Navigating the landscape of student loans can feel like a complex journey, but understanding your options is the first crucial step toward funding your education. Student loans serve as a vital financial bridge for millions, helping to cover tuition, housing, books, and other living expenses while pursuing higher education. The primary sources for these loans fall into two broad categories: federal student loans, offered by the U.S. government, and private student loans, provided by banks, credit unions, and other financial institutions. Each category comes with distinct advantages, disadvantages, and application processes that warrant careful consideration.

Understanding Your Student Loan Options

Before committing to any loan, it’s essential to grasp the fundamental differences between federal and private student loans. Federal loans are typically considered the first and best option due to their borrower-friendly terms, which include fixed interest rates, income-driven repayment plans, and opportunities for deferment or forbearance in times of financial hardship. Private loans, while necessary for some, often have higher, variable interest rates and fewer consumer protections, making them a secondary choice once all federal options have been exhausted.

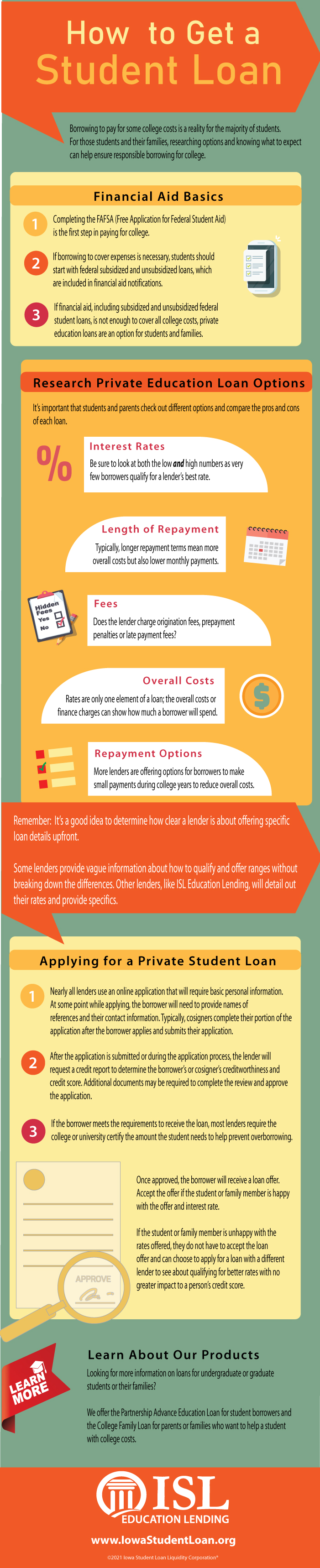

The key to responsible borrowing begins with maximizing “free money” – scholarships and grants – which never have to be repaid. Only after exploring these avenues should you turn to loans, and even then, federal loans should always be prioritized.

