Ohio’s sales tax system is a critical component of the state’s revenue generation, directly impacting consumers and businesses alike. While there’s a statewide base rate, the actual sales tax applied to purchases can vary significantly depending on the specific county where a transaction occurs. Understanding this nuanced structure is essential for accurate budgeting, compliance, and effective financial management, whether you’re an individual making everyday purchases, an entrepreneur starting a new venture, or an established business navigating multi-county operations.

Understanding Ohio’s Sales Tax Structure

At its core, Ohio’s sales tax system combines a uniform statewide rate with additional local permissive taxes imposed by counties. This layered approach means that the total sales tax rate is never just one figure across the entire state, but rather a spectrum of rates ranging from the statewide minimum to higher combined rates in various locales.

The Statewide Rate

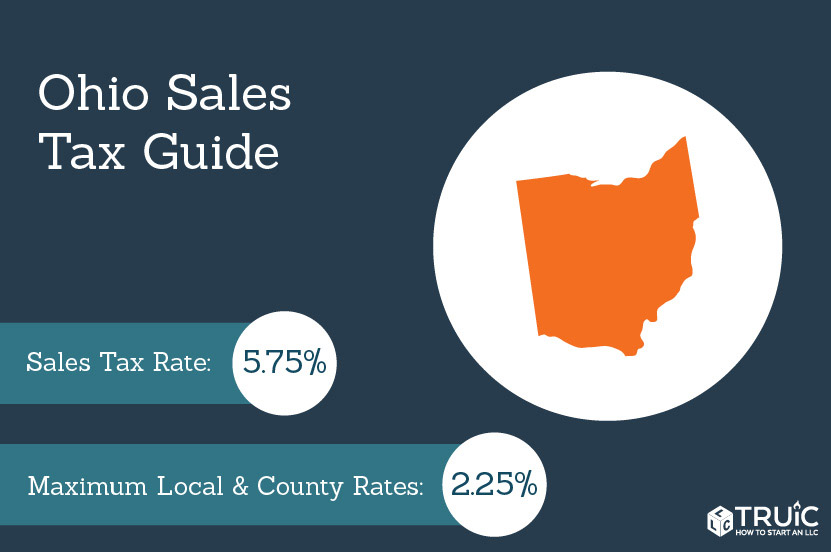

The Ohio Revised Code establishes a foundational sales tax rate that applies uniformly across all 88 counties. This base rate is crucial as it forms the irreducible minimum for any taxable sale within the state. While this rate can be subject to legislative changes, it provides a consistent starting point for all sales tax calculations before local additions. This statewide component ensures a baseline revenue stream for state-level services and initiatives.

Local Permissive Taxes

Beyond the statewide base, each county in Ohio has the authority to levy its own “permissive sales tax.” These county-specific taxes are approved by local authorities, often through voter referendums or county commission decisions, to fund local services such as public safety, infrastructure, and social programs. The rates of these permissive taxes vary widely, reflecting the individual financial needs and priorities of each county. Some counties may opt for a higher permissive tax to support more extensive local services, while others maintain lower rates.

