The question “Where are my federal taxes?” is more than just a passing thought; it’s a fundamental inquiry into the very fabric of our financial system and civic responsibility. For millions of Americans, the act of paying federal taxes is an annual, often complex, obligation. Yet, the tangible destination and impact of those hard-earned dollars can feel abstract, shrouded in bureaucratic layers. Understanding where your federal taxes go is not merely an academic exercise; it is crucial for informed citizenship, personal financial planning, and appreciating the vast ecosystem of public services and economic policies they support. This article delves into the journey of your federal tax contributions, from collection to allocation, illuminating the mechanisms and the ultimate beneficiaries of your financial commitment to the nation.

Unpacking the Fundamentals of Federal Taxation

Before we can trace the path of your tax dollars, it’s essential to grasp the foundational principles and structures of federal taxation in the United States. This understanding forms the bedrock upon which all subsequent financial flows are built, defining why we pay and who orchestrates the process.

The Mandate of Taxation: Why We Pay

At its core, taxation is the primary mechanism through which governments fund public goods and services. Without taxes, there would be no shared resources for defense, infrastructure, education, public health, or social safety nets. The U.S. Constitution grants Congress the power to lay and collect taxes, duties, imposts, and excises, enabling the federal government to “provide for the common Defence and general Welfare of the United States.” This mandate underscores a collective agreement: individuals contribute a portion of their income and wealth to support a society that benefits everyone. From maintaining national security to fostering economic stability, federal taxes are the lifeblood of collective action and national progress.

Key Federal Tax Types: Income, Payroll, and More

The federal tax system is not a monolith; it comprises several distinct categories, each with its own purpose and impact on individual finances. The two most significant for most Americans are income taxes and payroll taxes.

- Income Taxes: Levied on wages, salaries, investments, and other forms of income, these are progressive, meaning higher earners pay a larger percentage of their income in taxes. Income tax revenue is the single largest source of federal funds, used to finance a vast array of government activities.

- Payroll Taxes: These taxes, primarily Social Security and Medicare taxes (often seen as FICA contributions on your paycheck), are earmarked for specific social insurance programs. Social Security provides retirement, disability, and survivor benefits, while Medicare covers healthcare costs for the elderly and disabled. Both employees and employers contribute to these funds.

Beyond these, other federal taxes include corporate income taxes on business profits, excise taxes on specific goods like gasoline and tobacco, estate taxes on inherited wealth, and customs duties on imported goods. Each contributes to the overall federal revenue stream, albeit in varying proportions.

The Role of the Internal Revenue Service (IRS)

The Internal Revenue Service (IRS) stands as the primary federal agency responsible for tax collection and administration. While often perceived solely as an enforcement body, the IRS’s role is multifaceted. It interprets and enforces federal tax laws, processes tax returns, issues refunds, and provides taxpayer assistance. It also plays a critical role in educating the public about their tax obligations and rights. The efficiency and integrity of the IRS are paramount, as it is the conduit through which billions of dollars flow from individual taxpayers and businesses into the federal treasury, ensuring the operational capacity of the entire government.

Tracing the Flow: Where Your Tax Dollars Go

Once collected, your federal tax dollars don’t sit idly. They are meticulously allocated across an expansive range of government programs and services, reflecting national priorities and legal mandates. Understanding these broad categories helps paint a clearer picture of the tangible impact of your contributions.

Funding Essential Government Operations and Services

A significant portion of federal tax revenue is dedicated to the day-to-day operations of the government itself and the fundamental services it provides. This includes the salaries of federal employees, from postal workers to scientists; the upkeep of federal buildings; and the administrative costs of countless agencies that serve the public. Beyond basic operations, these funds support critical services such such as national parks maintenance, disaster relief efforts coordinated by FEMA, and the vital work of regulatory bodies ensuring consumer safety and environmental protection. In essence, these are the costs of running the country and delivering the basic functionalities citizens expect from their government.

