In an increasingly digital and financially savvy world, payment solutions have evolved far beyond traditional cash and credit cards. Among the innovators leading this transformation is Klarna, a Swedish fintech company that has become synonymous with “Buy Now, Pay Later” (BNPL) services. Far from being a niche offering, Klarna has woven itself into the fabric of modern commerce, providing consumers with unprecedented flexibility in how they manage their money and make purchases. The question “where can you use Klarna?” therefore extends beyond a simple list of retailers; it delves into the broader financial ecosystem, exploring how this tool empowers individuals to budget, save, and access goods and services that might otherwise be out of immediate reach.

This article, firmly rooted in the Money category, will explore the extensive reach of Klarna, detailing its applications across various spending environments and dissecting the financial implications for consumers. We will examine how Klarna serves as a versatile financial tool, from everyday shopping to significant investments, while also providing critical insights into its responsible and strategic use to optimize personal financial health.

The Evolving Retail Landscape: Online and In-Store Shopping

At its core, Klarna’s primary utility lies in facilitating consumer purchases, making it a powerful financial instrument in both digital and physical retail spaces. Its integration across diverse merchant platforms underscores its role in shaping contemporary spending habits and cash flow management.

E-commerce Dominance: Seamless Online Transactions

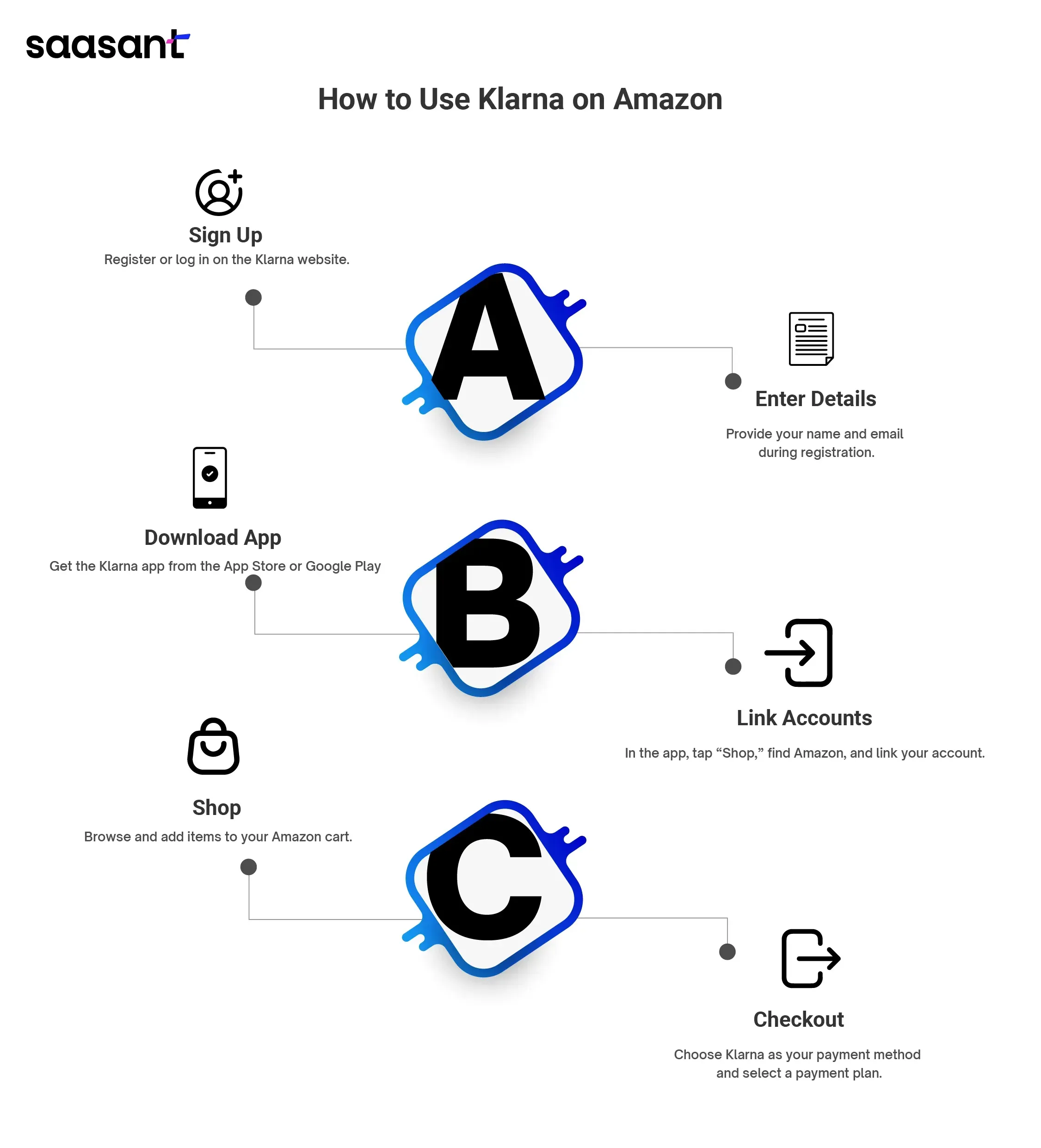

