In the dynamic landscape of personal finance, understanding the tools available for securing your future is paramount. Among the most foundational and powerful instruments for retirement savings is the Individual Retirement Account, or IRA. Far more than just another savings vehicle, an IRA is a tax-advantaged investment account designed specifically to help individuals save for retirement. It represents a cornerstone of long-term financial planning, offering various structures that cater to different financial situations and goals.

The concept of an IRA was introduced by the Employee Retirement Income Security Act of 1974 (ERISA) in the United States, intended to provide a mechanism for individuals without employer-sponsored retirement plans to save for retirement on a tax-deferred basis. Over the decades, IRAs have evolved, with new types emerging to offer even greater flexibility and tax benefits. Today, they are an indispensable part of a comprehensive retirement strategy for millions, whether used as a primary savings vehicle or as a valuable supplement to employer-sponsored plans like 401(k)s.

This article will demystify the IRA, breaking down its various types, illuminating its significant benefits, detailing the rules governing contributions and distributions, and guiding you on how to integrate an IRA effectively into your financial future. By the end, you’ll have a clear understanding of what an IRA account is and why it’s a critical component of a robust financial strategy.

Understanding the Basics of an IRA

At its core, an IRA is a specialized investment account that offers tax advantages to encourage saving for retirement. Unlike a standard brokerage account where investment gains are typically taxed annually, an IRA provides mechanisms for your investments to grow either tax-deferred or tax-free, depending on the account type. It’s not an investment itself, but rather a container within which you hold various investments like stocks, bonds, mutual funds, exchange-traded funds (ETFs), and more.

What is an IRA?

An IRA is an individual retirement arrangement that allows eligible individuals to save money for retirement with tax benefits. The term “individual” is key here; unlike employer-sponsored plans, an IRA is opened and managed by an individual, not tied to their employment status, although certain types can be established by self-employed individuals or small business owners. The primary allure of an IRA lies in its tax treatment, which can significantly boost your retirement nest egg over decades of compounding growth. These tax benefits are designed to incentivize long-term saving, making retirement more attainable and financially secure.

Why is an IRA Important for Retirement?

The importance of an IRA for retirement planning cannot be overstated. Firstly, it offers a disciplined approach to saving. With annual contribution limits, an IRA encourages consistent saving habits. Secondly, and perhaps most importantly, are the tax advantages. Whether you’re deferring taxes until retirement or eliminating them entirely on qualified withdrawals in retirement, these benefits allow your investments to grow more rapidly than in a taxable account. This compounding effect, where your earnings generate further earnings, is dramatically amplified within the tax-sheltered environment of an IRA. Furthermore, IRAs provide flexibility; you choose where to open your account and what to invest in, giving you control over your financial destiny. For many, an IRA serves as a crucial bridge between their current income and their future financial independence in retirement.

