It’s a common question, one that arises from the practical necessity of managing personal finances in an increasingly digital world. Many people, when asked to provide their bank’s routing number, instinctively reach for their debit card, assuming that this crucial piece of information, like their account number, might be printed there. However, the short answer is that you will not find your routing number on your debit card. This seemingly simple fact often leads to confusion, especially for those new to managing their own bank accounts or navigating specific financial transactions. Understanding why it’s not on the card, where to actually find it, and its fundamental role in various financial operations is essential for anyone looking to handle their money efficiently and securely.

This article delves into the purpose of a routing number, clarifies why debit cards aren’t the place to look for it, guides you to its correct locations, and emphasizes its importance in everyday financial tasks, all within the overarching context of prudent personal finance management. By demystifying this common query, we aim to equip you with the knowledge needed to confidently manage your banking needs, from setting up direct deposits to understanding the mechanics behind secure money transfers.

Understanding the Essence of a Routing Number

To fully grasp why a routing number isn’t printed on a debit card, we first need to understand what a routing number is, its purpose, and how it differs from other financial identifiers you might encounter. This foundational knowledge is critical for navigating the complexities of modern banking.

What Exactly Is a Routing Number?

A routing number, officially known as an ABA (American Bankers Association) Routing Transit Number (RTN), is a nine-digit code that identifies the financial institution involved in a transaction. It acts like a postal code for banks, ensuring that funds are directed to the correct bank when sent electronically. These numbers are primarily used for processing checks, facilitating electronic funds transfers (EFTs), such as direct deposits, wire transfers, and automated clearing house (ACH) payments. Each bank, and sometimes different branches or types of accounts within a single bank, will have its unique routing number. This system is crucial for the seamless and accurate movement of money across the vast network of financial institutions in the United States. Without it, the vast volume of daily transactions would be impossible to manage with precision.

The Role of Routing Numbers in Modern Finance

The utility of a routing number extends across a wide spectrum of financial activities. When your employer sets up direct deposit for your paycheck, they’ll ask for your routing number and account number. Similarly, if you’re paying a utility bill online directly from your bank account, setting up automatic loan payments, or sending money to a friend through an electronic transfer service, a routing number is almost always required. It serves as the initial identifier, directing the funds to the correct bank before the account number then pinpoints the specific individual account within that bank. This two-tiered identification system is a cornerstone of the financial infrastructure, enabling rapid and reliable money transfers that are integral to both personal and business finance.

Routing Numbers vs. Account Numbers vs. Debit Card Numbers

It’s crucial to distinguish between these three distinct identifiers, as they serve different purposes and carry varying levels of risk if compromised.

- Routing Number: As established, this identifies your bank (or specific branch/account type). It’s publicly available information for your bank and, while sensitive, doesn’t directly give access to your account on its own.

- Account Number: This unique number identifies your specific account within your bank. When combined with a routing number, it allows for deposits and withdrawals. This is highly sensitive information, as it directly links to your funds.

- Debit Card Number: This 16-digit (or sometimes 15-digit) number, along with the expiration date and CVV (Card Verification Value), identifies your debit card itself. It’s used for point-of-sale transactions, online purchases, and ATM withdrawals. While linked to your bank account, it’s a separate identifier used for card-based transactions, not direct bank-to-bank transfers. Compromising your debit card number can lead to unauthorized purchases, but it doesn’t necessarily give someone direct access to initiate bank transfers from your account, unlike a compromised account number combined with a routing number. The distinction between these numbers is fundamental to understanding financial security and the appropriate use of each identifier.

The Common Misconception: Why It’s Not On Your Debit Card

The instinct to look for a routing number on a debit card stems from a logical but ultimately incorrect assumption: that if a card represents your bank account, all associated information must be on it. However, the design and security protocols surrounding debit cards are intentionally structured to prevent this.

The Security Rationale Behind Card Design

The primary reason routing numbers are not printed on debit cards is security. Debit cards are routinely exposed to various points of contact—POS terminals, ATMs, online payment portals, and even physical handling. Printing a routing number, along with your account number (which is also not on the card, typically), would consolidate too much sensitive banking information in one easily accessible place. If your card were lost or stolen, or if you were a victim of “skimming” (where card details are copied), a perpetrator would have all the necessary information to directly initiate unauthorized electronic transfers from your account. By separating these pieces of information, banks add an extra layer of protection, making it harder for criminals to gain comprehensive access to your funds. The debit card is designed for transactional convenience, not as a complete repository of your bank account details.