Klarna first gained widespread traction by revolutionizing the online checkout experience. For many e-commerce platforms, Klarna is offered directly as a payment option, appearing alongside credit card fields and other digital wallets. This direct integration streamlines the purchasing process, allowing customers to select their preferred Klarna payment plan – often “Pay in 4” (four interest-free installments) or “Pay in 30” (pay the full amount in 30 days) – with just a few clicks. This immediate access to installment plans turns a lump sum into manageable segments, significantly aiding in personal budgeting for online shoppers.

Beyond direct merchant partnerships, Klarna extends its reach through its dedicated app and browser extensions. The Klarna app functions as a sophisticated shopping portal, allowing users to browse products from thousands of retailers. Crucially, even if a merchant doesn’t directly integrate Klarna at checkout, the app facilitates purchases through the generation of a one-time virtual card. This virtual card acts like a prepaid debit card, funded by Klarna, which can then be used at virtually any online store that accepts major card payments. This mechanism ensures that the flexibility of BNPL is not restricted to a select group of partners but is broadly accessible, turning almost any online purchase into a potential Klarna transaction.

The sectors where Klarna sees significant online usage are diverse. Fashion retailers, electronics stores, home goods providers, beauty brands, and even niche markets have embraced Klarna. For consumers, this translates to the ability to acquire desired items without immediate financial strain, spread the cost of larger purchases like a new laptop or furniture, or even “try before you buy” with the Pay in 30 option, offering a grace period to assess products before committing financially. This directly impacts personal cash flow, allowing consumers to retain liquidity for other expenses or emergencies.

