Understanding the “current interest rate” is akin to asking “what’s the weather like?” – the answer depends heavily on where you are, what you’re looking at, and what specifically you want to measure. There isn’t a single, universal interest rate that applies to all financial transactions. Instead, the financial landscape is governed by a complex ecosystem of rates, each influencing different aspects of our economic lives, from borrowing for a home to saving for retirement. These rates are dynamic, constantly shifting in response to economic indicators, central bank policies, and global market forces.

For individuals and businesses alike, knowing and understanding these rates is paramount. It dictates the cost of debt, the return on savings, and the overall economic environment for investment and growth. This article will demystify the various facets of “the current interest rate,” exploring its foundational elements, its impact on borrowing and saving, and strategies for navigating today’s rate environment to achieve financial wellness. We’ll delve into the central bank’s role, the specifics of consumer and business rates, and how these figures shape investment opportunities and challenges.

Understanding the Fed Funds Rate and Its Ripple Effect

At the heart of the interest rate ecosystem in the United States lies the Federal Funds Rate. While not a rate directly charged to consumers, it’s the benchmark that sets the tone for nearly all other interest rates in the economy. Grasping its function and influence is the first step in understanding “what’s the current interest rate” truly means.

The Federal Reserve’s Role

The Federal Reserve, often called the “Fed,” is the central banking system of the United States. Its primary mandates are to promote maximum employment, stable prices, and moderate long-term interest rates. To achieve these goals, the Fed utilizes several monetary policy tools, with the Federal Funds Rate being the most prominent. This rate is the target rate for overnight lending between banks, crucial for maintaining adequate liquidity in the banking system. The Federal Open Market Committee (FOMC), comprising members of the Board of Governors and presidents of various Federal Reserve Banks, meets eight times a year (or more, if necessary) to decide whether to raise, lower, or maintain the target range for the Federal Funds Rate. Their decisions are based on a careful assessment of economic data, including inflation, employment figures, GDP growth, and global economic conditions. A higher target rate typically aims to cool down an overheating economy and curb inflation, while a lower rate is intended to stimulate economic activity during downturns.

How It Impacts Other Rates

The ripple effect of the Federal Funds Rate is profound and pervasive. When the Fed adjusts its target rate, it sends a strong signal throughout the financial markets, influencing a cascade of other interest rates.

- Prime Rate: Banks use the Federal Funds Rate as a key input for determining the prime rate, which is the interest rate banks charge their most creditworthy corporate customers. The prime rate is typically about 3 percentage points higher than the upper limit of the Federal Funds Rate target range.

- Consumer Loans: Because many consumer loans, such as credit cards, home equity lines of credit (HELOCs), and some adjustable-rate mortgages (ARMs), are tied to the prime rate, changes in the Fed Funds Rate directly impact their Annual Percentage Rates (APRs). When the Fed raises rates, the cost of borrowing for these products increases, and vice versa.

- Mortgage Rates: While mortgage rates aren’t directly tied to the Federal Funds Rate, they are heavily influenced by it and by the broader bond market, particularly the yield on 10-year Treasury bonds. Higher Fed rates often lead to higher yields on Treasuries, which in turn push mortgage rates upward.

- Savings Rates: On the flip side, higher Federal Funds Rates generally translate to better returns for savers. Banks, needing to attract deposits, will offer higher interest rates on savings accounts, money market accounts, and Certificates of Deposit (CDs).

