Navigating the complex landscape of tax deadlines can often feel like deciphering an intricate puzzle. For individuals and businesses alike, understanding when tax payments are due is not merely a matter of compliance; it’s a fundamental aspect of sound financial management and a critical step in avoiding costly penalties and interest charges. While “Tax Day” might conjure up images of a singular annual event, the reality is a multi-layered calendar of federal, state, and sometimes local obligations that span the entire year. This comprehensive guide aims to demystify these crucial deadlines, providing clarity on when and why various tax payments are expected, empowering you with the knowledge to maintain impeccable financial health and ensure timely compliance.

Understanding Key Tax Deadlines for Individuals

For most individual taxpayers, the tax year operates on a calendar basis, from January 1st to December 31st. However, the deadlines for reporting income and remitting payments extend into the following year, with several key dates that every taxpayer should mark on their calendar.

The All-Important April 15th (or Equivalent)

For the vast majority of individual filers in the United States, April 15th stands as the most prominent tax deadline. This is the date by which federal income tax returns (Form 1040, U.S. Individual Income Tax Return) must typically be filed, and any outstanding tax liability for the previous calendar year must be paid. If April 15th falls on a weekend or a holiday, the deadline is automatically pushed to the next business day. For instance, if April 15th is a Saturday, the deadline moves to Monday, April 17th. Similarly, if a holiday like Emancipation Day (observed in Washington D.C.) falls on April 15th, it can also shift the nationwide deadline.

Beyond federal taxes, many states also adhere to this April 15th deadline for their state income tax returns and payments. However, it’s crucial to remember that state rules can vary significantly, with some states having earlier or later deadlines. Residents of these states must be vigilant in checking their specific state’s tax department website for accurate information.

Navigating Quarterly Estimated Taxes

Not all income is subject to withholding by an employer. Individuals who are self-employed, own a business, receive significant investment income, or have other sources of income not subject to withholding (such as rents or alimony) are generally required to pay estimated taxes throughout the year. The IRS operates on a “pay-as-you-go” system, meaning taxpayers are expected to pay most of their tax liability during the year, rather than in one lump sum at the annual filing deadline.

