Understanding Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) is crucial for anyone involved in business finance, investing, or even just trying to grasp the financial health of a company. It’s a widely used profitability metric that offers a glimpse into a company’s operational performance, stripping away certain financial and accounting decisions to provide a clearer picture of its core earnings power. While not a Generally Accepted Accounting Principles (GAAP) measure, its prevalence in financial analysis, valuation, and lending agreements makes it an indispensable tool.

Understanding the Components of EBITDA

At its core, EBITDA is a modification of net income. It starts with a company’s net profit and then adds back certain expenses that are either non-operational or non-cash. Let’s break down each component to understand its significance.

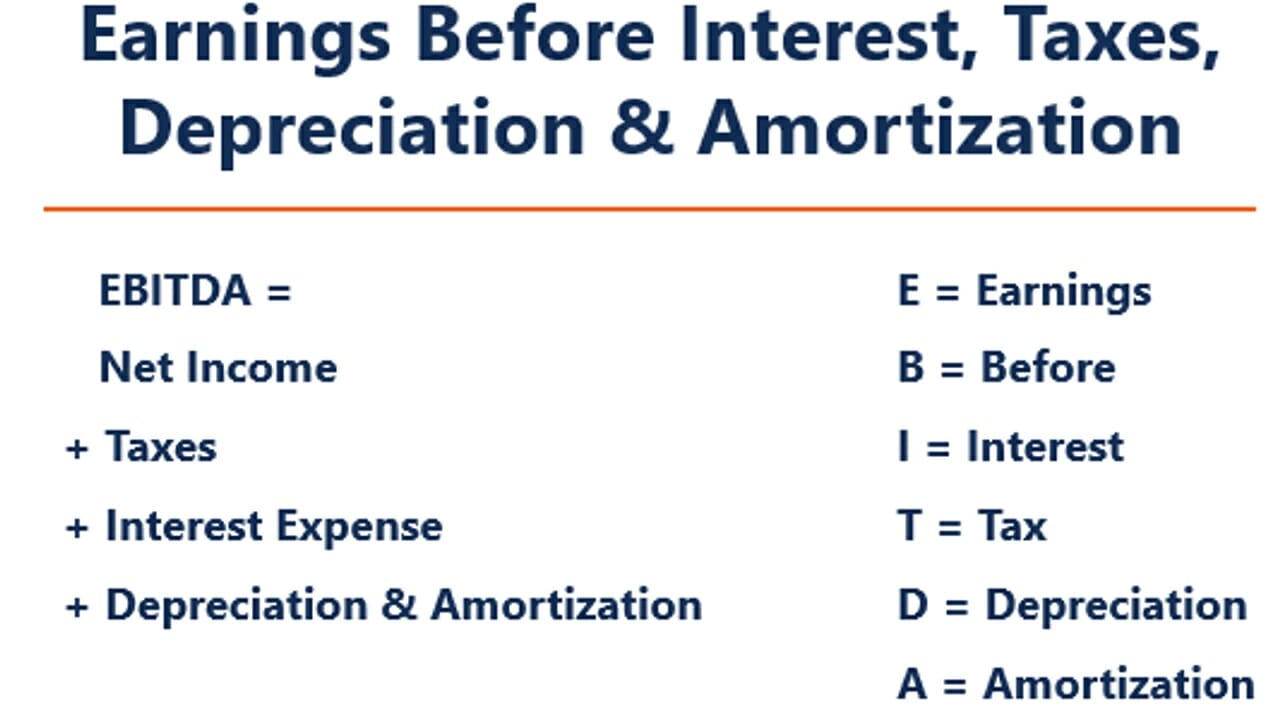

Earnings Before Interest, Taxes, Depreciation, and Amortization

- Earnings: This typically refers to operating income or net income before the specific add-backs. It represents the profit generated from a company’s primary business activities.

- Interest: This refers to the cost of a company’s debt financing. By adding back interest expense, EBITDA removes the impact of how a company is financed. This is important because two companies with identical operational performance might have vastly different interest expenses due to their capital structures (e.g., one with significant debt, another with very little). Excluding interest allows for a more apples-to-apples comparison of their operational profitability.

- Taxes: Corporate income taxes are also added back. Similar to interest, tax expenses can vary significantly based on a company’s jurisdiction, tax planning strategies, and tax credits. By excluding taxes, EBITDA aims to present a picture of profitability before the impact of tax policies, allowing for a comparison of operational performance across different tax environments.

