In the landscape of personal finance, few tools spark as much debate and interest as the Indexed Universal Life (IUL) account. Often marketed as a “Swiss Army knife” of financial planning, the IUL is a permanent life insurance policy that combines a death benefit with a cash value component. Unlike traditional term life insurance, which only pays out upon the death of the policyholder, an IUL account offers a living benefit: the ability to build wealth that is tied to market performance without the risk of direct market exposure.

As investors look for ways to diversify their portfolios and mitigate the impact of market volatility, understanding the nuances of an IUL account becomes essential. This guide explores the mechanics, benefits, risks, and strategic applications of IUL accounts within a modern financial framework.

Understanding the Mechanics of an Indexed Universal Life (IUL) Account

An IUL account is a form of permanent life insurance, meaning it covers the insured for their entire life, provided premiums are paid. However, its primary appeal lies in how it handles the “cash value” portion of the policy. When you pay a premium into an IUL, a portion goes toward the cost of insurance (COI) and administrative fees, while the remainder is added to the cash value.

How the Cash Value Accumulates

The cash value in an IUL account does not earn a fixed interest rate. Instead, the insurance company credits interest to the account based on the performance of a specific equity index, such as the S&P 500 or the Nasdaq-100. It is important to note that the money is not actually invested in the stock market; rather, the index serves as a benchmark for the interest credited to the account. This distinction is crucial for understanding the safety profile of the asset.

The Role of Market Indexes and Participation Rates

The amount of interest credited to an IUL account is determined by several factors, most notably the participation rate. If an index grows by 10% and your policy has a 100% participation rate, your account is credited based on that 10% gain. However, if the participation rate is 80%, you would only receive an 8% credit. Some policies offer participation rates over 100%, often in exchange for higher fees or lower caps, allowing for enhanced growth during bullish market years.

Protection Through Floors and Caps

The defining feature of an IUL account is the “floor” and the “cap.” The floor is a guaranteed minimum interest rate, typically 0%. This means that even if the stock market crashes by 20%, your IUL cash value will not lose money due to market performance; it simply earns 0% for that period.

Conversely, the “cap” is the maximum interest rate the insurance company will credit. If the index returns 15% but your policy has a 10% cap, your account will be credited 10%. This trade-off—sacrificing the highest peaks of market returns for total protection against market valleys—is the cornerstone of the IUL’s value proposition.

The Financial Advantages of Using an IUL for Wealth Building

For high-earning individuals and those seeking tax efficiency, the IUL account offers several strategic advantages that traditional brokerage accounts or retirement plans may lack.

Tax-Advantaged Growth and Distributions

One of the most compelling reasons to utilize an IUL is its tax treatment under the Internal Revenue Code (specifically Sections 7702 and 101a). The cash value within an IUL grows tax-deferred. More importantly, policyholders can access this money tax-free through policy loans. Unlike a 401(k) or traditional IRA, where distributions are taxed as ordinary income, or a brokerage account subject to capital gains tax, a properly structured IUL allows for “tax-free retirement income.”

Flexibility in Premiums and Death Benefits

IUL accounts offer a level of flexibility not found in Whole Life insurance. Policyholders can often adjust their premium payments based on their current financial situation. If you have a high-income year, you can “overfund” the policy (up to certain IRS limits) to maximize cash growth. Conversely, during leaner years, you can reduce payments or even allow the accumulated cash value to cover the cost of insurance, keeping the policy in force without out-of-pocket expenses.

Asset Protection and Estate Planning Benefits

In many jurisdictions, the cash value within a life insurance policy is protected from creditors and lawsuits, making it a preferred vehicle for business owners and professionals in high-liability fields. Furthermore, the death benefit is generally passed to beneficiaries tax-free and outside of the probate process. This makes the IUL an effective tool for estate equalization and ensuring that heirs have immediate liquidity to cover estate taxes or final expenses.

Potential Drawbacks and Risks to Consider

While the benefits of an IUL are significant, they are not without costs. An IUL is a complex financial product that requires active management and a clear understanding of its internal expenses.

Fee Structures and Cost of Insurance

Every IUL policy carries internal costs, including premium load fees, administrative charges, and the Cost of Insurance (COI). The COI is not static; it increases as the insured person ages. In the early years of a policy, the fees may consume a significant portion of the premium. If the policy is not sufficiently funded in the early years, the rising COI in later years could potentially deplete the cash value, leading to a policy lapse. This makes “maximum funding” a critical strategy for those using an IUL for wealth accumulation.

The Impact of Gains Caps and Participation Rates

The caps and participation rates are not set in stone. Insurance companies have the right to adjust these figures periodically based on the economic environment and the cost of the options they buy to hedge the index. If an insurance company lowers the cap from 10% to 7%, the long-term growth projections of the policy will be significantly impacted. Investors must choose companies with a strong track record of maintaining competitive caps and participation rates.

Complexity and Long-Term Commitment

An IUL is not a short-term investment. It typically takes 10 to 15 years of consistent funding before the cash value and tax benefits become truly advantageous. Surrender charges—fees penalized for cancelling the policy early—can be quite high during the first decade. This is a “buy and hold” financial strategy that requires a long-term commitment to be successful.

Comparing IULs to Other Financial Vehicles

To determine if an IUL account fits into your financial plan, it is helpful to compare it against more common investment and insurance options.

