Navigating the world of automotive financing can feel like a complex journey, often overshadowed by the excitement of choosing a new vehicle. Yet, understanding the financial mechanics, particularly car loan interest rates, is paramount to making a fiscally sound decision. For many, a car purchase represents one of the largest financial commitments outside of a mortgage. The interest rate on your car loan is not merely a small percentage; it’s a critical factor that directly influences your monthly payments, the total cost of your vehicle, and ultimately, your long-term financial health.

The “average” interest rate for a car loan is a figure often sought after by prospective buyers as a benchmark. However, this average is a moving target, influenced by a myriad of economic conditions, lender policies, and, perhaps most significantly, individual borrower profiles. This article will demystify car loan interest rates, explore the factors that shape them, provide insights into current market averages, and arm you with strategies to secure the most favorable terms for your next vehicle purchase. By delving deep into these aspects, we aim to empower you to approach car financing with confidence and financial acumen.

Understanding Car Loan Interest Rates: A Foundation for Savvy Borrowing

Before diving into averages and strategies, it’s crucial to grasp the fundamental concepts surrounding car loan interest rates. This foundational understanding will serve as your compass in the often-murky waters of automotive financing.

Defining Interest Rates in Automotive Financing

At its core, an interest rate is the cost of borrowing money, expressed as a percentage of the principal amount. When you take out a car loan, the lender provides you with the funds to purchase the vehicle, and in return, you agree to repay that principal amount plus interest over a predetermined period.

It’s important to distinguish between the simple interest rate and the Annual Percentage Rate (APR). While the interest rate reflects only the cost of borrowing the principal, the APR provides a more comprehensive measure. The APR includes the interest rate plus any additional fees associated with the loan, such as origination fees or administrative charges. Therefore, the APR is generally a more accurate reflection of the total annual cost of your loan. When comparing loan offers, always focus on the APR for an apples-to-apples comparison. A seemingly lower interest rate might hide higher fees that push its APR above an alternative offer.

Why the Average Matters (and Why It’s Just a Starting Point)

The “average” interest rate serves as a valuable benchmark. It gives you a general idea of what borrowers with similar credit profiles are currently paying in the market. Knowing the average can help you identify if a loan offer is competitive, exceptionally good, or potentially too high. If you’re offered a rate significantly above the average for someone with your credit standing, it’s a strong signal to shop around more aggressively or investigate the reasons for the disparity.

However, it’s crucial to understand that the average is just that—an average. It smooths out vast differences between individual borrowers and market conditions. Your specific rate will be tailored to your unique financial situation, the type of car you’re buying, and the prevailing economic climate. Using the average as a reference point for negotiation and comparison is smart, but never expect to automatically qualify for it. Your individual profile is the ultimate determinant.

The Cost of Borrowing: How Interest Impacts Your Payment

The interest rate is arguably the single most impactful factor on the total cost of your car loan and your monthly payment amount. Even a seemingly small difference in percentage points can translate into hundreds or thousands of dollars over the life of the loan.

Consider a $30,000 car loan over 60 months.

- At an interest rate of 5%, your monthly payment would be approximately $566, and you’d pay roughly $3,960 in total interest.

- At an interest rate of 8%, your monthly payment jumps to about $608, and your total interest paid climbs to roughly $6,480.

This difference of just three percentage points results in an additional $42 per month and over $2,500 in total interest paid. This illustrates how the interest rate is not just a number on a contract but a tangible figure that directly impacts your budget and overall expenditure on the vehicle. Understanding this impact encourages diligence in seeking the best possible rate.

Deciphering the Drivers: Key Factors Influencing Your Car Loan Interest Rate

While the average interest rate provides a broad overview, your personal rate will be a highly individualized figure determined by several critical factors. Lenders meticulously assess these elements to gauge the risk associated with lending to you.

Your Credit Score and History: The Ultimate Predictor

Your credit score is arguably the most significant determinant of the interest rate you’ll be offered. Lenders use this three-digit number, primarily FICO and VantageScore, to quickly assess your creditworthiness and the likelihood of you repaying the loan.