Current Stance and Future Outlook

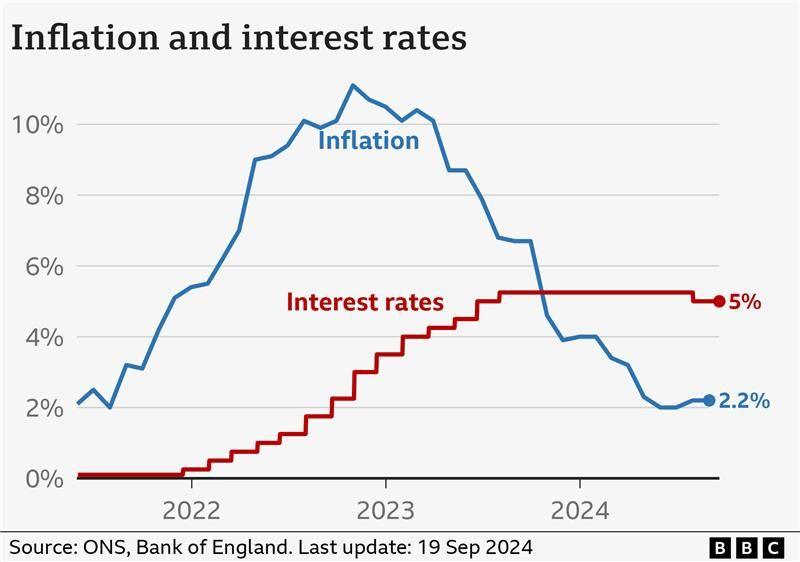

As of my last update, the Federal Reserve had taken significant action to combat elevated inflation by raising the Federal Funds Rate aggressively. This period has seen a shift from an era of historically low interest rates to a more restrictive monetary policy environment. The “current stance” typically involves the Fed maintaining a cautious approach, weighing incoming economic data carefully. Discussions around “higher for longer” have dominated, implying that rates might remain elevated for an extended period to ensure inflation is firmly brought under control, even if this means potential headwinds for economic growth. Future outlooks are constantly debated among economists and policymakers, with potential for rate cuts if inflation cools significantly or if the economy shows signs of a severe slowdown, or further hikes if inflation proves stubbornly persistent. These dynamics underscore the need for individuals and businesses to stay informed about the Fed’s announcements and economic projections.

Interest Rates for Borrowers: Mortgages, Loans, and Credit

For most individuals and businesses, the “current interest rate” primarily registers as the cost of borrowing. Whether it’s securing a home, financing a car, or funding business expansion, interest rates dictate affordability and long-term financial commitments.

Mortgage Rates Explained

Mortgage rates are arguably the most impactful interest rates for many households. They determine the monthly payment on potentially the largest debt many people will ever take on.

- Fixed-Rate Mortgages (FRMs): The interest rate remains constant for the entire loan term (e.g., 15 or 30 years). This provides predictability and protection against rising rates but means you won’t benefit if rates fall unless you refinance. Factors influencing FRMs include the yield on long-term Treasury bonds, lender profitability, and the overall economic outlook.

- Adjustable-Rate Mortgages (ARMs): These loans feature an initial fixed-rate period (e.g., 3, 5, 7, or 10 years), after which the rate adjusts periodically based on a chosen index (like SOFR – Secured Overnight Financing Rate) plus a margin set by the lender. ARMs can offer lower initial payments but carry the risk of significantly higher payments if rates rise.

The current mortgage rate environment is influenced by the Fed’s actions (indirectly affecting bond yields) and the market’s perception of inflation and economic growth. Higher rates mean higher monthly payments and reduced purchasing power for homebuyers, impacting housing affordability and market activity.

Consumer Loans (Auto & Personal)

Auto loans and personal loans are also directly affected by the prevailing interest rate environment.

- Auto Loans: Interest rates on car loans are influenced by the Federal Funds Rate, the prime rate, and, significantly, the borrower’s credit score. A higher credit score typically translates to a lower interest rate, as lenders perceive less risk. In a high-rate environment, the total cost of a vehicle increases, potentially pushing buyers towards more affordable models or longer loan terms, which can accumulate more interest over time.

- Personal Loans: These unsecured loans are often used for debt consolidation, home improvements, or unexpected expenses. Their interest rates are highly dependent on the borrower’s creditworthiness and the lender’s risk assessment. Like other consumer loans, personal loan rates tend to rise when the Fed increases its benchmark rate, making them a more expensive option for accessing funds. Understanding the current rates for these loans is crucial before taking on new debt, as even a percentage point difference can amount to hundreds or thousands of dollars over the loan’s lifetime.

Credit Card APRs

Credit card Annual Percentage Rates (APRs) are typically among the highest interest rates consumers face. Most credit card APRs are variable, meaning they fluctuate with changes in the prime rate, which, as discussed, moves in tandem with the Federal Funds Rate.

- Impact of Fed Hikes: When the Fed raises rates, credit card APRs often follow suit within one or two billing cycles. This directly increases the cost of carrying a balance, making it more challenging for consumers to pay off debt and potentially leading to higher minimum payments.