- Depreciation: This is a non-cash expense that represents the gradual decrease in the value of tangible assets (like machinery, buildings, and vehicles) over their useful lives. Depreciation is an accounting method to allocate the cost of an asset over time, but it doesn’t involve an actual outflow of cash in the current period. Adding it back provides a better sense of the cash generated by the business operations before considering the wear and tear on its physical assets.

- Amortization: This is similar to depreciation but applies to intangible assets (like patents, copyrights, and goodwill). It’s also a non-cash expense that spreads the cost of an intangible asset over its useful life. Like depreciation, adding back amortization helps to isolate the operational cash flow by removing non-cash charges related to the depletion of intangible assets.

Why is EBITDA Important in Business Finance?

EBITDA serves multiple critical functions within the realm of business finance, offering a standardized lens through which to evaluate a company’s performance and potential. Its ability to smooth out certain financial and accounting variables makes it particularly useful for comparison and analysis.

Operational Performance Evaluation

EBITDA is often considered a proxy for a company’s operational cash flow or its ability to generate cash from its core business activities. By removing the effects of financing decisions (interest) and accounting treatments (depreciation and amortization) that don’t involve current cash outlays, as well as the impact of taxes, it provides a cleaner view of how efficiently the company’s operations are generating profits. This makes it an excellent metric for comparing the underlying performance of companies within the same industry, even if they have different levels of debt, different tax situations, or different asset bases.

For example, consider two manufacturing companies. Company A has a lot of older machinery that is heavily depreciated, while Company B has recently invested in new, state-of-the-art equipment. Without accounting for depreciation, Company A might appear more profitable on a net income basis due to lower depreciation charges. However, EBITDA would add back depreciation for both companies, providing a more comparable view of their operational efficiency in producing goods, irrespective of their fixed asset lifecycles.

Debt Service Capacity Assessment

Lenders frequently use EBITDA to assess a company’s ability to service its debt obligations. This is because EBITDA is a good indicator of a company’s cash-generating ability, which is ultimately what pays down debt and its associated interest. Many loan agreements, particularly those for leveraged buyouts (LBOs) or corporate bonds, include covenants tied to EBITDA.

A common metric used by lenders is the Debt-to-EBITDA ratio, which measures how many years it would take for a company to repay its debt if it dedicated all of its EBITDA to debt reduction. A lower ratio generally indicates a stronger ability to repay debt and a lower risk for lenders. For instance, a company with a Debt-to-EBITDA ratio of 3x means it would theoretically take three years of its current EBITDA to pay off its total debt. This ratio is a critical factor in determining loan terms, interest rates, and the overall availability of credit.

Valuation Purposes

EBITDA is also a key input in various business valuation methods, most notably the Enterprise Value (EV) to EBITDA multiple. This multiple is widely used to compare the valuations of companies within the same industry. Enterprise Value represents the total value of a company, including its debt and equity, minus any cash. Dividing this by EBITDA provides a multiple that can be used to assess whether a company is overvalued or undervalued relative to its peers.

This method is particularly useful for valuing mature, stable companies where cash flow generation is a primary driver of value. It allows investors to quickly gauge the market’s perception of a company’s worth based on its operational profitability, abstracting from the capital structure and tax complexities that can distort other valuation metrics like Price-to-Earnings (P/E) ratios. When acquiring a business, EBITDA multiples are often the first benchmark used to establish a preliminary purchase price range.

Limitations and Criticisms of EBITDA

While EBITDA is a valuable tool, it’s not without its flaws and is often subject to criticism. Understanding these limitations is crucial for a balanced financial analysis.

Ignores Capital Expenditures (CapEx)

One of the most significant criticisms of EBITDA is that it does not account for capital expenditures (CapEx). CapEx represents the money a company spends on acquiring or upgrading its physical assets, such as property, plant, and equipment. These are necessary investments for maintaining and growing a business, and they represent a real cash outflow.

Since EBITDA adds back depreciation, which is a non-cash expense related to the wear and tear of assets, it doesn’t reflect the actual cash needed to replace or maintain those assets. A company might have high EBITDA, suggesting strong operational profitability, but if it’s not reinvesting sufficiently in its assets, its long-term sustainability could be at risk. This is where metrics like Free Cash Flow (FCF), which subtracts CapEx from operating cash flow, become more important for understanding the true cash available to the business and its stakeholders.

Doesn’t Reflect Financing Costs

As mentioned earlier, EBITDA adds back interest expense, meaning it doesn’t show how much cash is consumed by servicing debt. Companies with high levels of debt will have significant interest payments, which directly impact their ability to generate free cash flow. Relying solely on EBITDA can mask the financial strain placed on a company by its debt obligations. This is particularly problematic when evaluating companies with different leverage ratios, as a high-debt company might appear more profitable on an EBITDA basis than a lower-debt one, even if its net income and available cash are lower after interest payments.