IUL vs. 401(k) or Roth IRA

Traditional retirement accounts like the 401(k) have contribution limits and mandatory distribution rules (RMDs). An IUL, when structured correctly, has no IRS-mandated contribution limits (provided it doesn’t become a Modified Endowment Contract, or MEC) and no required distributions. While a Roth IRA also offers tax-free withdrawals, it has strict income eligibility requirements that many high-earners exceed. An IUL can serve as a “shadow Roth” for those who are ineligible for traditional Roth accounts.

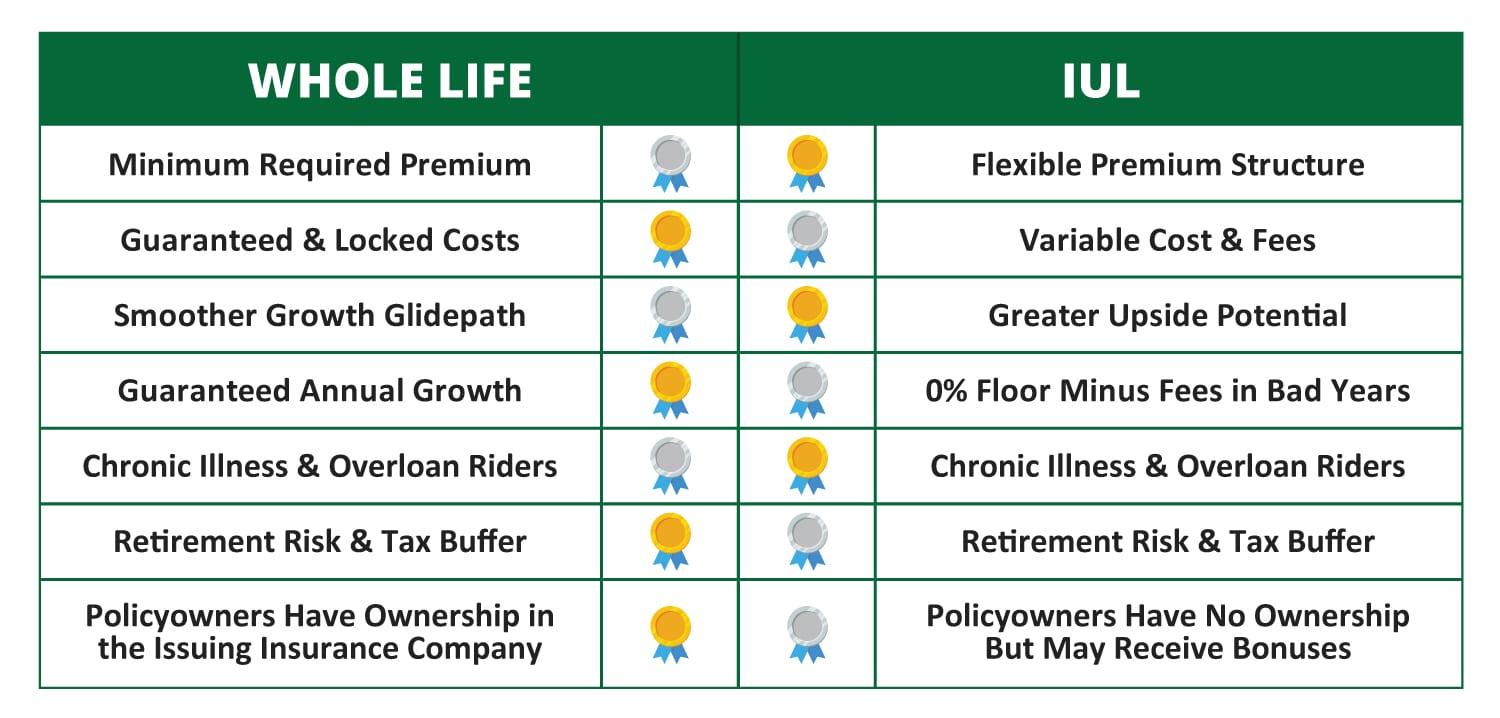

IUL vs. Whole Life Insurance

Whole Life insurance offers guaranteed growth and a fixed premium, providing more certainty but often lower potential returns. IUL accounts offer the potential for higher growth because they are linked to market indexes. While Whole Life is often viewed as a “conservative” bond alternative, an IUL is often viewed as a “moderate” equity-linked alternative with a safety net.

Is an IUL Account Right for Your Financial Strategy?

The decision to open an IUL account should be based on your specific financial goals, risk tolerance, and time horizon. It is rarely a replacement for a diversified portfolio of stocks and bonds, but rather a complementary asset.

Ideal Candidates for IUL Policies

The ideal candidate for an IUL is typically someone who has already maximized their contributions to employer-sponsored retirement plans and is looking for additional tax-advantaged ways to save. They generally have a need for life insurance and a desire to participate in market gains without the risk of losing their principal. Because of the high upfront costs, IULs are best suited for individuals with stable, high incomes who can commit to funding the policy for the long haul.

How to Evaluate a Policy Before Signing

Before committing to an IUL, it is vital to request a “full illustration” from the insurance provider. This document shows how the policy might perform under various market scenarios. Pay close attention to the “guaranteed” column versus the “proposed” column. Furthermore, work with a financial professional who understands how to structure the policy for “minimum death benefit and maximum cash value”—a configuration that minimizes the cost of insurance and maximizes the wealth-building potential of the account.

In conclusion, an IUL account is a sophisticated financial tool that offers a unique blend of protection, growth potential, and tax advantages. While it requires a deep understanding of its moving parts and a commitment to long-term funding, it can be a powerful engine for wealth preservation and tax-free income in a well-rounded financial plan.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.