In the intricate world of personal finance, few concepts hold as much weight and potential impact as the mortgage. For most individuals, acquiring a home represents the single largest financial transaction of their lives, and the mortgage is the linchpin that makes this dream a reality. Far from being a mere loan, a mortgage is a sophisticated financial instrument, a binding contract, and a strategic financial commitment that demands careful understanding. It’s the bridge between aspiring homeowners and the property they wish to possess, enabling the purchase of real estate without requiring the full cash amount upfront. This deep dive will unravel the complexities of what a mortgage entails, exploring its fundamental mechanics, diverse forms, the meticulous process of obtaining one, and the crucial financial factors that shape its long-term implications. Understanding a mortgage is not just about securing a loan; it’s about making an informed investment in your future and building a cornerstone of your personal wealth.

The Fundamentals of Mortgage Lending

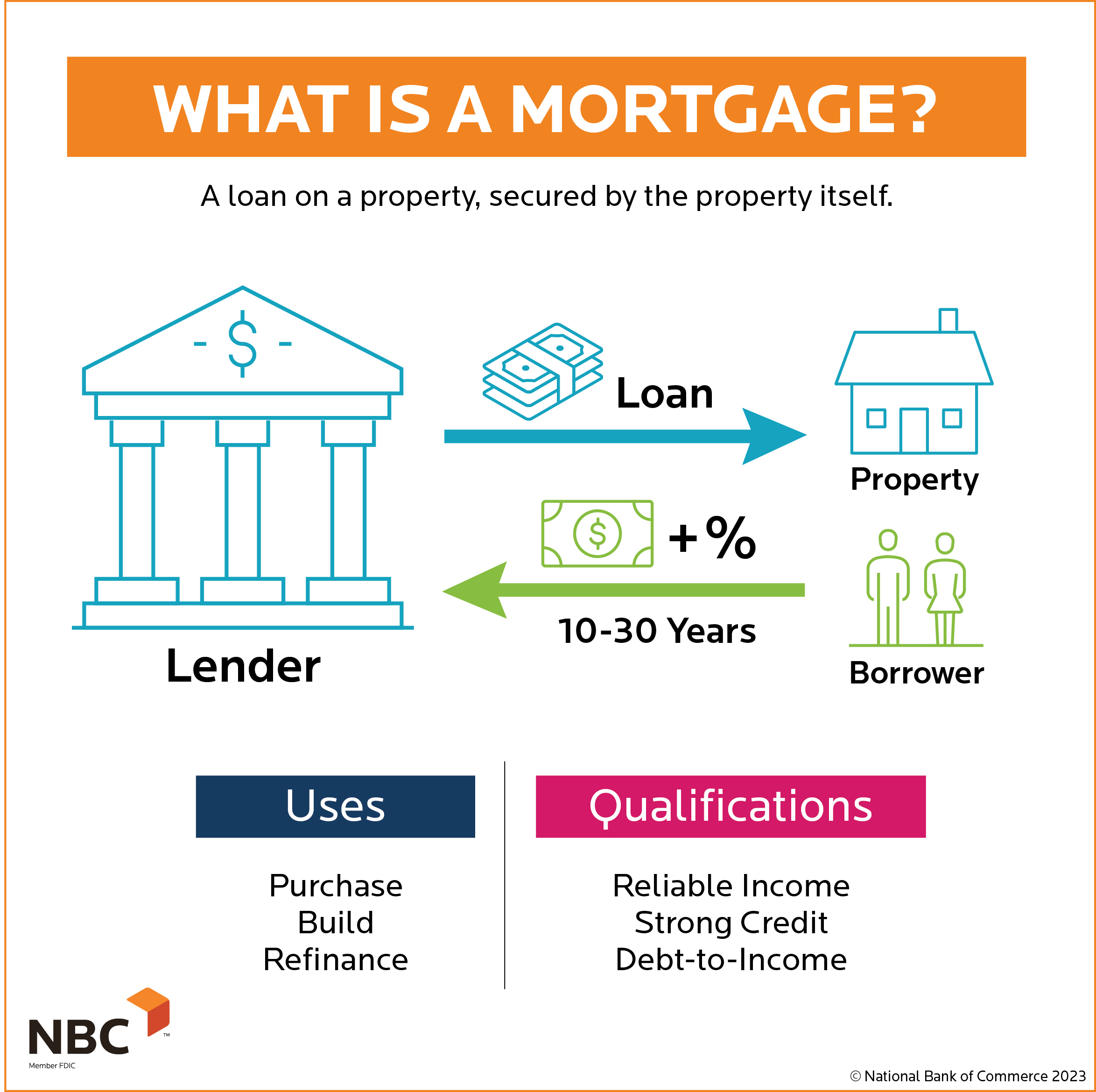

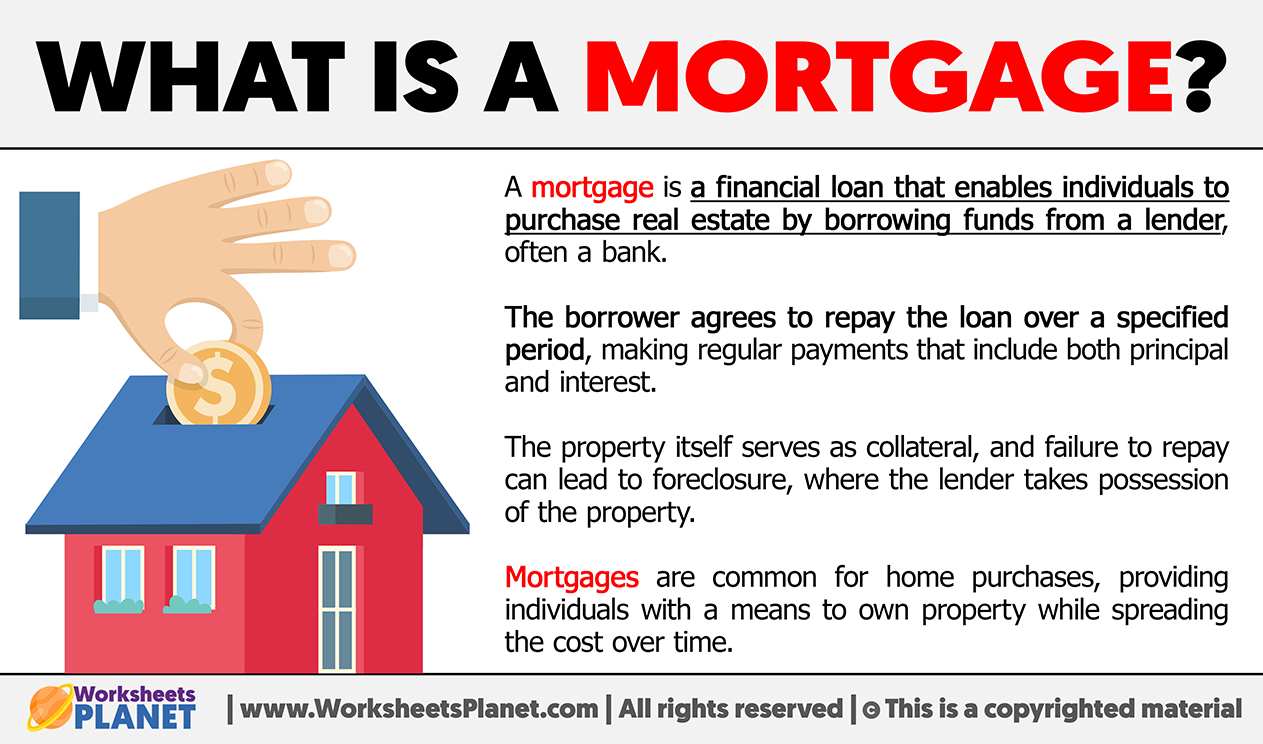

At its core, a mortgage is a loan secured by real estate. When you take out a mortgage, you’re borrowing a substantial sum of money from a financial institution (the lender) to purchase a home or other property. In exchange, the property itself serves as collateral, meaning the lender has a legal claim to it if you fail to repay the loan as agreed. This security is what allows lenders to offer large sums of money over extended periods, typically 15 to 30 years.