Bridging the Digital-Physical Divide: In-Store Shopping

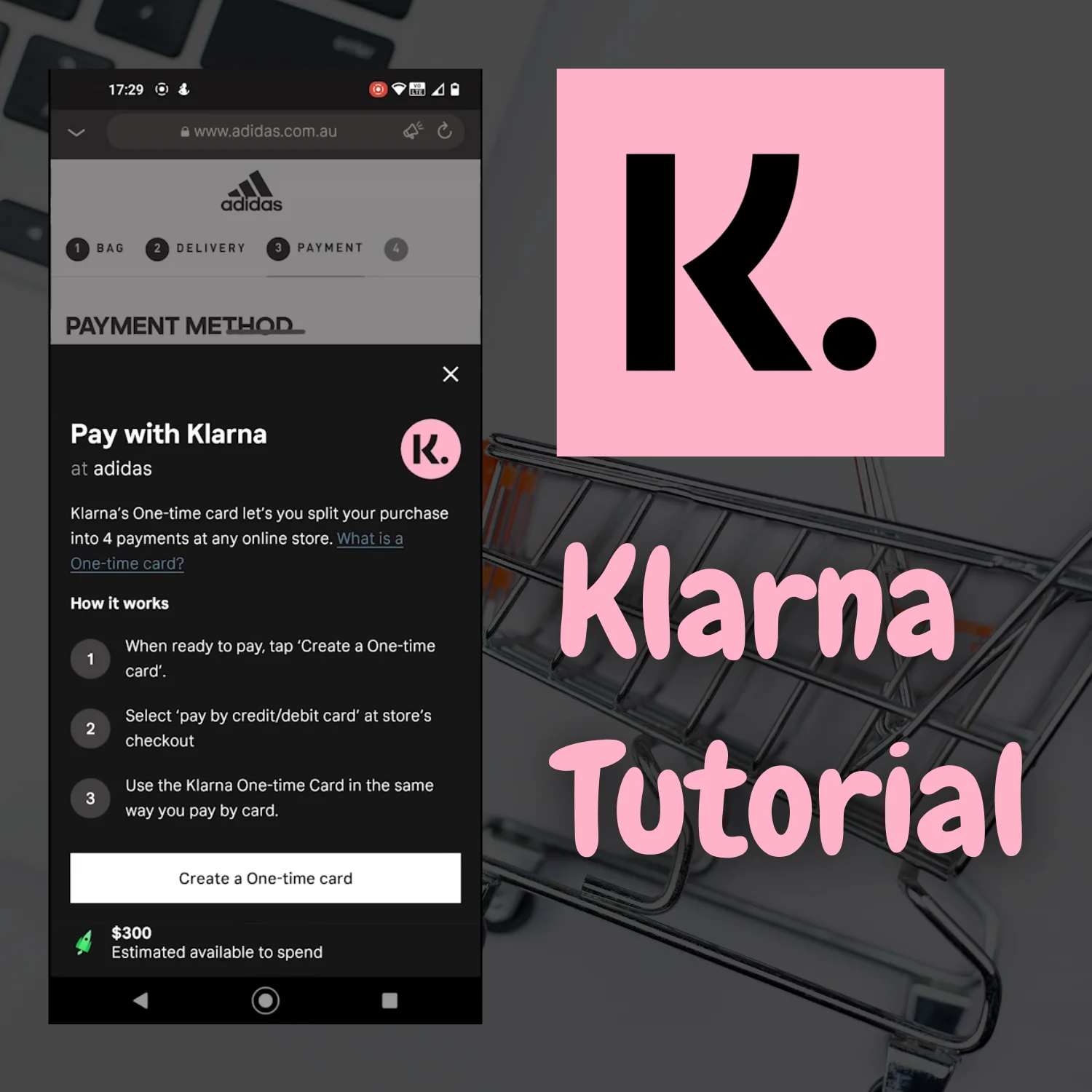

While its roots are digital, Klarna has successfully expanded its financial utility to brick-and-mortar stores, ensuring that the benefits of flexible payments are available regardless of the shopping environment. The physical Klarna Card, for instance, functions like a traditional debit or credit card, allowing users to make purchases at any store that accepts Visa. When a transaction is made with the Klarna Card, the user can then choose from their available Klarna payment options within the app, effectively transforming a standard card swipe into an installment plan. This provides an elegant solution for managing larger in-store expenses, from appliance purchases to clothing hauls, by allowing consumers to budget for them over time.

For those without a physical card, the Klarna app still facilitates in-store BNPL. Through mobile wallets like Apple Pay or Google Pay, users can generate a one-time card within the Klarna app and use their phone to pay at compatible terminals. Some retailers also offer Klarna payments via QR codes at the point of sale, allowing customers to scan and complete their transaction through the app.

This extension to physical retail has profound implications for personal finance. It democratizes access to immediate gratification while simultaneously promoting responsible spending through structured payment plans. Consumers can confidently make significant in-store purchases, knowing they have a clear payment schedule, helping to avoid the sudden depletion of savings or reliance on high-interest credit card debt. This seamless integration ensures that whether shopping online or walking into a physical store, the financial flexibility offered by Klarna remains consistently accessible, enhancing overall financial control.