Federal Student Loans: Your Primary Resource

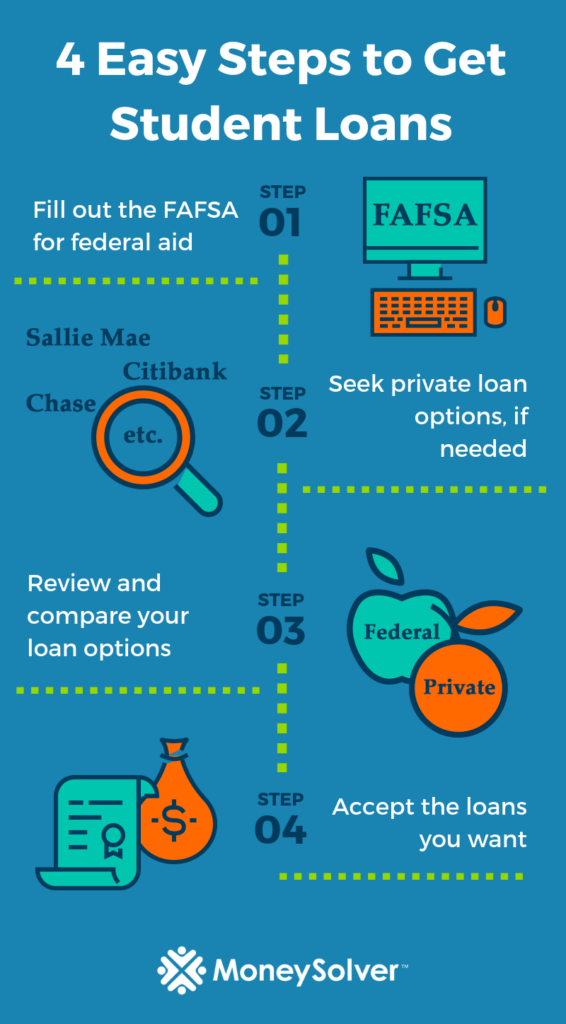

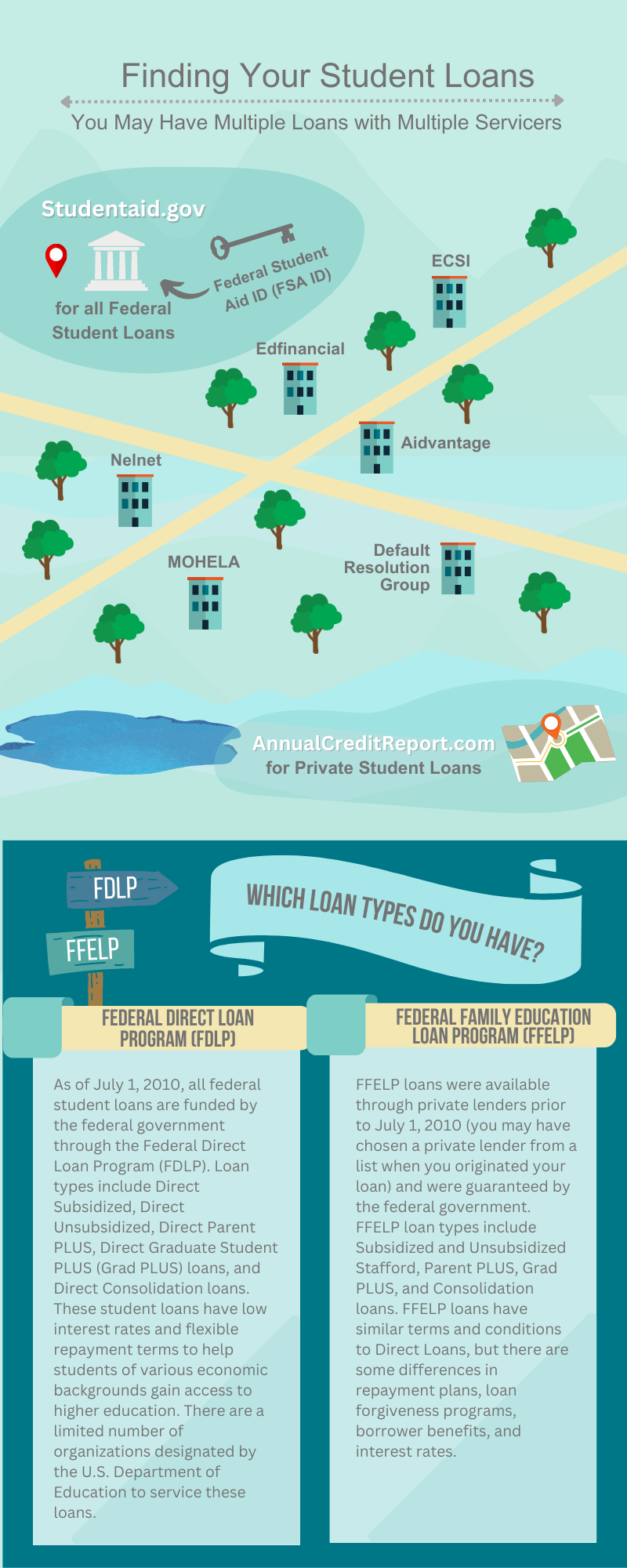

Federal student loans are backed by the U.S. Department of Education and are generally the most advantageous borrowing option for students. To access them, you must complete the Free Application for Federal Student Aid (FAFSA) annually. The FAFSA determines your eligibility for all types of federal financial aid, including grants, work-study programs, and various federal student loans.