Types of IRA Accounts

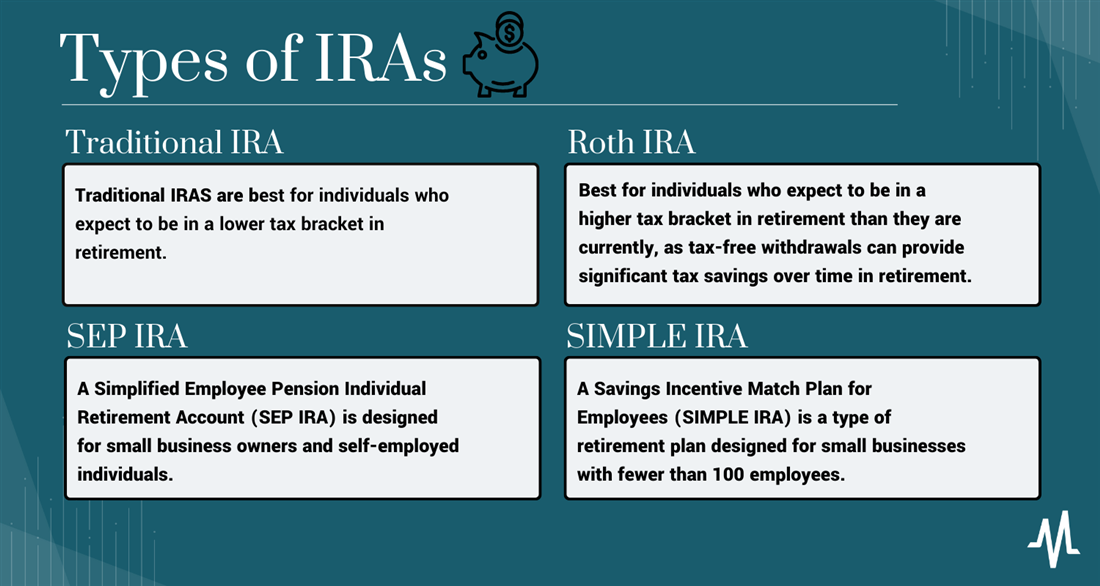

While the fundamental purpose of an IRA remains consistent – to save for retirement with tax advantages – there are several distinct types, each with unique rules regarding contributions, tax deductions, and withdrawals. Understanding these differences is crucial for selecting the IRA that best aligns with your financial situation and retirement goals. The most common types are Traditional IRAs and Roth IRAs, but others like SEP IRAs and SIMPLE IRAs cater to specific employment scenarios.

Traditional IRA

The Traditional IRA is the original Individual Retirement Account and remains a popular choice for many. Its defining characteristic is its tax-deferred growth.

How it Works

Contributions to a Traditional IRA may be tax-deductible in the year they are made, reducing your taxable income in the present. This deduction is particularly attractive for those who anticipate being in a lower tax bracket during retirement than they are during their working years. Money contributed to a Traditional IRA grows tax-deferred, meaning you don’t pay taxes on investment gains or income until you withdraw the funds in retirement. You can contribute to a Traditional IRA regardless of your income level, though the deductibility of contributions may be limited if you or your spouse are covered by a retirement plan at work and your income exceeds certain thresholds. Withdrawals in retirement are typically taxed as ordinary income.

Tax Implications

- Contributions: May be tax-deductible.

- Growth: Tax-deferred.

- Withdrawals: Taxable as ordinary income in retirement.

- Required Minimum Distributions (RMDs): Generally begin at age 73 (as of 2023).

Roth IRA

The Roth IRA, established in 1997, offers an alternative tax treatment that has made it incredibly popular, especially among younger investors or those who expect to be in a higher tax bracket in retirement.

How it Works

Contributions to a Roth IRA are made with after-tax dollars, meaning they are not tax-deductible. However, the significant advantage comes at retirement: qualified withdrawals from a Roth IRA are completely tax-free. This includes both your contributions and all the investment earnings. For withdrawals to be qualified, the account must be open for at least five years, and the account holder must be age 59½ or older, disabled, or using the funds for a qualified first-time home purchase (up to $10,000). Unlike Traditional IRAs, Roth IRAs do not have required minimum distributions (RMDs) during the original owner’s lifetime, offering greater flexibility in estate planning.

Tax Implications

- Contributions: Not tax-deductible.

- Growth: Tax-free.

- Withdrawals: Qualified withdrawals are tax-free in retirement.

- Required Minimum Distributions (RMDs): No RMDs for the original owner.

- Income Limitations: Eligibility to contribute directly to a Roth IRA is phased out for those with higher modified adjusted gross incomes (MAGI).

SEP IRA (Simplified Employee Pension IRA)

The SEP IRA is designed primarily for self-employed individuals and small business owners. It allows employers to contribute to their own and their employees’ retirement plans.

Who is it For?

SEP IRAs are ideal for self-employed individuals, independent contractors, and small business owners with few or no employees. They offer a relatively simple and low-cost way to establish a retirement plan.

Key Features

- Higher Contribution Limits: Generally much higher than Traditional or Roth IRAs, allowing for more aggressive saving.

- Employer Contributions Only: Only employer contributions (including contributions for a self-employed individual to their own plan) are permitted.

- Tax-Deductible Contributions: Contributions are tax-deductible for the employer.

- Tax-Deferred Growth: Investments grow tax-deferred, with withdrawals taxed as ordinary income in retirement, similar to a Traditional IRA.

SIMPLE IRA (Savings Incentive Match Plan for Employees IRA)

The SIMPLE IRA is another option for small businesses (generally with 100 or fewer employees) that don’t offer other retirement plans. It’s relatively easy to set up and administer.

Who is it For?

Small businesses that want to offer a retirement plan to their employees without the complexity and higher costs associated with 401(k)s.

Key Features

- Employee and Employer Contributions: Both employees can contribute, and employers are required to make either matching contributions (up to 3% of an employee’s pay) or non-elective contributions (2% of an employee’s pay).

- Tax-Deductible Contributions: Both employee and employer contributions are generally tax-deductible.

