Navigating the complexities of tax season can often feel like deciphering a secret code. For many, the perennial question, “When exactly do I need to file my taxes?” looms large, bringing with it a mix of anxiety and a desire for clarity. Understanding the deadlines for filing your taxes is not just a matter of compliance; it’s a critical component of sound personal finance, preventing unnecessary penalties, facilitating timely refunds, and ensuring financial peace of mind.

This comprehensive guide aims to demystify tax filing deadlines, offering insights into the standard schedules, specific scenarios that might alter your obligations, and the crucial steps you can take to manage your tax responsibilities effectively. Whether you’re an employee, self-employed, or facing unique circumstances, knowing your tax calendar is the first step towards a stress-free tax season.

Understanding the Annual Tax Calendar

The tax system, at its core, operates on a predictable annual cycle. However, various factors can introduce nuances that necessitate careful attention.

The Standard Tax Filing Deadline

For the vast majority of individual taxpayers in the United States, the federal income tax return (Form 1040) is due annually on April 15th. This date marks the culmination of the previous year’s financial activities and the deadline for reporting your income, deductions, and calculating your tax liability or refund.

- Weekends and Holidays: It’s important to note that if April 15th falls on a weekend or a holiday recognized by the District of Columbia, the deadline automatically shifts to the next business day. For example, if April 15th is a Saturday, the deadline moves to the following Monday, April 17th. Similarly, if it’s a Friday and a holiday falls on Monday, the deadline might move to Tuesday.

- Payments Due: This April 15th deadline (or the adjusted date) is not just for filing your return; it’s also the deadline for paying any taxes you owe for the previous tax year. Failing to pay by this date can incur penalties, even if you file on time.

Special Considerations for State Taxes

While the federal deadline provides a primary benchmark, it’s crucial to remember that most states also impose their own income tax filing deadlines, which can sometimes differ from the federal schedule.

- Varying State Deadlines: Many states align their individual income tax deadlines with the federal April 15th date. However, some states, like Virginia, have later deadlines (e.g., May 1st), while others might have slightly earlier ones. It’s imperative to consult your specific state’s department of revenue or taxation website to confirm their exact filing and payment deadlines.

- No State Income Tax: A handful of states, such as Florida, Texas, and Washington, do not impose a state income tax on wages, meaning residents in these states only need to concern themselves with federal filing requirements.

Quarterly Estimated Tax Deadlines

For individuals who earn income not subject to withholding – such as self-employed individuals, independent contractors, gig economy workers, or those with significant investment income – the IRS requires estimated taxes to be paid throughout the year in quarterly installments. These payments ensure taxpayers are meeting their tax obligations as income is earned, rather than facing a large, unexpected bill at year-end.

The deadlines for these quarterly payments are typically:

- Q1 (January 1 to March 31): April 15th

- Q2 (April 1 to May 31): June 15th

- Q3 (June 1 to August 31): September 15th

- Q4 (September 1 to December 31): January 15th of the following year

Again, if any of these dates fall on a weekend or holiday, the deadline shifts to the next business day. Missing these deadlines can result in underpayment penalties.

Key Factors That Influence Your Filing Deadline

While April 15th serves as the standard, several specific situations can alter your personal tax filing timeline. Understanding these exceptions is crucial for accurate compliance.

Requesting a Tax Extension

If you find yourself unable to complete your tax return by the April 15th deadline, you can request an extension. Filing Form 4868, “Application for Automatic Extension of Time To File U.S. Individual Income Tax Return,” grants you an automatic six-month extension to file, typically moving your deadline to October 15th.

- Time to File, Not Time to Pay: It’s critical to understand that an extension only grants you more time to file your return, not more time to pay any taxes you owe. If you anticipate owing taxes, you must estimate your liability and pay it by the original April 15th deadline to avoid penalties and interest. Failure to pay on time, even with an extension to file, can still result in late payment penalties.