The main types of federal student loans available include:

- Direct Subsidized Loans: These are available to undergraduate students who demonstrate financial need. The U.S. Department of Education pays the interest on these loans while you’re in school at least half-time, during your grace period (typically six months after leaving school), and during periods of deferment. This makes them the most cost-effective federal loan option.

- Direct Unsubsidized Loans: These loans are available to both undergraduate and graduate students, regardless of financial need. Unlike subsidized loans, interest begins to accrue immediately after the loan is disbursed, even while you are in school. You are responsible for all the interest. You can choose to pay the interest while in school or defer it, but deferred interest will be capitalized (added to your principal balance), increasing the total amount you owe.

- Direct PLUS Loans: These are available to graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). Eligibility for PLUS loans is not based on financial need, but a credit check is required. Borrowers with adverse credit histories may need an endorser (co-signer) or to document extenuating circumstances. PLUS loans have higher interest rates than subsidized or unsubsidized loans and typically come with an origination fee.

- Federal Consolidation Loans: While not a direct loan type for new borrowing, a Direct Consolidation Loan allows you to combine multiple federal education loans into a single loan with one loan servicer and one monthly payment. This can simplify repayment but may extend the repayment period and increase the total interest paid over time.

Key Advantages of Federal Loans:

- Fixed Interest Rates: Your interest rate won’t change over the life of the loan, providing predictability.

- Income-Driven Repayment (IDR) Plans: These plans adjust your monthly payment based on your income and family size, offering a safety net if your post-graduation income is lower than expected.

- Public Service Loan Forgiveness (PSLF): If you work for a qualifying government or non-profit organization, your remaining federal loan balance may be forgiven after 120 qualifying monthly payments.

- Deferment and Forbearance: These options allow you to temporarily postpone or reduce your loan payments during periods of financial hardship, unemployment, or returning to school.

- No Credit Check (for most undergraduate loans): Direct Subsidized and Unsubsidized Loans do not require a credit check, making them accessible to students with limited credit history.

How to Apply for Federal Loans:

The process always begins with completing the FAFSA. You can fill it out online at studentaid.gov. Be sure to submit it as early as possible each year, as some federal aid is awarded on a first-come, first-served basis. Your college financial aid office will then use your FAFSA information to create an aid package that may include federal loans.

Navigating Private Student Loans

Private student loans are offered by banks, credit unions, and other private lenders. They are typically used to bridge the gap between the cost of attendance and what federal financial aid covers. Unlike federal loans, private loans are credit-based, meaning lenders will assess your creditworthiness (or that of a co-signer) to determine eligibility, interest rates, and loan terms.

Where to Find Private Student Loans:

- Traditional Banks: Large national banks (e.g., Chase, Wells Fargo, PNC) and regional banks often offer student loan products.

- Credit Unions: Local credit unions can be a good option, sometimes offering competitive rates and more personalized service to members.

- Online Lenders: A growing number of online-only lenders (e.g., Sallie Mae, Discover, Ascent, College Ave) specialize in student loans, often featuring streamlined application processes and various repayment options.

- State-Based Lenders: Some states offer their own student loan programs, which can sometimes provide favorable terms to residents.

Key Considerations for Private Loans:

- Creditworthiness: Most students have little to no credit history, making a co-signer almost a necessity for private loans. A co-signer (typically a parent or another adult) assumes equal responsibility for the debt, and their good credit can help you qualify for the loan and secure a lower interest rate.

- Variable vs. Fixed Interest Rates: Private loans offer both. Variable rates can start lower but can fluctuate over the life of the loan, potentially increasing your monthly payments. Fixed rates remain constant, offering predictability. Most financial advisors recommend fixed rates to avoid unexpected payment hikes.

- Fewer Borrower Protections: Private loans generally lack the flexible repayment options (like income-driven repayment) and forgiveness programs available with federal loans. Deferment and forbearance options may be limited or less generous.