- Tax-Deferred Growth: Investments grow tax-deferred, with withdrawals taxed as ordinary income in retirement.

- Lower Contribution Limits: Contribution limits are generally lower than SEP IRAs but higher than Traditional/Roth IRAs for employees.

Key Benefits of an IRA

Regardless of the specific type, IRAs offer a suite of powerful benefits that make them indispensable for long-term financial planning. These advantages extend beyond simple tax breaks, contributing significantly to wealth accumulation and financial security in retirement.

Tax Advantages

The cornerstone benefit of an IRA is its tax-advantaged status. For Traditional IRAs, contributions may be tax-deductible, lowering your current taxable income. The money then grows tax-deferred, meaning you don’t pay taxes on interest, dividends, or capital gains year after year. Taxes are only paid upon withdrawal in retirement. For Roth IRAs, while contributions are not deductible, all qualified withdrawals in retirement are completely tax-free. This means that decades of compounded growth escape taxation entirely, a powerful incentive for long-term investors.

Compounding Growth

The tax advantages amplify the power of compounding. Compounding is the process where your investment earnings generate their own earnings. In a tax-sheltered IRA, this effect is turbo-charged because you’re not losing a portion of your gains to taxes each year. Over several decades, this can lead to a substantially larger retirement nest egg compared to a taxable account, where annual taxes can erode growth potential. This exponential growth is one of the most compelling reasons to consistently contribute to an IRA.

Flexibility and Control

IRAs offer significant flexibility that employer-sponsored plans often lack. You have complete control over:

- Account Provider: You can choose any brokerage firm, bank, or mutual fund company to open your IRA, allowing you to select one with competitive fees and investment options.

- Investment Choices: Within your IRA, you can typically invest in a wide array of assets, including individual stocks, bonds, mutual funds, ETFs, and sometimes even real estate or commodities, depending on the custodian. This control enables you to tailor your investment strategy to your risk tolerance and financial goals.

- Accessibility: While designed for retirement, IRAs do offer some limited provisions for penalty-free withdrawals for specific circumstances (e.g., first-time home purchase, qualified education expenses, disability), though income taxes may still apply to Traditional IRA withdrawals.

Estate Planning Benefits

IRAs can also play a vital role in estate planning. For Roth IRAs, the absence of Required Minimum Distributions (RMDs) during the original owner’s lifetime allows the account to continue growing tax-free, potentially for decades. Upon the owner’s death, beneficiaries typically inherit the Roth IRA tax-free, making it an excellent vehicle for transferring wealth. Traditional IRAs, while subject to RMDs for beneficiaries, still offer a way to pass on assets in a structured manner.

Contribution Rules and Limits

Understanding the rules governing IRA contributions is essential for maximizing their benefits and avoiding penalties. These rules can change annually, so it’s important to stay informed about the most current limits.

Annual Contribution Limits

The IRS sets annual limits on how much you can contribute to IRAs. For 2023, the maximum amount an individual can contribute to all their Traditional and Roth IRAs combined is $6,500. This limit applies across all your IRAs; for example, if you contribute $3,000 to a Traditional IRA, you can only contribute $3,500 to a Roth IRA for that year. These limits are periodically adjusted for inflation.

Income Limitations for Roth IRA

While anyone can contribute to a Traditional IRA (though deductibility may be limited by income), direct contributions to a Roth IRA are subject to income limitations. If your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute directly to a Roth IRA is phased out or eliminated entirely. For those above these income limits, a “backdoor Roth IRA” strategy might be an option, which involves contributing to a Traditional IRA (non-deductible) and then converting it to a Roth IRA.

Spousal IRA Contributions

If you are married and file jointly, and one spouse has little or no earned income, the working spouse can contribute to a Spousal IRA for the non-working spouse. This allows both spouses to save for retirement in their own IRA accounts, effectively doubling the household’s annual IRA contribution capacity, provided the working spouse has sufficient earned income to cover both contributions.

Catch-up Contributions

To help older individuals boost their retirement savings as they near retirement, the IRS allows “catch-up contributions” for those age 50 and older. For 2023, individuals age 50 and over can contribute an additional $1,000 to their Traditional or Roth IRAs, bringing their total annual contribution limit to $7,500. This provision recognizes the financial realities of later-life saving and provides an extra opportunity to accumulate wealth.

Getting Started with an IRA

Opening and managing an IRA is a straightforward process, but making informed decisions at each step can significantly impact your retirement security.