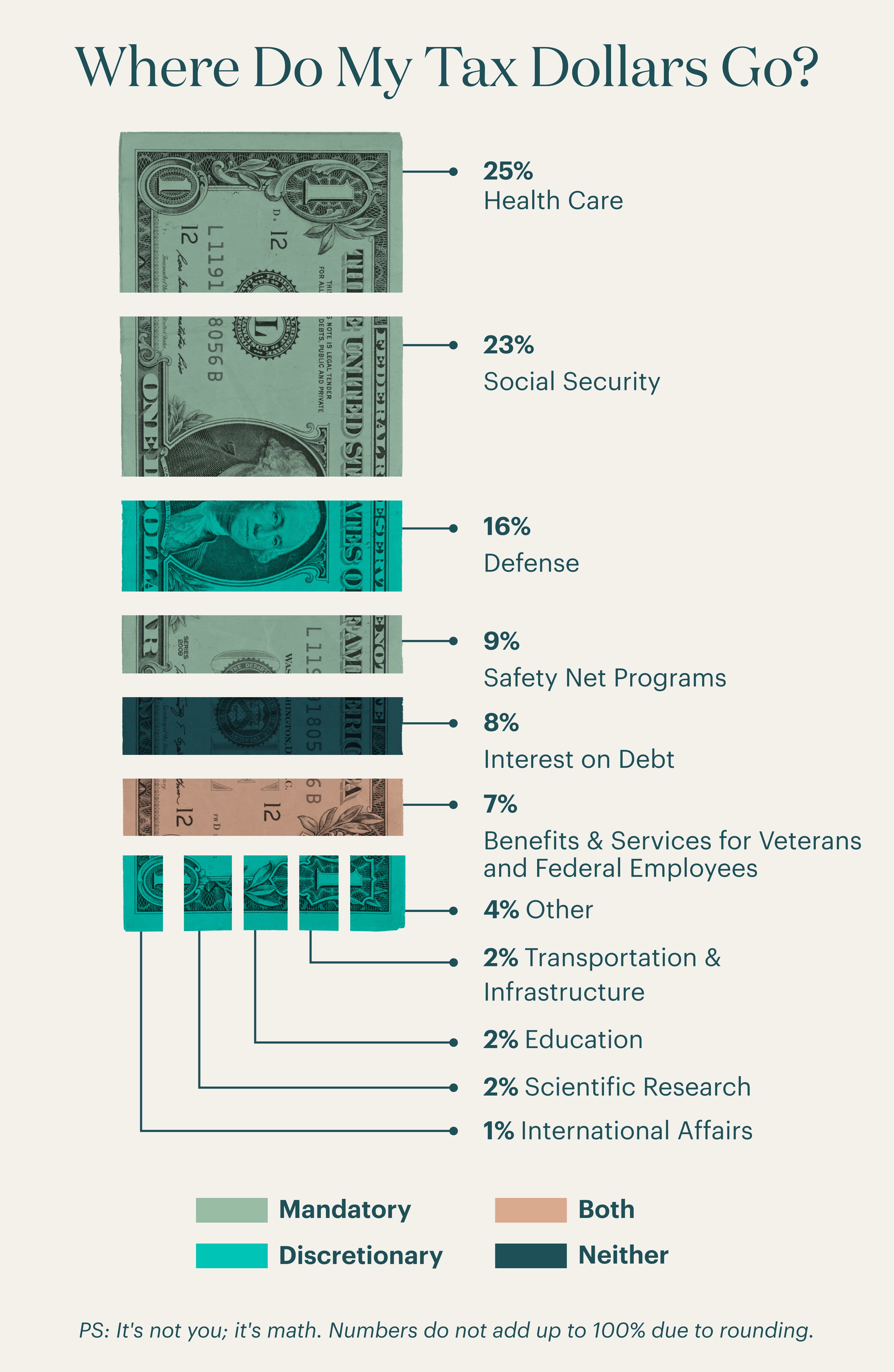

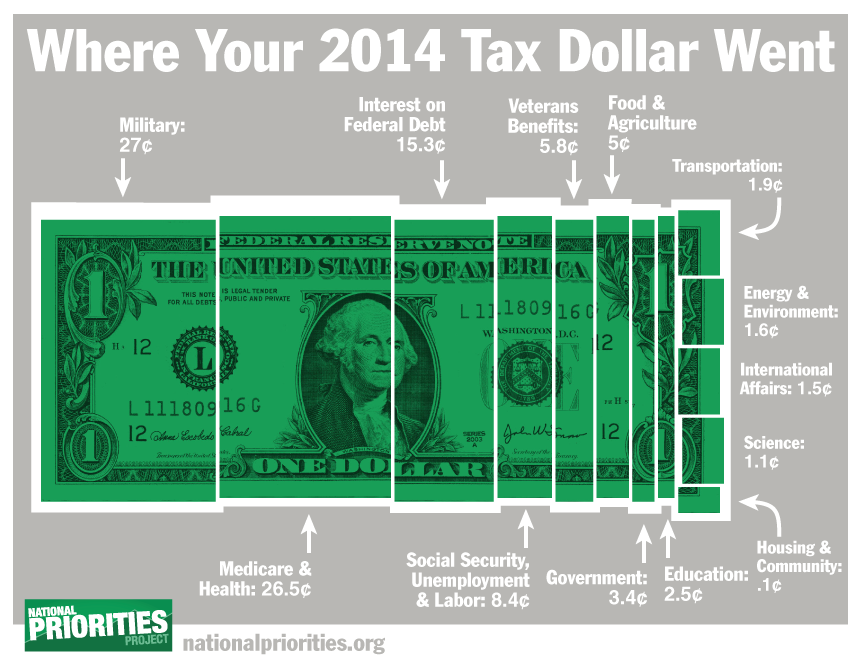

Major Spending Categories: Social Security, Medicare, and Defense

Three areas consistently command the largest share of the federal budget, primarily funded by a combination of general revenues and dedicated payroll taxes:

- Social Security: As a pay-as-you-go system, current payroll tax contributions largely fund benefits for current retirees, disabled individuals, and survivors. It represents a promise of financial security for millions of Americans in their golden years or times of need.