Combined Rates and How They Work

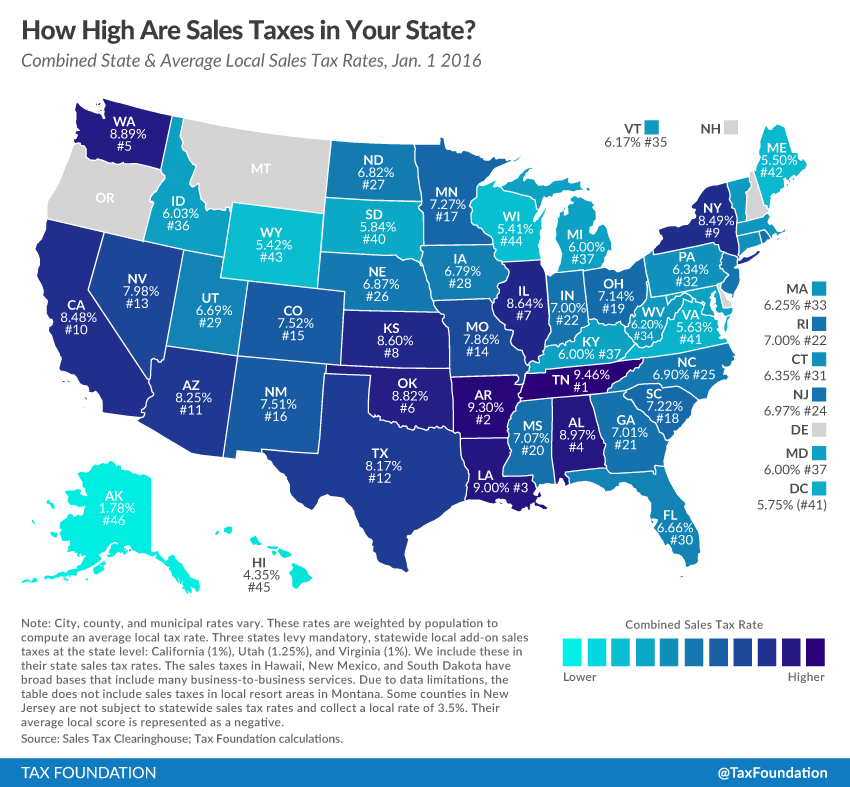

The effective sales tax rate a consumer pays or a business collects is the sum of the statewide rate and the applicable county permissive tax. For example, if the statewide rate is 5.75% and a particular county has a 1.25% permissive tax, the combined rate in that county would be 7.00%. This combination means that two identical items purchased in different counties could carry different sales tax amounts.

For businesses, especially those operating across county lines or engaging in remote sales, this necessitates a robust system for determining the correct tax rate based on the point of sale or the customer’s location. Accurate application of these combined rates is paramount for compliance and avoiding potential penalties.

Where to Find Current Rates

Given the variability of county rates, relying on outdated information can lead to significant errors. The most reliable source for current sales tax rates across all Ohio counties is the Ohio Department of Taxation. Their official website typically provides a comprehensive list or interactive tool that allows users to look up the combined sales tax rate for any given county. This resource is indispensable for businesses needing to program their point-of-sale systems or accounting software with the correct rates, and for consumers seeking to verify charges.

What’s Taxable and What’s Exempt in Ohio?

Understanding what goods and services are subject to Ohio sales tax, and which are exempt, is as important as knowing the rates themselves. The general rule is that tangible personal property and certain enumerated services are taxable, but a comprehensive list of exemptions exists to support specific industries, essential needs, or economic activities.

General Rule for Tangible Personal Property

In Ohio, the sale of most tangible personal property is subject to sales tax. This includes a vast array of physical goods, from clothing and electronics to vehicles and building materials. If you can touch it, see it, and take it with you, chances are it’s taxable when sold at retail. This broad category forms the bulk of transactions generating sales tax revenue.

Taxable Services

While many services are exempt, Ohio does apply sales tax to a specific list of services. These often include services that are closely tied to tangible personal property or fall under specific legislative definitions. Examples of taxable services can include certain types of repairs (e.g., automobile repair, appliance repair where parts are involved), landscaping services, and some types of telecommunications services. Businesses offering these specific services must understand their obligations to collect and remit sales tax.

Common Exemptions

Ohio provides numerous exemptions from sales tax, often to alleviate the burden on consumers for essential goods, support charitable activities, or promote economic development. Key exemptions include:

- Food for Home Consumption: Most food items purchased from grocery stores or similar establishments for preparation and consumption at home are exempt. However, prepared foods, restaurant meals, and certain snacks or beverages sold for immediate consumption typically remain taxable.

- Prescription Drugs and Medical Devices: To ensure access to healthcare, prescription medications and many types of medical devices are exempt from sales tax.

- Sales for Resale: A fundamental principle of sales tax is to tax the final consumer. Therefore, items purchased by a business with the intent to resell them (without alteration or significant use) are exempt, provided the purchasing business provides a valid exemption certificate.

