To the uninitiated, the stock market can feel like a high-stakes game of chance. To the seasoned investor, however, it is a complex, breathing ecosystem defined by cycles of expansion and contraction. One of the most common questions asked by both novice savers and experienced portfolio managers is: “When was the last stock market crash?” The answer depends largely on how one defines a “crash” versus a “correction” or a “bear market,” but looking back at recent history provides a roadmap for how wealth is lost—and ultimately built—during times of crisis.

Understanding the timing and the “why” behind market collapses is not just an exercise in nostalgia. It is a fundamental component of financial literacy. By examining the catalysts of previous downturns, investors can better position their capital to withstand future volatility.

Pinpointing the Last Major Downturn: 2020 vs. 2022

When searching for the last stock market crash, two distinct periods stand out in recent memory. Depending on whether you prioritize the speed of the decline or the duration of the pain, the answer varies between the pandemic-induced “flash crash” of 2020 and the grinding bear market of 2022.

The 2020 Pandemic Flash Crash

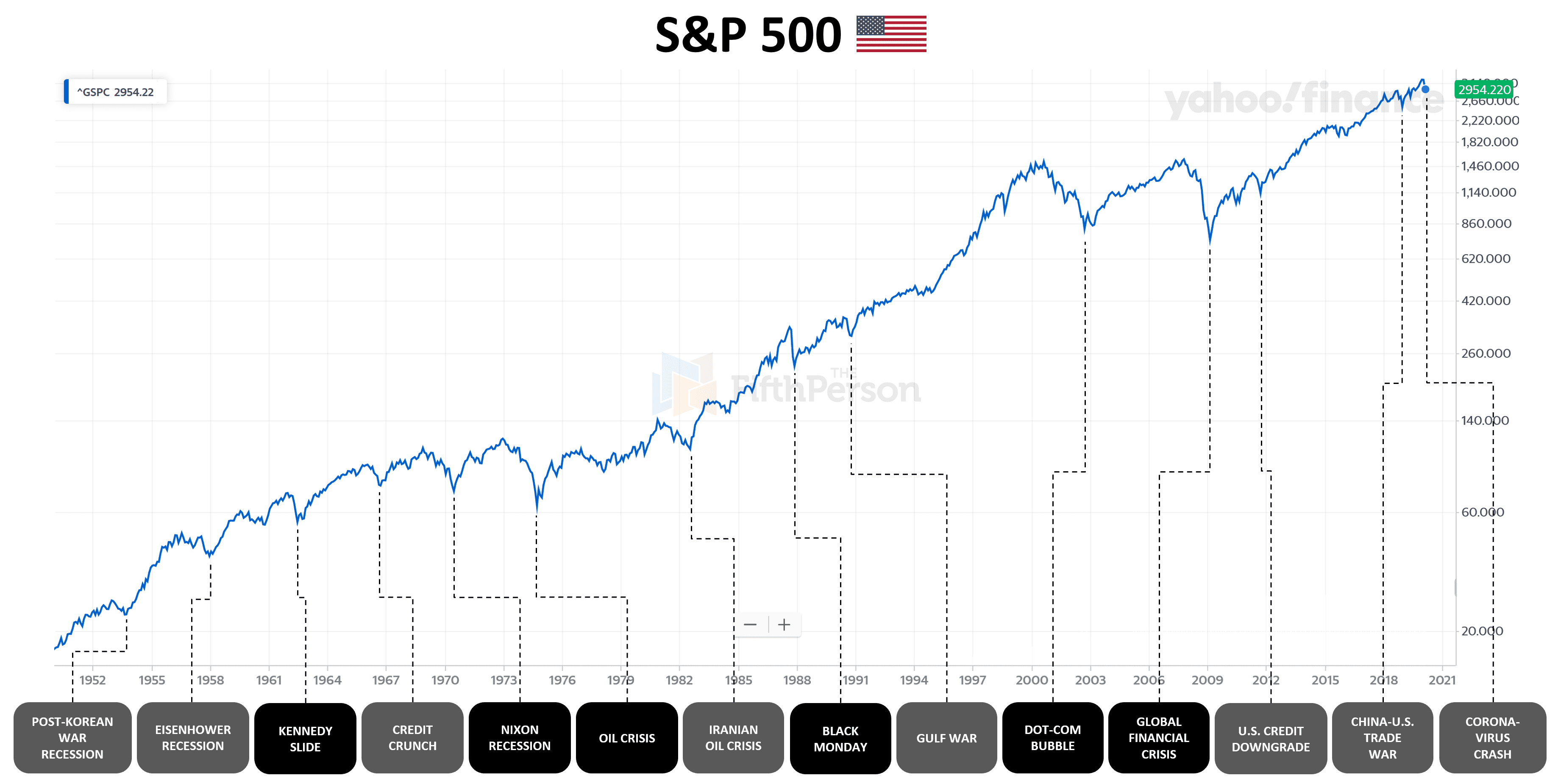

The most visceral “crash” in recent history occurred in February and March of 2020. As the COVID-19 pandemic swept across the globe, forcing unprecedented lockdowns and halting international commerce, the stock market reacted with a velocity never seen before. Between February 19 and March 23, 2020, the S&P 500 plummeted roughly 34%. This was a true “black swan” event—an unpredictable occurrence that has a massive impact.

What made 2020 unique was the speed of both the descent and the recovery. While typical crashes take months to bottom out, the 2020 crash was a vertical drop followed by a sharp “V-shaped” recovery, fueled by massive government stimulus and the Federal Reserve’s intervention. For many, this served as a masterclass in market resilience, though it also set the stage for the inflationary pressures that would haunt the market two years later.

The 2022 Inflationary Bear Market

While 2020 was a sudden shock, 2022 represented a slow, agonizing erosion of wealth. Technically defined as a bear market because the S&P 500 fell more than 20% from its peaks, 2022 was driven by a “perfect storm” of macroeconomic factors: soaring inflation, the end of “easy money” policies, and geopolitical instability following the invasion of Ukraine.

In 2022, the Nasdaq—heavy with growth and tech stocks—was particularly hit hard, falling over 33%. This period was a sobering reminder that the stock market is sensitive to interest rates. As the Federal Reserve aggressively hiked rates to combat inflation, the “discount rate” applied to future earnings increased, causing the valuations of high-growth companies to crater. For most modern investors, the 2022 downturn is the most relevant “crash” because it fundamentally shifted the investment landscape from a decade of growth-at-all-costs to a focus on profitability and valuation.

Lessons from History: The Most Significant Crashes of the Modern Era

To understand the present, we must look at the scars of the past. Every market crash leaves a legacy of new regulations, shifted investor psychology, and a reshuffled deck of dominant companies.

