In the complex yet indispensable world of personal finance, a routing number stands as a fundamental identifier, often overlooked until its immediate need arises. This nine-digit code is far more than just a sequence of numbers; it’s the digital fingerprint of your financial institution, playing a critical role in facilitating nearly every electronic money transfer within the United States. Whether you’re setting up direct deposit for your paycheck, paying bills online, or initiating a wire transfer, knowing precisely where to locate this crucial piece of information is paramount.

This guide will demystify the routing number, explain its various functions, and, most importantly, provide clear, actionable instructions on where and how to reliably find it. Understanding your routing number is a cornerstone of financial literacy, empowering you to manage your money efficiently and securely in an increasingly digital economy.

Understanding the Crucial Role of a Routing Number

Before we delve into its discovery, it’s essential to grasp what a routing number is and why it holds such significant weight in your financial dealings. It’s not merely a random identifier but a carefully assigned code that ensures your money reaches its intended destination without a hitch.

What Exactly Is a Routing Number?

A routing number, officially known as an American Bankers Association (ABA) routing transit number, is a nine-digit code used to identify a specific financial institution in the United States. It was established by the ABA in 1910 to process paper checks, but its role has dramatically expanded with the advent of electronic banking. Think of it as a postal code for your bank, enabling the correct delivery of funds from one account to another. Each digit within the routing number holds specific significance, identifying the bank’s district, federal reserve branch, and the bank itself.

It’s crucial to understand that a routing number is distinct from your individual bank account number. While your account number identifies your specific account within the bank, the routing number identifies the bank itself. Furthermore, it should not be confused with a SWIFT code, which is used for international wire transfers to identify banks globally. Routing numbers are specifically for domestic transactions within the U.S. banking system.

Why Is Your Routing Number So Important?

The importance of your routing number cannot be overstated, as it underpins numerous everyday financial transactions that keep your personal economy flowing smoothly.

- Direct Deposits: This is perhaps its most common application. Employers, government agencies (for Social Security or tax refunds), and various benefit providers use your routing number and account number to electronically deposit funds directly into your bank account. Without it, your paycheck or benefits could be significantly delayed.

- Automatic Bill Payments (ACH Transfers): Many people set up recurring payments for utilities, loans, mortgages, or subscriptions. These automated clearing house (ACH) transfers rely on your routing number to ensure the funds are drawn from and sent to the correct financial institutions.

- Domestic Wire Transfers: While less common for daily transactions, wire transfers for larger sums of money or time-sensitive payments often require a routing number to ensure rapid and secure delivery between U.S. banks.

- Setting Up Online Payment Services: When linking your bank account to platforms like PayPal, Venmo, or other financial apps, you’ll typically need to provide your routing number to establish the connection for deposits and withdrawals.

- Processing Paper Checks: Even in the digital age, paper checks still circulate. When you write a check, your bank’s routing number is pre-printed on it, allowing the recipient’s bank to identify your bank and process the payment correctly.

In essence, any transaction that involves moving money electronically into or out of your bank account within the U.S. will almost certainly require a routing number.

Primary Locations to Discover Your Routing Number

Given its critical importance, financial institutions make it relatively easy to find your routing number through several reliable channels. Knowing these sources can save you time and prevent potential financial headaches.