Defining the Mortgage Agreement

The mortgage agreement is a legally binding contract between the borrower (the homeowner) and the lender (a bank, credit union, or mortgage company). It outlines the terms of the loan, including the principal amount borrowed, the interest rate, the repayment schedule, and the lender’s rights if the borrower defaults. The agreement essentially grants the lender a lien on the property, which is a legal right to possess and sell the property if the borrower fails to make payments. Once the loan is fully repaid, the lien is removed, and the borrower holds clear title to the property.

Key Elements of a Mortgage Loan

Understanding the components of a mortgage is crucial for any prospective homeowner. These elements collectively determine the total cost of the loan and the structure of your monthly payments.

- Principal: This is the original amount of money you borrow to purchase the home. Every payment you make chipping away at the principal reduces your outstanding debt.

- Interest: This is the cost of borrowing the principal, expressed as a percentage rate. Interest is a significant portion of your early mortgage payments and is how lenders make a profit.

- Term: The loan term is the duration over which you agree to repay the mortgage, commonly 15 or 30 years. A shorter term typically means higher monthly payments but less interest paid over the life of the loan, while a longer term offers lower monthly payments but accrues more interest overall.

- Down Payment: This is the initial amount of money you pay upfront towards the purchase price of the home. A larger down payment reduces the amount you need to borrow, potentially leading to lower interest rates and smaller monthly payments.

- Escrow: Many mortgages include an escrow account, managed by the lender, which collects a portion of your monthly payment to cover property taxes and homeowner’s insurance premiums. This ensures these crucial expenses are paid on time and prevents homeowners from facing large lump-sum bills.

Understanding Amortization

Amortization is the process of paying off a loan with a fixed repayment schedule in regular installments over a period of time. For a mortgage, this means that early payments are heavily weighted towards interest, with only a small portion going towards the principal. As the loan matures, a greater percentage of each payment is applied to the principal, accelerating the equity you build in your home. An amortization schedule provides a clear breakdown of how each payment contributes to reducing both the interest owed and the principal balance over the life of the loan.

Navigating the Diverse Landscape of Mortgage Types

The mortgage market is not a one-size-fits-all environment. Lenders offer a variety of mortgage products, each designed to cater to different financial situations, risk tolerances, and homeownership goals. Choosing the right type of mortgage is a critical decision that can significantly impact your financial well-being for decades.