- Medicare: This federal health insurance program provides critical healthcare coverage for individuals aged 65 or older, younger people with disabilities, and people with End-Stage Renal Disease. Its increasing costs reflect an aging population and rising healthcare expenditures.

- National Defense: Funding for the Department of Defense covers military personnel, weapons systems, research and development, and operations around the globe. It is aimed at protecting national security interests, deterring aggression, and maintaining global stability.

These three categories alone often account for more than half of all federal spending, illustrating their central role in the nation’s priorities and the substantial financial commitment required to sustain them.

Investing in Infrastructure, Education, and Research

Beyond the major entitlement programs and defense, federal taxes are also crucial for long-term investments that drive national progress and economic growth.

- Infrastructure: Funds are allocated to build and maintain roads, bridges, airports, waterways, and public transit systems, facilitating commerce, enhancing safety, and improving quality of life. The condition of a nation’s infrastructure is a direct reflection of its investment priorities.

- Education: While primary and secondary education are largely state and local responsibilities, the federal government provides significant funding for higher education (student aid, research grants), special education programs, and initiatives aimed at improving educational outcomes and ensuring equitable access.

- Research and Development: Federal agencies like the National Institutes of Health (NIH), the National Science Foundation (NSF), and NASA fund groundbreaking scientific research in medicine, technology, space exploration, and environmental science. These investments not only push the boundaries of human knowledge but also often lead to innovations with vast economic and social benefits.

These investments, though often less visible in daily life than a Social Security check, lay the groundwork for future prosperity, innovation, and competitiveness on the global stage.

The Journey from Payer to Public Good: Collection & Disbursement

Understanding the “where” is inextricably linked to the “how.” The collection and disbursement processes are intricate, involving various stages from individual payments to complex governmental budget allocations. This journey highlights the mechanics that transform individual contributions into collective resources.

Withholding, Estimated Payments, and Tax Filings

For most wage earners, federal taxes are collected throughout the year through payroll withholding. Employers deduct an estimated amount of income and payroll taxes from each paycheck, remitting these funds to the IRS on the employee’s behalf. This “pay-as-you-go” system ensures a steady stream of revenue for the government and prevents a massive, unmanageable tax bill at year-end for individuals.

For self-employed individuals, freelancers, and those with significant income not subject to withholding, estimated tax payments are required. These quarterly payments ensure they also contribute their share throughout the year.

Finally, the annual tax filing process (typically by April 15th) serves as a reconciliation. Taxpayers calculate their actual tax liability for the year, comparing it to the amounts already withheld or paid. This results in either a tax refund (if too much was paid) or an additional payment (if too little was paid). This filing confirms individual financial contributions and adjusts any discrepancies.

The Federal Budget Process: Allocation and Appropriation

Once collected, federal tax revenues flow into the U.S. Treasury. However, the decision of how these funds are spent is a complex, multi-stage process involving both the Executive Branch and Congress.

- President’s Budget Request: The President submits an annual budget proposal to Congress, outlining the administration’s spending priorities for the upcoming fiscal year.

- Congressional Review and Action: Congress then reviews, revises, and ultimately passes a series of appropriation bills. These bills legally authorize federal agencies to spend money for specific purposes. This legislative process involves numerous committees, debates, and negotiations, reflecting the diverse priorities and political landscape of the nation.

The federal budget categorizes spending into two main types: mandatory and discretionary. Mandatory spending (e.g., Social Security, Medicare, interest on the national debt) is determined by existing laws and is not subject to annual appropriation. Discretionary spending (e.g., defense, education, infrastructure) is decided annually by Congress through the appropriations process. This distinction is crucial for understanding the flexibility—or lack thereof—in how future tax dollars can be allocated.

Understanding the National Debt and Deficit

A complete picture of federal finances must include an understanding of the national debt and the annual budget deficit. When the government spends more than it collects in revenue in a given fiscal year, it incurs a budget deficit. To cover this shortfall, the government must borrow money, primarily by issuing Treasury securities. The accumulation of these annual deficits over time constitutes the national debt. Interest payments on this debt become a mandatory spending item, claiming a portion of tax revenues that could otherwise fund other programs. While federal taxes directly fund current spending, they also indirectly contribute to managing the debt by providing the revenue base from which interest payments are made. The size and trajectory of the national debt are significant financial concerns, influencing economic stability and future generations’ tax burdens.