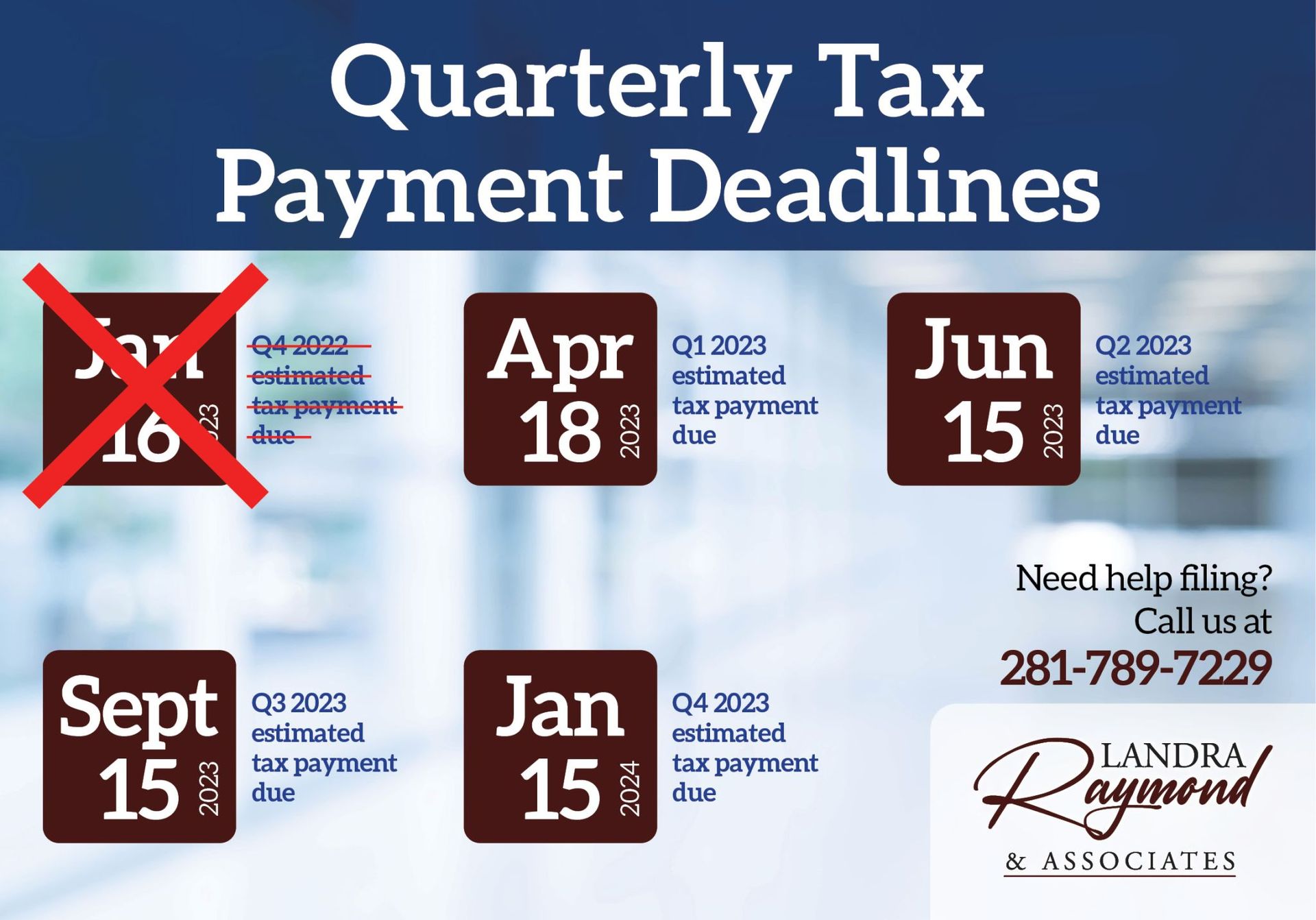

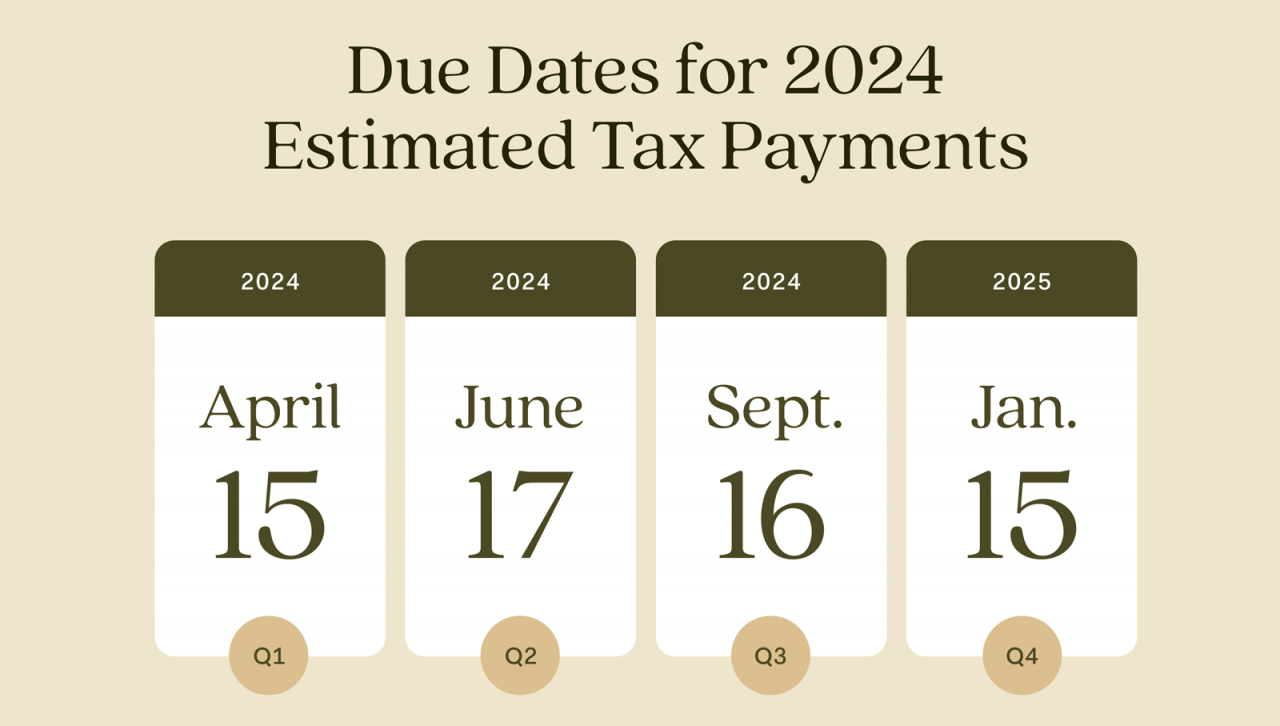

These estimated tax payments are typically due on a quarterly basis. The four key deadlines for estimated tax payments are:

- April 15th: For income earned between January 1st and March 31st.

- June 15th: For income earned between April 1st and May 31st.

- September 15th: For income earned between June 1st and August 31st.

- January 15th of the following year: For income earned between September 1st and December 31st.

Similar to the annual filing deadline, if any of these dates fall on a weekend or holiday, the deadline shifts to the next business day. Failure to pay enough estimated tax throughout the year, or missing these quarterly deadlines, can result in penalties, even if you ultimately receive a refund when you file your annual return. Taxpayers can use Form 1040-ES, Estimated Tax for Individuals, to calculate and make these payments.

State Income Tax Variations

While many states align with the federal April 15th deadline, it is a dangerous assumption to make without verification. Some states, like Virginia, often have a May 1st deadline, while others might have deadlines in other months. Additionally, states have their own rules regarding estimated tax payments, which may or may not mirror the federal schedule. For individuals living or working in multiple states, or those who have recently moved, understanding the unique tax calendar for each relevant state is paramount. Consulting state tax department websites or a tax professional familiar with multi-state taxation is highly recommended to avoid oversights.

Filing for an Extension: What You Need to Know

Life can be unpredictable, and sometimes, despite best intentions, taxpayers simply need more time to prepare their returns. The good news is that both the IRS and most states offer an automatic extension of time to file your income tax return. For federal taxes, filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return, by the April 15th deadline typically grants an automatic six-month extension, pushing the filing deadline to October 15th.

It is crucial to understand that an extension to file is not an extension to pay. If you anticipate owing taxes, you must still estimate and pay that liability by the original April 15th deadline to avoid potential penalties and interest charges. An extension simply provides more time to compile your documentation and complete your return; any taxes owed are still due by the original payment date.

Crucial Tax Timelines for Businesses and Employers

Businesses face an even broader array of tax obligations and corresponding deadlines, often dictated by their legal structure (sole proprietorship, partnership, S corporation, C corporation), industry, and the number of employees. Missing these deadlines can have significant financial and legal repercussions for the entity.

Corporate and Partnership Income Tax Deadlines

The income tax deadlines for businesses vary significantly based on their structure:

- Partnerships (Form 1065) and S Corporations (Form 1120-S): Generally, these entities have a tax filing and payment deadline of March 15th for calendar year filers. This is to allow partners and S corporation shareholders to receive their K-1 forms in time to file their individual returns by April 15th. If an extension is filed, the deadline is typically extended to September 15th.

- C Corporations (Form 1120): For calendar year filers, C corporations typically have a tax filing and payment deadline of April 15th. If an extension is filed, the deadline is usually extended to October 15th. Corporations with fiscal years (not ending December 31st) generally file on the 15th day of the fourth month after the end of their tax year.

Similar to individuals, businesses are also required to pay estimated taxes quarterly if they expect to owe tax of $500 or more. The deadlines are the same as for individuals: April 15, June 15, September 15, and January 15 of the following year.

The Intricacies of Payroll Tax

For any business with employees, payroll taxes represent a significant and recurring compliance obligation. These include federal income tax withholding, Social Security and Medicare taxes (FICA), and federal unemployment tax (FUTA). State-level payroll taxes, such as state unemployment insurance (SUI) and state disability insurance (SDI), also apply in many jurisdictions.

The payment schedule for payroll taxes (FICA and withheld income tax) can be complex, typically determined by the total tax liability accumulated. Businesses are generally required to deposit these taxes either monthly or semi-weekly.

- Monthly depositors: Generally deposit taxes by the 15th of the following month.