- Managing High-Interest Debt: In a high-rate environment, managing credit card debt becomes even more critical. Strategies include paying off balances in full each month, prioritizing payments on cards with the highest APRs, and considering balance transfer cards (though be wary of introductory periods and transfer fees). The “current interest rate” for credit cards underscores the importance of minimizing revolving debt.

Business Loans

For businesses, interest rates are a critical factor in growth, operations, and investment decisions. Whether it’s a small business seeking a line of credit or a large corporation issuing bonds, the cost of capital directly impacts profitability and expansion plans.

- Small Business Loans: Small business loans, including term loans, SBA loans, and lines of credit, are heavily influenced by the prime rate and market conditions. Higher rates increase the cost of borrowing for equipment purchases, inventory, or working capital, potentially slowing down expansion or even necessitating budget cuts.

- Corporate Bonds: Larger corporations often raise capital by issuing bonds. The interest rate (yield) on these bonds is determined by market demand, the company’s creditworthiness, and the prevailing interest rate environment. Higher general interest rates mean companies have to offer higher yields to attract investors, increasing their financing costs.

Understanding the current rate environment for business loans is vital for strategic planning, cash flow management, and making informed decisions about taking on debt for future growth.

Interest Rates for Savers and Investors: Opportunities and Challenges

While higher interest rates generally mean higher borrowing costs, they often present a more favorable environment for savers and certain types of investors. The “current interest rate” significantly impacts how money grows and where capital is allocated.

Savings Accounts & CDs

For everyday savers, a rising interest rate environment can be a welcome change after years of near-zero returns.

- High-Yield Savings Accounts (HYSAs): As the Fed raises its benchmark rate, banks often increase the interest rates offered on savings accounts to attract deposits. Online-only banks and challenger banks typically lead the way with high-yield savings accounts, offering significantly better rates than traditional brick-and-mortar institutions. These accounts provide a safe place to store cash while earning a competitive return.

- Money Market Accounts: Similar to savings accounts, money market accounts offer competitive interest rates and often come with limited check-writing privileges. Their rates also tend to climb with broader market interest rates.

- Certificates of Deposit (CDs): CDs lock in your money for a specified term (e.g., 3 months, 1 year, 5 years) in exchange for a fixed interest rate, which is usually higher than standard savings accounts. In a rising rate environment, CDs become more attractive as their yields increase. Savers can employ a “CD laddering” strategy, investing in CDs with staggered maturity dates to take advantage of potentially higher rates in the future while maintaining some liquidity. The current rate environment makes these vehicles particularly attractive for parking emergency funds or short-term savings goals.

Bond Market Dynamics

The bond market has an inverse relationship with interest rates. When interest rates rise, the price of existing bonds (which pay a fixed coupon rate) typically falls, because newly issued bonds offer higher yields, making older bonds less attractive.

- Yields and Prices: Understanding this dynamic is crucial for bond investors. If you buy a bond at a lower interest rate, and then market rates rise, the resale value of your bond will likely decrease. Conversely, if you buy a bond when rates are high, you lock in a higher yield, and its value could increase if market rates subsequently fall.

- Government Bonds (Treasuries): Treasury bills, notes, and bonds are considered among the safest investments. Their yields are a benchmark for the broader market and are highly responsive to the Fed’s actions and economic forecasts. In a high-rate environment, Treasury yields become more competitive, offering a low-risk option for generating income.

- Corporate Bonds: The yields on corporate bonds also rise with the general interest rate environment, reflecting both the prevailing risk-free rate (like Treasuries) and the credit risk of the issuing company.

Impact on Stock Market

The relationship between interest rates and the stock market is complex and multifaceted.

- Valuation: Higher interest rates increase the cost of capital for businesses, meaning future earnings are discounted at a higher rate. This can lead to lower valuations for companies, particularly growth stocks that rely heavily on future earnings potential.

- Corporate Earnings: Higher rates can increase borrowing costs for businesses, potentially reducing their profitability if they carry significant debt. This can negatively impact earnings per share.

- Investor Sentiment: When interest rates on safe assets (like savings accounts or government bonds) increase, they become more attractive relative to riskier investments like stocks. This can cause some investors to shift capital away from equities, putting downward pressure on stock prices.

- Sectoral Impact: Certain sectors may be more sensitive than others. For example, financial institutions (banks) can sometimes benefit from higher rates if their lending margins improve, while highly leveraged companies or those in capital-intensive industries might struggle more.