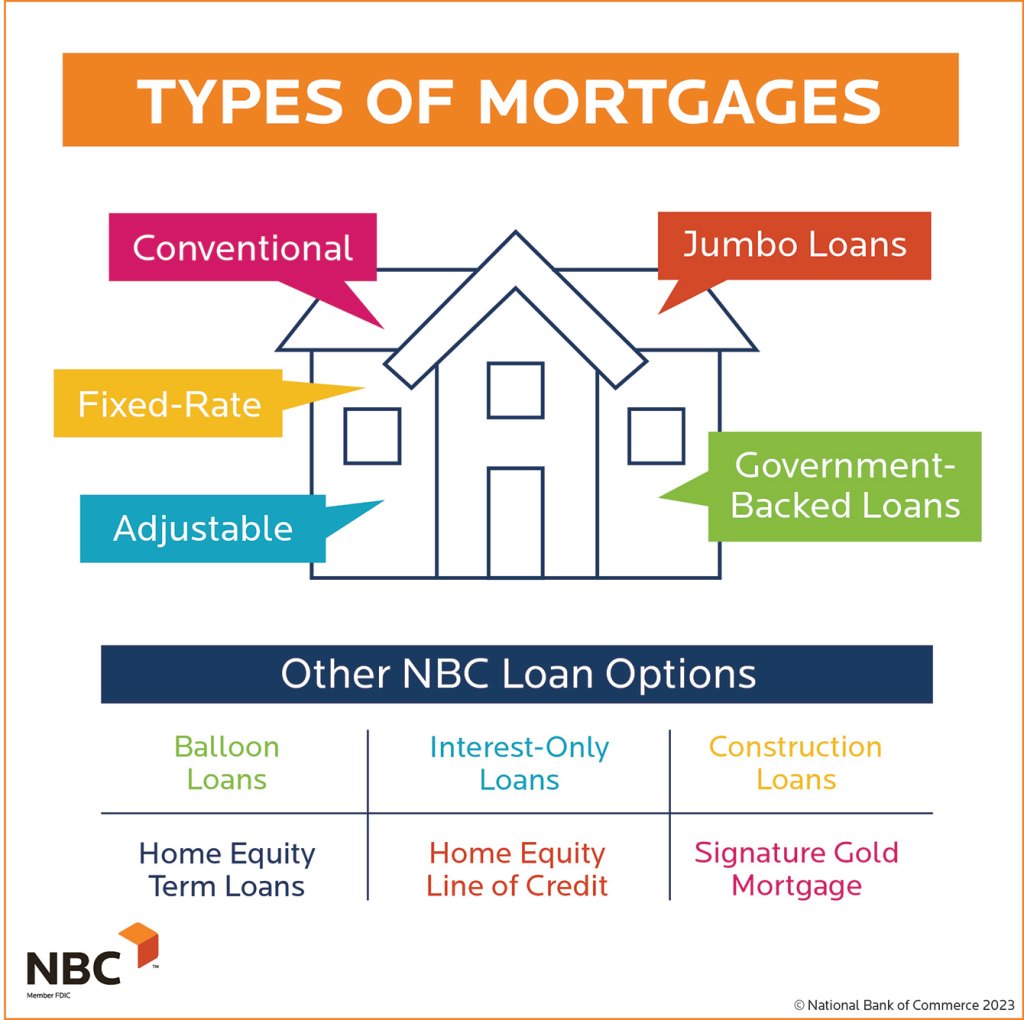

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

These are the two fundamental categories of mortgages, differing primarily in how their interest rates are determined over time.

- Fixed-Rate Mortgage: With a fixed-rate mortgage, the interest rate remains constant for the entire duration of the loan. This provides predictability and stability, as your principal and interest payment will never change. It’s an excellent choice for borrowers who prefer consistent monthly expenses and are concerned about potential interest rate increases in the future.

- Adjustable-Rate Mortgage (ARM): ARMs feature an interest rate that is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a chosen market index, plus a margin. While ARMs often offer lower initial interest rates, the potential for future rate increases (and thus higher monthly payments) introduces a degree of risk. They can be suitable for borrowers who plan to sell or refinance before the fixed-rate period ends, or those who anticipate their income will rise significantly.

Government-Backed Loans: FHA, VA, and USDA

These mortgage programs are insured or guaranteed by federal agencies, making homeownership more accessible to specific groups of borrowers, often with more lenient qualification requirements.

- FHA Loans: Insured by the Federal Housing Administration (FHA), these loans are popular for first-time homebuyers or those with lower credit scores. They require a smaller down payment (as low as 3.5%) but typically involve mortgage insurance premiums (MIP) for the life of the loan.

- VA Loans: Guaranteed by the Department of Veterans Affairs, VA loans are available to eligible service members, veterans, and surviving spouses. They are highly advantageous as they often require no down payment and no private mortgage insurance (PMI).

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed to promote homeownership in eligible rural and suburban areas. They offer 100% financing (no down payment) for qualified low- to moderate-income borrowers, with income and property location restrictions.

Conventional Mortgages: The Most Common Path

Conventional mortgages are not insured or guaranteed by a government agency. They are the most common type of home loan and generally require good credit scores and a down payment of at least 3-5%, though 20% is ideal to avoid private mortgage insurance (PMI).

- Private Mortgage Insurance (PMI): If your down payment is less than 20% of the home’s purchase price, lenders typically require you to pay PMI. This protects the lender in case you default on the loan. PMI payments are usually added to your monthly mortgage bill and can often be canceled once you reach 20% equity in your home.

Specialized Mortgages: Jumbo and Interest-Only

Beyond the mainstream options, some mortgages cater to unique financial situations or property types.

- Jumbo Mortgages: These loans exceed the “conforming loan limits” set by government-sponsored enterprises like Fannie Mae and Freddie Mac. They are used for high-value properties and typically have stricter underwriting requirements and may carry slightly higher interest rates.

- Interest-Only Mortgages: With an interest-only mortgage, the borrower pays only the interest on the principal balance for a specified period (e.g., 5-10 years). After this period, the payments typically increase significantly as the borrower begins to pay down the principal. These are often used by investors or those expecting a substantial increase in income.

