Navigating the complexities of federal taxation is a fundamental aspect of personal and business finance management. For many taxpayers, the most stressful part of the fiscal year is not just calculating what is owed, but ensuring that the funds reach the Internal Revenue Service (IRS) accurately and on time. Misrouting a payment can lead to administrative headaches, unnecessary penalties, and accrual of interest that can erode your financial health.

In an increasingly digital financial landscape, the IRS has expanded its repertoire of payment channels. Whether you are a high-net-worth investor, a small business owner, or a salaried employee with additional income streams, understanding the “where” and “how” of tax remittance is vital for maintaining a clean audit trail and optimizing your cash flow. This guide explores the diverse avenues available for sending payments to the IRS, categorized by efficiency, security, and strategic financial planning.

Modern Payment Methods: Navigating IRS Digital Portals

The shift toward digital finance has revolutionized how taxpayers interact with the federal government. For most individuals and businesses, electronic payment methods are the preferred choice because they offer immediate confirmation and reduce the risk of documents getting lost in the mail. From a financial management perspective, digital payments allow for precise timing, ensuring that funds remain in your interest-bearing accounts until the moment they are due.

IRS Direct Pay for Individuals

For individual taxpayers filing Form 1040, IRS Direct Pay is often the most streamlined solution. This service allows you to pay directly from your checking or savings account without any processing fees. It is particularly useful for paying 1040-ES estimated taxes, which are a cornerstone of financial planning for freelancers and independent contractors. One of the primary benefits of Direct Pay is the “Look Up a Payment” feature, which provides an instant digital receipt—a critical component for your annual financial records.

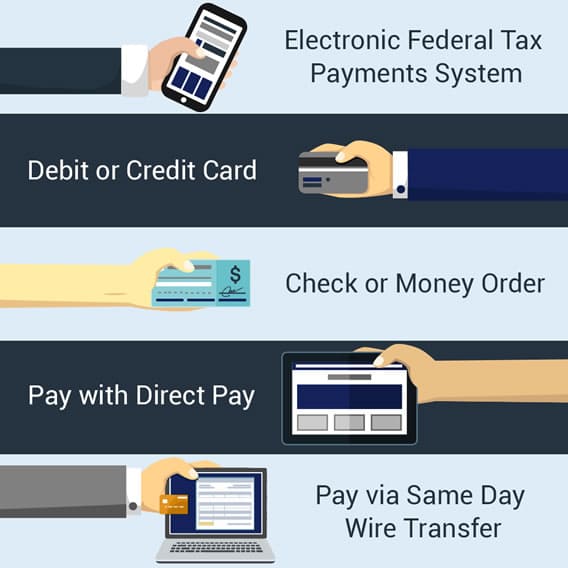

Electronic Federal Tax Payment System (EFTPS) for Businesses

While Direct Pay serves individuals, the Electronic Federal Tax Payment System (EFTPS) is the gold standard for business entities and large-scale investors. EFTPS is a free service provided by the U.S. Department of the Treasury that allows for the scheduling of payments up to 365 days in advance. From a business finance standpoint, this is an invaluable tool for managing liquidity. By scheduling quarterly corporate taxes or payroll tax deposits ahead of time, financial officers can ensure compliance without manual intervention on the actual due date.

Digital Wallets and Credit Card Options

In recent years, the IRS has integrated with third-party processors to accept payments via credit cards, debit cards, and digital wallets like PayPal or Click to Pay. While this offers convenience and the potential to earn “cash back” or travel rewards, it comes with a financial trade-off. Third-party processors charge a percentage-based fee. For a substantial tax bill, these fees can outweigh the value of any credit card points earned. A savvy financial strategy involves calculating the “net cost” of using a credit card to ensure the convenience doesn’t negatively impact your bottom line.

The Traditional Route: Mailing Your Payment to the IRS

Despite the digital revolution, a significant portion of the population still prefers or requires the use of paper checks or money orders. Mailing a payment is a viable option, but it requires meticulous attention to detail regarding geographic jurisdictions and documentation. The IRS utilizes several different processing centers, often referred to as “lockboxes,” and sending your payment to the wrong location can delay processing for weeks.

Determining the Correct Mailing Address by State

The IRS divides the United States into several regions, each assigned to a specific processing center in cities such as Charlotte, Louisville, or Cincinnati. The “where” depends entirely on your state of residence and whether you are enclosing a tax return with your payment. For instance, a resident of California might send their payment to a different address than a resident of New York. It is imperative to check the official IRS instructions for Form 1040 or Form 1040-V annually, as these addresses can change based on internal IRS restructuring.

