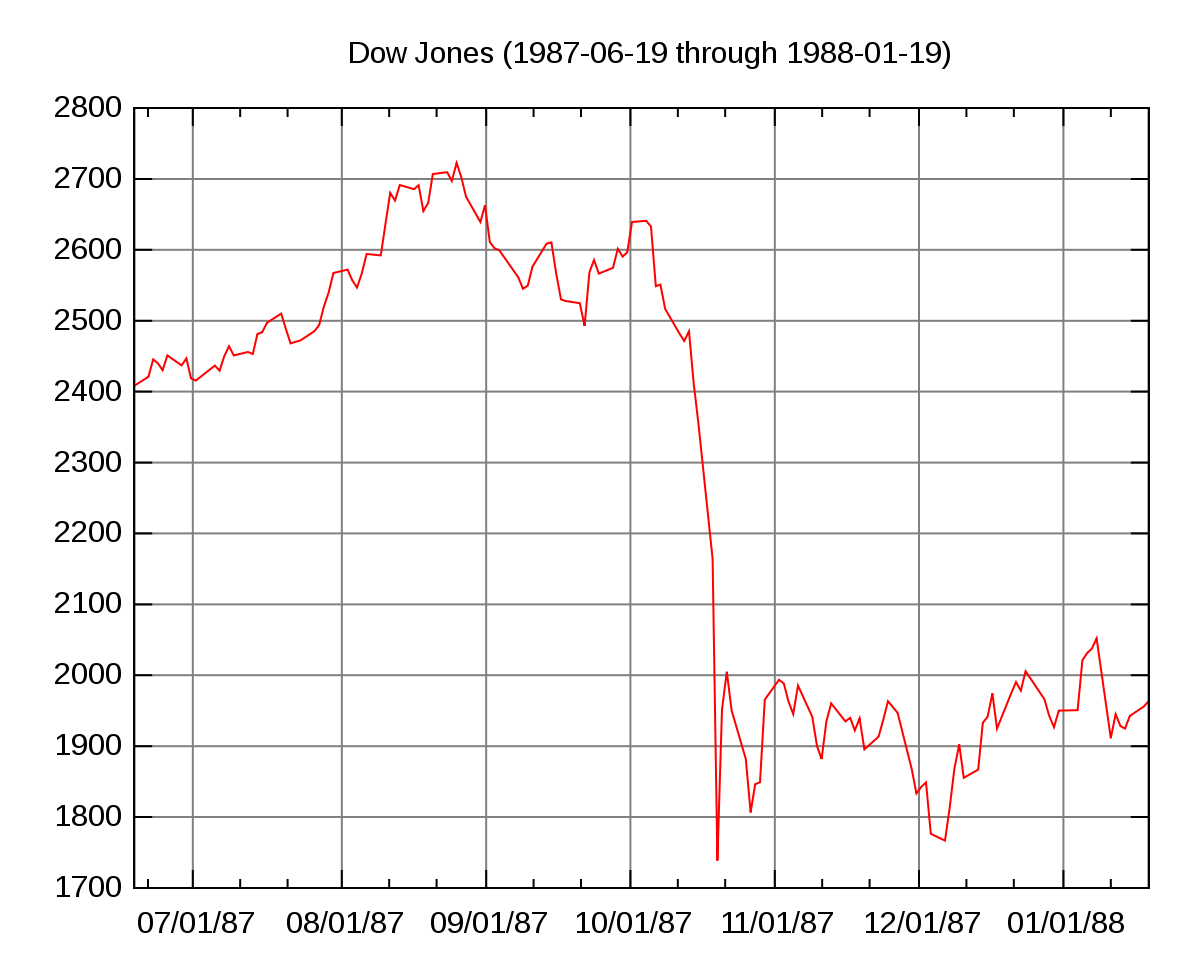

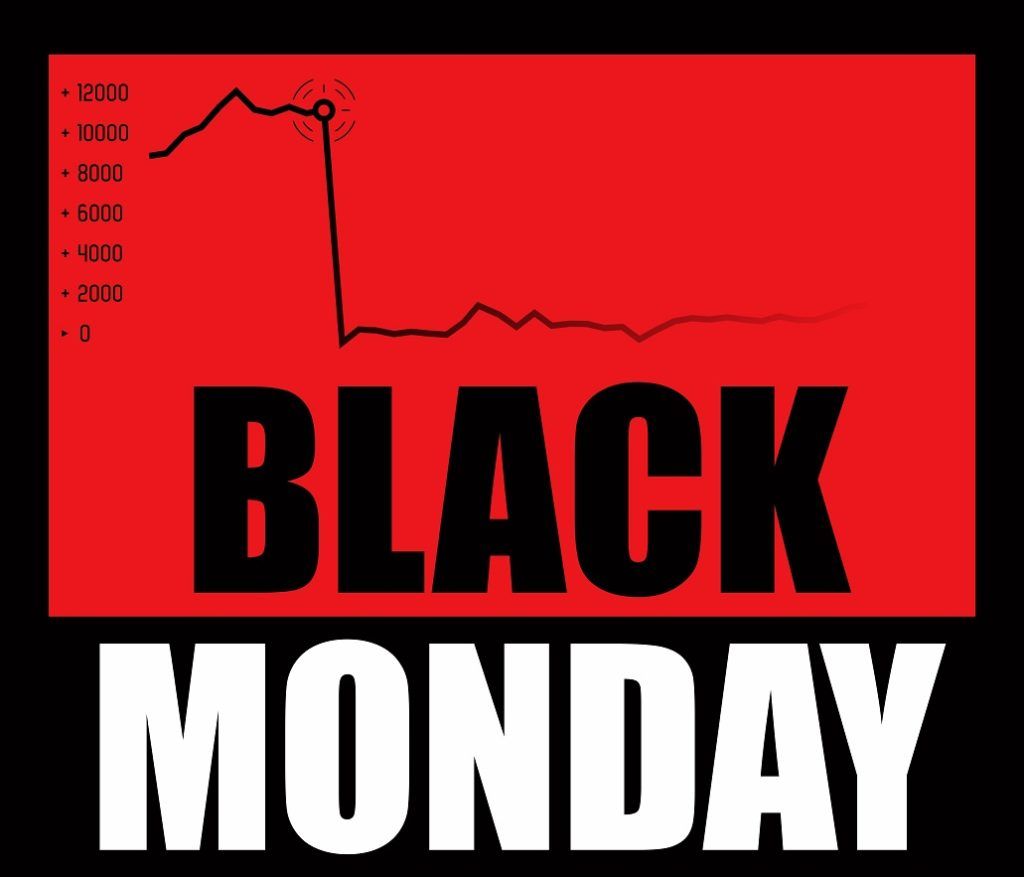

October 19, 1987, is a date etched into the annals of financial history as “Black Monday.” On this harrowing day, the Dow Jones Industrial Average (DJIA) plummeted by an unprecedented 508 points, representing a colossal 22.6% loss in a single trading session. This wasn’t merely a bad day for the market; it was a seismic event that sent shockwaves across global financial centers, triggering a cascade of fear and uncertainty that reverberated for months. For many, particularly those who lived through it, Black Monday serves as a stark reminder of the inherent volatility and psychological fragilities that underpin even the most sophisticated financial systems. Understanding the chronology, causes, and consequences of this pivotal event offers invaluable insights into market dynamics, regulatory evolution, and the enduring principles of investing.

A Day That Shook Global Markets: October 19, 1987

The events of Black Monday didn’t emerge from a vacuum; they were the culmination of several simmering tensions and novel market conditions that created a perfect storm for an unprecedented collapse.

The Precipice of Panic: Market Conditions Leading Up to Black Monday

In the months leading up to October 1987, the U.S. stock market had enjoyed an extended bull run, characterized by rapid gains and a sense of invincibility. From the beginning of 1987, the DJIA had surged by over 40%, reaching an all-time high in August. However, beneath the surface of this apparent prosperity, several red flags were emerging. Economists worried about a growing U.S. trade deficit and a weakening dollar, which threatened the nation’s economic stability. Inflation concerns were also rising, prompting the Federal Reserve to increase interest rates earlier in the year, a move typically seen as a brake on economic growth and, by extension, corporate profits.

Adding to this complex backdrop was the burgeoning role of “program trading,” particularly a strategy known as “portfolio insurance.” Developed to protect institutional investors from market downturns, portfolio insurance involved using computer models to automatically sell large blocks of stocks or stock index futures as the market declined. While conceptually sound in theory, its widespread adoption meant that a significant portion of market participants were poised to sell simultaneously if prices dropped, creating a systemic risk that was poorly understood at the time. As the week preceding Black Monday unfolded, a pattern of declining prices and increased volatility became apparent, with significant drops on October 14th and 16th, setting a nervous tone for the fateful Monday.

The Unfolding Collapse: What Happened on October 19th?

The trading day on October 19th began with a sense of unease that quickly escalated into full-blown panic. From the opening bell, selling pressure was intense and unrelenting. Major institutional investors, triggered by their portfolio insurance algorithms, initiated massive sell orders in an attempt to cut losses. This wave of selling overwhelmed market makers and specialists on the New York Stock Exchange (NYSE), who were traditionally responsible for maintaining orderly markets by buying when others were selling. They simply could not absorb the sheer volume of sell orders, leading to massive bid-ask spreads and rapidly plummeting prices.