The 2008 Global Financial Crisis

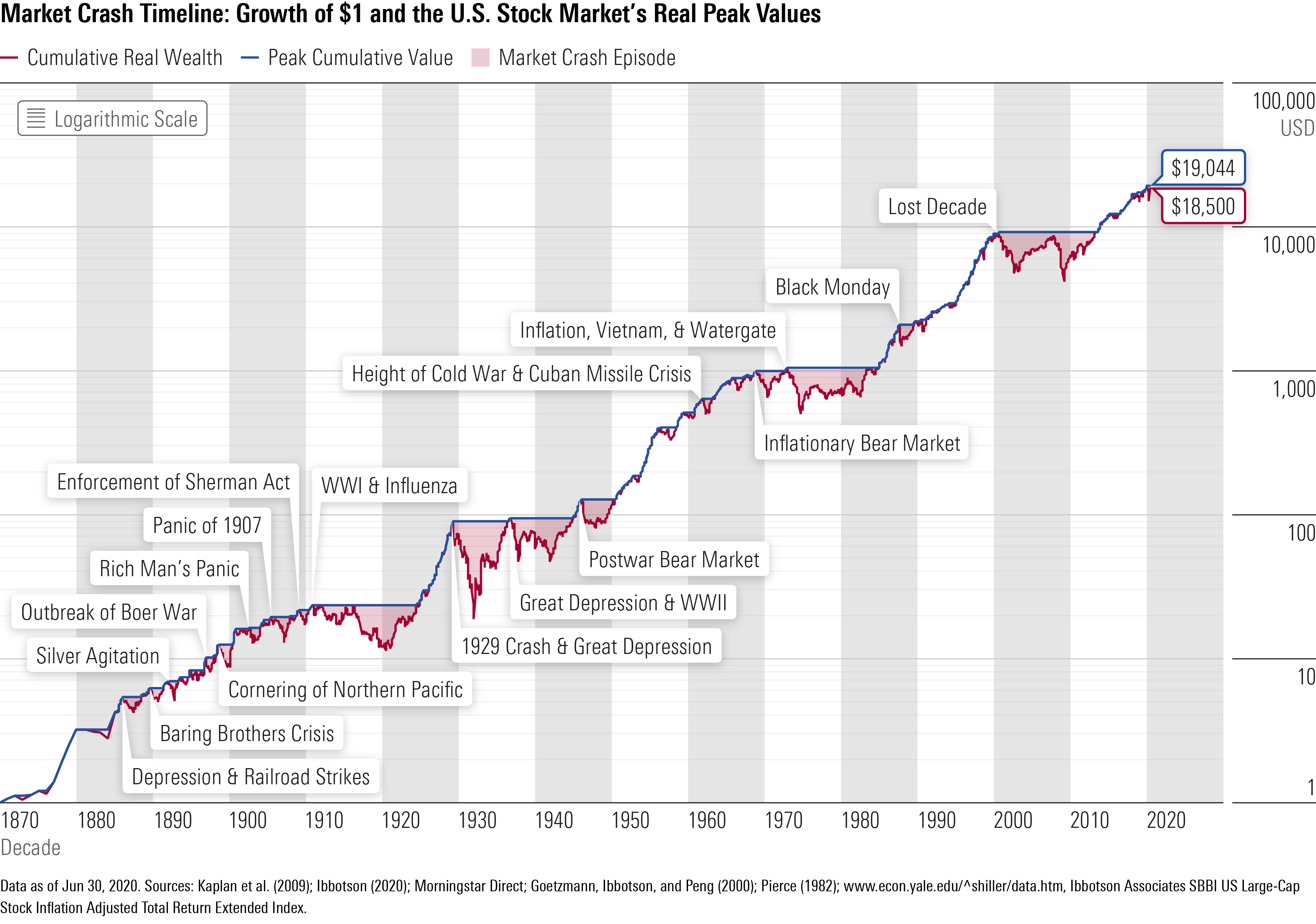

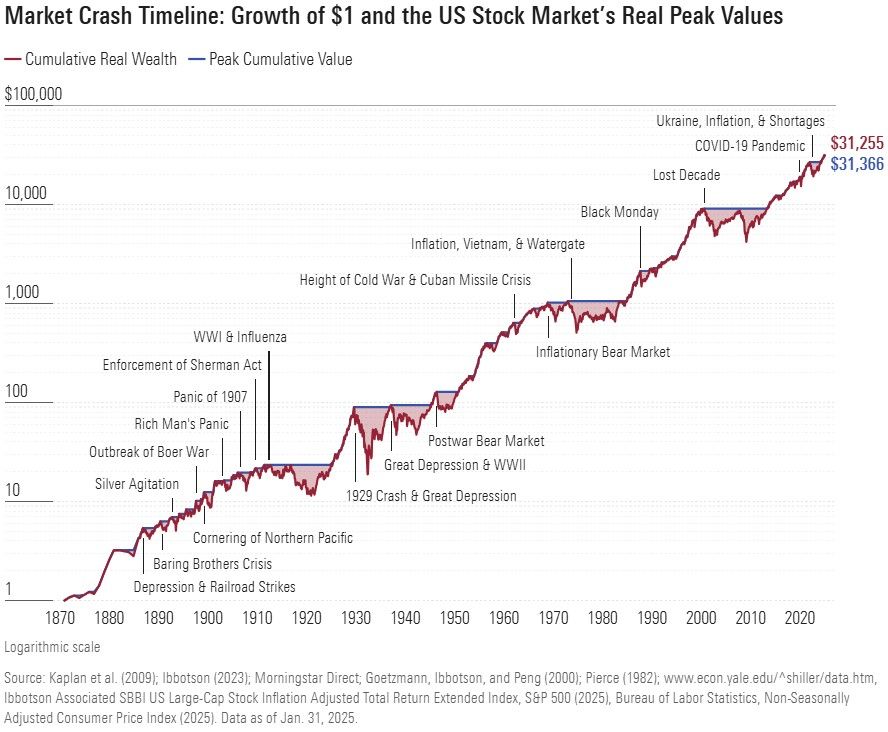

Often referred to as the “Great Recession,” the 2008 crash was systemic. Unlike the 2020 crash, which was caused by an external biological factor, 2008 was caused by internal rot within the financial system—specifically the subprime mortgage bubble and the proliferation of complex derivative products.

The S&P 500 lost approximately 50% of its value between October 2007 and March 2009. The collapse of Lehman Brothers became the symbol of this era, proving that even “too big to fail” institutions were vulnerable. The lesson for investors from 2008 was the importance of systemic risk assessment; it wasn’t just about picking good stocks, but about understanding the health of the underlying financial plumbing that supports the entire market.

The 2000 Dot-Com Bubble

At the turn of the millennium, the crash was driven by “irrational exuberance.” Investors poured billions into internet companies that had no clear path to profitability, often valued solely on “eyeballs” or “clicks.” When the bubble burst, the tech-heavy Nasdaq fell by a staggering 78% from its peak.