- Manufacturing Equipment: To encourage industrial growth and investment, certain machinery and equipment used directly in the manufacturing process are exempt from sales tax.

- Digital Products: This is an evolving area. While traditionally many digital products (like software downloads, streaming services, or e-books) were not taxed, states are increasingly adapting their laws. Ohio has specific rules regarding software and other digital goods, which may depend on whether the product is considered a “transfer of tangible personal property” or a “service.”

- Newspapers and Periodicals: Generally exempt when sold by subscription.

- Sales to Non-profit Organizations: Qualified non-profit organizations often enjoy exemptions for purchases made in pursuit of their charitable, educational, or religious missions, provided they have the necessary exemption certificates.

Use Tax – The Counterpart to Sales Tax

Ohio’s use tax is a critical complement to its sales tax. It applies to taxable purchases of tangible personal property or services made outside Ohio, or from an out-of-state vendor that does not collect Ohio sales tax, when those items are subsequently stored, used, or consumed in Ohio. The use tax rate is the same as the combined sales tax rate that would have applied had the purchase been made in Ohio.

For consumers, this often comes into play with online purchases from retailers who lack nexus in Ohio (though this is increasingly rare after the Wayfair decision). For businesses, it’s crucial to self-assess and remit use tax on office supplies, equipment, or inventory purchased from out-of-state suppliers who didn’t charge Ohio sales tax. Failing to remit use tax is a common audit finding and can result in significant penalties.

Practical Implications for Consumers and Businesses

The intricacies of Ohio’s sales tax system have profound practical implications for both individual consumers and businesses operating within or selling into the state. Navigating these rules successfully requires vigilance, accurate record-keeping, and sometimes, specialized tools.

For Consumers

For individuals, understanding sales tax impacts budgeting and purchasing decisions. Knowing the combined rate in your county helps you estimate the final cost of goods before checkout. Furthermore, the rise of e-commerce means consumers are more likely to encounter situations where an out-of-state seller might not collect Ohio sales tax. In such cases, the burden falls on the consumer to report and pay Ohio use tax, though many popular online retailers now collect sales tax nationwide following economic nexus laws. Awareness of exemptions for items like groceries and prescription drugs helps consumers optimize their spending.

For Businesses (Especially Small Businesses & Online Sellers)

The challenges for businesses are significantly more complex, encompassing compliance, collection, remittance, and audit preparedness.

Sales Tax Nexus

The concept of “nexus” is fundamental for businesses. Historically, physical presence (e.g., an office, warehouse, or employees) in Ohio established nexus, obligating a business to collect sales tax. However, the 2018 Supreme Court decision in South Dakota v. Wayfair introduced “economic nexus.” This means even businesses without a physical presence in Ohio must collect and remit sales tax if their sales into the state exceed certain revenue or transaction thresholds (e.g., $100,000 in sales or 200 separate transactions within a calendar year). Businesses selling remotely into Ohio must regularly monitor their sales volume to determine if they’ve crossed these thresholds.

Registration Requirements

Any business making taxable sales in Ohio must first obtain a vendor’s license from the Ohio Department of Taxation. This license authorizes the business to collect sales tax and provides a unique identification number for filing. There are different types of licenses (e.g., regular vendor’s license, transient vendor’s license), depending on the nature and location of the sales.

Collection and Remittance

Once registered, businesses must accurately collect the correct combined sales tax rate (state + county permissive tax) at the point of sale. This requires sophisticated point-of-sale systems or e-commerce platforms capable of determining the appropriate rate based on the customer’s shipping address or the sales location. Businesses are then required to remit these collected taxes to the Ohio Department of Taxation on a periodic basis, typically monthly, quarterly, or annually, depending on their sales volume. Timely and accurate filing is crucial.

Record Keeping

Meticulous record-keeping is non-negotiable. Businesses must maintain detailed records of all sales, both taxable and exempt, including copies of exemption certificates for non-taxed sales for resale or other qualifying exemptions. These records are vital for demonstrating compliance during potential audits.

