In the world of personal finance and corporate strategy, we often use biological metaphors to describe the health of our portfolios or companies. We talk about “bleeding cash,” “organic growth,” or “market paralysis.” However, one of the most apt comparisons for financial distress is the distinction between a headache and a migraine. While both represent pain and dysfunction, they differ significantly in their intensity, duration, and the level of intervention required to resolve them.

For the modern investor or business owner, distinguishing between a financial “headache”—a minor, transient nuisance—and a financial “migraine”—a debilitating, systemic threat—is the difference between a quick recovery and a total collapse. This article explores how to diagnose these fiscal ailments, the underlying causes of financial pain, and the strategic protocols necessary to maintain long-term economic health.

The Anatomy of Financial Pain: Defining the Scope

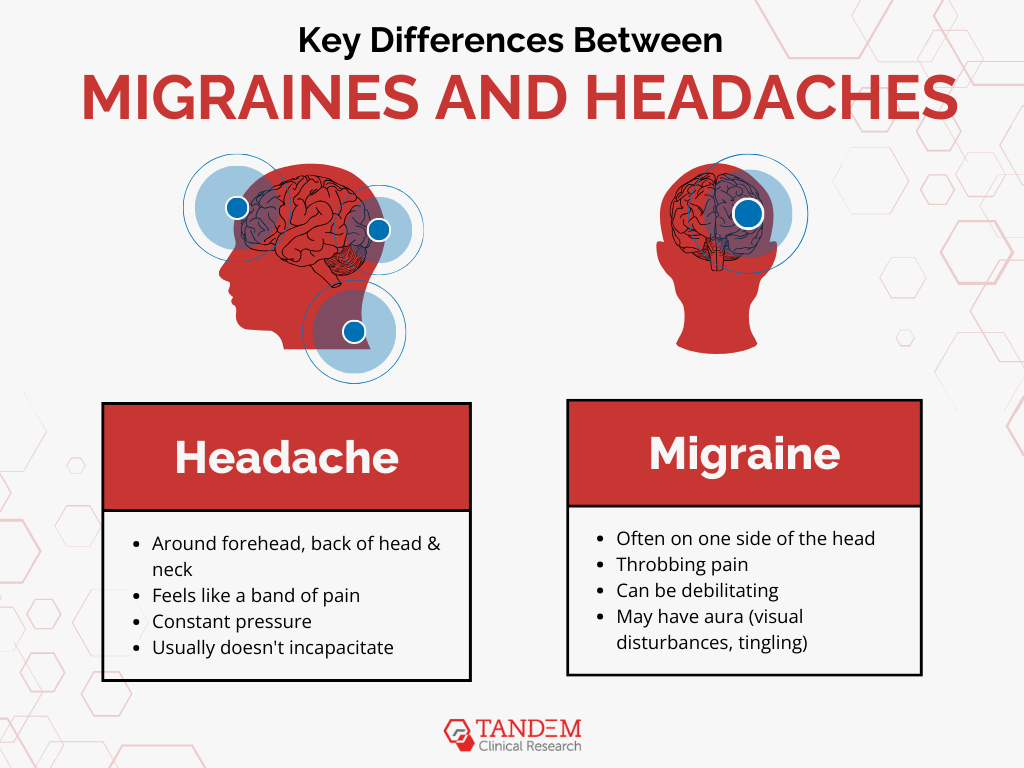

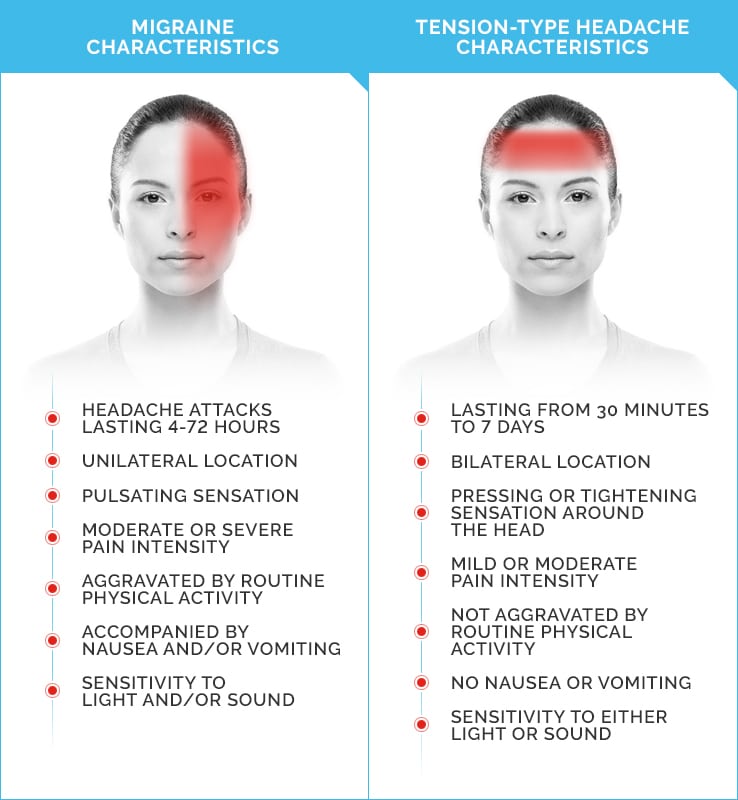

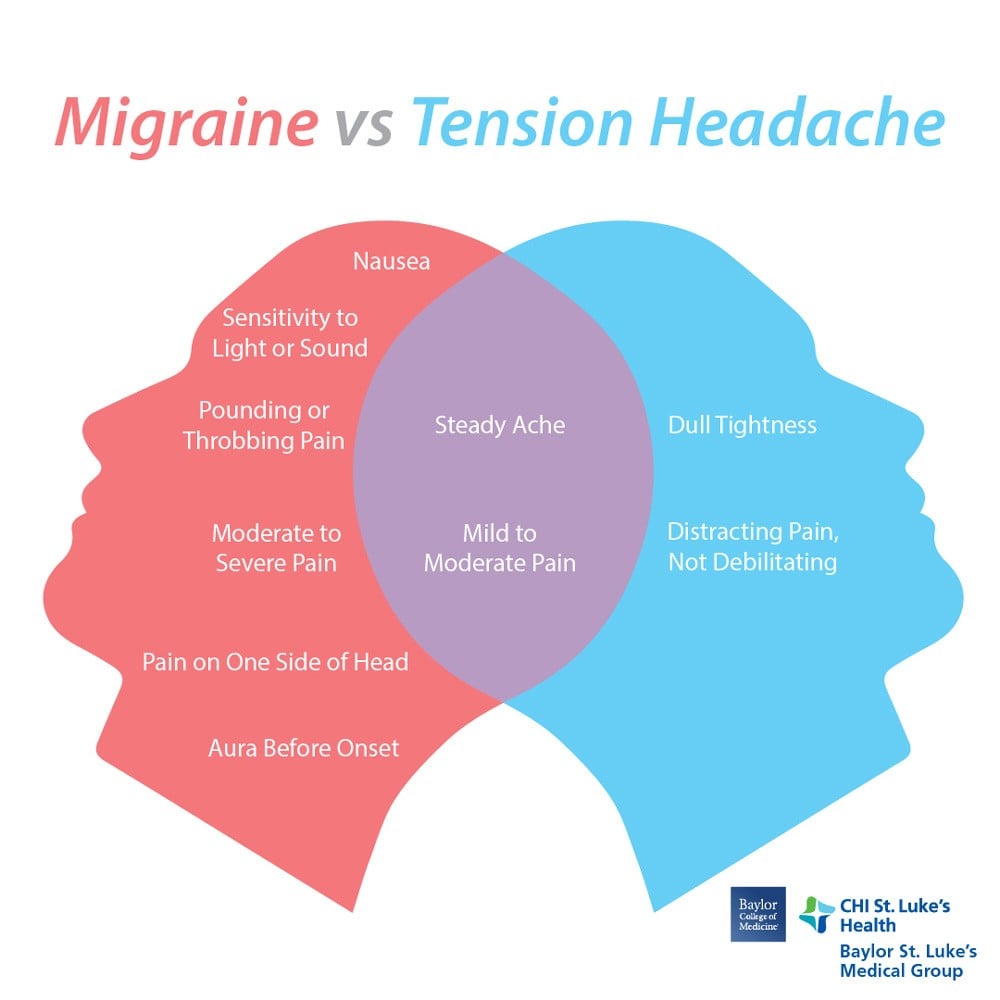

Before one can treat a problem, one must understand its nature. In medicine, a headache is often a symptom of external stress or dehydration. A migraine, conversely, is a complex neurological condition. In finance, this distinction holds true: a headache is an isolated incident, while a migraine is a systemic failure.

The Temporary Tension: Understanding the Financial Headache