- Loan Fees: Some private loans may come with origination fees or other charges, which can increase the overall cost of borrowing.

- Repayment Terms: Private loan repayment terms can vary widely, from 5 to 15 or 20 years. Shorter terms typically mean higher monthly payments but less interest paid over time.

How to Apply for Private Loans:

- Exhaust Federal Aid: Confirm you have applied for and accepted all available federal loans, grants, and scholarships first.

- Research Lenders: Compare interest rates, fees, repayment terms, and borrower benefits from multiple private lenders. Read reviews and check their customer service ratings.

- Gather Documentation: You’ll typically need proof of enrollment, income verification (for you or your co-signer), and possibly tax returns.

- Apply with a Co-signer: If you have limited credit, applying with a creditworthy co-signer will significantly improve your chances of approval and help you secure a better rate.

- Review Loan Offer: Carefully read all terms and conditions before signing any loan agreement. Understand the interest rate (fixed or variable), repayment schedule, fees, and any penalties for late payments.

Exploring Alternative Funding and Smart Strategies

While student loans are a significant resource, they shouldn’t be your only consideration. A holistic approach to funding your education involves exploring all available avenues and making informed decisions to minimize your overall debt.

Beyond Loans:

- Scholarships and Grants: These are gift aid that you don’t have to repay. Sources include colleges, private organizations, community groups, and the federal government. Search engines like Fastweb, Scholarship.com, and the College Board’s scholarship search can help.

- Work-Study Programs: If you qualify for federal financial aid, you may be offered a work-study award, allowing you to earn money through part-time jobs on or off campus to help cover educational expenses.

- Employer Tuition Assistance: If you are currently employed, check if your employer offers tuition reimbursement or assistance programs. Many companies invest in their employees’ education.

- Military Benefits: Veterans and active-duty service members may qualify for substantial educational benefits through programs like the GI Bill.

- Personal Savings: Any amount you can contribute from savings will reduce your reliance on loans.

Smart Borrowing Strategies:

- Borrow Only What You Need: Calculate your actual expenses and only borrow the minimum necessary. Every dollar borrowed accrues interest.

- Create a Budget: Understand your total cost of attendance (tuition, fees, room, board, books, personal expenses, transportation) and create a budget to manage your spending while in school.

- Live Frugally: While in college, making conscious choices to save money on housing, food, and entertainment can significantly reduce the amount you need to borrow.

- Understand Repayment: Before you even take out a loan, have a basic understanding of how repayment works. Know your potential monthly payments and interest accrual.

- Build Good Credit (even before private loans): Start building good credit history early by using a secured credit card responsibly or becoming an authorized user on a parent’s card. This will be beneficial if you need private loans in the future.

Responsible Borrowing and Repayment Planning

The decision to take on student loans is a serious financial commitment. It’s not just about where to get them, but how to manage them responsibly through repayment.

Before graduation, most federal loan borrowers participate in exit counseling, which provides critical information about your loan servicer, repayment options, and borrower responsibilities. Understanding your loan terms – including interest rates, repayment start dates, and potential penalties for missed payments – is paramount.

Federal loans offer various repayment plans, including the Standard 10-year plan, Extended plans, Graduated plans, and several Income-Driven Repayment (IDR) plans. IDR plans are particularly helpful for those with lower post-graduation incomes, as they cap your monthly payment at an affordable percentage of your discretionary income.

For both federal and private loans, strategies to minimize your debt include:

- Making interest payments while you’re in school, if possible, especially on unsubsidized and private loans.

- Making extra payments on the principal whenever you can afford it.

- Exploring refinancing options for private loans (or even federal loans, though this forfeits federal protections) after graduation, especially if you have a stable job and improved credit, to potentially secure a lower interest rate.

Ultimately, securing student loans is a strategic decision that empowers you to invest in your future. By prioritizing federal aid, carefully evaluating private loan options, maximizing free money, and planning for responsible repayment, you can navigate the process effectively and achieve your educational goals without undue financial burden.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.