- Semi-weekly depositors: Deposit taxes on Wednesday for payments made on Friday, Saturday, and Sunday, and on Friday for payments made on Monday, Tuesday, Wednesday, and Thursday.

Beyond these frequent deposits, businesses must also file various payroll reports:

- Form 941 (Employer’s Quarterly Federal Tax Return): Due by the last day of the month following the end of each calendar quarter (April 30, July 31, October 31, January 31).

- Form 940 (Employer’s Annual Federal Unemployment (FUTA) Tax Return): Due by January 31st of the following year.

- W-2 Forms (Wage and Tax Statement): Issued to employees and filed with the Social Security Administration by January 31st.

- 1099 Forms (Various types, for independent contractors, etc.): Issued to recipients and filed with the IRS by January 31st (for non-employee compensation) or later for other types.

Sales Tax and Other Business-Specific Obligations

Businesses that sell goods or services may be required to collect and remit sales tax to their state and/or local governments. Sales tax deadlines vary widely by jurisdiction and can be monthly, quarterly, or annually, often depending on the volume of sales a business generates. It is critical for businesses to register with relevant state and local tax authorities and understand their specific filing and payment schedule.

Beyond sales tax, businesses might also face other specific taxes, such as excise taxes (on certain goods or services), property taxes (on real estate and sometimes business personal property), and industry-specific levies. Property tax deadlines are determined by local municipalities and can vary significantly from one county or city to another.

The Repercussions of Missed Deadlines

Ignoring tax deadlines is a perilous path that can lead to significant financial strain and legal complications. The IRS and state tax agencies are diligent in enforcing compliance, and they have various mechanisms to penalize those who fail to meet their obligations.

Penalties for Failure to File and Failure to Pay

There are two primary categories of penalties for non-compliance:

- Failure to File Penalty: This is typically 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid tax. If the return is more than 60 days late, the minimum penalty is $485 (for returns due in 2024) or 100% of the tax due, whichever is smaller.

- Failure to Pay Penalty: This penalty is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25% of your unpaid tax.

It’s important to note that the failure to file penalty is generally ten times higher than the failure to pay penalty. This highlights the IRS’s emphasis on at least filing a return, even if you cannot pay the full amount due.

Accruing Interest on Underpayments

In addition to penalties, the IRS charges interest on underpayments and unpaid tax balances. The interest rate is determined quarterly and can fluctuate. It is typically the federal short-term rate plus 3 percentage points. Interest is compounded daily and applies from the original due date of the tax until the date it is paid in full. This interest applies not only to unpaid taxes but also to any penalties assessed, further increasing the financial burden.

Mitigating Risks: What to Do If You Can’t Pay

If you find yourself unable to pay your tax liability by the deadline, it is crucial to take proactive steps rather than avoiding the situation.

- File Your Return (or Extension) on Time: Always file your tax return or an extension by the due date. This avoids the much higher failure-to-file penalty.

- Pay What You Can: Even if you can’t pay the full amount, pay as much as you can to minimize penalties and interest.

- Contact the IRS (or State Tax Agency): The IRS offers various payment options for taxpayers facing financial hardship, including:

- Short-Term Payment Plan: Up to 180 days to pay, though interest and penalties still apply.

- Offer in Compromise (OIC): Allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This is typically for taxpayers in extreme financial distress.

- Installment Agreement: Allows taxpayers to make monthly payments for up to 72 months. While interest and penalties still apply, they may be reduced.

Timely communication and a willingness to cooperate with tax authorities are key to finding a workable solution and minimizing the financial impact of unpaid taxes.

Proactive Strategies for Seamless Tax Compliance

Successful tax compliance isn’t about scrambling in the weeks leading up to April 15th; it’s about year-round diligence and strategic planning. Adopting proactive habits and leveraging available resources can transform tax season from a stressful ordeal into a manageable process.

The Power of Diligent Record-Keeping

Accurate and organized record-keeping is the cornerstone of effective tax planning. This includes maintaining meticulous records of all income, expenses, deductions, credits, and investments.

- Digital Records: Utilize cloud storage, digital scanning, and financial software to keep electronic copies of all receipts, invoices, bank statements, and tax forms.

- Categorization: Categorize expenses throughout the year to simplify the process of identifying deductible items.

- Separation: For businesses, always keep personal and business finances strictly separate to avoid confusion and simplify accounting.