A financial headache is a short-term disruption. It is the “tension-type” pain of the business world. Perhaps a client is late on a single payment, or a specific stock in your portfolio dips 3% due to a general market correction. These events are irritating and may cause temporary stress, but they do not threaten the underlying viability of your financial life.

Financial headaches are typically characterized by their “surface-level” nature. They are often solved by simple adjustments—cutting discretionary spending for a month, reallocating a small portion of an emergency fund, or negotiating a brief extension on a vendor contract. They are localized and do not “radiate” into other areas of your financial health.

The Systemic Surge: When a Headache Evolves into a Migraine

A financial migraine is a different beast entirely. It is not just “a worse headache”; it is a systemic crisis that renders you unable to function. If a headache is a late payment, a migraine is the loss of your largest contract while simultaneously carrying a high debt-to-income ratio.

Financial migraines are often accompanied by “aura”—warning signs that the pain is coming, such as declining industry trends or rising interest rates. When the “attack” hits, it affects everything: your credit score, your ability to leverage assets, and your long-term retirement goals. Unlike a headache, you cannot simply “power through” a financial migraine; it requires a specialized recovery plan and often a fundamental change in behavior.

Diagnosing the Symptoms: Why Your Portfolio is Hurting

To manage risk effectively, you must identify the triggers of your financial discomfort. Misdiagnosing a migraine as a simple headache can lead to “under-treatment,” where you apply a small fix to a gaping structural hole.