Beyond Retail: Expanding Financial Applications

While retail forms the cornerstone of Klarna’s utility, its applications extend far beyond buying clothes or gadgets. As a versatile financial tool, Klarna is increasingly being utilized for a broader range of services and experiences, helping individuals manage diverse expenditures that fall outside traditional product purchases.

Travel and Experiences: Budgeting for Adventures

One significant area where Klarna is gaining traction is in the travel and leisure industry. Airlines, hotel chains, vacation rental platforms, and tour operators are increasingly partnering with Klarna to offer flexible payment options. This allows consumers to spread the cost of larger travel expenses – such as flights, accommodation, or an entire vacation package – over several months or interest-free installments.

From a personal finance perspective, this is a game-changer. Travel, while often desired, can represent a substantial one-time outlay, sometimes delaying or preventing experiences. By using Klarna, individuals can book their trips earlier, take advantage of better deals, and manage the financial burden over time without having to deplete their savings immediately or incur high credit card interest. It transforms aspirational travel into an achievable financial goal, making leisure and cultural enrichment more accessible and budget-friendly. This impacts how individuals allocate discretionary income and plan for significant life experiences.

Everyday Services and Wellness: Investing in Well-being

Klarna’s utility also extends to various services that contribute to daily life and overall well-being. While it’s generally not used for recurring utility bills (like electricity or water), it can be employed for one-off or larger service-based payments that benefit from installment plans. Examples include automotive repair shops for significant vehicle maintenance, dental clinics for procedures not fully covered by insurance, and some specialized educational courses or certification programs.

Furthermore, the wellness sector has seen an uptake in Klarna usage. From high-end fitness equipment and annual gym memberships (when paid upfront) to aesthetic treatments and specialized health products, Klarna provides a means to invest in personal health without an immediate large financial commitment. For instance, an elective dental procedure or a new wellness device can be split into manageable payments, making essential or desired health investments more attainable and less financially disruptive. This enables individuals to prioritize their well-being by spreading the cost of services that enhance their quality of life.

Understanding Klarna’s Financial Models and Their Implications

To effectively use Klarna as a financial tool, it’s crucial to understand the distinct models it offers and their respective financial implications. Each option is designed to address different consumer needs and repayment capacities, directly influencing personal cash flow and debt management strategies.

“Pay in 4” and “Pay in 30”: Short-Term Budgeting Tools

The “Pay in 4” and “Pay in 30” options are Klarna’s most popular offerings and serve as excellent short-term budgeting tools. “Pay in 4” allows consumers to split the cost of a purchase into four equal, interest-free installments, typically paid every two weeks. “Pay in 30” grants customers 30 days to pay the full amount after an item ships, also interest-free.

These options are powerful for managing immediate cash flow. They enable individuals to make purchases without locking up their available funds for an extended period, allowing them to retain liquidity for other expenses or to keep an emergency fund intact. The interest-free nature means that, unlike credit cards, there’s no additional cost for the convenience, provided payments are made on time. This makes Klarna a financially astute choice for consumers who need a temporary bridge between their purchase and their next paycheck, or simply prefer to spread out expenses without incurring debt interest. However, responsible use is paramount; missing payments can lead to late fees, which negate the interest-free benefit and can impact financial health.

Financing Options: Longer-Term Installments for Larger Purchases

For more substantial purchases, Klarna also offers longer-term financing options, which typically extend beyond four installments and may involve interest. These plans are more akin to traditional personal loans or store credit cards, designed for items like large appliances, furniture, or expensive electronics. The interest rates, if applicable, are determined based on the user’s creditworthiness and the specific terms of the agreement.

When considering these financing options, it’s vital for consumers to assess them against alternatives such as personal loans from banks or credit card promotions. Klarna’s long-term financing can be a viable option, particularly if the interest rate is competitive or if the consumer wishes to consolidate their financing through a single platform. However, the decision should be made with a clear understanding of the total cost of borrowing, including interest and any potential fees. For responsible money management, users should evaluate whether the purchase is truly necessary and if the repayment schedule aligns with their budget, ensuring they don’t overextend their financial commitments.