The Mortgage Application Journey: From Pre-Approval to Closing

Securing a mortgage is a multi-step process that requires thorough documentation, careful review, and several key milestones. Navigating this journey effectively is crucial for a smooth path to homeownership.

The Importance of Pre-Approval

Before you even start seriously looking at homes, obtaining a mortgage pre-approval is a vital first step. A pre-approval letter from a lender states the maximum amount you’re qualified to borrow, based on a preliminary review of your financial information (credit, income, assets). This not only helps you understand your budget and narrow your home search but also demonstrates to sellers that you are a serious and qualified buyer, strengthening your offer in a competitive market. It’s different from pre-qualification, which is a less rigorous estimate of what you might be able to borrow.

Documentation and Underwriting

Once you find a home and your offer is accepted, the rigorous underwriting process begins. The lender will request extensive documentation to verify your financial stability and ability to repay the loan. This typically includes:

- Income verification: Pay stubs, W-2 forms, tax returns for the past two years, profit and loss statements for self-employed individuals.

- Asset verification: Bank statements, investment account statements to show down payment funds and reserves.

- Debt verification: Credit reports, loan statements for existing debts.

- Employment history: Verification of employment, often directly from your employer.

Underwriters meticulously review all this information to assess the risk of lending to you. They scrutinize your credit history, debt-to-income (DTI) ratio, and overall financial health to ensure you meet the lender’s criteria.

Appraisal and Inspection: Valuing Your Investment

Two crucial steps protect both you and the lender by evaluating the property itself:

- Appraisal: The lender will order an independent property appraisal to determine the home’s fair market value. This ensures that the loan amount is justified by the property’s worth and prevents the lender from lending more than the collateral is actually valued at. If the appraisal comes in lower than the purchase price, it can impact the loan amount the lender is willing to provide.

- Inspection: While not strictly required by lenders, a home inspection is highly recommended for buyers. An inspector thoroughly examines the property’s condition, identifying any potential issues with the foundation, roof, plumbing, electrical systems, and other components. This allows you to negotiate repairs with the seller or walk away from the deal if significant problems are found, protecting your investment.

The Closing Process: Finalizing Your Homeownership Dream

Closing, also known as settlement, is the final stage where all parties meet to sign the legal documents and officially transfer ownership of the property. This typically involves:

- Signing numerous legal documents: Including the promissory note (your promise to repay the loan) and the mortgage or deed of trust (the lien on the property).

- Paying closing costs: These are fees associated with the mortgage transaction, such as origination fees, appraisal fees, title insurance, attorney fees, and recording fees. They typically range from 2-5% of the loan amount.

- Transfer of funds: The down payment and closing costs are paid, and the loan funds are disbursed.

- Receiving the keys: Once all documents are signed and funds are disbursed, you officially become the homeowner.

Factors Influencing Your Mortgage and Long-Term Costs

The specific terms of your mortgage – primarily the interest rate – are not arbitrary. They are a direct reflection of several key financial indicators, both personal and market-driven. Understanding these factors empowers you to position yourself for the most favorable loan terms.

The Crucial Role of Your Credit Score

Your credit score is arguably the most significant personal factor influencing your mortgage interest rate and eligibility. Lenders use it as a primary indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score (generally above 740-760 for the best rates) signals lower risk to lenders, translating into access to lower interest rates and a wider range of loan products. Conversely, a lower score will result in higher interest rates, if a loan is offered at all, to compensate the lender for the increased risk.

Debt-to-Income (DTI) Ratio and Loan Affordability

Your Debt-to-Income (DTI) ratio is another critical metric that lenders use to assess your ability to manage monthly mortgage payments. It’s calculated by dividing your total monthly debt payments (including the proposed mortgage payment) by your gross monthly income. Lenders typically look for a DTI ratio below 43%, though this can vary by loan program and lender. A lower DTI indicates that you have sufficient income relative to your debt obligations, making you a less risky borrower.