Navigating the stock market in a high-rate environment requires careful analysis of company fundamentals, sector exposure, and a focus on diversification to mitigate risks.

Navigating the Current Rate Environment: Strategies for Financial Wellness

The current interest rate environment, characterized by central banks’ efforts to manage inflation, demands a proactive and informed approach to personal and business finance. Adapting your strategies can help you mitigate risks and capitalize on opportunities.

For Borrowers

In an environment where interest rates are elevated or expected to rise, borrowers need to be strategic to minimize costs.

- Prioritize High-Interest Debt: Focus on paying down credit card balances, personal loans, or other variable-rate debts with the highest APRs first. This will save you significant money over time as interest accrues faster on these debts.

- Lock in Fixed Rates: If you are considering a major purchase requiring financing, such as a home or a car, and you anticipate rates might rise further, explore locking in a fixed-rate loan if possible. This provides payment predictability and protects you from future increases.

- Refinancing Opportunities: If rates have fallen since you took out a loan, or if you have an adjustable-rate mortgage with a rising rate, investigate refinancing options. A lower fixed rate could reduce your monthly payments and overall interest costs. However, be sure to factor in closing costs and the time it will take to break even.

- Improve Your Credit Score: A higher credit score can qualify you for better interest rates on new loans, even in a generally high-rate environment. Regularly check your credit report, pay bills on time, and keep credit utilization low.

For Savers

Higher interest rates offer a prime opportunity for savers to maximize their returns without taking on significant risk.

- Maximize High-Yield Options: Move idle cash from traditional low-interest savings accounts into high-yield savings accounts (HYSAs) or money market accounts. Compare rates from various online banks and credit unions, as they often offer the most competitive yields.

- Utilize CDs Strategically: Consider Certificate of Deposit (CDs) for funds you don’t need immediate access to. For flexibility, employ a “CD laddering” strategy, investing in multiple CDs with staggered maturity dates (e.g., 6 months, 1 year, 2 years). As shorter-term CDs mature, you can reinvest the money at the then-current rates, potentially capturing higher yields.

- Explore Treasury Bills and Bonds: For safety and competitive returns, consider investing in short-term Treasury bills (T-bills) or Treasury bonds directly through TreasuryDirect. These are backed by the full faith and credit of the U.S. government and can offer attractive yields in a high-rate environment.

For Investors

Investors need to adjust their portfolio strategies to account for the impact of interest rates on different asset classes.

- Diversification: Maintain a diversified portfolio across various asset classes (stocks, bonds, real estate, commodities) and geographies. This helps mitigate risk as different assets perform differently in varying economic conditions.

- Rebalance Portfolios: Periodically review and rebalance your portfolio to ensure it aligns with your risk tolerance and long-term goals. In a high-rate environment, you might find certain sectors or types of investments (e.g., value stocks over growth stocks, or short-term bonds) more appealing.

- Focus on Quality and Fundamentals: In an uncertain rate environment, focus on investing in companies with strong balance sheets, consistent earnings, and competitive advantages. These “quality” companies tend to be more resilient during economic fluctuations.

- Consult a Financial Advisor: For complex financial situations or significant assets, a qualified financial advisor can provide personalized guidance, helping you tailor your investment strategy to the current rate environment and your individual circumstances.

Personal Financial Planning

Regardless of interest rate fluctuations, solid personal financial planning remains the bedrock of financial wellness.

- Budgeting and Cash Flow Management: Maintain a detailed budget to understand your income and expenses. This clarity helps you identify areas to save more, especially when borrowing costs are high, or to direct extra funds toward high-yield savings.

- Emergency Fund: Always prioritize building and maintaining a robust emergency fund (3-6 months of living expenses) in a readily accessible, high-yield account. This provides a crucial buffer against unexpected expenses and reduces the need to take on high-interest debt.

- Long-Term Goal Setting: Keep your long-term financial goals (retirement, college savings, homeownership) in sight. While the current rate environment influences short-term tactics, your overarching strategy should remain focused on these objectives, adjusting your path as needed.

The “current interest rate” is not a static figure but a dynamic reflection of economic health and monetary policy. By understanding its many facets and proactively implementing sound financial strategies, individuals and businesses can navigate its complexities and build a more secure financial future. Continuous learning and adaptation are key to thriving in any economic cycle.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.