For many aspiring homeowners, the path to the front door begins with a mortgage application. However, the mortgage landscape is not one-size-fits-all. Navigating the differences between an FHA loan and a conventional loan is arguably the most critical financial decision a buyer will make before committing to a purchase. While both products serve the same primary goal—financing the acquisition of a property—they operate under fundamentally different rules, qualification requirements, and long-term cost structures.

The Structural Divide: Understanding the Basics

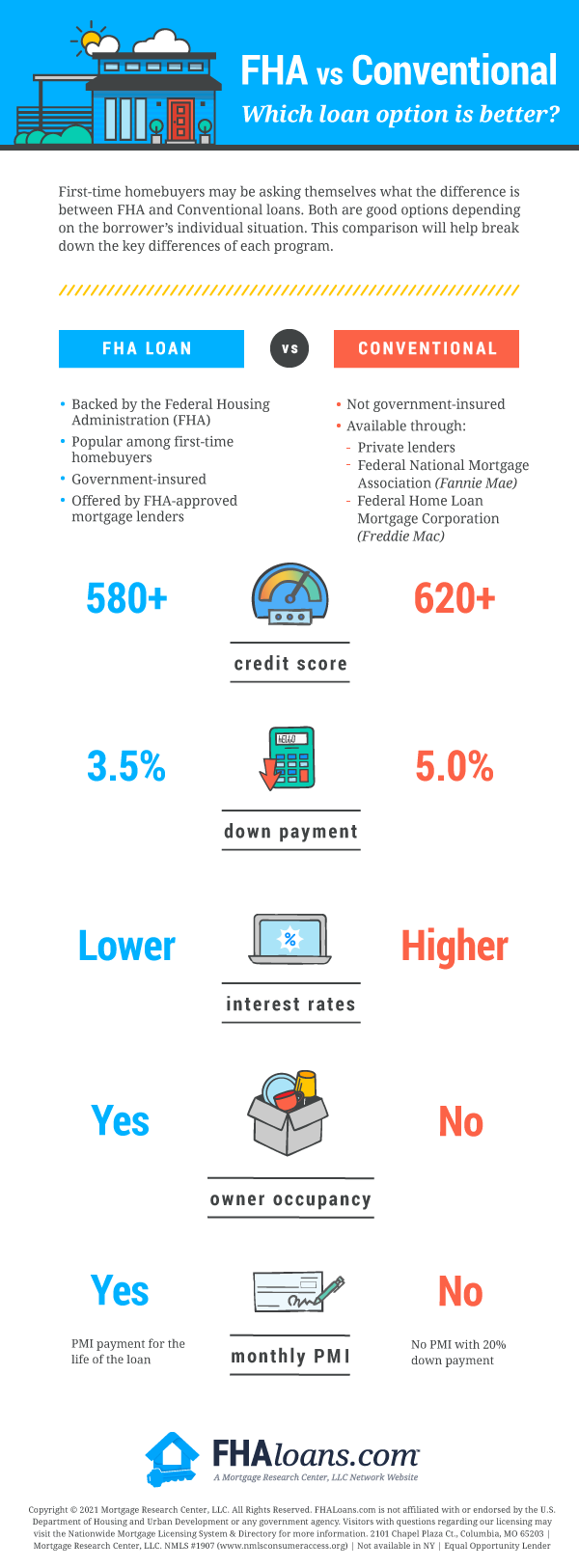

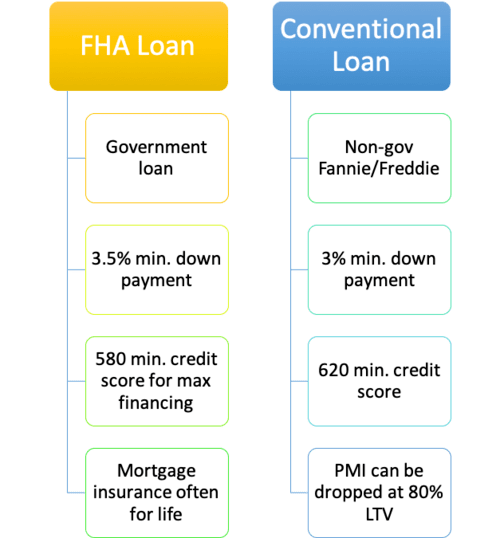

At the core of the choice between an FHA loan and a conventional loan lies a distinction in backing. A conventional loan is not insured by the federal government. Instead, these loans are originated by private lenders, such as banks, credit unions, and mortgage companies, and are typically governed by standards set by Fannie Mae and Freddie Mac. Because these loans carry more risk for the lender, they are designed primarily for borrowers with solid credit histories and stable financial profiles.

In contrast, an FHA loan is insured by the Federal Housing Administration, which is a division of the U.S. Department of Housing and Urban Development (HUD). Because the government guarantees the loan against loss in the event of default, lenders are willing to extend credit to borrowers who might not meet the stringent criteria of conventional underwriting. This insurance acts as a safety net, allowing for more flexible qualification guidelines.