Market Interest Rates and Economic Indicators

Beyond your personal finances, broader economic conditions heavily influence mortgage interest rates. Factors such as inflation, the Federal Reserve’s monetary policy, bond market performance (especially U.S. Treasury yields), and general economic growth or contraction all play a role. When the economy is strong and inflation is a concern, the Fed may raise benchmark interest rates, which often leads to higher mortgage rates. Conversely, during economic downturns, rates may be lowered to stimulate borrowing and spending.

The Down Payment and Loan-to-Value (LTV) Ratio

The size of your down payment directly impacts your Loan-to-Value (LTV) ratio, which is the percentage of the property’s value that you are borrowing. A larger down payment means a lower LTV ratio, which reduces the risk for lenders. Lenders often offer better interest rates to borrowers with lower LTVs. Furthermore, a down payment of 20% or more allows you to avoid Private Mortgage Insurance (PMI) on conventional loans, saving you significant money over time.

Hidden Costs and Fees: Beyond the Principal and Interest

While the principal and interest make up the core of your monthly mortgage payment, it’s essential to account for other costs associated with homeownership and the mortgage itself.

- Closing Costs: As mentioned, these are one-time fees paid at closing, including loan origination fees, appraisal fees, title insurance, legal fees, and recording fees.

- Property Taxes: These are recurring taxes levied by local government authorities based on your property’s assessed value. They are often collected via your escrow account.

- Homeowner’s Insurance: Required by lenders, this insurance protects your home and belongings from damage due to events like fire, theft, or natural disasters. It’s also often collected via escrow.

- Private Mortgage Insurance (PMI): If applicable, this is a monthly premium paid until you reach sufficient equity in your home.

Failing to budget for these additional costs can strain your finances and lead to unexpected difficulties.

Strategic Considerations for Mortgage Seekers

Embarking on the journey to homeownership is a significant financial undertaking. Approaching it strategically, with careful planning and an understanding of your options, can lead to a more financially sound and less stressful experience.

Building a Strong Financial Foundation

Before even thinking about a mortgage, focus on strengthening your personal financial health. This includes:

- Improving your credit score: Pay bills on time, reduce credit card balances, and avoid opening new credit accounts unnecessarily.

- Saving for a substantial down payment: The more you put down, the less you borrow, potentially leading to better rates and lower monthly payments.

- Managing existing debt: Lowering your debt-to-income ratio makes you a more attractive borrower.

- Building an emergency fund: Having 3-6 months of living expenses saved provides a crucial buffer for unexpected costs of homeownership or life events.

Shopping Around for the Best Rates and Terms

Do not settle for the first offer you receive. Mortgage rates and terms can vary significantly between different lenders. Contact multiple banks, credit unions, and mortgage brokers to compare offers. Pay close attention to not only the interest rate but also the Annual Percentage Rate (APR), which includes fees and other costs, giving you a more accurate picture of the total cost of the loan. Even a small difference in interest rate can save you tens of thousands of dollars over the life of a 30-year mortgage.

Understanding Your Long-Term Financial Commitment

A mortgage is a long-term commitment. It’s crucial to understand not just the monthly payment but also how it fits into your overall budget, considering property taxes, insurance, potential HOA fees, and maintenance costs. Use online mortgage calculators to project different scenarios, factoring in various interest rates and loan terms. Ensure that your housing expenses are comfortably within your means, allowing room for other financial goals like saving for retirement, education, and unexpected expenses.

When Refinancing Makes Sense

Even after you’ve secured a mortgage, your financial journey isn’t over. Refinancing involves replacing your existing mortgage with a new one, often to take advantage of lower interest rates, shorten the loan term, or convert an adjustable-rate mortgage to a fixed-rate one. A “cash-out” refinance also allows you to borrow against your home’s equity. While refinancing can offer significant benefits, it also involves closing costs, so it’s important to analyze whether the savings outweigh these upfront expenses.

In conclusion, a mortgage is more than just a financial product; it’s a gateway to homeownership and a cornerstone of personal wealth building. By understanding its fundamental principles, the various types available, the process of obtaining one, and the factors that influence its cost, individuals can make informed decisions that align with their financial goals and secure their future. While the process can seem daunting, a strategic approach, coupled with diligent research and preparation, can transform the complex world of mortgages into a clear path towards achieving the dream of owning a home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.