Form 1040-V: The Payment Voucher Essential

If you choose to mail a check, you should never simply drop it in an envelope. The IRS requires Form 1040-V, the Payment Voucher. This small but mighty document contains a scannable code that links your payment directly to your Social Security Number (SSN) or Employer Identification Number (EIN). Without this voucher, there is a risk that your payment could be misapplied to the wrong tax year or account, leading to “failure to pay” notices even if the check was cashed.

Proof of Mailing and Certified Mail Protocols

From a risk management perspective, mailing a check to the IRS should always involve a paper trail. Financial advisors recommend using USPS Certified Mail with a Return Receipt Requested. This provides legal proof of the date of mailing, which the IRS recognizes as the “date paid” under the “timely mailed, timely paid” rule. In the event of a dispute or a lost envelope, this $4 to $8 investment protects you from hundreds of dollars in late-payment penalties.

Strategic Financial Management: Timing and Tax Planning

Knowing where to send your payments is only half the battle; knowing when and how much to send is what separates basic compliance from expert financial management. Effective tax remittance is an integral part of a broader wealth-building strategy, as it prevents the government from holding your money interest-free while also protecting you from the high costs of IRS interest rates.

Understanding Quarterly Estimated Tax Payments

For those with income not subject to withholding—such as investment dividends, capital gains, or self-employment income—the IRS requires quarterly estimated tax payments. These are typically due on April 15, June 15, September 15, and January 15. Failing to send these payments to the correct “lockbox” or digital portal on time can result in an underpayment penalty. Strategically, many taxpayers use these dates to re-evaluate their annual profit-and-loss statements, adjusting their payments to mirror their actual income and maintain optimal liquidity.

Avoiding Late Payment Penalties and Interest

The IRS interest rate for underpayments is adjusted quarterly and can be significantly higher than what you might earn in a high-yield savings account. Therefore, identifying the most efficient payment channel is a defensive financial move. If you find yourself unable to pay the full amount, the IRS provides “Offer in Compromise” or “Installment Agreements.” These are managed through specific departments within the IRS, and payments for these agreements are often sent to different addresses than standard tax returns.

Leveraging Tax Software for Automatic Scheduling

Modern financial tools and tax software (such as TurboTax, H&R Block, or professional CPA portals) often have built-in features that handle the “where” for you. By linking your bank account to the software, you can authorize an Electronic Funds Withdrawal (EFW). This method is highly efficient as it submits the payment along with the electronic return, ensuring that the data and the dollars arrive at the IRS simultaneously, minimizing the chance of accounting discrepancies.

Security and Verification: Protecting Your Financial Information

Whenever money is being moved, security is paramount. Tax-related identity theft and phishing scams cost taxpayers billions of dollars annually. Ensuring that you are sending your money to the actual IRS and not a fraudulent entity is a critical step in digital security and personal finance protection.

Identifying IRS Official Sites vs. Phishing Scams

The IRS will never initiate contact with taxpayers via email, text message, or social media to request personal or financial information. When sending payments online, always ensure the URL ends in .gov. Many fraudulent websites mimic the look of the IRS but use .org or .net suffixes. Using the official IRS.gov/payments gateway is the only way to guarantee your financial data is encrypted and handled by the Treasury Department.

Tracking Your Payment Status Through “View Your Account”

A key feature of modern financial management is the “IRS Online Account” tool. Once you have sent a payment—whether by mail or electronically—you can log in to your secure account to verify that the payment has been applied to your balance. This provides peace of mind and allows you to catch errors early. If a payment does not show up within 2–3 weeks of mailing, it serves as an early warning system to initiate a trace or stop-payment on a check.

Record Keeping for Audits and Future Planning

Finally, the “where” of your payment should always be documented in your personal financial archives. Keep copies of your 1040-V vouchers, electronic confirmation numbers, and cancelled checks for at least seven years. These documents are the ultimate defense in an audit. Furthermore, reviewing these records at the end of the year helps you and your financial advisor accurately calculate your tax liability for the following year, ensuring that your wealth management strategy remains proactive rather than reactive.

In conclusion, sending a payment to the IRS is more than a chore; it is a precise financial transaction that requires a choice between digital speed and traditional paper trails. By utilizing tools like IRS Direct Pay, understanding the geographic requirements of mailing, and maintaining strict security protocols, you can ensure that your obligations are met with professional efficiency, leaving you free to focus on growing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.