Opening an Account

The first step is to choose a reputable financial institution. Most major brokerage firms, banks, and mutual fund companies offer IRA accounts. You’ll need to decide between a Traditional IRA, Roth IRA, or potentially a SEP/SIMPLE IRA if you’re self-employed or a small business owner. The application process typically involves providing personal information, your Social Security number, and selecting your desired IRA type. You can usually fund the account through electronic transfers, checks, or rollovers from other retirement plans.

Choosing Investments

Once your IRA is open and funded, the next critical step is selecting your investments. Remember, an IRA is just the account wrapper; what you put inside it dictates its growth. Most custodians offer a wide range of investment options, including:

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other assets.

- Exchange-Traded Funds (ETFs): Similar to mutual funds but traded like stocks throughout the day.

- Individual Stocks and Bonds: For those who prefer to build their own portfolio.

- Target-Date Funds: Funds that automatically adjust their asset allocation as you approach a specific retirement year.

Your investment choices should align with your risk tolerance, time horizon, and retirement goals. Diversification is key to managing risk.

Rollovers and Transfers

If you leave a job, you may have the option to roll over your employer-sponsored retirement plan (like a 401(k)) into an IRA. This is often an excellent way to consolidate your retirement savings, gain more control over investment options, and potentially reduce fees. Similarly, you can transfer an IRA from one custodian to another without incurring taxes or penalties. These moves are typically initiated through a “direct rollover” or “trustee-to-trustee transfer” to ensure funds never pass directly through your hands, thus avoiding potential tax complications.

Planning for Withdrawals

While the primary goal is to save for retirement, it’s also important to understand the rules around withdrawals. Generally, withdrawing from a Traditional IRA before age 59½ incurs a 10% early withdrawal penalty, in addition to income taxes. Roth IRA withdrawals of contributions are typically tax and penalty-free at any time, but earnings withdrawn before age 59½ and before the account is five years old may be subject to taxes and penalties. Planning for how you will draw down your assets in retirement, considering factors like RMDs and tax implications, is a crucial part of a comprehensive retirement strategy.

Deciding Which IRA is Right for You

Choosing between a Traditional and Roth IRA, or determining if a SEP or SIMPLE IRA is appropriate, depends heavily on your individual circumstances. There’s no one-size-fits-all answer, but by considering a few key factors, you can make an informed decision.

Traditional vs. Roth: A Comparison

The central debate between Traditional and Roth IRAs boils down to when you prefer to pay taxes: now or later.

- Traditional IRA is often better if: You expect to be in a lower tax bracket in retirement than you are now. The upfront tax deduction is valuable today, and paying taxes on withdrawals later at a lower rate is advantageous.

- Roth IRA is often better if: You expect to be in a higher tax bracket in retirement. Paying taxes on your contributions now means all qualified withdrawals are tax-free in your golden years, which can be immensely valuable. Roth IRAs are also attractive for younger investors who have many years for their investments to grow tax-free.

Factors to Consider

- Current Income and Tax Bracket: Your current income and the tax bracket you fall into are primary drivers for the Traditional vs. Roth decision.

- Future Income and Tax Bracket Expectations: Projecting your future financial situation can help you anticipate future tax rates.

- Access to Employer Plans: If you have access to a 401(k) or similar plan, it might influence your IRA strategy, especially regarding contribution deductibility.

- Age and Time Horizon: Younger investors often benefit more from a Roth IRA due to the longer period for tax-free growth.

- Employment Status: Self-employed individuals or small business owners might find SEP or SIMPLE IRAs more suitable due to higher contribution limits and employer matching aspects.

Seeking Professional Advice

Navigating the complexities of IRAs and integrating them into a broader financial plan can be challenging. Consulting with a qualified financial advisor can provide invaluable personalized guidance. An advisor can help you assess your current financial situation, understand your long-term goals, project future tax scenarios, and recommend the most appropriate IRA strategy to maximize your retirement savings. They can also assist with investment selection and ongoing portfolio management, ensuring your IRA consistently works towards your financial future.

In conclusion, an IRA account is more than just a savings vehicle; it’s a powerful and flexible tool designed to secure your financial future through tax-advantaged investing. By understanding the different types, their benefits, and the rules that govern them, you can strategically leverage IRAs to build a robust retirement nest egg and achieve lasting financial independence. Starting early and contributing consistently are two of the most effective strategies for harnessing the full power of an IRA.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.