As stock prices fell, more portfolio insurance programs were triggered, creating a vicious feedback loop. The continuous sell orders further depressed prices, which in turn triggered more selling. The lack of liquidity became a critical issue; there were simply not enough buyers to meet the avalanche of sellers. At one point, trading in some major stocks ground to a halt as specialists struggled to find any buyers. By the close of trading, the DJIA had fallen by 22.6%, a loss that dwarfed any single-day percentage drop in its history, including those during the Great Depression. The impact was not confined to New York; markets around the world, from London to Hong Kong and Tokyo, experienced similar, albeit slightly less severe, crashes as the news and fear propagated across global financial networks.

Dissecting the Causes: Beyond Simple Panic

While market psychology undoubtedly played a crucial role in amplifying the crash, Black Monday was not solely attributable to irrational panic. A complex interplay of technological advancements, underlying economic conditions, and behavioral biases converged to create the perfect storm.

The Role of Program Trading and Computerized Systems

Perhaps the most frequently cited technical cause of Black Monday was the widespread adoption of program trading, specifically “portfolio insurance.” This strategy involved large institutional investors, such as pension funds and mutual funds, using computer algorithms to automatically sell stock index futures or the underlying stocks themselves when the market began to decline. The intention was to hedge against losses in their portfolios. However, the sheer volume of capital tied to these strategies meant that when a market downturn began, a synchronized wave of sell orders hit the market simultaneously.

This created a perilous feedback loop: falling prices triggered more selling by portfolio insurers, which further exacerbated the decline, triggering even more selling. The technology, designed to mitigate risk, paradoxically amplified it by removing human discretion and creating an avalanche of automatic orders that overwhelmed market liquidity and traditional market-making mechanisms. Regulators and market participants were ill-prepared for the systemic effects of such large-scale, automated selling.

Economic Fundamentals and Geopolitical Tensions

Beneath the technical market mechanisms, several macroeconomic factors contributed to the market’s underlying fragility. The United States was grappling with significant “twin deficits” – a large budget deficit and a substantial trade deficit. These deficits were a source of concern for international investors, who began to question the long-term health of the U.S. economy. The U.S. dollar had been weakening for some time, which, while making U.S. exports cheaper, also signaled a lack of confidence in the currency.

Furthermore, rising inflation prompted the Federal Reserve to increase interest rates in the months leading up to October 1987. Higher interest rates typically make bonds more attractive relative to stocks and can signal a tightening of monetary policy that could slow economic growth. There was also a growing sense of global economic uncertainty, with simmering geopolitical tensions and concerns about protectionist trade policies adding to investor apprehension. These fundamental economic worries provided the fertile ground upon which a technical sell-off could quickly morph into a full-blown crash.

Market Psychology and Herd Behavior

While program trading provided the mechanism, and economic fundamentals provided the backdrop, human psychology was the accelerant that turned a sharp correction into a full-blown rout. Fear and panic are powerful forces in financial markets, often leading to irrational decision-making and herd behavior. As prices began to fall on Black Monday, investors, both institutional and individual, saw their portfolios rapidly eroding. The instinct to “get out” before things got worse became overwhelming.

The lack of clear information and the rapid pace of the decline fueled this panic. News reports amplified the sense of crisis, and the sight of major indices plummeting led many to believe that the market was in a freefall with no bottom in sight. This widespread fear led to a self-reinforcing cycle of selling, where each new seller contributed to the downward pressure, convincing others that selling was the only rational course of action. This powerful emotional contagion demonstrated how even sophisticated markets can be swayed by collective psychological forces, overriding fundamental valuations and creating a liquidity crisis as everyone rushes for the exits simultaneously.

The Aftermath and Lessons Learned

Black Monday was a profound wake-up call for regulators, policymakers, and investors worldwide. The immediate aftermath required swift and decisive action, leading to significant reforms that reshaped how markets operate and how crises are managed.

Immediate Responses and Policy Changes

The immediate response to Black Monday was critical in preventing a complete financial meltdown. The Federal Reserve, under the leadership of Chairman Alan Greenspan, played a pivotal role. On the morning of October 20th, the Fed issued a brief but powerful statement: “The Federal Reserve, in its capacity as the central bank of the United States, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.” This signal, backed by direct actions to inject liquidity into the banking system, reassured banks that they would have the necessary funds to meet their obligations and prevent a broader credit crunch. This decisive action helped to stabilize confidence and prevent a bank run or systemic collapse.