- Excellent Credit (780+): Borrowers in this tier typically qualify for the lowest available rates, often referred to as “prime” rates, reflecting minimal risk.

- Good Credit (670-739): Still considered low-risk, these borrowers can expect competitive rates, though slightly higher than those with excellent credit.

- Fair Credit (580-669): Rates for this group begin to climb, as lenders perceive a moderate risk.

- Poor Credit (Below 580): Borrowers with poor credit fall into the “subprime” category and will face significantly higher interest rates to compensate lenders for the increased risk of default.

Your credit history, which details your past payment behavior, debt levels, and credit utilization, provides the narrative behind your score, reinforcing or mitigating the lender’s risk assessment. Consistent on-time payments, low credit utilization, and a long credit history all contribute to a stronger credit profile and, consequently, lower interest rates.

Loan Term and Down Payment: Balancing Monthly Payments and Total Cost

The loan term, or the length of time you have to repay the loan, also plays a crucial role.

- Shorter Terms (e.g., 36 or 48 months): Typically come with lower interest rates because the lender’s money is at risk for a shorter period. While monthly payments will be higher, you’ll pay significantly less interest over the life of the loan.

- Longer Terms (e.g., 72 or 84 months): Often carry higher interest rates. Lenders perceive a greater risk over extended periods, and there’s a higher chance of the car depreciating faster than the loan balance (becoming “upside down”). While longer terms reduce monthly payments, they dramatically increase the total interest paid.

A down payment also significantly influences your rate. A larger down payment reduces the principal amount you need to borrow, thus lowering the lender’s risk. It also demonstrates your financial commitment to the purchase. Lenders are more likely to offer better rates when their exposure is minimized. Aim for at least 10-20% of the car’s purchase price as a down payment, if possible.

Vehicle Age and Type: New vs. Used, Luxury vs. Economy

The car itself impacts the loan rate.

- New Cars: Generally qualify for lower interest rates. They depreciate slower in the initial years compared to used cars, making them better collateral for the lender. Manufacturers also often offer promotional low-APR financing on new vehicles to boost sales.

- Used Cars: Typically carry higher interest rates. They have already undergone significant depreciation, and their future value is less predictable, presenting a higher risk for the lender. Additionally, mechanical issues are more likely with used vehicles, which can impact a borrower’s ability to repay.

The type of vehicle (e.g., a high-demand luxury car versus a standard economy sedan) can also subtly affect rates, reflecting perceived market value and resale liquidity.

Economic Conditions and Lender Policies: Broader Market Influences

Beyond individual factors, broader economic conditions exert significant influence:

- Federal Reserve Interest Rates: When the Federal Reserve raises its benchmark interest rates, the cost of borrowing for banks increases, which then translates to higher rates for consumers on various loans, including car loans.

- Inflation: High inflation can also push rates up as lenders seek to maintain the real value of their returns.

- Lender Competition: A competitive lending market can drive rates down as banks, credit unions, and online lenders vie for customers. Conversely, less competition might lead to higher rates.

- Lender-Specific Risk Assessment: Each lender has its own internal algorithms and risk tolerance that can lead to slightly different rate offers for the same borrower.

Debt-to-Income Ratio: Assessing Your Repayment Capacity

Lenders also examine your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. A lower DTI indicates that you have ample income to cover your existing obligations plus the new car payment, signaling a lower risk to the lender. A high DTI might suggest you’re overextended, making you a higher risk and potentially leading to a higher interest rate or even loan denial. Lenders typically prefer a DTI below 36%, though some may accept higher depending on other strong credit factors.

The Current Landscape: What Are Typical Car Loan Interest Rates Right Now?

Understanding the factors that influence car loan rates is one thing; knowing what rates are generally available in the current market is another. It’s important to remember that these figures are averages and ranges, subject to change based on the economy, Federal Reserve policy, and specific lender offerings.