- How to File: You can file Form 4868 electronically through tax software, via a tax professional, or by mail. Many tax software programs allow you to file an extension with just a few clicks.

Military Service Members and Overseas Filers

Members of the U.S. Armed Forces serving in combat zones or contingency operations generally receive an automatic extension to file and pay their taxes. This extension typically lasts for 180 days after they leave the combat zone, plus the number of days they had remaining in the original filing period when they entered the combat zone.

Similarly, U.S. citizens and resident aliens who live and work outside the United States and Puerto Rico have an automatic two-month extension to file their federal income tax return, moving their deadline to June 15th. If they need more time beyond June 15th, they can file Form 4868 to request an additional four-month extension, pushing their deadline to October 15th. They must attach a statement to their return explaining their eligibility for the June 15th extension.

Disaster Victims

The IRS often grants filing and payment relief to taxpayers affected by federally declared disasters. This relief typically extends deadlines for various tax acts, including filing returns and making payments. The specific extension period and eligibility criteria vary based on the disaster and the affected geographic areas. Taxpayers in designated disaster zones should check the IRS website or local news for updates on extended deadlines.

Deceased Taxpayers

When an individual passes away, their final tax return must still be filed. The deadline for filing the final income tax return of a deceased taxpayer is generally the same as the standard April 15th deadline. The personal representative (executor) of the estate is responsible for filing this return. If an extension is needed, Form 4868 can be filed.

Why Timely Filing and Payment Matter

Adhering to tax deadlines is more than just good practice; it’s essential for avoiding financial repercussions and maintaining a healthy financial standing.

Penalties for Late Filing

The IRS takes late filing seriously. If you fail to file your tax return by the deadline (including extensions), you could face a failure-to-file penalty. This penalty is generally 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid taxes. If your return is more than 60 days late, the minimum penalty is either $485 (for returns due in 2024) or 100% of the tax due, whichever is smaller.

Penalties for Late Payment

Even if you file your return on time, failing to pay any taxes owed by the April 15th deadline (or the extended payment deadline for specific circumstances) can trigger a failure-to-pay penalty. This penalty is typically 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25% of your unpaid taxes. Additionally, the IRS charges interest on underpayments, which can compound over time. The interest rate is determined quarterly and can add up significantly.

It’s important to note that the failure-to-file penalty is significantly higher than the failure-to-pay penalty. This means that if you can’t pay your taxes, you should still file your return on time and then explore payment options with the IRS.

Benefits of Early or Timely Filing

- Peace of Mind: Eliminates the stress and anxiety associated with a looming deadline.

- Quicker Refunds: If you’re due a refund, filing early means you’ll receive your money sooner, which can be put to good use in your financial planning.

- Reduced Risk of Identity Theft: Filing early can help prevent tax-related identity theft, where fraudsters use your information to file a fake return and claim your refund.

- Time to Address Issues: Filing early provides more time to address any discrepancies or questions that may arise, whether from your own review or from tax software.

Navigating Your Tax Filing Process

Once you understand when to file, the next step is efficiently managing how to file. Proactive steps can make the process smoother and less daunting.

Gathering Your Documents

Effective tax filing begins with meticulous record-keeping. Throughout the year, and especially as tax season approaches, you should systematically gather all necessary financial documents. These typically include:

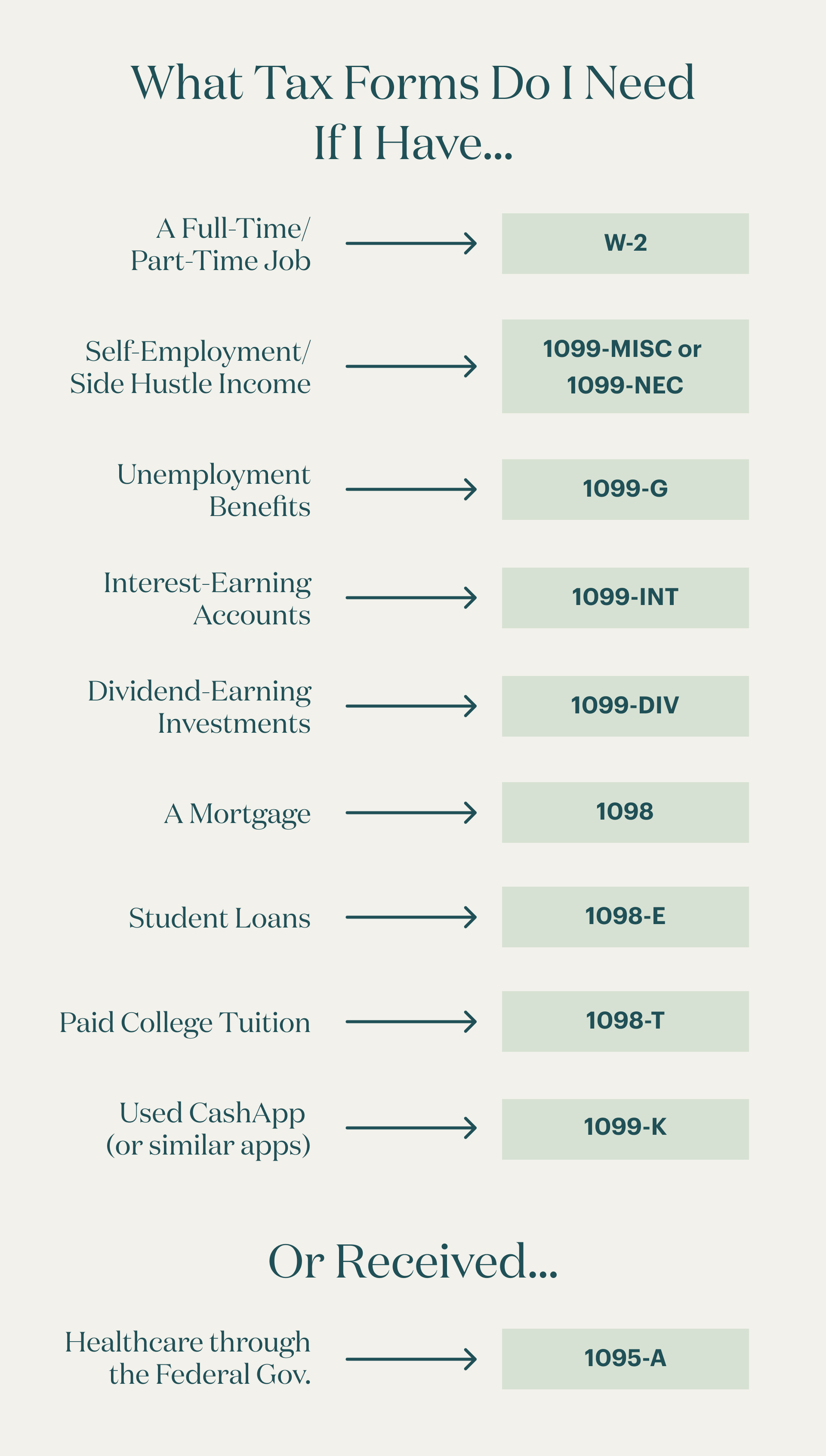

- Income Statements: W-2 forms (from employers), 1099 forms (1099-NEC for non-employee compensation, 1099-MISC for miscellaneous income, 1099-INT for interest, 1099-DIV for dividends, 1099-B for stock sales).

- Deduction and Credit Documentation: Mortgage interest statements (Form 1098), student loan interest (Form 1098-E), tuition statements (Form 1098-T), records of charitable contributions, medical expenses, property tax payments, and any business expenses if you’re self-employed.

- Other Forms: K-1 statements (from partnerships, S corporations, or trusts), IRA or 401(k) contribution records.

Organizing these documents well in advance prevents last-minute scrambling and reduces the chance of errors.

