In the modern financial landscape, the ability to move money seamlessly is the backbone of personal and business commerce. Whether you are setting up a direct deposit for a new job, paying your monthly rent via an online portal, or sending a wire transfer to a family member, you will inevitably be asked for two critical pieces of information: your account number and your routing number.

While most people are familiar with their account number—the unique identifier for their specific funds—the routing number often remains a bit of a mystery. Understanding what this nine-digit code represents and knowing exactly where to find it is a fundamental skill in personal finance. This guide provides an in-depth look at the routing number, its various locations, and its vital role in the global movement of capital.

1. Understanding the Fundamentals of the Routing Number

Before searching for the number, it is helpful to understand what it actually is. In the United States, a routing number (often referred to as an ABA routing transit number or RTN) is a nine-digit code used to identify a specific financial institution during a transaction.

The History and Purpose of the ABA Number

The system was developed by the American Bankers Association (ABA) in 1910. Its primary purpose was to simplify the sorting, bundling, and shipment of paper checks. By assigning a unique code to every bank, the Federal Reserve and other clearinghouses could ensure that a check written in California and deposited in New York would find its way back to the correct “drawer” bank for settlement. Today, while paper checks are less common, the routing number remains the standard for electronic transfers, including ACH (Automated Clearing House) transactions and domestic wire transfers.

The Anatomy of the Nine-Digit Code

A routing number isn’t just a random sequence of integers; it follows a specific format that conveys information to financial processing systems.

- The first four digits: These identify the Federal Reserve symbol, representing the physical location of the bank or the processing center.

- The middle four digits: These represent the specific financial institution’s unique identifier.

- The ninth digit: This is a “check digit.” It is calculated using a complex mathematical formula based on the previous eight digits. If the result doesn’t match the check digit, the banking system immediately flags the number as invalid, preventing processing errors.

2. Practical Methods to Locate Your Routing Number

In the digital age, there are several ways to retrieve your routing number. Depending on whether you have physical documents or just a smartphone, you can find this information in seconds.

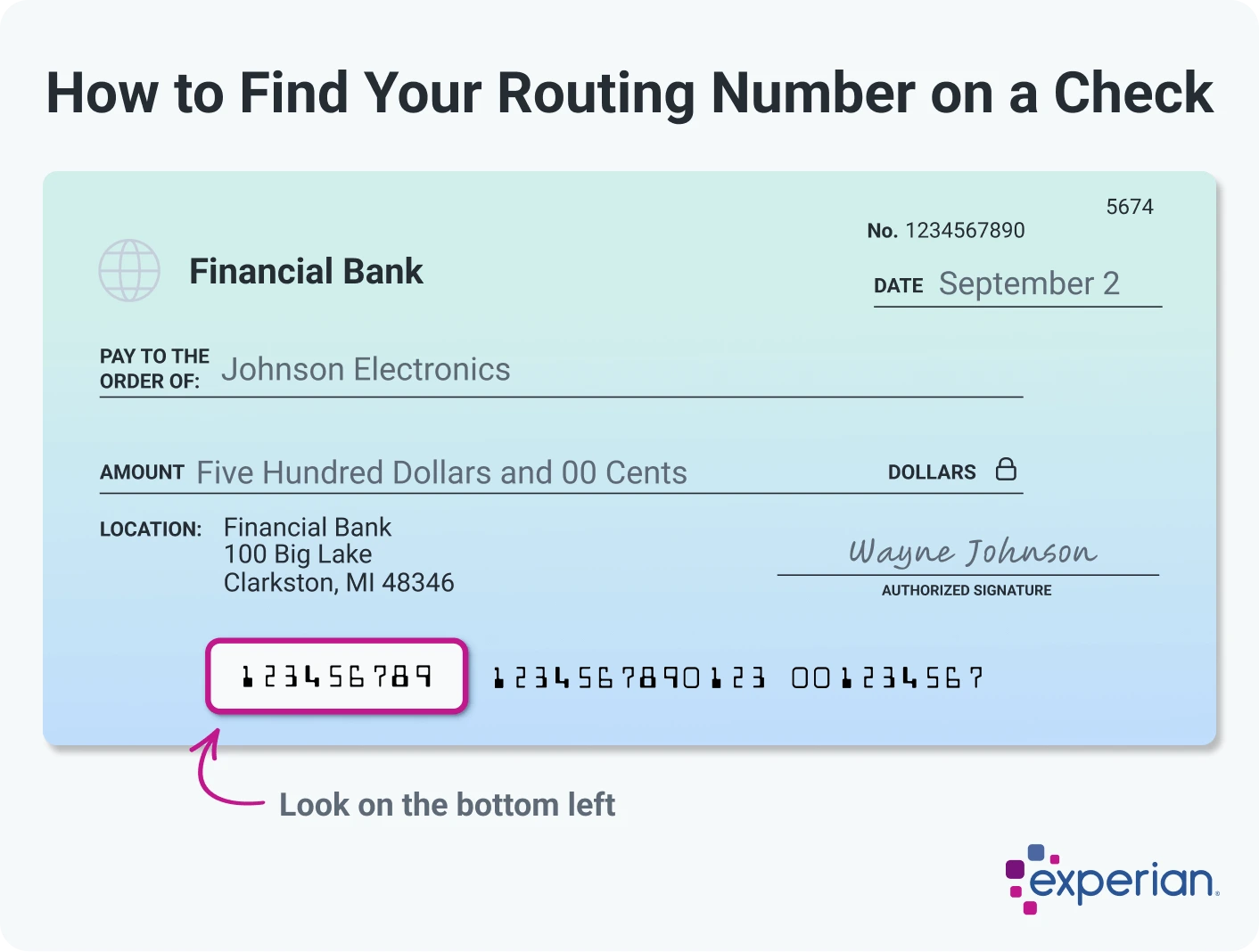

Locating the Number on a Personal Check

The most traditional and reliable way to find your routing number is to look at a physical check associated with your account. At the bottom of every check, there is a string of numbers printed in a special font known as MICR (Magnetic Ink Character Recognition).