General Trends in Auto Lending

Over recent years, the auto lending market has seen fluctuations. Periods of low interest rates, driven by accommodative monetary policies, have given way to higher rates as central banks combat inflation. This means that rates today are generally higher than they were a few years ago. Supply chain issues affecting vehicle availability can also indirectly influence rates, as demand-supply imbalances can shift market dynamics.

Average Rates for New Cars

For borrowers with excellent credit (780+), typical new car loan interest rates often fall within the 3.5% to 6.0% APR range. These are often the lowest rates available, sometimes even lower if a manufacturer is offering special promotional financing (e.g., 0% or 0.9% APR for highly qualified buyers on specific models).

Borrowers with good credit (670-739) can expect rates usually between 5.0% and 8.0% APR. While still competitive, these rates reflect a slightly increased risk profile compared to those with excellent credit.

For those with fair credit (580-669), new car loan rates typically range from 8.0% to 12.0% APR, sometimes higher. Lenders require a greater premium for the perceived elevated risk.

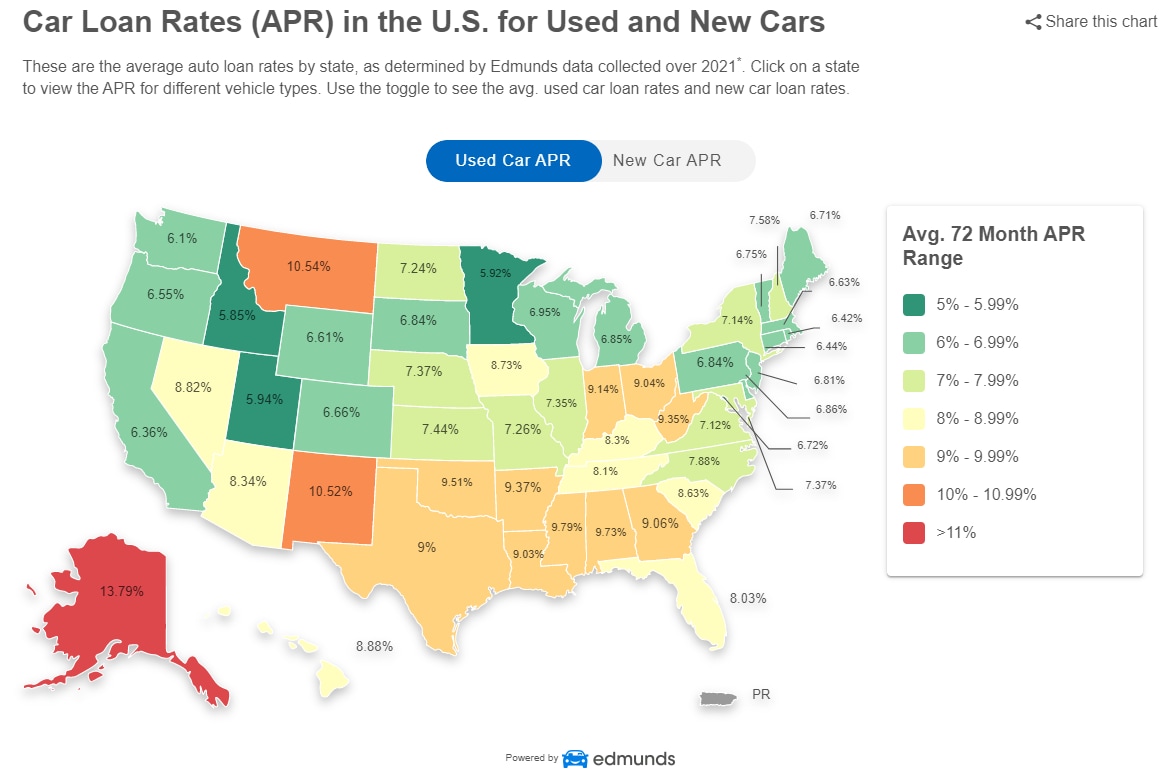

Average Rates for Used Cars

Used car loans, as mentioned, generally carry higher interest rates than new car loans due to higher perceived risk and faster depreciation.