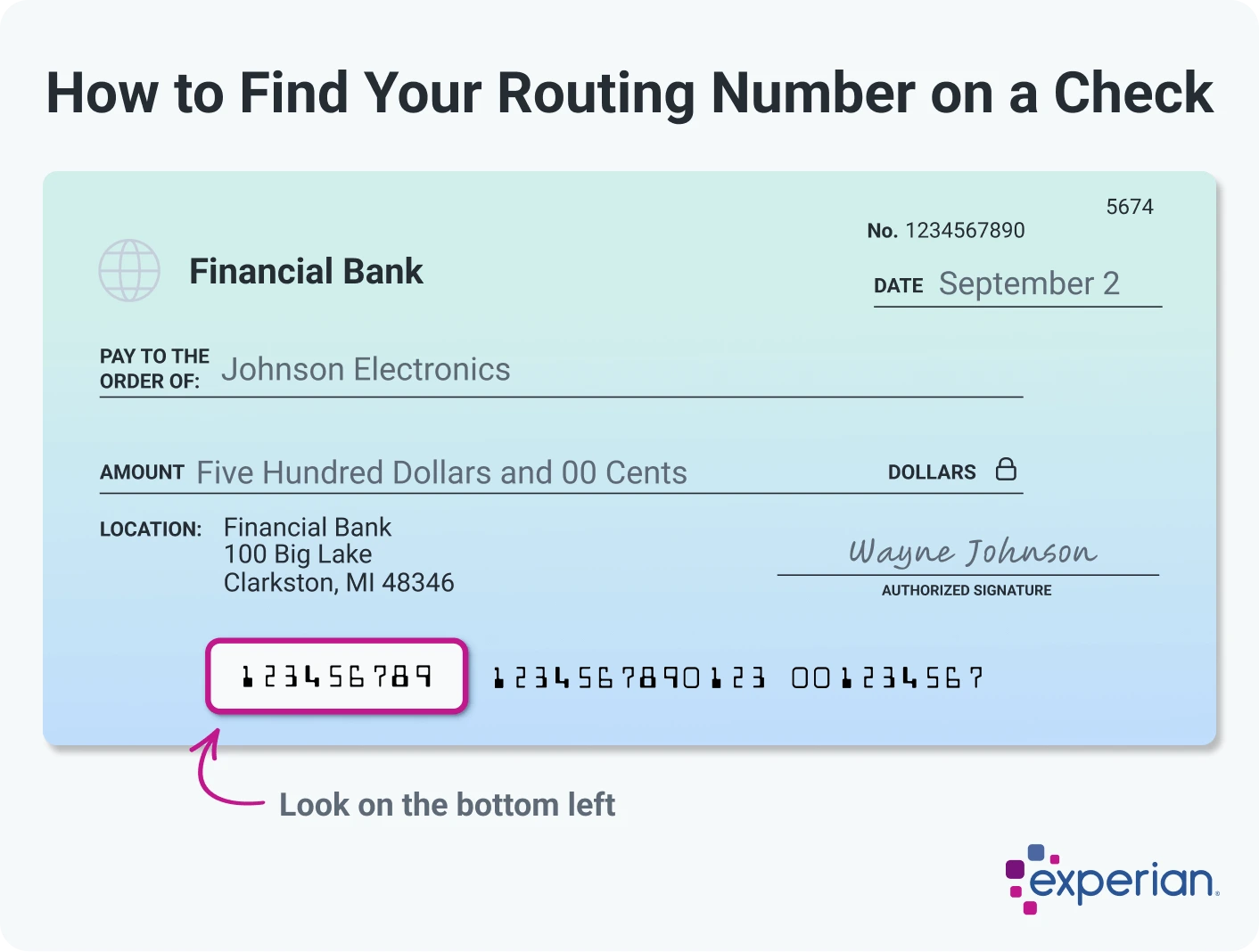

On Your Physical Checks

For many, the quickest and most traditional way to find a routing number is by looking at a physical check from your checking account. This method is straightforward and has been a standard practice for decades.

Typically, your routing number is the first set of nine digits printed at the bottom left-hand side of your check. Following it will be your account number, and then the check number. It’s usually separated by special symbols or spaces to distinguish it from the other numbers. However, layouts can vary slightly, so always confirm. If you use temporary checks provided when you first opened an account, these might sometimes lack the pre-printed routing number, so it’s always best to use a permanent, personalized check if available. Keep in mind this method is specific to checking accounts, as savings accounts do not have associated checks.

Through Your Bank’s Online Banking Portal or Mobile App

In today’s digital age, your bank’s online platform or mobile application is often the most convenient and up-to-date source for your routing number. This method is particularly useful for those who don’t use physical checks or prefer digital access.

Most financial institutions prominently display routing information within your online banking portal or mobile app. After logging in, navigate to your account details, account summary, or a specific section labeled “Routing Number,” “Account Information,” or “Direct Deposit Information.” For many banks, it might be found by clicking on the specific checking or savings account you wish to retrieve the number for. Some banks even have a dedicated search function or an FAQ section that provides this information. This method also often indicates if different routing numbers are used for specific transaction types (e.g., wire transfers vs. ACH).

On Your Monthly Bank Statements

Your monthly bank statements, whether paper or electronic, are another reliable source for your bank’s routing number. These documents provide a comprehensive overview of your account activity and essential banking details.

If you receive paper statements in the mail, your routing number is usually printed near your account number and other bank information at the top or bottom of the statement. For those who opt for electronic statements, you can access these through your online banking portal. Download a recent e-statement (usually in PDF format), and you’ll find the routing number in a similar location as a physical statement. This method is particularly useful if you don’t have access to your checks or prefer a documented source. Always ensure you’re looking at a recent statement, especially if there have been any bank mergers or changes.

By Contacting Your Financial Institution Directly

When all else fails, or if you require specific routing numbers for specialized transactions (like a domestic wire transfer, which might use a different number than ACH), contacting your bank directly is the most definitive solution.

You can call your bank’s customer service line, which is usually found on their official website, the back of your debit card, or on a recent statement. Be prepared to verify your identity with personal information such as your account number, address, and potentially answers to security questions. Alternatively, you can visit a local branch in person. A bank teller or customer service representative will be able to provide you with the correct routing number and clarify any specific requirements for different types of transactions. This method ensures accuracy and allows for clarification on any unique banking circumstances you might have.