Market Volatility vs. Fundamental Weakness

Every investor experiences the headache of market volatility. The stock market is naturally noisy, and price fluctuations are the “weather” of the financial world. If your portfolio drops because the entire S&P 500 is down, you are experiencing a common headache.

However, if your portfolio is suffering while the rest of the market is thriving, you have a financial migraine caused by fundamental weakness. This might be due to over-concentration in a dying industry, poor asset selection, or high management fees that are eroding your returns. Diagnosing this requires looking past the daily news and analyzing the “bones” of your investments.

Debt Management: From Interest Friction to Insolvency

Debt is a common source of financial pain. A “headache” level of debt might be a credit card balance that you didn’t quite clear this month, leading to a small interest charge. It’s annoying, but manageable.

The “migraine” version of debt is structural insolvency or a “debt trap.” This occurs when the cost of servicing your debt (interest) exceeds your ability to pay down the principal, or when your debt-to-equity ratio in a business venture becomes so skewed that lenders refuse to work with you. At this stage, the pain is chronic. It prevents you from taking advantage of new opportunities, much like a physical migraine prevents a person from standing in a bright room.

Tax Inefficiency: The Silent Throb

Sometimes, financial pain isn’t a sudden sharp pang; it’s a dull, constant throb. Tax inefficiency is the quintessential example. Many people treat tax season as an annual headache—a few weeks of gathering receipts and feeling stressed. However, for high-net-worth individuals or complex businesses, poor tax planning is a chronic migraine. Over decades, losing an extra 5% to 10% of your wealth to avoidable taxes can result in millions of dollars in lost compounded growth.

Preventative Medicine: Strategies for Long-term Financial Health

The best way to deal with a migraine is to prevent it from happening in the first place. In finance, “preventative medicine” involves building a robust framework that can absorb shocks without collapsing.

Diversification as the Ultimate Aspirin

In the medical world, there is no single cure for a migraine, but there are treatments that reduce frequency. In finance, that treatment is diversification. By spreading your capital across different asset classes—equities, fixed income, real estate, and perhaps private equity or commodities—you ensure that a “migraine” in one sector (such as a tech bubble bursting) only registers as a “headache” in your overall portfolio.

Diversification acts as a shock absorber. It doesn’t stop the market from moving, but it prevents the movement from becoming a debilitating event for your personal net worth.

Building an Emergency Fund Buffer

A significant cause of financial migraines is the “liquidity crunch”—needing cash immediately but having it locked away in illiquid assets. An emergency fund is the financial equivalent of a preventative daily medication.

By maintaining three to six months of operating expenses in a high-yield savings account, you transform potential catastrophes into manageable inconveniences. A car breakdown or a sudden home repair is a headache when you have the cash; it becomes a migraine when you have to put it on a high-interest credit card and start a cycle of debt.

The Role of Financial Audits and Check-ups

Just as a doctor uses an MRI to see what’s happening beneath the surface, a regular financial audit can reveal hidden triggers. This involves reviewing your insurance policies, updating your estate plan, and analyzing your spending patterns.

Many financial migraines are caused by “lifestyle creep”—the gradual increase in spending as income rises. Periodic audits help you identify if your overhead is becoming too heavy, allowing you to trim the fat before the weight causes a systemic breakdown.

Operational Resilience: Scalability and Risk Assessment

For business owners, the stakes of misdiagnosing a headache vs. a migraine are even higher. A business that ignores a “migraine” doesn’t just lose money; it ceases to exist.

Auditing Your Tech Stack to Reduce Overhead Stress

In the modern economy, “Money” and “Tech” are inextricably linked. Often, what looks like a financial migraine (high overhead and low margins) is actually a tech headache. Using outdated software or manual processes for tasks that could be automated creates a “friction cost” that bleeds profit.

By investing in the right financial tools—automated accounting, AI-driven inventory management, and robust CRM systems—businesses can eliminate the repetitive headaches that lead to organizational burnout and financial strain.

The Role of Professional Financial Advisory

Finally, we must recognize that we cannot always self-diagnose. In medicine, if you have a recurring migraine, you see a neurologist. In money management, if you face recurring financial instability, you see a Certified Financial Planner (CFP) or a specialized consultant.

Professional advisors provide an objective perspective. They can see the “blind spots” that you might miss because you are too close to the situation. They help differentiate between a temporary dip in the business cycle and a fundamental shift in the economy that requires a total pivot of your business model.

Conclusion: The Cost of Misdiagnosis

The difference between a headache and a migraine is more than just intensity; it is about the “why” and the “how long.” A financial headache is an event; a financial migraine is a condition.

If you treat a migraine with just an aspirin—meaning, if you treat a systemic financial failure with a temporary patch—the pain will return, and it will be worse. Success in personal finance and business requires the maturity to recognize when a problem is deep-rooted. By building diversified portfolios, maintaining high liquidity, and conducting regular “health checks” on your assets, you can ensure that your financial life remains vibrant, healthy, and, most importantly, pain-free.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.