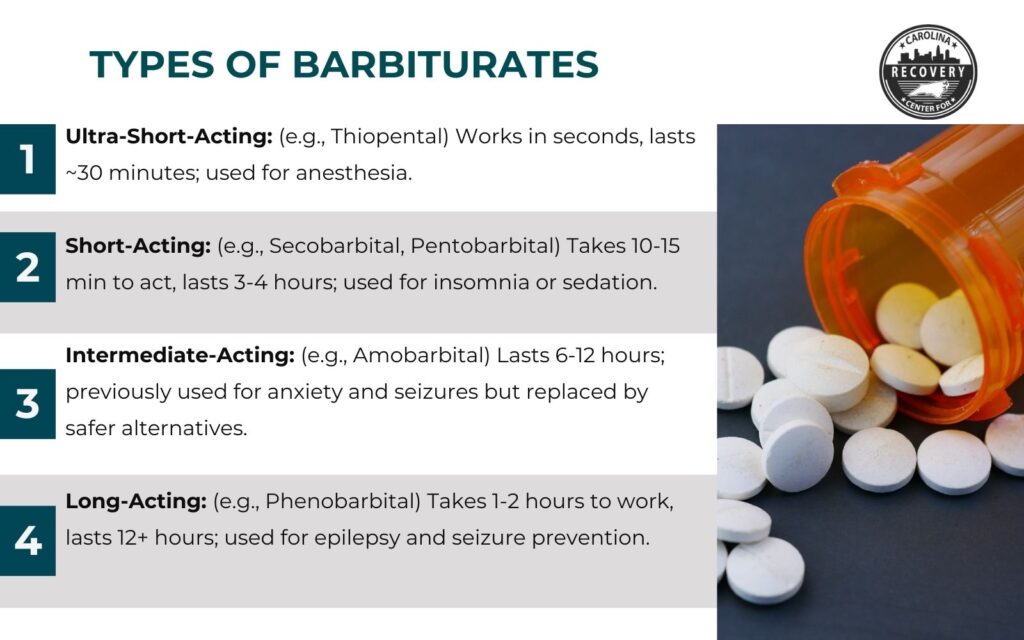

The Pharmaceutical Origin and Early Market Dominance

To understand the financial journey and impact of barbiturates, it’s essential first to define what they are. Barbiturates represent a class of central nervous system (CNS) depressant drugs that were once widely prescribed for their sedative, hypnotic, anxiolytic, and anticonvulsant properties. Chemically derived from barbituric acid, synthesized in 1864, the first pharmacologically active barbiturate, barbital, was introduced in 1903 under the trade name Veronal by Bayer. Subsequent decades saw the development and widespread adoption of numerous variants, including phenobarbital (Luminal), amobarbital (Amytal), secobarbital (Seconal), and pentobarbital (Nembutal), each with varying onset and duration of action.

In the early to mid-20th century, barbiturates carved out a dominant position in the burgeoning pharmaceutical market. They addressed significant unmet medical needs, offering solutions for insomnia, anxiety, epilepsy, and even as anesthetic agents. Their broad applicability across various therapeutic areas meant substantial commercial potential. For pharmaceutical companies, the development and marketing of these compounds translated into immense profitability. Low production costs, coupled with high demand and relatively straightforward synthesis, made them attractive products for investment. Companies invested heavily in research and development, not necessarily to discover entirely new drug classes, but to refine existing barbiturate structures, seeking improved efficacy, reduced side effects, and more convenient dosing schedules. This iterative innovation fostered a competitive market where companies vied for market share through product differentiation and aggressive marketing to physicians, establishing barbiturates as cornerstone revenue generators for the industry for decades. The financial drivers were clear: a desperate public seeking relief, a medical community eager for effective tools, and pharmaceutical firms ready to capitalize on a seemingly revolutionary class of drugs.

Shifting Investment Landscape: The Rise and Fall of a Drug Class

The market dominance of barbiturates peaked around the mid-20th century, representing a significant portion of pharmaceutical sales and a lucrative investment for stockholders in companies like Eli Lilly, Abbott Laboratories, and Bayer. Billions were generated globally as these drugs became household names, synonymous with sleep and tranquility. However, this financial zenith was precarious. As widespread usage continued, the inherent risks associated with barbiturates became increasingly evident. Issues like high potential for physical and psychological dependence, severe withdrawal symptoms, and, critically, a narrow therapeutic index (meaning the difference between an effective dose and a toxic dose was small) led to a significant number of accidental and intentional overdoses. This growing public health concern began to cast a long shadow over their economic viability.

The late 1950s and 1960s marked a pivotal shift in the pharmaceutical investment landscape with the advent of benzodiazepines, notably chlordiazepoxide (Librium) in 1960 and diazepam (Valium) in 1963. These new anxiolytics and hypnotics offered a significantly wider therapeutic index, a lower risk of overdose mortality, and generally milder withdrawal symptoms compared to barbiturates. This scientific advancement represented a severe competitive pressure on the established barbiturate market. Pharmaceutical companies, driven by both public safety and competitive advantage, began to redirect substantial research and development (R&D) investments away from barbiturate analogs and towards these safer, more effective alternatives.