For borrowers with excellent credit (780+), used car loan rates might be in the 5.0% to 8.0% APR range.

With good credit (670-739), expect to see rates typically between 7.0% and 11.0% APR.

For those with fair credit (580-669), used car loan rates often start at 12.0% APR and can go as high as 18.0% APR or more, reflecting a significant risk premium.

The Spectrum: From Excellent to Subprime Borrowers

It’s crucial to acknowledge the wide spectrum of rates. Borrowers with poor credit (below 580), often categorized as subprime, face the highest rates. These can easily exceed 20% or even 25% APR for both new and used cars. Such high rates significantly inflate the total cost of the vehicle and can make monthly payments challenging. For subprime borrowers, improving credit or making a very substantial down payment can be critical to securing more manageable terms. The average rate quoted often skews towards prime borrowers, meaning that many people will encounter rates higher than the widely publicized “average.”

Strategies for Securing a Lower Car Loan Interest Rate

While some factors like economic conditions are beyond your control, there are many proactive steps you can take to improve your chances of securing a lower interest rate. A diligent approach can save you thousands of dollars over the life of your loan.

Boost Your Credit Score

This is arguably the most impactful strategy. A higher credit score signals lower risk to lenders.

- Pay Bills on Time: Payment history is the biggest factor in your credit score. Make all payments (credit cards, loans, utilities) on time, every time.

- Reduce Credit Card Debt: Keep your credit utilization (the amount of credit you’re using compared to your total available credit) low, ideally below 30%. Paying down balances can quickly improve your score.

- Check Your Credit Report Regularly: Dispute any errors or inaccuracies, as these can unfairly drag down your score. You’re entitled to a free report from each of the three major bureaus annually at AnnualCreditReport.com.

- Avoid New Credit Applications: Opening too many new credit accounts in a short period can temporarily lower your score.

Save for a Substantial Down Payment

A larger down payment reduces the amount you need to borrow, which directly lowers the lender’s risk. Aim for at least 10-20% of the car’s purchase price. Not only does it make you a more attractive borrower, but it also reduces your monthly payments and the total interest you’ll pay over the loan term. It also helps prevent you from being “upside down” on your loan (owing more than the car is worth) early in the loan term.

Shop Around Aggressively for Lenders

Never take the first loan offer you receive, especially from a dealership. Instead, compare offers from multiple sources:

- Banks: Traditional banks often offer competitive rates to their existing customers.

- Credit Unions: These member-owned financial institutions are known for offering some of the lowest interest rates on car loans. They often prioritize member benefits over profit.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans and can offer quick pre-approvals and competitive rates.

- Dealership Financing: While often convenient, dealership financing can sometimes be marked up. However, they can also offer promotional rates, especially on new cars.

Get pre-approved for a loan before you step into the dealership. Pre-approval gives you a firm offer of credit, so you know exactly what rate you qualify for. This turns you into a cash buyer at the dealership, giving you leverage to negotiate the car price separately, without the stress of simultaneously arranging financing. Multiple loan inquiries within a short period (typically 14-45 days) will count as a single hard inquiry on your credit report, so shopping for rates won’t harm your score significantly if done within a reasonable timeframe.

Consider a Shorter Loan Term (If Affordable)

While longer loan terms offer lower monthly payments, they nearly always come with higher interest rates and significantly higher total interest paid. If your budget allows, opt for the shortest loan term you can comfortably afford. This strategy not only saves you money on interest but also allows you to pay off the car faster.

Negotiate the Car Price First

Always negotiate the purchase price of the car independently of the financing. Some dealerships might try to distract you with a low monthly payment, which could be achieved through a high interest rate or a very long loan term. By settling on the car’s price first, you ensure you’re getting a fair deal on the vehicle itself before layering financing on top.