The Klarna App: A Hub for Financial Management

The Klarna app is not just a payment gateway; it’s a comprehensive hub for financial management related to Klarna transactions. Within the app, users can view all their past and current orders, track payment schedules, receive timely reminders for upcoming installments, and manage their payment methods. This centralized control empowers users to stay on top of their financial obligations, reducing the risk of missed payments and associated fees.

Beyond basic transaction management, the app often provides spending insights, categorizing purchases and offering a snapshot of spending habits. This functionality aligns with personal finance best practices, allowing users to monitor where their money is going and make informed decisions about future spending. For many, the app serves as a crucial tool in maintaining financial discipline within the flexible payment landscape offered by Klarna.

Strategic Considerations for Using Klarna Responsibly

While Klarna offers unparalleled flexibility and convenience, its use, like any financial tool, requires strategic thought and responsible practices to ensure it contributes positively to personal financial health rather than leading to overspending or debt.

The Allure of Flexibility vs. The Peril of Overspending

The ease with which purchases can be split into smaller, interest-free installments can be a double-edged sword. While it aids budgeting, it can also create a psychological detachment from the full cost of an item, potentially leading to overspending. The cumulative effect of multiple “Pay in 4” plans can quickly add up, creating a significant monthly outflow that might exceed an individual’s financial capacity.

Responsible use dictates a strict adherence to a personal budget. Consumers should view Klarna as a cash flow management tool, not an extension of their income. Before initiating a Klarna purchase, it’s crucial to confirm that all installments can be comfortably met within existing financial obligations. Developing a disciplined approach to assess each purchase’s necessity and affordability within the context of one’s entire financial picture is paramount to harnessing Klarna’s benefits without falling into debt traps.

Impact on Credit Score: Nuances and Best Practices

The impact of Klarna on a user’s credit score is a nuanced but critical aspect for financial well-being. Klarna typically performs a “soft credit check” for its Pay in 4 and Pay in 30 options, which does not affect the credit score. However, for longer-term financing options, a “hard credit check” may be performed, which can temporarily lower a credit score.

Crucially, Klarna does report payment activity to credit bureaus in some markets, and this trend is growing. On-time payments can positively contribute to a credit history, demonstrating responsible financial behavior. Conversely, missed or late payments can negatively impact a credit score, making it harder to secure loans or credit in the future. Therefore, treating Klarna payments with the same seriousness as any other loan or credit card payment is essential for maintaining a healthy credit profile. Responsible use involves ensuring funds are always available for automatic payments and actively monitoring payment schedules to avoid any defaults.

Consumer Protections and Returns Policies

Understanding Klarna’s consumer protections and how it interacts with merchant return policies is another vital financial consideration. Klarna often acts as an intermediary, which can offer an added layer of security for disputes. If an item is faulty, damaged, or not as described, Klarna’s resolution process can provide a structured way to address issues with merchants. Payments can often be paused during a dispute, protecting the consumer from having to pay for an unsatisfactory product.

Regarding returns, if an item purchased with Klarna is returned according to the merchant’s policy, Klarna will adjust the payment plan accordingly, canceling future payments and refunding any already made. This seamless integration with merchant operations ensures that consumers are not financially penalized for returns, reinforcing trust and providing peace of mind. Familiarity with both Klarna’s and the merchant’s specific return and dispute resolution policies is a key aspect of informed financial engagement.

In conclusion, Klarna has firmly established itself as a ubiquitous financial tool across a vast array of spending categories, from the immediate gratification of online retail to the strategic budgeting of travel and essential services. Its diversified payment models offer consumers unprecedented flexibility in managing their finances, transforming large expenses into manageable installments and aiding in cash flow optimization. However, like any powerful financial instrument, its benefits are maximized through thoughtful, disciplined, and informed use. By understanding its applications, its financial models, and the crucial strategic considerations for responsible engagement, individuals can harness Klarna’s potential to empower their personal financial journey, making smarter purchasing decisions and achieving greater economic freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.