Conventional Loans: The Standard for Financial Health

Conventional loans are often the preferred route for borrowers with strong credit scores and sufficient liquid assets for a down payment. They are viewed as the “standard” of the industry, offering a variety of terms and often lower long-term costs for those who qualify.

FHA Loans: The Gateway to Homeownership

FHA loans serve as a vital tool for first-time buyers, individuals with lower credit scores, or those who have faced past financial challenges. By lowering the barriers to entry, the FHA program aims to make homeownership accessible to a wider demographic of the American public.

Qualification Standards: Credit and Down Payment

The most immediate difference you will encounter as an applicant involves the threshold for entry. Qualifying for a mortgage is essentially a balancing act between your creditworthiness, your debt-to-income (DTI) ratio, and the size of your down payment.

Credit Score Thresholds

Conventional mortgages generally require a minimum credit score of 620. However, those aiming for the most competitive interest rates typically need a score in the mid-700s or higher. A higher credit score signifies lower risk to the lender, which translates into lower mortgage rates and more favorable terms.

FHA loans are significantly more forgiving regarding credit. Borrowers with a credit score as low as 580 can qualify for the program’s maximum financing, which includes the lower down payment option. In some cases, lenders may even consider applicants with scores between 500 and 579, though this usually requires a larger down payment—typically 10%—to compensate for the elevated risk profile.

Down Payment Realities

The disparity in down payment requirements is perhaps the most cited difference between the two products:

- Conventional Loans: While 20% down is the industry benchmark for avoiding private mortgage insurance (PMI), many conventional loan programs allow for down payments as low as 3% for first-time buyers.

- FHA Loans: FHA loans allow for a down payment of just 3.5%. For many buyers, this difference—3.5% versus 3%—is less important than the ability to utilize gift funds from family members or down payment assistance programs, which are frequently more seamlessly integrated into the FHA process.

The Cost of Borrowing: PMI and Mortgage Insurance Premiums

One of the most misunderstood aspects of mortgage financing is the insurance requirement. Insurance is the cost of protecting the lender from the risk that you might default on your loan. The method by which this insurance is applied is a major factor in the long-term affordability of your mortgage.

Private Mortgage Insurance (PMI) on Conventional Loans

If you put down less than 20% on a conventional loan, you will be required to pay PMI. This is a monthly fee added to your mortgage payment. The silver lining is that PMI on a conventional loan is temporary. Once you reach 20% equity in your home—either through paying down the principal or through natural appreciation—you can request the cancellation of the PMI. Eventually, the lender is legally required to drop the insurance once you hit a specific loan-to-value ratio.

Mortgage Insurance Premiums (MIP) on FHA Loans

FHA loans utilize a dual-structured insurance system known as the Mortgage Insurance Premium (MIP). This includes:

- Upfront MIP: A fee equal to 1.75% of the loan amount, which is typically rolled into the total loan balance.

- Annual MIP: A recurring fee added to your monthly mortgage payment.

Unlike conventional PMI, the annual MIP for an FHA loan usually stays with the loan for the duration of its term if you put down less than 10%. If you put down 10% or more, the MIP can be removed after 11 years. For most FHA borrowers, this means that the mortgage insurance is a “sunk cost” that lasts until the loan is refinanced or paid off.

Property Standards and Loan Limits

Beyond the borrower’s personal finances, the property itself plays a role in which loan product you choose.

FHA Appraisal Requirements

FHA appraisals are notably more stringent than conventional ones. Because the government is insuring the loan, it wants to ensure the property meets basic safety, security, and structural integrity standards. An FHA appraiser will look for peeling paint, roof issues, exposed wiring, and other “habitability” concerns. If a home is a “fixer-upper” with significant damage, it may fail an FHA inspection, whereas a conventional lender might be more willing to approve the loan depending on the borrower’s capital.

Loan Limits

Both conventional and FHA loans are subject to maximum borrowing limits, which are adjusted annually based on regional housing prices. Conventional loans generally follow the limits set by the Federal Housing Finance Agency (FHFA), while FHA loan limits are based on the median home price in a specific county. In high-cost areas, FHA limits can be quite generous, allowing buyers to finance properties that might otherwise require a “jumbo” conventional loan.

Making the Final Decision: Which Path is Right?

Choosing between an FHA loan and a conventional loan requires a clear-eyed look at your current financial strategy and your future goals.

If you have a high credit score, a stable income, and the ability to put down at least 5% to 20%, a conventional loan will almost always be the more cost-effective choice in the long run. By avoiding the upfront MIP and eliminating the monthly PMI once your equity grows, you will save thousands of dollars in interest and insurance fees over the life of the loan.

However, if your credit is bruised, your cash reserves are limited, or you are looking for more flexibility in your debt-to-income ratio, the FHA loan remains a powerful and essential financial instrument. It provides a reliable pathway to homeownership for those who would be locked out of the market by stricter conventional underwriting standards.

Ultimately, consult with a mortgage professional who can run the numbers based on your specific situation. By comparing the APR (Annual Percentage Rate), closing costs, and the total cost of mortgage insurance, you can move forward with a financing plan that aligns with your household budget and secures your future as a homeowner.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.