For many students and families, the choice between a public and a private college is one of the most significant financial decisions they will ever make. Beyond the academic programs and campus culture, the fundamental distinction between these institutions lies in their financial structures, revenue streams, and the ultimate return on investment (ROI) they provide. In the modern economic landscape, where student debt has surpassed $1.7 trillion in the United States alone, understanding the fiscal machinery behind these institutions is essential for making an informed capital allocation toward one’s future.

This analysis explores the financial nuances of public and private colleges through the lens of institutional finance, tuition modeling, and long-term economic outcomes.

The Funding Gap: How Institutional Revenue Impacts Your Wallet

The primary difference between public and private institutions is their source of funding. This “back-end” financial structure dictates the “front-end” price tag for students. While both types of institutions provide education, they operate on vastly different fiscal philosophies.

State Appropriations vs. Private Endowments

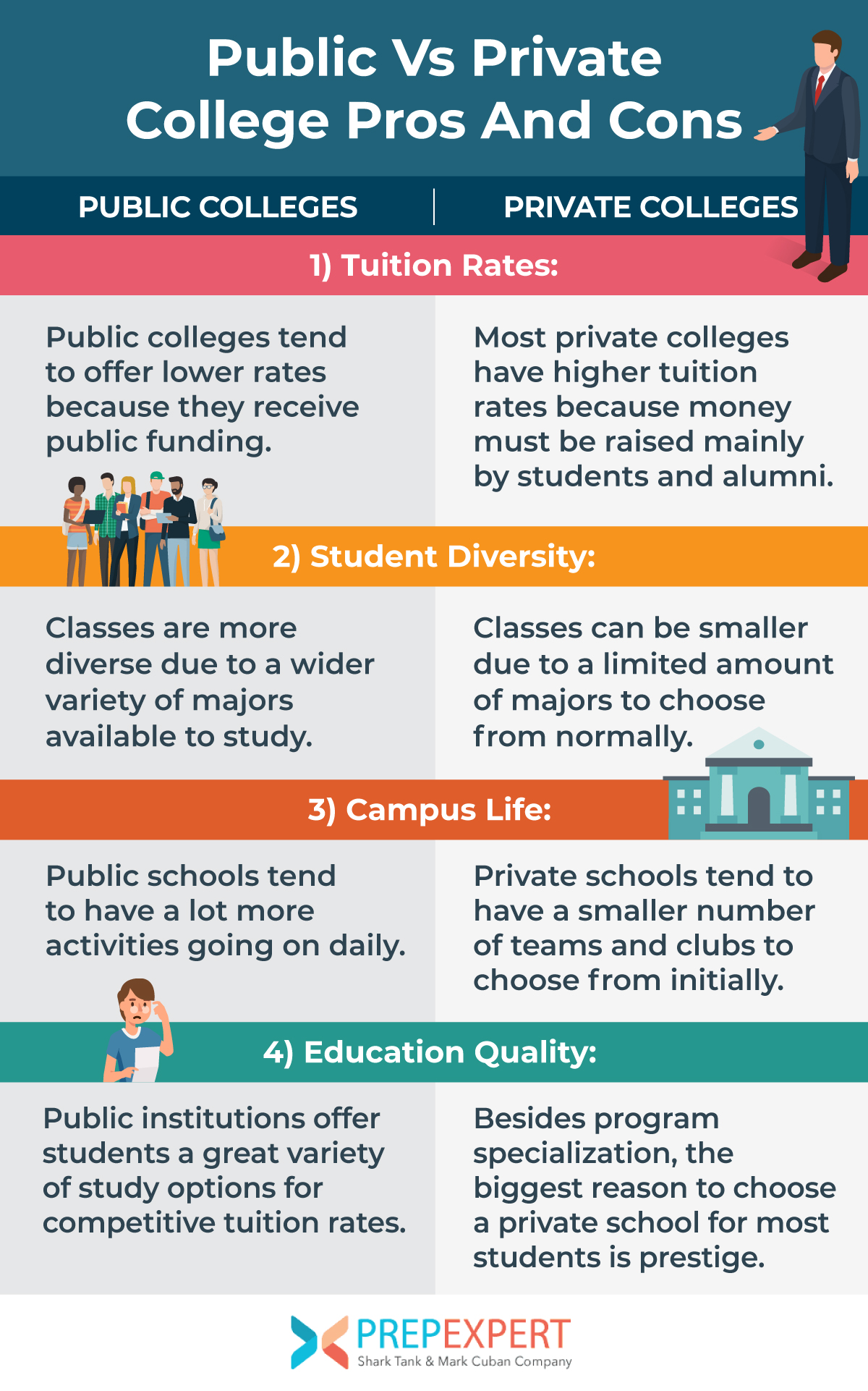

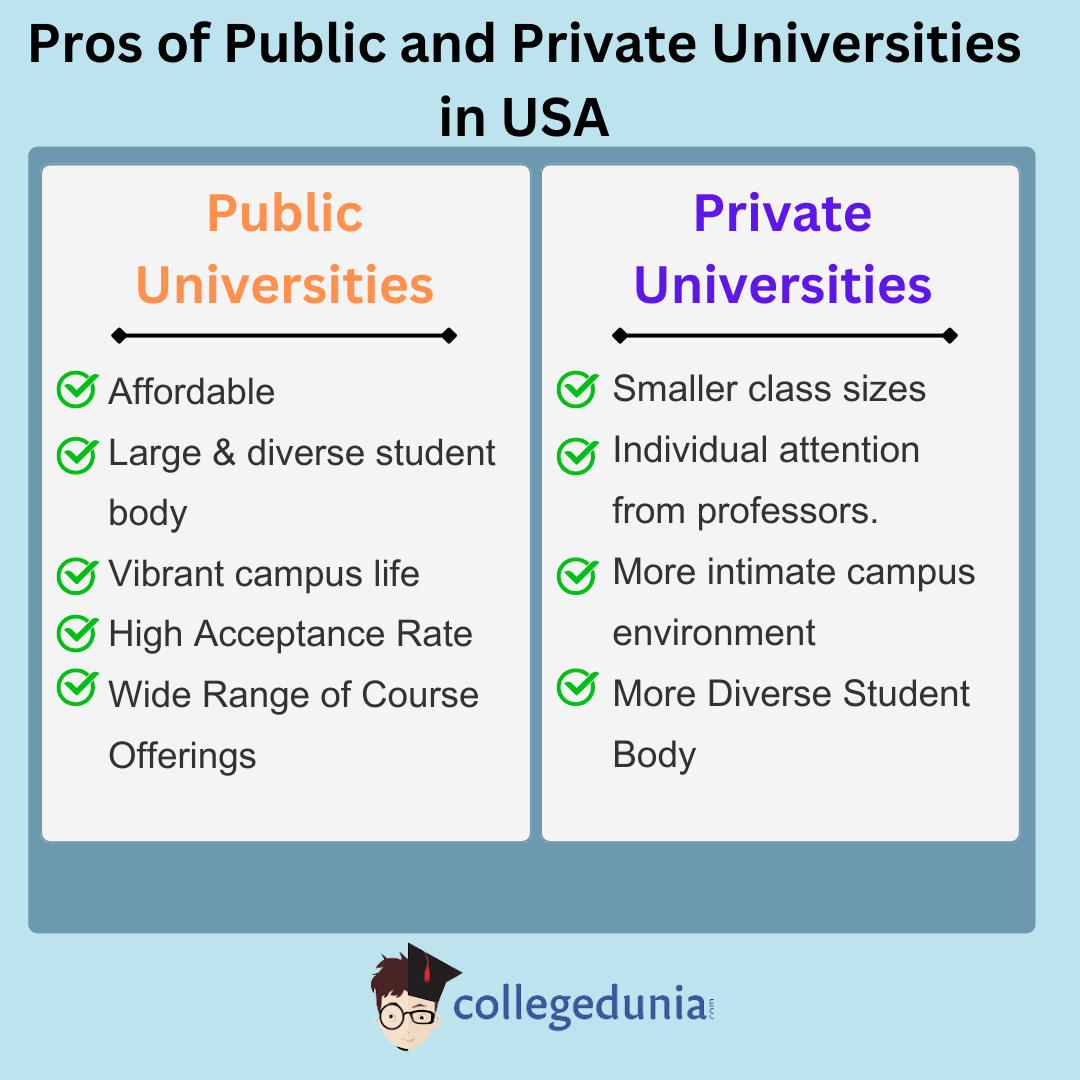

Public universities are largely funded by state governments. These institutions were established with a mission to provide affordable education to the residents of a specific state. Consequently, a significant portion of their operating budget comes from taxpayer dollars. This state subsidy allows public colleges to offer lower tuition rates to “in-state” residents.

In contrast, private colleges receive little to no direct funding from state governments. Their revenue is generated through tuition, private donations, and investment income from their endowments. An endowment is essentially an institutional investment portfolio. Large, prestigious private universities often have endowments valued in the billions, which they use to fund research, faculty salaries, and financial aid packages. The reliance on these private funds gives these institutions more fiscal autonomy but necessitates a higher base tuition to cover operating costs.

Taxpayer-Funded Education and the Tuition Subsidy

When an in-state student attends a public university, the state government is effectively subsidizing their education. This is a form of social investment intended to build a skilled local workforce. However, this model is sensitive to political and economic shifts. During state budget crises, appropriations for higher education are often the first to be cut, leading to “tuition creep”—where the financial burden is shifted from the state to the student.

Private institutions do not face this specific risk, but they are highly sensitive to market fluctuations that affect their endowment performance. For the student, the “money” aspect of this difference is simple: at a public school, the government helps pay the bill; at a private school, you—or the school’s wealthy donors—pay the bill.