Distinguishing Between Card Information and Bank Account Information

It’s vital to differentiate between the information pertaining to your card and the information pertaining to your bank account. Your debit card number, expiration date, and CVV are specific to the card itself. They are credentials for using that card as a payment instrument. Your bank account number and routing number, on the other hand, are credentials for accessing and moving funds directly to or from your bank account. While your debit card draws funds from your bank account, the card itself is an interface, not the account’s complete identity. Banks intentionally keep these two sets of identifiers separate to minimize the risk associated with card theft or compromise. This separation is a deliberate security measure aimed at protecting your financial assets.

The Primary Function of a Debit Card (and its limitations)

A debit card’s main function is to provide convenient, immediate access to the funds in your checking account for purchases and cash withdrawals. It acts as an electronic check, deducting money directly from your account. This convenience is paramount, allowing for quick transactions without the need for cash or checks. However, its limitations lie precisely in its specialization. It is not designed to be an information hub for your bank account’s entire identity. For transactions that require direct bank-to-bank communication, such as setting up payroll or initiating large transfers, the specific bank account details—routing number and account number—are required, and these are obtained through more secure channels than the physical card itself. Understanding this functional distinction helps clarify why you shouldn’t expect to find all your bank details on the plastic.

Unveiling the True Location: Where to Find Your Routing Number

Since your debit card is not the place to look, where should you go to find your routing number when you need it? Fortunately, financial institutions provide several reliable and secure methods for locating this crucial nine-digit code.

Your Bank’s Official Website or Mobile App

In today’s digital age, the most common and often quickest way to find your routing number is through your bank’s official website or mobile application. After logging into your online banking portal, you typically navigate to a section related to “Account Details,” “My Accounts,” or “Direct Deposit Information.” Your checking account details, including the routing number specific to your account, will usually be displayed prominently there. Many banks even provide an easily printable or copyable version for convenience. This method is not only fast but also highly secure, as you are accessing the information directly from your bank’s verified platforms. Most banks understand the frequent need for this information and make it readily accessible within their digital offerings.