Good records not only make tax preparation easier but are also invaluable in the event of an audit, providing verifiable proof for all reported figures.

Leveraging Technology: Financial Software and Tools

The digital age offers a plethora of financial tools designed to simplify tax management.

- Accounting Software: Programs like QuickBooks, Xero, or FreshBooks can automate expense tracking, generate financial reports, and often integrate directly with tax preparation software.

- Tax Preparation Software: TurboTax, H&R Block, and TaxAct offer user-friendly interfaces to guide individuals and small businesses through the tax filing process, calculate liabilities, and even e-file returns.

- Spreadsheets and Cloud Tools: Simple spreadsheets or cloud-based platforms like Google Sheets can be effective for basic income and expense tracking for those with less complex financial situations.

- Reminder Apps: Set up automated reminders for all key tax deadlines to ensure nothing is missed.

These tools can significantly reduce the time and effort required for tax compliance, minimize errors, and provide real-time insights into your financial position.

The Value of Professional Guidance

While self-preparation is feasible for many, the complexity of tax law, especially for businesses, high-net-worth individuals, or those with unique financial circumstances, often warrants professional assistance.

- Tax Preparers and Accountants: Certified Public Accountants (CPAs) and Enrolled Agents (EAs) are experts in tax law and can provide invaluable advice, prepare accurate returns, identify eligible deductions and credits, and represent clients during audits.

- Tax Planning: Beyond mere preparation, professionals can help with proactive tax planning strategies throughout the year to optimize your financial situation and reduce future tax liabilities.

- Staying Current: Tax laws are constantly changing. Professionals stay up-to-date on the latest regulations, ensuring your compliance aligns with current requirements.

Investing in professional guidance can often save more in taxes and penalties than the cost of the service itself.

Budgeting and Saving for Tax Liabilities

A common pitfall is failing to set aside funds specifically for tax payments, leading to a scramble when deadlines loom.

- Automated Savings: Set up automated transfers from your primary checking account to a dedicated savings account for taxes.

- Percentage-Based Savings: For self-employed individuals or business owners, regularly set aside a percentage of your income (e.g., 25-35%) specifically for estimated tax payments.

- Review Throughout the Year: Periodically review your income and expenses to adjust your tax savings as needed, especially if your income changes significantly.

Treating tax payments as a regular expense, rather than a surprise annual bill, is a hallmark of strong personal and business financial management.

Special Circumstances and Further Considerations

While the general rules apply to most, certain situations can alter tax deadlines or create unique considerations.

Weekends, Holidays, and Emancipation Day

As mentioned, if a tax deadline falls on a weekend or a legal holiday, the deadline is automatically pushed to the next business day. This applies nationwide for federal deadlines. For state deadlines, it typically applies if the state observes that specific holiday. Emancipation Day, observed in Washington D.C. on April 16th, can uniquely impact the federal April 15th deadline by pushing it to April 18th if April 15th is a Friday or Saturday. Always confirm the exact date for a given tax year.

Disaster Relief and Other Exemptions

In the event of federally declared disasters, the IRS often grants extensions for various tax deadlines for affected individuals and businesses. These extensions are typically announced publicly and can provide much-needed relief during challenging times. Furthermore, military personnel serving in combat zones or certain contingency operations may also qualify for extensions to file and pay their taxes. It’s important to stay informed through official IRS announcements if you fall into one of these categories.

Tax Planning Beyond Deadlines

Understanding “when” taxes are due is fundamental, but true financial acumen extends to strategic tax planning. This involves looking beyond just meeting deadlines to actively seeking ways to reduce your taxable income, maximize deductions and credits, and structure your finances in a tax-efficient manner. This could involve contributing to retirement accounts, utilizing health savings accounts (HSAs), strategizing capital gains and losses, or exploring various business tax incentives. Tax planning is an ongoing process that, when done effectively, can significantly impact your financial well-being.

In conclusion, managing tax payment due dates requires vigilance, organization, and a proactive approach. By understanding the specific deadlines for individuals and businesses, the potential penalties for non-compliance, and the strategies available for seamless adherence, taxpayers can navigate their obligations with confidence. Whether you’re an individual making quarterly payments or a business managing complex payroll and sales tax schedules, staying informed and prepared is the ultimate key to financial peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.