The financial implications were profound. Barbiturate market share plummeted rapidly as physicians transitioned to prescribing benzodiazepines. Companies that had heavily invested in barbiturate production and marketing faced declining revenues and required strategic pivots. While some continued to manufacture specific barbiturates for niche applications, the era of broad-market dominance and high profitability for this class of drugs effectively ended. This dramatic shift serves as a stark historical lesson in pharmaceutical economics: innovation, particularly in safety and efficacy, can rapidly reconfigure entire market segments, making once-dominant product lines financially obsolete and necessitating a constant re-evaluation of R&D portfolios to maintain long-term profitability and shareholder value.

The Economics of Regulation and Risk Management

The inherent dangers of barbiturates prompted significant governmental and regulatory intervention, profoundly impacting their financial trajectory and the pharmaceutical industry at large. Regulatory bodies, such as the U.S. Food and Drug Administration (FDA) and the Drug Enforcement Administration (DEA), increased their scrutiny, leading to stricter controls on manufacturing, prescribing, and dispensing. In the United States, barbiturates were eventually classified under the Controlled Substances Act, primarily as Schedule II, III, or IV drugs, depending on their potential for abuse and dependence.

This regulatory environment imposed substantial financial burdens on pharmaceutical companies. Compliance costs escalated significantly, encompassing rigorous manufacturing standards, comprehensive record-keeping, enhanced security measures for storage, and stringent reporting requirements. For companies, navigating this complex regulatory maze became an overhead expense, impacting profit margins for drugs that were already experiencing declining market demand. Furthermore, the financial risk associated with barbiturates extended beyond compliance. Litigation costs related to addiction, overdose deaths, and product liability became a tangible threat, leading to expensive lawsuits and settlements that directly eroded corporate assets and damaged brand reputation, indirectly affecting future sales and investor confidence.

Healthcare systems and insurers also felt the economic ripple effect. As the risks became clearer, prescribing guidelines evolved, often limiting the duration and dosage of barbiturate use. This affected pricing and reimbursement strategies, pushing the market toward less risky alternatives. The societal costs of barbiturate abuse and addiction, including emergency room visits, long-term treatment programs, and lost productivity, placed additional strain on public health budgets. While not directly borne by pharmaceutical companies as production costs, these externalized costs highlighted the broader economic impact of a drug class with significant public health consequences, influencing policy decisions that further constrained their commercial viability. This regulatory and risk management landscape fundamentally reshaped the investment thesis for barbiturates, shifting the focus from high-volume sales to carefully managed, low-volume production for specific, medically justified applications.

Current Market Niche and Future Financial Outlook

Today, the financial footprint of barbiturates is significantly reduced, reflecting their limited role in modern medicine. While once blockbuster drugs, their market has shrunk to a highly specialized niche, with their use largely superseded by safer and more targeted pharmacotherapies. Few barbiturates remain commercially available for human use, primarily phenobarbital for the long-term management of certain seizure disorders, and pentobarbital and secobarbital for specific acute medical needs like procedural sedation or physician-assisted death in jurisdictions where it is legal. Thiopental, once a staple for induction of anesthesia, is now rarely used clinically due to availability issues and the rise of alternatives.

For the pharmaceutical companies that still manufacture these legacy compounds, the economics are fundamentally different from their heyday. Production volumes are significantly lower, catering to a small, specialized demand rather than mass markets. This can lead to higher per-unit manufacturing costs due to reduced economies of scale, though proprietary synthesis methods or long-amortized infrastructure might mitigate some of this. Investment in these legacy drugs is minimal; R&D budgets are overwhelmingly directed towards novel drug discovery, particularly in areas like biologics, gene therapies, and precision medicine, which promise higher returns on investment and address current unmet needs with superior safety profiles. The opportunity cost of investing resources in barbiturate research or development is simply too high for most pharmaceutical firms, given the competitive landscape and regulatory hurdles.

The financial outlook for barbiturates remains constrained. Their continued presence in the market is often a matter of maintaining availability for essential niche applications rather than a pursuit of significant profit. For instance, in veterinary medicine, pentobarbital remains a key component in euthanasia solutions, ensuring a consistent, if emotionally difficult, market demand. The ongoing economic shadow of barbiturates also includes the substantial public health spending on managing past addiction and overdose legacies, reminding us that the financial impact of a drug class extends far beyond its immediate sales figures. As an investment class, barbiturates serve as a historical case study: a powerful reminder of how scientific advancement, regulatory pressures, and evolving public health perspectives can transform a once-dominant financial asset into a highly specialized, low-volume necessity, underscoring the dynamic and often unforgiving nature of the pharmaceutical market.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.