Examining Your Checkbook

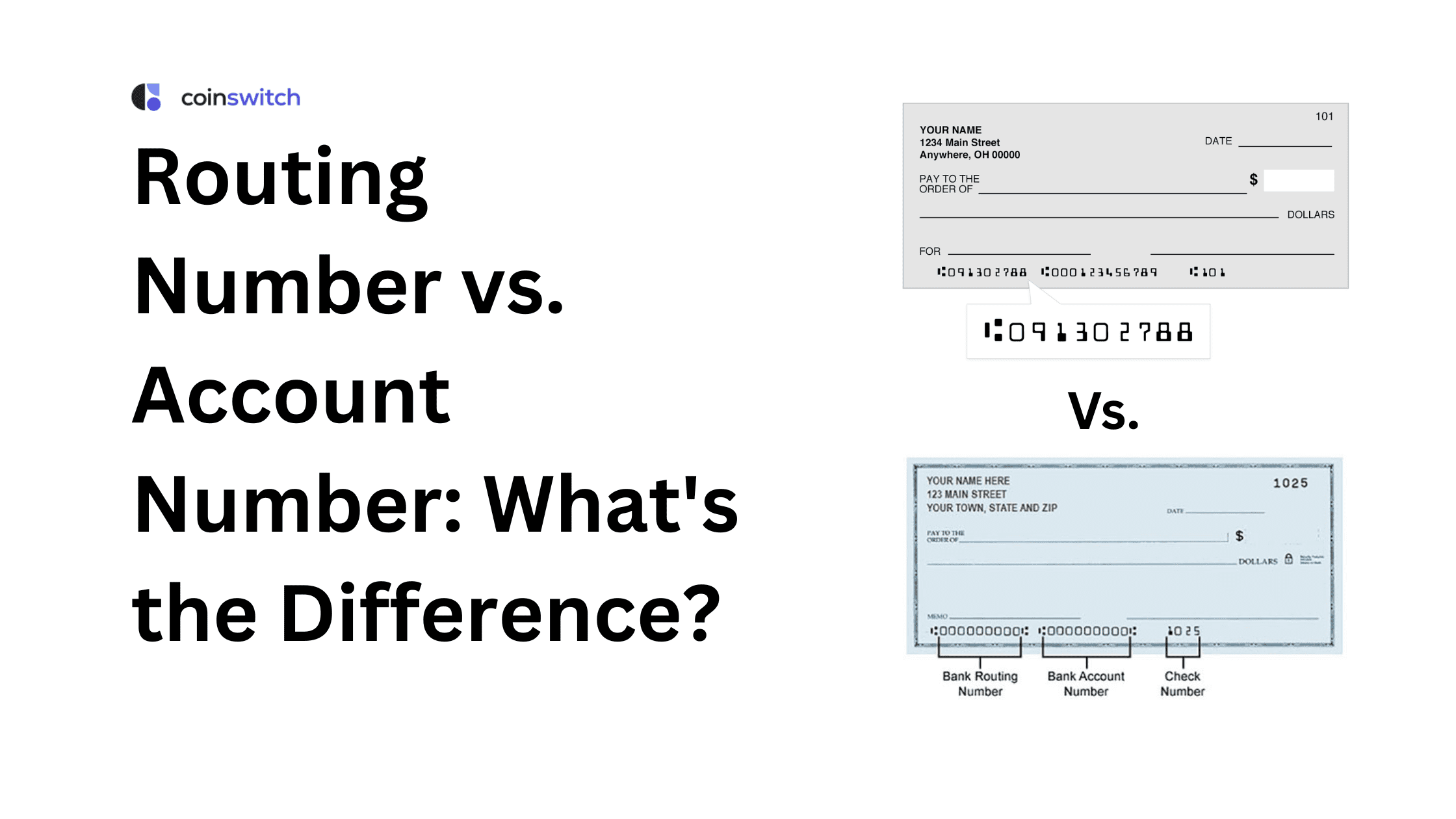

For those who still use paper checks, your checkbook is arguably the most traditional and reliable place to find your routing number. Look at the bottom left-hand corner of any check. You will see a series of numbers printed in magnetic ink (MICR line). The first set of nine digits on the left is your routing number. The second set of numbers, usually in the middle, is your account number. The final set is the check number. This method is particularly useful because it provides a tangible, physical record of the number, ensuring accuracy for transactions that require manual entry or verification. If you have a checkbook for the account in question, this is an excellent, time-tested way to confirm your routing number.

Contacting Your Bank Directly

If you don’t have access to online banking or a checkbook, or if you simply prefer direct communication, contacting your bank is always an option. You can call your bank’s customer service line (the number is usually on the back of your debit card or on their official website) or visit a local branch in person. When you call, be prepared to verify your identity through security questions, as banks are required to protect your personal information. A bank representative will then be able to provide you with the correct routing number for your specific account. Visiting a branch offers the added benefit of speaking with a teller who can directly confirm the information and potentially print it out for you.

Bank Statements and Official Documents

Your monthly bank statements, whether paper or electronic, are another reliable source of your routing number. Typically, the routing number is printed near the top of the statement, along with your account number and other bank details. Any official document issued by your bank at the time of account opening, such as a welcome packet or account agreement, will also contain this information. These documents are designed to provide a comprehensive overview of your account and are generally kept for reference, making them a safe fallback if other methods are unavailable. Regularly reviewing your bank statements is a good financial habit anyway, and now you know it serves an additional purpose!

Practical Applications and Importance in Personal Finance

Understanding where to find your routing number is not just about curiosity; it’s a fundamental aspect of managing various crucial financial transactions. Its correct usage ensures your money goes where it’s intended, playing a pivotal role in maintaining financial health.

Setting Up Direct Deposits

One of the most common applications for a routing number is setting up direct deposit for your paycheck, government benefits, or tax refunds. Employers and government agencies require both your routing number and your account number to ensure your funds are deposited directly into your chosen bank account. This eliminates the need for paper checks, speeds up access to your funds, and enhances security by reducing the risk of lost or stolen checks. Getting this information right is crucial; an incorrect routing number could delay your payment or, in rare cases, send it to the wrong institution, leading to significant inconvenience and potential complications.