Seeking Clarity: Tools for Taxpayer Transparency

For taxpayers, understanding where their money goes can feel like peering into a black box. However, various resources and tools exist to shed light on government finances and help individuals track their tax contributions and their ultimate impact.

Accessing Government Financial Reports and Data

The U.S. government, through various agencies, provides a wealth of publicly accessible financial information. The Treasury Department regularly publishes reports on federal revenues and expenditures. The Office of Management and Budget (OMB) releases the President’s budget proposal and supporting documents, offering detailed breakdowns of spending by agency and program. The Congressional Budget Office (CBO) provides independent analyses of the budget and economic projections. Websites like USAspending.gov offer searchable databases of federal spending, allowing citizens to track how funds are allocated down to the agency and even specific contract level. While navigating these resources can be daunting, they represent the official record of federal financial activity and are invaluable for those seeking a deeper understanding.

Leveraging Personal Financial Software and Tax Preparation Tools

On a more personal level, modern financial tools can help individuals track their own tax contributions and plan accordingly. Sophisticated personal finance software (e.g., Mint, Quicken) and tax preparation software (e.g., TurboTax, H&R Block) allow users to accurately calculate their tax liability, understand their deductions and credits, and track their estimated payments and refunds. While these tools primarily focus on individual compliance, they also offer insights into how much one is contributing to the federal system over time. Many even provide summaries of how income is taxed and what percentage goes to various federal programs, demystifying the direct impact of one’s own paycheck.

The Importance of Personal Record-Keeping

Beyond software, good old-fashioned personal record-keeping remains paramount. Keeping meticulous records of income statements (W-2s, 1099s), tax returns, receipts for deductible expenses, and confirmation of estimated tax payments is crucial. These records not only simplify tax filing each year but also provide a historical overview of one’s financial contributions to the federal government. Understanding your personal tax footprint over years can empower you to make more informed financial decisions, plan for future tax obligations, and engage more meaningfully in discussions about government spending and fiscal policy.

Empowering Your Financial Future: Strategic Tax Planning

Understanding where your federal taxes go is foundational, but equally important is leveraging this knowledge for proactive personal financial management. Strategic tax planning isn’t about evasion; it’s about optimizing your financial situation within the bounds of the law, ensuring you pay what you owe efficiently and effectively.

Understanding Deductions, Credits, and Exemptions

A key component of tax planning involves maximizing available tax benefits.

- Deductions reduce your taxable income. For example, contributions to traditional IRAs or 401(k)s, interest paid on student loans, or certain itemized expenses can lower the amount of income subject to tax. A lower taxable income means a lower tax bill.

- Credits directly reduce the amount of tax you owe, dollar for dollar. Unlike deductions, which reduce income, credits are a direct subtraction from your tax liability. Examples include the Child Tax Credit, education credits, or credits for energy-efficient home improvements. Credits are generally more valuable than deductions.

- Exemptions (now mostly replaced by a higher standard deduction) previously allowed taxpayers to reduce their taxable income based on the number of dependents they supported.

Understanding and appropriately utilizing these provisions is critical. It ensures you’re not overpaying and that your tax burden is fair relative to your circumstances, allowing you to retain more of your income for savings, investments, or personal spending.

Proactive Strategies for Tax Optimization

Effective tax planning is a year-round activity, not just an annual chore.

- Retirement Planning: Contributing to tax-advantaged retirement accounts like 401(k)s, IRAs (traditional or Roth), or HSAs offers immediate tax deductions or tax-free growth, significantly impacting your long-term financial health.

- Investment Strategy: Understanding how different investments are taxed (e.g., short-term vs. long-term capital gains, qualified dividends) can inform your investment decisions. Tax-loss harvesting, where you sell investments at a loss to offset capital gains, is another strategy.

- Life Event Planning: Major life events like marriage, divorce, purchasing a home, or having children all have significant tax implications. Proactively planning for these changes can help you adjust your withholding, maximize eligible deductions or credits, and avoid surprises.

- Seeking Professional Advice: For complex financial situations, consulting with a qualified tax professional (CPA, Enrolled Agent) can provide personalized guidance, ensure compliance, and identify opportunities for optimization that might be overlooked.

The Broader Impact of Informed Tax Citizenship

Ultimately, the journey of “where are my federal taxes” culminates in the understanding that your individual contributions are part of a vast, interconnected system. Being an informed tax citizen means more than just filing on time; it means understanding your role in funding society, exercising your rights to maximize your financial efficiency, and participating in the ongoing dialogue about fiscal policy and government spending. Your tax dollars are an investment in the collective future, and by understanding their trajectory, you become a more engaged and empowered participant in the nation’s financial landscape. This knowledge not only enhances your personal financial well-being but also strengthens the foundation of a transparent and accountable government.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.