Nuances and Specific Scenarios for Routing Numbers

While the methods above cover most situations, there are a few nuances and specific scenarios related to routing numbers that are worth understanding to avoid potential errors.

Different Routing Numbers for Different Purposes?

Yes, it’s a common misconception that a bank has only one routing number. While many banks use the same routing number for most common transactions like direct deposits and ACH payments, some larger financial institutions might have different routing numbers for specific types of transfers.

For instance, a bank might use one routing number for standard ACH transactions (like direct deposits and bill payments) and a completely different one for incoming domestic wire transfers. This is because these different transaction types often route through separate processing networks within the financial system. It is absolutely critical to confirm the correct routing number for the specific transaction you intend to make. Using a wire transfer routing number for an ACH payment, or vice-versa, can result in delays, rejections, or even loss of funds. When contacting your bank or looking online, always specify the type of transaction you are performing.

Routing Numbers for Various Account Types

Typically, if you have both a checking and a savings account at the same bank, they will share the same routing number. The routing number identifies the bank, not the specific account type. However, there can be exceptions, especially if your savings account is structured differently or held by a subsidiary.

For credit unions, the principles remain the same as traditional banks; they will also have a unique nine-digit routing number. Online-only banks or fintech companies that offer banking services often partner with traditional banks for FDIC insurance. In these cases, the routing number you use will likely belong to the underlying partner bank. Always refer to the online banking portal or contact customer service for these modern banking solutions.

What if Your Bank Merges or Changes Names?

Bank mergers and acquisitions are not uncommon in the financial industry. When two banks combine, or one bank acquires another, there is often a transition period during which routing numbers might change.

If your bank merges with another institution, it’s highly probable that a new routing number will be issued for all accounts, or the acquiring bank’s routing number will become standard. Financial institutions are legally obligated to communicate these changes to their customers well in advance. You will typically receive notices via mail, email, or through your online banking portal, detailing the effective date of the change and any actions you need to take. It’s crucial to update any recurring direct deposits or automatic payments with the new routing number to prevent disruptions to your financial flow. Always keep an eye on communications from your bank regarding such significant changes.

Best Practices and Security Considerations

Having a routing number is powerful, but with power comes responsibility. It’s vital to handle this piece of financial information securely and judiciously.

Always Verify Before Using

The single most important best practice when dealing with your routing number is to always verify it before initiating any transaction. Mistakes can be costly, leading to significant delays, bounced payments, or even the accidental transfer of funds to the wrong institution.

- Double-Check All Digits: A single digit error can redirect funds.

- Confirm with the Recipient: If someone is asking for your routing number, ensure their request is legitimate and that you provide the correct number for the specific type of transaction they intend.

- Use Official Sources: Rely only on your bank’s official website, secure online banking portal, physical checks, or direct communication with bank staff. Avoid getting routing numbers from third-party websites unless they are officially linked to your bank.

Protecting Your Financial Information

While a routing number alone isn’t enough for someone to drain your bank account, combined with your account number, it becomes highly sensitive information. This combination could potentially be used to initiate unauthorized ACH debits.

- Be Cautious Online: Only enter your routing and account numbers on secure, encrypted websites (look for “https://” in the URL and a padlock symbol).

- Beware of Phishing: Legitimate banks will rarely ask for your full account and routing number via unsolicited emails or text messages. Be highly suspicious of any communication requesting this information.

- Secure Physical Documents: Shred old bank statements or checks before discarding them.

When NOT to Share Your Routing Number

While essential for legitimate financial transactions, there are times when you should exercise extreme caution or outright refuse to share your routing number.

- Unsolicited Requests: Never provide your routing number to unknown individuals or organizations that contact you out of the blue, especially if they claim you’ve won a lottery or need to pay an urgent fee.

- Suspicious Websites/Apps: If a website or mobile app seems untrustworthy or asks for unnecessary financial details, do not input your routing number or any other banking information.

- Public Forums: Avoid posting your routing number on social media or other public online platforms, as this makes you vulnerable to identity theft and fraud.

Only share your routing number with trusted entities for legitimate purposes where you have initiated the transaction or have a well-established relationship.

Understanding “where can you find a routing number” is more than just a trivial piece of knowledge; it’s a fundamental aspect of managing your personal finances effectively and securely. From setting up crucial direct deposits to facilitating online bill payments, this nine-digit code is the backbone of domestic electronic money movement. By knowing its importance, its various uses, and the reliable places to locate it, you empower yourself with greater control over your financial life. Always prioritize accuracy and security when handling this essential banking identifier to ensure your financial transactions proceed smoothly and safely.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.