- The Bottom Left: On a standard check, the routing number is the first set of nine digits located in the bottom left-hand corner. It is typically bracketed by a specific symbol that looks like a colon and a dash.

- The Middle Set: The sequence following the routing number is usually your account number.

- The Final Set: The last group of numbers is the specific check number.

Utilizing Online Banking and Mobile Apps

As society moves toward a paperless economy, many consumers no longer carry checkbooks. If this is the case, your bank’s digital platform is your best resource.

- Account Details Page: Once you log into your mobile banking app or online portal, navigate to the specific checking or savings account you wish to use. Look for a link labeled “Account Details,” “Account Info,” or “Direct Deposit Information.”

- Search Function: Many modern banking apps include a search bar. Typing “routing number” will often trigger a pop-up window or a direct link to the necessary digits.

- Digital Statements: If the app interface is confusing, you can download a PDF of your most recent monthly statement. Most banks print the routing number near the top of the statement or in the “Account Summary” section.

Contacting the Bank or Checking Their Public Website

Because routing numbers identify the institution rather than the individual, they are not considered private information in the same way an account number is. You can often find a bank’s routing number by simply visiting their official website and looking at the “Contact Us” or “FAQs” section. However, be cautious: some large national banks have different routing numbers for different states or for different types of transactions (e.g., one for ACH and another for Wires). If you are unsure, calling the bank’s customer service line is a foolproof way to verify the correct number for your specific region.

3. Routing Numbers vs. Account Numbers: Key Differences

One of the most common mistakes in personal finance is confusing the routing number with the account number. Understanding the distinction is vital for ensuring your money reaches the right destination without delays or fees.

Identifying the Distinct Roles of Each

The easiest way to visualize the difference is to think of a routing number as a zip code and an account number as your specific street address.

- Routing Number (The “Where”): This tells the financial system which bank “building” the money needs to go to. Multiple people—potentially millions in the case of a bank like JPMorgan Chase—share the same routing number.

- Account Number (The “Who”): This tells the bank which specific “office” or “mailbox” within that building the money belongs to. This number is unique to you.

Why You Shouldn’t Confuse Them

If you accidentally swap these numbers during an electronic transfer, the transaction will fail. In some cases, if the numbers happen to correspond to another valid account, the money could be deposited into the wrong person’s hands. While banks have recovery processes, it can take weeks to reverse such an error. Furthermore, many businesses charge “returned item fees” if a payment fails due to incorrect banking info, making it an expensive mistake to make.

4. When and Why You Need Your Routing Number

In your daily financial life, you won’t need your routing number for every transaction (you don’t need it for debit card purchases or ATM withdrawals, for example). However, it is essential for specific high-value or automated movements of money.

Setting Up Direct Deposit and Automatic Payments

The most common use for a routing number is the “Electronic Funds Transfer” (EFT). When you start a new job, you fill out a direct deposit form. By providing your routing number, you are telling your employer’s payroll software exactly which bank to send your wages to every payday. Similarly, when you set up “Auto-Pay” for your mortgage, car loan, or utility bills, the billing company uses your routing number to request funds from your specific bank.

Wire Transfers and International Transactions

While ACH transfers (like direct deposits) are the standard for domestic payments, “Wire Transfers” are used for immediate, high-priority, or international transactions.

- Domestic Wires: Some banks use a specific routing number for incoming domestic wires that is different from their standard ACH routing number. It is critical to confirm this with your bank before initiating a wire, as using the ACH number might cause the wire to be rejected.

- International Transactions: If you are receiving money from abroad, a standard nine-digit ABA routing number may not be enough. You will likely need a SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or a BIC (Bank Identifier Code). These serve a similar purpose to the routing number but on a global scale.

5. Security and Fraud Prevention

Given how often we share our routing and account numbers, a common question arises: Is it safe to give this information out? In the context of “Money” and personal finance, understanding the risks and protections is essential.

Is It Safe to Share Your Routing Number?

Strictly speaking, your routing number is public information. However, when combined with your account number, a malicious actor could theoretically initiate unauthorized ACH withdrawals. This is why you should only provide these numbers to trusted entities, such as your employer, the IRS, or established utility companies.

Protecting Your Financial Information

To maintain high financial security, follow these best practices:

- Monitor Your Accounts: Check your transaction history at least once a week. Because routing and account numbers are “open” identifiers, the best defense is vigilance. If you see an unauthorized ACH withdrawal, you have a limited window (typically 60 days for consumers) to report it and get your money back.

- Use Secure Portals: Never send your routing and account numbers via unencrypted email. Always use a secure, “https” encrypted portal provided by the bank or the service provider.

- Shred Old Checks: If you close an account or move, shred your old checks. A discarded check contains both your routing and account numbers in plain sight, providing a roadmap for potential identity thieves.

By understanding how to find and use your routing number, you gain greater control over your personal finances. Whether it’s ensuring your paycheck arrives on time or securely paying your bills, this nine-digit code is an indispensable tool in your financial toolkit. Through careful management and a clear understanding of the banking system’s mechanics, you can navigate the world of electronic payments with confidence and precision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.