Taxes are Essential

While adding back taxes might facilitate comparisons across different tax jurisdictions, it’s important to remember that taxes are a real and unavoidable cost of doing business. A company’s tax burden can significantly impact its net profitability and the cash available for reinvestment or distribution to shareholders. For a true understanding of a company’s bottom line and its ability to retain earnings, net income remains the ultimate measure.

Potential for Manipulation

Because EBITDA is a non-GAAP measure, companies have some flexibility in how they present it. While there are standard practices, there’s always a risk that management could selectively present EBITDA in a way that paints a more favorable picture. This can include using aggressive accounting policies or focusing on adjusted EBITDA figures that may exclude a broader range of expenses deemed “non-recurring” or “unusual,” which can sometimes obscure underlying operational weaknesses. Investors and analysts must always scrutinize the adjustments made to arrive at an EBITDA figure.

Calculating and Using EBITDA

Calculating EBITDA is straightforward, and its application in financial analysis is widespread. Understanding how to derive it and what it tells you is key to making informed financial decisions.

The Formula for EBITDA

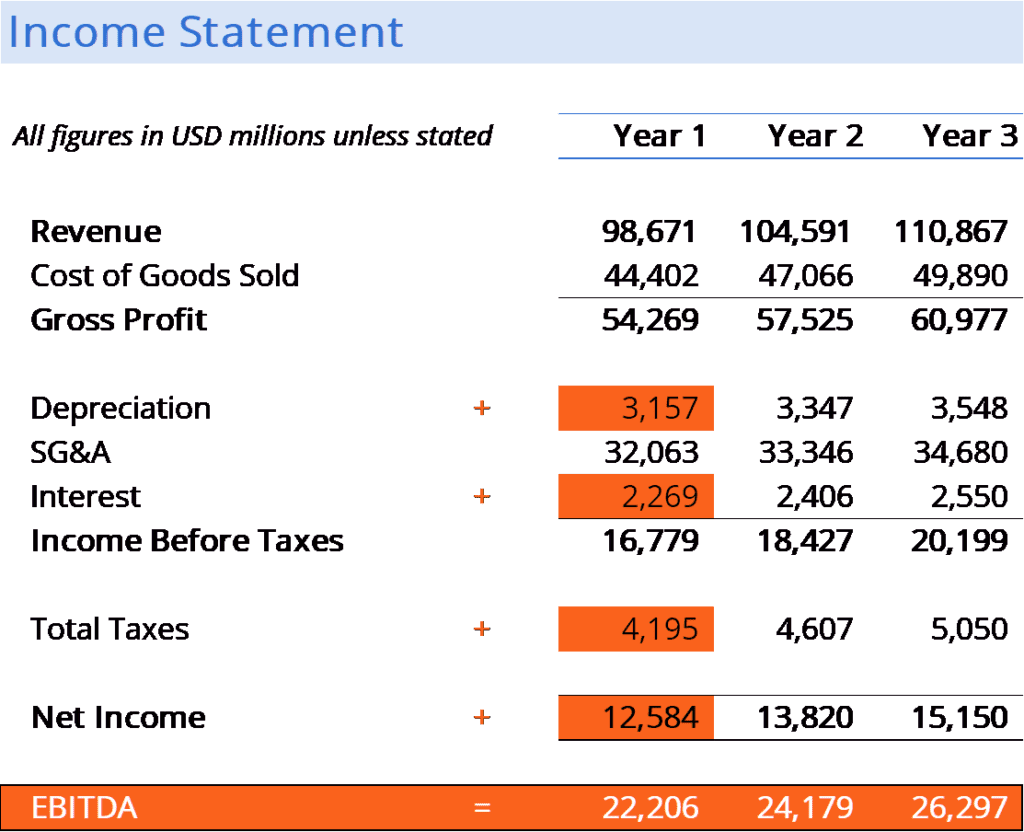

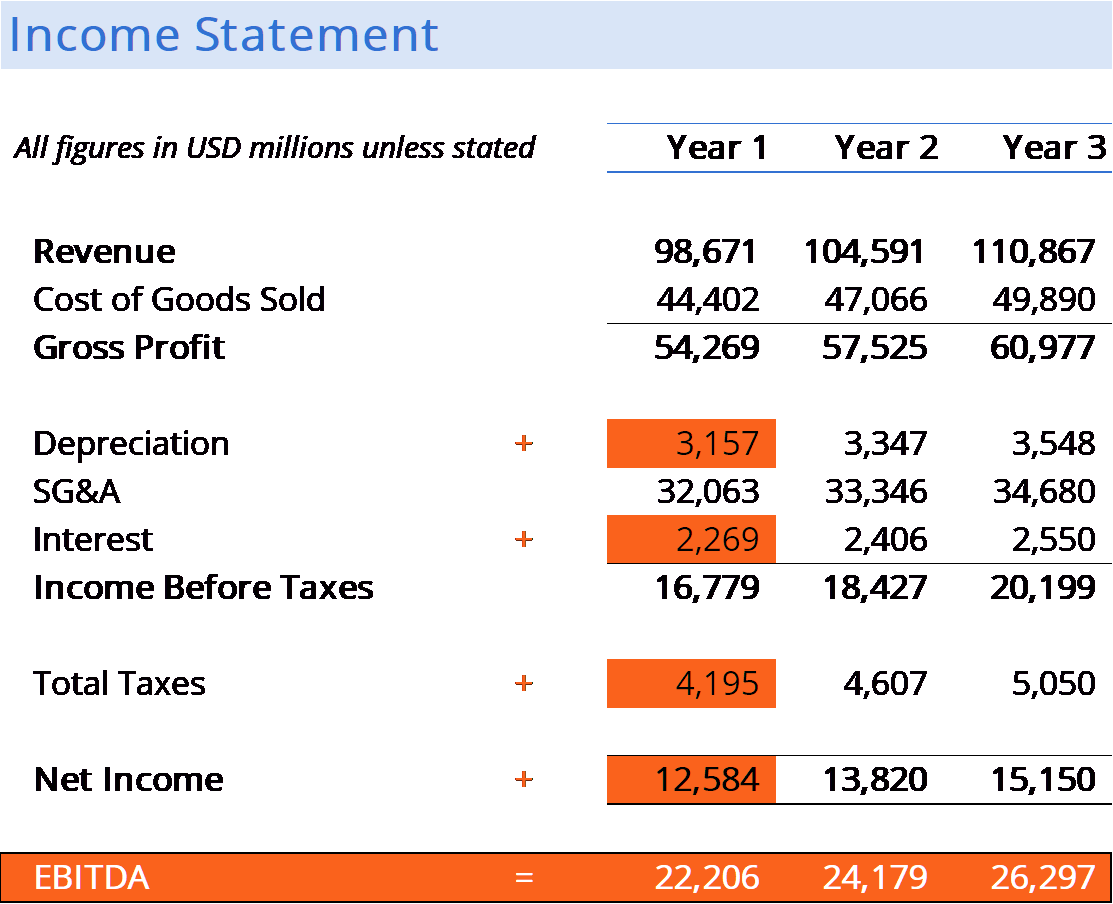

The most common way to calculate EBITDA is to start with a company’s net income and add back interest, taxes, depreciation, and amortization.

EBITDA = Net Income + Interest Expense + Tax Expense + Depreciation Expense + Amortization Expense

Alternatively, you can derive it from operating income:

EBITDA = Operating Income (or EBIT) + Depreciation Expense + Amortization Expense

Where EBIT (Earnings Before Interest and Taxes) is calculated as:

EBIT = Net Income + Interest Expense + Tax Expense