Sales Tax Software and Tools

Given the complexity of varying rates, nexus rules, and filing requirements, many businesses, particularly those operating across multiple states or with high transaction volumes, leverage specialized sales tax software. These financial tools can automate rate calculations, manage exemption certificates, track nexus, and even prepare and file returns, significantly reducing the administrative burden and risk of error.

Audits and Penalties

The Ohio Department of Taxation conducts audits to ensure compliance. If discrepancies are found, businesses can face significant penalties, interest charges, and assessments for uncollected or underpaid taxes. Non-compliance can be costly, highlighting the importance of understanding and adhering to Ohio’s sales tax regulations.

Navigating Sales Tax in the Digital Age

The proliferation of e-commerce and digital services has continuously reshaped sales tax policy. Ohio, like many states, has adapted its laws to capture revenue from the burgeoning digital economy, creating new considerations for businesses and consumers.

The Impact of E-commerce and Remote Sellers

The Wayfair decision fundamentally changed sales tax for online retailers. No longer could out-of-state businesses simply avoid collecting sales tax if they lacked a physical presence. This meant that many online merchants who previously didn’t charge Ohio sales tax are now obligated to do so once they meet Ohio’s economic nexus thresholds. This has leveled the playing field for brick-and-mortar stores but added a significant layer of compliance for remote sellers.

Economic Nexus in Ohio

Ohio established its economic nexus rules following Wayfair. Generally, a remote seller has economic nexus in Ohio if, in the current or preceding calendar year, they have either:

- Gross receipts from sales of tangible personal property or services into Ohio exceeding $100,000, OR

- 200 or more separate transactions for delivery into Ohio.

Once these thresholds are met, the remote seller must register for an Ohio vendor’s license and begin collecting and remitting sales tax on all taxable sales into the state.

Digital Goods and Services

The taxation of digital goods and services remains a complex and evolving area. Ohio’s stance on items like software, streaming services, and digital downloads can depend on the specific nature of the product and how it’s delivered or accessed. For example, while canned software delivered electronically might be taxable as tangible personal property, custom software development services might not be. Businesses dealing in these products must consult specific Ohio tax guidelines or seek professional advice to determine their sales tax obligations.

SaaS and Cloud-Based Services

Software as a Service (SaaS) and other cloud-based services present particular challenges. Often, these are viewed as services rather than the sale of tangible personal property, which could imply exemption. However, some states define these services as taxable, especially if they involve access to software or the performance of a taxable service. Ohio’s treatment of SaaS can depend on the specifics of the subscription agreement and the nature of the service provided. Businesses offering these types of services need to carefully evaluate their taxability under Ohio law.

Key Takeaways and Resources

Navigating Ohio’s sales tax landscape requires ongoing attention and a proactive approach. Both consumers and businesses benefit from a clear understanding of the rules and responsibilities.

Staying Compliant

For businesses, compliance is not a one-time task but an ongoing commitment. This includes continuously monitoring sales volume for nexus thresholds, ensuring correct rates are applied, maintaining accurate records, and filing returns on time. Ignorance of the law is not a valid defense during an audit, making proactive education and system implementation critical.

Consulting Experts

Given the complexity of sales tax, particularly for businesses with multi-state operations, significant sales volumes, or unique product offerings (like digital goods), consulting with qualified tax professionals or accountants specializing in sales tax can be invaluable. These experts can provide tailored advice, assist with registration, ensure correct nexus determination, and help implement robust compliance strategies.

Official Resources

The Ohio Department of Taxation is the ultimate authority and primary resource for all sales tax-related information. Their website offers:

- Current sales tax rates by county.

- Forms for vendor’s license applications and sales tax returns.

- Guidance documents and FAQs on taxable goods and services, exemptions, and use tax.

- Information on economic nexus and remote seller obligations.

Regularly consulting these official resources ensures that businesses and individuals remain up-to-date with any changes in legislation or policy, thereby fostering compliance and mitigating financial risk.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.