loss or theft to your bank as soon as possible. They can advise you on the necessary steps, which may include placing a stop payment on any outstanding checks, closing the compromised account, or changing your account number.

- Monitor Your Account: Keep a close watch on all your transactions for any signs of fraudulent activity.

- Notify Law Enforcement: Depending on the circumstances, filing a police report might be advisable, especially if you suspect foul play or identity theft.

Conclusion

The routing number and account number are the bedrock of modern banking and personal finance management. While the humble physical check might seem like an antiquated tool, it remains the definitive visual guide to these crucial identifiers. From enabling seamless direct deposits and online bill payments to facilitating secure wire transfers, these numerical codes are indispensable for navigating your financial life.

However, simply knowing where to find them is only half the equation. A truly financially savvy individual understands the profound importance of these numbers and prioritizes their protection. By adopting best practices for security, diligently monitoring your accounts, and being aware of the risks, you can ensure that your financial information remains safe and your money management continues to be efficient and secure. Embrace this knowledge, and you’ll be well-equipped to manage your finances with confidence and peace of mind in any scenario.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.