It’s important to consult a company’s financial statements, specifically the income statement, to find these figures. Depreciation and amortization are typically line items within the income statement or disclosed in the notes to the financial statements.

Applications in Financial Analysis

Beyond the core uses in evaluating operational performance, debt service capacity, and valuation, EBITDA finds its way into several other areas of financial analysis:

- Mergers and Acquisitions (M&A): EBITDA multiples are a standard starting point for valuing target companies in M&A transactions. Buyers and sellers often use EBITDA as a benchmark to establish an initial price range.

- Lending Covenants: As previously mentioned, many loan agreements contain covenants tied to EBITDA. These covenants protect lenders by ensuring the borrower maintains a certain level of profitability and cash flow to service the debt. Violating these covenants can trigger loan defaults.

- Performance Benchmarking: Investors and analysts use EBITDA to compare the operational efficiency of companies across different industries and geographies, assuming they are in similar stages of their business cycle and have comparable business models.

- Management Performance Metrics: Some companies use EBITDA or adjusted EBITDA as a performance metric for their management teams, aligning executive compensation with operational profitability.

In conclusion, EBITDA is a powerful financial metric that provides a valuable, albeit incomplete, picture of a company’s profitability and operational strength. While it simplifies analysis by removing the impact of financing, taxes, and non-cash accounting charges, its limitations necessitate its use in conjunction with other financial metrics to form a comprehensive understanding of a company’s financial health and future prospects.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.