Choosing Your Filing Method

Taxpayers have several options for preparing and filing their returns:

- Tax Software: Popular online tax preparation software like TurboTax, H&R Block, and FreeTaxUSA offer user-friendly interfaces to guide you through the process. Many provide free filing options for simple returns or for those below certain income thresholds.

- Professional Tax Preparer: For complex financial situations, self-employment income, or simply for peace of mind, hiring a Certified Public Accountant (CPA) or Enrolled Agent (EA) can be invaluable. They can offer expert advice, ensure accuracy, and help identify potential deductions or credits you might overlook.

- IRS Free File: For taxpayers with adjusted gross income (AGI) below a certain limit (which changes annually), the IRS offers Free File. This program partners with various tax software companies to provide free online tax preparation and e-filing.

What to Do If You Can’t Pay

If you’ve filed your taxes on time but realize you can’t afford to pay the full amount you owe, don’t panic or ignore the problem. The IRS offers several payment relief options:

- Short-Term Payment Plan: You might be granted up to 180 days to pay your tax liability in full, although interest and penalties still apply.

- Installment Agreement: This allows you to make monthly payments for up to 72 months. You must submit Form 9465, “Installment Agreement Request.” Interest and late payment penalties still apply, but the failure-to-pay penalty rate is reduced.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This option is generally available when taxpayers are experiencing significant financial difficulty. The IRS considers your ability to pay, income, expenses, and asset equity when evaluating an OIC.

- File On Time: Remember, even if you can’t pay, always file your return on time or file for an extension. This minimizes the more severe failure-to-file penalty.

Proactive Tax Planning for Future Deadlines

Managing your tax obligations effectively extends beyond merely meeting deadlines; it involves year-round strategic planning.

Year-Round Record Keeping

The best defense against tax season stress is a good offense in the form of diligent record-keeping throughout the year.

- Digital vs. Physical: Decide on a system – whether it’s a dedicated folder for physical receipts, a digital scanning solution, or cloud storage for electronic documents – and stick to it.

- Categorization: Categorize your income, expenses, and investment activities. This not only aids tax preparation but also provides a clearer picture of your financial health.

- Review Regularly: Periodically review your financial statements and records to catch any discrepancies or missing information early on.

Adjusting Withholdings and Estimated Payments

A common reason for owing a large sum at tax time, or for receiving a surprisingly small refund, is incorrect tax withholding or insufficient estimated payments.

- W-4 Review: If you’re an employee, review your Form W-4 annually or whenever you experience a major life event (marriage, birth of a child, new job) to ensure your employer is withholding the correct amount of federal income tax from your paychecks. The IRS Tax Withholding Estimator tool can help you determine the right amount.

- Estimated Tax Review: If you’re self-employed or have significant non-wage income, regularly review your income and expenses to adjust your quarterly estimated tax payments. This helps you avoid underpayment penalties and prevents a large tax bill at year-end.

Seeking Professional Guidance

While self-preparation tools are excellent for many, knowing when to consult a tax professional is a hallmark of wise financial management.

- Complex Situations: If you’ve had major life changes, started a business, bought or sold property, or have investment income, a CPA or EA can provide expert advice.

- Tax Planning: Beyond just filing, tax professionals can help you plan strategically throughout the year to minimize your tax liability legally and maximize deductions and credits.

- Audit Support: In the unlikely event of an audit, a tax professional can represent you and provide invaluable support.

Conclusion

Understanding “when do I need to file my taxes” is a fundamental pillar of responsible financial stewardship. The standard April 15th deadline serves as the primary benchmark, but taxpayers must be aware of various exceptions, extensions, and state-specific requirements. Proactive planning, meticulous record-keeping, and a clear understanding of the consequences of late filing or payment are essential for a smooth tax season. By staying informed and utilizing available resources, you can navigate your tax obligations with confidence, ensuring compliance and fostering your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.