The Dot-Com crash taught the investment world about the danger of speculative bubbles. It served as a reminder that regardless of how revolutionary a new technology might be, the fundamental laws of economics—revenue, margins, and cash flow—eventually reassert themselves. Many of the companies that survived this crash, such as Amazon and Microsoft, went on to become the giants of the modern economy, proving that crashes often “clear the brush” for the strongest players to dominate.

Identifying the Catalysts: What Triggers a Market Collapse?

Crashes are rarely the result of a single factor. Instead, they are usually the result of several economic pressures reaching a breaking point simultaneously. By identifying these triggers, investors can better gauge when the market is moving into “danger territory.”

Macroeconomic Shifts and Interest Rates

The most influential force in the financial markets is the cost of money, also known as the interest rate. When the Federal Reserve or other central banks raise rates, borrowing becomes more expensive for companies and consumers. This slows down economic expansion and makes “safe” investments like bonds more attractive relative to “risky” investments like stocks. Most historical crashes have been preceded or accompanied by a tightening of monetary policy, making interest rate cycles a primary indicator for market health.

Asset Bubbles and Irrational Exuberance

Human psychology plays a massive role in market cycles. During long periods of prosperity, investors often become overconfident, leading to “asset bubbles” where prices far exceed intrinsic value. Whether it is Dutch tulips in the 1600s, Florida real estate in the 1920s, or tech stocks in the late 1990s, the pattern is the same: greed drives prices to unsustainable levels until a catalyst (often a minor one) causes the herd to turn, leading to a panic sell-off.

Defensive Maneuvers: How to Protect Your Wealth During a Crash

For the individual investor, the goal isn’t necessarily to “time” the crash—which is nearly impossible—but to build a portfolio that can survive one. Protecting wealth requires a combination of structural strategy and emotional discipline.

The Importance of Diversification and Asset Allocation

The only “free lunch” in investing is diversification. By spreading capital across different asset classes—such as domestic stocks, international equities, bonds, real estate, and commodities—investors can ensure that a crash in one sector doesn’t wipe out their entire net worth.

For example, during the 2022 bear market, while growth stocks were plummeting, certain value sectors and energy stocks performed remarkably well. A well-allocated portfolio naturally hedges against localized crashes, providing a smoother ride through turbulent waters.

Psychological Fortitude and Long-Term Thinking

The biggest threat to an investor’s wealth during a crash is often their own reflection. Behavioral finance shows that humans are hardwired for “loss aversion”—the pain of losing $1,000 is twice as intense as the joy of gaining $1,000. This often leads investors to sell at the bottom of a crash out of fear, effectively locking in their losses.

Successful investing requires a shift in perspective: viewing a market crash not as a disaster, but as a temporary decline in the price of productive assets. Maintaining a long-term horizon (10–20 years) allows an investor to look past the “noise” of a crash and focus on the eventual recovery.

The Aftermath: Why Crashes Are Often the Greatest Wealth-Building Opportunities

While crashes cause short-term pain, they are historically the birthplaces of long-term wealth. For those with liquid capital and a high risk tolerance, a market crash is effectively a “clearance sale” on the world’s best companies.

Buying the Dip: Historical Returns Post-Crash

Historical data is overwhelmingly clear: the periods following a market crash are often the most lucrative for investors. Following the 2008 crisis, the S&P 500 embarked on the longest bull market in history. Following the 2020 flash crash, the market doubled in value in record time.

The strategy of “Dollar Cost Averaging” (DCA)—consistently investing the same amount of money regardless of market price—is particularly effective during a crash. By buying more shares when prices are low, investors lower their average cost basis, positioning themselves for outsized gains when the market inevitably recovers.

Rebalancing for Future Growth

A crash provides a unique opportunity to rebalance a portfolio. If your target allocation was 60% stocks and 40% bonds, a stock market crash might leave you with 40% stocks and 60% bonds. Rebalancing forces you to sell the “expensive” asset (bonds) and buy the “cheap” asset (stocks). This disciplined approach removes emotion from the equation and ensures that you are consistently adhering to a “buy low, sell high” philosophy.

In conclusion, while the “last” stock market crash may have been the grinding bear market of 2022 or the sharp shock of 2020, it certainly won’t be the last one we see. Market crashes are an inherent feature of capitalism, not a bug. By understanding their history, identifying their causes, and maintaining a disciplined investment strategy, you can transform these periods of fear into the foundation of your financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.