Co-Signer or Secured Loan

If you have a lower credit score, a co-signer with excellent credit can significantly improve your chances of getting a lower interest rate. The co-signer essentially guarantees the loan, mitigating the lender’s risk. However, this carries risk for the co-signer, as they are equally responsible for the debt.

A secured loan, using another asset (like a savings account or CD) as collateral, is another option, though less common for car loans directly. Some lenders might offer slightly better rates if you’re willing to secure the loan with an asset other than the car itself, further reducing their risk.

Beyond the Rate: Understanding the Full Financial Commitment of a Car Loan

While the interest rate is a critical component, it’s essential to look at the broader financial picture to fully understand the commitment you’re undertaking. A car loan involves more than just the principal and interest.

Total Cost of Ownership: Interest, Principal, and Fees

The true cost of your car loan extends beyond just the sale price and the interest rate. It includes:

- Principal: The actual amount borrowed to purchase the car.

- Interest: The cost of borrowing the principal over the loan term.

- Fees: Be aware of potential charges such as loan origination fees, documentation fees (doc fees), late payment penalties, and pre-payment penalties (though less common in auto loans, always check). These can add hundreds of dollars to your overall cost. Always ask for a detailed breakdown of all fees.

Understanding the total amount you will pay over the life of the loan is far more important than just focusing on the monthly payment. A lower monthly payment achieved through a longer loan term often means paying significantly more in total interest.

The Impact of Add-ons and Warranties

Dealerships often try to sell various add-ons and extended warranties with your vehicle purchase. While some might offer value, many are overpriced or unnecessary. If you roll the cost of these items into your car loan, you’re not only paying for the add-on but also paying interest on it for the entire loan term. This significantly inflates the actual cost of the add-on. Carefully evaluate each add-on, negotiate its price separately, and if possible, pay for it upfront or finance it through a cheaper, separate method if it’s truly essential.

Long-Term Affordability and Budgeting

Before signing on the dotted line, ensure the car payment fits comfortably within your overall budget. Financial experts often recommend that your total car expenses (including payment, insurance, fuel, maintenance) should not exceed 10-20% of your net monthly income. A common rule of thumb is the “20/4/10” rule:

- 20% Down Payment: To avoid being upside down and reduce interest.

- 4-Year Loan Term (Maximum): To minimize interest paid and avoid excessive depreciation.

- 10% of Gross Income: For total monthly car expenses (payment, insurance, fuel, maintenance).

Stretching your budget too thin for a car can impact your ability to save for other financial goals, contribute to retirement, or handle unexpected emergencies. Always factor in ongoing costs like insurance, fuel, and maintenance, which can be substantial.

Refinancing Options: A Second Chance at a Better Rate

If you’ve already taken out a car loan and your financial situation has improved (e.g., your credit score has increased, or you’ve reduced other debts), or if market interest rates have dropped, refinancing could be a smart move. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can reduce your monthly payments, decrease the total interest paid, or shorten your loan term. It’s a particularly effective strategy for those who initially had a high interest rate due to a poor credit score that has since improved. Shop around for refinance loans just as you would for a new car loan.

Conclusion

Understanding “what’s the average interest rate on a car loan” is far more nuanced than simply looking up a single number. It requires an appreciation of the dynamic interplay between your personal financial health, the specific characteristics of the vehicle, the prevailing economic climate, and the policies of individual lenders. While current averages provide a useful benchmark, your individual rate will be a direct reflection of your creditworthiness and the terms you negotiate.

By diligently working to improve your credit score, making a substantial down payment, actively shopping around for the best rates from multiple lenders, and carefully considering the loan term and all associated fees, you can significantly reduce the cost of financing your vehicle. Remember to view the car loan not in isolation but as part of your broader financial strategy, ensuring it aligns with your long-term goals and budget. With thoughtful planning and informed decision-making, you can drive away with a car loan that is both affordable and fiscally responsible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.