Additionally, the NYSE and other exchanges took steps to manage the market’s functionality. Trading was sometimes halted or delayed in certain stocks to allow specialists to process orders and prevent even greater disarray. The focus was on restoring order and ensuring that the financial plumbing continued to function.

Regulatory Reforms and Market Structure Evolution

In the wake of Black Monday, extensive investigations and studies were conducted to understand its causes and prevent a recurrence. A key outcome was the implementation of “circuit breakers.” These mechanisms automatically halt trading across exchanges for specified periods if stock market indices fall by a certain percentage (e.g., 7%, 13%, and 20%). The intention is to give investors a chance to pause, assess the situation, and absorb information, thereby curbing panic selling and providing market makers an opportunity to restore liquidity.

Regulators also focused on better coordinating between stock and futures markets, as the interaction between these two spheres was identified as a major amplifying factor. Rules regarding capital requirements for brokers and market makers were reviewed and strengthened to ensure they could withstand periods of extreme volatility. There was also a renewed emphasis on transparency and better data sharing among regulatory bodies. These reforms aimed to build greater resilience into the market structure and provide tools to manage extreme volatility more effectively.

Enduring Impacts on Investors and Financial Theory

Black Monday had a lasting impact on how investors perceive risk and how financial theory evolved. It underscored the importance of diversification and the potential for even sophisticated hedging strategies to fail under extreme conditions. For individual investors, it served as a brutal lesson in the dangers of emotional investing and the need for a long-term perspective.

From an academic standpoint, Black Monday spurred greater interest in behavioral finance, which seeks to understand how psychological biases influence financial decision-making. It highlighted that markets are not always perfectly rational and efficient, and that human emotions like fear and greed can create significant deviations from fundamental values. The crash also reinforced the critical role of central banks as lenders of last resort and demonstrated the profound interconnectedness of global financial markets, emphasizing the need for international cooperation during crises.

Could Another Black Monday Happen? Modern Market Safeguards and Vulnerabilities

The question of whether another Black Monday could occur is a perennial one for investors and policymakers. While significant safeguards have been put in place, new vulnerabilities have also emerged, creating a complex risk landscape.

Enhanced Protections: Circuit Breakers and Capital Requirements

The most direct response to Black Monday was the introduction of market-wide circuit breakers. These pre-determined thresholds for index declines are designed to cool down rapidly escalating sell-offs, providing a temporary halt to trading. This pause allows market participants to digest information, reassess valuations, and prevents the kind of automated, panic-driven spiral that characterized 1987. Furthermore, regulatory bodies like the SEC have significantly tightened capital requirements for brokerage firms and financial institutions, ensuring they have sufficient buffers to absorb losses during volatile periods and prevent cascading failures. Enhanced risk management practices are now standard across the industry, with stress tests and scenario analyses regularly conducted to assess financial institutions’ resilience to extreme market events.

New Risks: High-Frequency Trading and Algorithmic Vulnerabilities

While old risks have been mitigated, new ones have emerged, largely driven by technological advancements. The rise of high-frequency trading (HFT) and complex algorithmic trading strategies means that markets can move with astonishing speed. While HFT often adds liquidity, it also introduces the potential for “flash crashes,” where markets can drop dramatically in a matter of minutes due to faulty algorithms or a sudden withdrawal of liquidity, as seen in the 2010 Flash Crash. The interconnectedness of global markets through modern communication technologies also means that a crisis in one region can propagate globally far more rapidly than in 1987. The sheer volume and speed of automated trading mean that human oversight, while present, may struggle to keep pace with an emergent crisis.

The Human Element: Still the Ultimate Unknown

Despite all the technological advancements and regulatory safeguards, the human element remains the ultimate unknown. Investor psychology – fear, greed, and herd mentality – continues to be a powerful force in markets. While circuit breakers can provide a pause, they cannot fundamentally change human behavior. Major geopolitical events, pandemics, or unforeseen economic shocks can still trigger widespread panic and a flight to safety, irrespective of underlying market structures. The growing complexity and opaque nature of some financial instruments also pose challenges, making it difficult to fully assess systemic risks. Ultimately, while the precise conditions of Black Monday 1987 may not recur, the potential for significant market dislocations, driven by a combination of technological quirks and human reactions to perceived crises, remains an enduring feature of financial markets.

In conclusion, Black Monday was a watershed moment that forever changed the financial landscape. While the specific details of October 19, 1987, are rooted in a particular historical context, its lessons about market fragility, the interplay of technology and human behavior, and the critical role of robust regulation continue to resonate. For modern investors and financial professionals, understanding this pivotal event is not merely an exercise in history but a crucial foundation for navigating the inherent complexities and risks of today’s dynamic global markets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.