Cost Comparison: Breaking Down Tuition, Fees, and Financial Aid

On paper, the price difference between public and private colleges is staggering. However, the “sticker price” is rarely what the savvy consumer actually pays. To understand the true financial impact, one must look at the net price.

Sticker Price vs. Net Price: The Private School Paradox

The “sticker price” is the advertised cost of tuition and fees. For a prestigious private university, this can exceed $80,000 per year, while a public university might advertise $10,000 to $25,000 for in-state residents. This leads many to assume that public schools are always the more affordable option.

However, private colleges often engage in a practice known as “tuition discounting.” Because they have access to large endowments and private scholarship funds, they can offer significant institutional aid. It is not uncommon for a private college with an $80,000 sticker price to provide a $50,000 “merit scholarship” or “need-based grant,” bringing the net price down to $30,000. In some cases, for low-to-middle-income families, the net price of a private college can actually be lower than that of a state school.

Institutional Aid and the FAFSA Advantage

The financial toolset for managing college costs starts with the Free Application for Federal Student Aid (FAFSA). While both public and private schools use the FAFSA to determine federal aid eligibility (Pell Grants, work-study, and federal loans), private schools often require an additional form called the CSS Profile.

The CSS Profile allows private institutions to take a deeper dive into a family’s financial health, looking at home equity and non-custodial parent income. This complexity is designed to help the school distribute its private institutional wealth more strategically. From a financial planning perspective, students should never rule out a private institution based on the sticker price alone until they receive their “Financial Aid Award Letter,” which details the actual out-of-pocket costs.

Return on Investment (ROI): Is the Private Prestige Worth the Premium?

When viewed as an investment, the value of a degree is measured by the career opportunities and earning potential it generates relative to the cost of acquisition. This is where the debate between public and private colleges becomes a matter of long-term wealth management.

Long-term Earning Potential and Career Outcomes

Data suggests that for many “general” degrees, the ROI of a public university is superior because the initial cost is so much lower. A nurse or an accountant graduating from a state school often earns the same starting salary as one graduating from a private school, but carries significantly less debt.

However, the calculation changes when discussing “elite” private institutions. These schools offer more than just a curriculum; they offer access to high-value networks and “brand equity.” In fields like investment banking, management consulting, and high-level tech, a degree from a top-tier private university (like Harvard, Stanford, or MIT) can lead to significantly higher starting bonuses and faster career progression. In these specific cases, the “premium” paid for the private education acts as a capital investment in a network that pays dividends over a 40-year career.

Debt-to-Income Ratios and Student Loan Management

A critical financial metric for any graduate is the debt-to-income ratio. Financial advisors generally recommend that a student’s total loan balance should not exceed their expected first-year salary.

Public universities often make this ratio easier to maintain. Because the principal balance of the loans is lower, the interest capitalization is less aggressive, allowing for a faster path to net-worth growth after graduation. Conversely, students at private colleges must be more clinical in their approach. Taking on $200,000 in debt for a career in a field with a $50,000 average salary is a high-risk financial move, regardless of the institution’s prestige.

Strategic Financial Planning for Prospective Students

Navigating the choice between public and private education requires a sophisticated approach to personal finance. It is about maximizing “found money” and utilizing tax-advantaged tools to mitigate the total cost of ownership.

Leveraging Scholarships and Grants

To minimize the financial burden, students should categorize aid into “gift aid” (grants and scholarships) and “self-help aid” (loans and work-study).

- Public Strategy: Focus on state-sponsored grants and local scholarships. Since the tuition is already subsidized, a few small external scholarships can often cover the entire remaining balance.

- Private Strategy: Focus on institutional merit aid. Many mid-tier private colleges use aggressive discounting to attract high-achieving students. This is a “market-clearing” strategy where the school trades a tuition discount for an increase in their academic rankings.

The Role of 529 Plans in College Selection

The 529 College Savings Plan is one of the most powerful financial tools for managing education costs. These plans allow for tax-free growth and tax-free withdrawals for qualified education expenses.

When choosing between a public and private school, the balance in a 529 plan dictates the “leverage” a family has. If a student has a well-funded 529, they may be able to afford the higher net price of a private school without resorting to high-interest private student loans. For families with smaller savings, the public route remains the most fiscally responsible path to ensure that the student—and the parents—do not compromise their long-term retirement goals.

Final Thoughts: The Fiscal Bottom Line

Ultimately, the difference between public and private colleges is a matter of institutional economics. Public colleges offer a “socially subsidized” model that prioritizes broad access and lower upfront costs. Private colleges offer a “market-driven” model that relies on high sticker prices balanced by high-value institutional aid and networking potential.

From a money perspective, neither is objectively “better.” The best choice is the one that aligns with your career goals while maintaining a manageable debt-to-income ratio. By looking past the campus amenities and focusing on net price, endowment health, and ROI, students can treat their college education as the significant financial asset it truly is.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.