Facilitating Online Bill Payments

Many individuals opt to pay recurring bills directly from their bank accounts rather than using a debit card. This often involves providing the biller with your bank’s routing number and your account number. This method is particularly popular for larger bills like mortgages, car payments, or utilities, offering a secure and convenient way to ensure payments are made on time without relying on physical checks or credit card transaction fees. Automated online bill payments, powered by routing numbers, contribute significantly to financial organization and help avoid late fees, making them an indispensable tool in personal finance management.

Initiating Wire Transfers and ACH Transactions

Routing numbers are indispensable for initiating both wire transfers and Automated Clearing House (ACH) transactions. Wire transfers are typically used for large, time-sensitive, or international money movements and require the sending and receiving banks’ routing numbers (or SWIFT/IBAN for international wires) to ensure funds reach their destination quickly and securely. ACH transactions, on the other hand, are electronic payments or debits processed through the ACH network, including direct deposits, direct debits (like recurring loan payments), and person-to-person payments. Both types of transfers rely heavily on accurate routing numbers to ensure the correct financial institutions are engaged in the transaction, highlighting their critical role in the underlying infrastructure of financial transactions.

Understanding International Transactions (SWIFT/IBAN vs. Routing)

While routing numbers are vital for domestic transactions within the United States, it’s important to note their limitations in international contexts. For international wire transfers, you’ll typically need a SWIFT (Society for Worldwide Interbank Financial Telecommunication) code or BIC (Bank Identifier Code) for most countries, or an IBAN (International Bank Account Number) for European countries and some others. These international codes serve a similar purpose to routing numbers, identifying the specific bank and sometimes even the branch globally. Understanding this distinction is crucial for anyone engaging in international money transfers, as providing a U.S. routing number for an overseas transaction will likely lead to delays or rejection. This knowledge empowers you to confidently manage both domestic and global financial interactions.

Safeguarding Your Financial Information

Given the critical role of routing and account numbers, protecting this information is paramount. While routing numbers are less sensitive than account numbers, their combination can enable unauthorized transactions. Prudent financial habits dictate a careful approach to sharing and storing these details.

When and How to Share Your Routing Number

You will need to share your routing number (usually with your account number) when setting up direct deposit with an employer, establishing automatic bill payments with service providers, or initiating transfers to or from your account with trusted financial institutions or individuals. Always ensure you are sharing this information through secure channels. For online forms, verify that the website is legitimate and uses HTTPS encryption (look for the padlock icon in your browser). When providing it over the phone, confirm you are speaking with a representative from a trusted institution and avoid sharing it in unsecured emails or public messages. Remember, only share it with entities you trust and for legitimate financial purposes.

Recognizing Potential Scams

Scammers frequently attempt to trick individuals into divulging their banking information. Be wary of unsolicited emails, phone calls, or text messages asking for your routing and account numbers, even if they appear to be from your bank or a government agency. Banks will rarely ask for this information via unsecure channels. Phishing attempts often mimic legitimate communications to steal your data. Always independently verify the request by contacting the institution directly using a known, official phone number or website, rather than responding to the message you received. Legitimate requests for this information will typically come from entities with whom you have an established financial relationship or are actively trying to set one up.

Best Practices for Financial Security

Beyond careful sharing, adopt broader financial security practices. Regularly monitor your bank statements for any unauthorized transactions. Use strong, unique passwords for your online banking accounts and enable multi-factor authentication whenever possible. Be cautious about public Wi-Fi networks when accessing sensitive financial information. Shred old bank statements or documents containing your routing and account numbers before discarding them. By staying vigilant and adopting these best practices, you can significantly reduce the risk of fraud and protect your financial assets from unauthorized access. Your financial security is a continuous effort, and being informed is your first line of defense.

In conclusion, while your debit card is an invaluable tool for daily spending, it is not the repository for all your banking information. The absence of a routing number on your card is a deliberate security measure, separating card-specific details from your core bank account identifiers. Understanding the distinction between these financial numbers and knowing the secure, reliable places to find your routing number—your bank’s website, checkbook, statements, or by contacting them directly—empowers you to confidently manage your money. By applying this knowledge and adhering to best practices for financial security, you can ensure your transactions are smooth, secure, and contribute to your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.