The “Gen X” label often evokes images of grunge music, flannel shirts, and a healthy dose of skepticism towards authority. But beyond the cultural touchstones, understanding the birth years that define Generation X is crucial for a comprehensive financial perspective. For those born between the mid-1960s and the early 1980s, their formative years and subsequent financial journeys have been uniquely shaped by a confluence of economic shifts, technological advancements, and evolving societal expectations. This article delves into the financial landscape of Gen X, exploring their unique challenges, opportunities, and the strategies they can employ to secure their financial future.

The Gen X Financial Crucible: Navigating Economic Turbulence

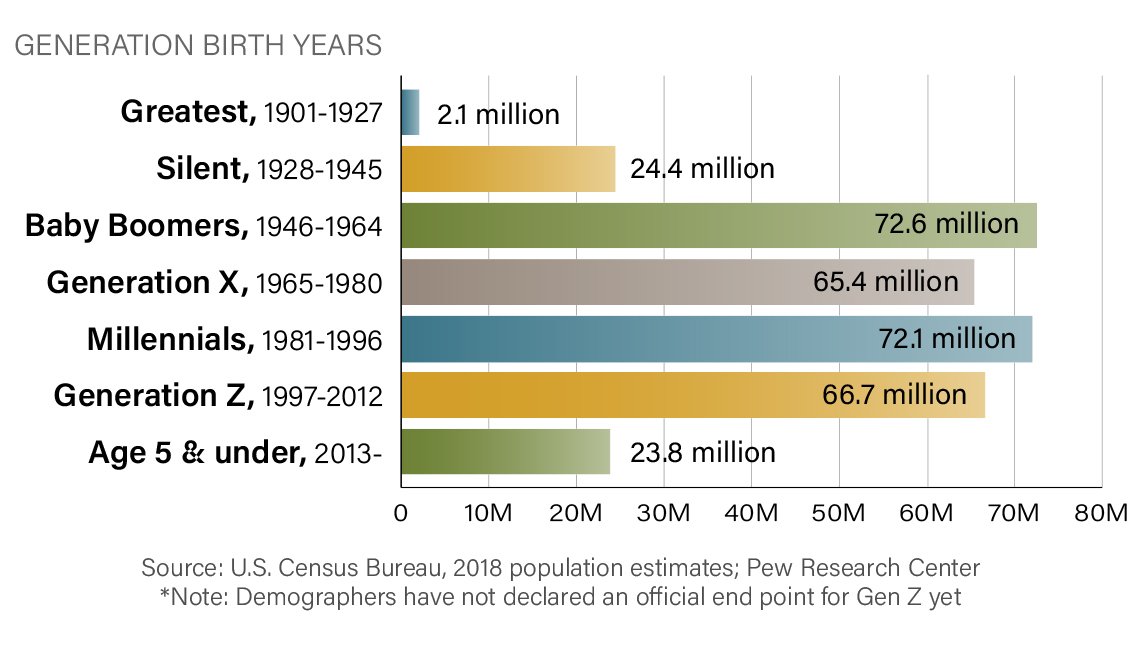

Generation X, typically defined as those born between approximately 1965 and 1980, has experienced a financial upbringing vastly different from both their Baby Boomer predecessors and their Millennial successors. Their economic reality has been characterized by periods of significant volatility, demanding a distinct approach to financial planning and wealth accumulation.

The Dawn of the Information Age and its Economic Ripple Effects

Gen X came of age during the rapid ascent of personal computing and the early stages of the internet. This technological revolution, while offering new avenues for income and innovation, also coincided with significant economic shifts. The deindustrialization of many Western economies, the rise of globalization, and periods of economic recession—including the Savings and Loan crisis of the late 1980s and early 1990s, and the dot-com bubble burst in the early 2000s—created an environment of uncertainty.

For Gen Xers entering the workforce, this often meant navigating a less stable job market than their parents might have experienced. The concept of a “job for life” began to erode, necessitating greater adaptability and a proactive approach to career development. This also translated into a more cautious mindset towards financial commitments. For example, the housing market’s fluctuations during their prime home-buying years meant that many Gen Xers delayed homeownership or were forced to contend with higher interest rates compared to previous generations. This period also saw the gradual shift from defined-benefit pension plans to defined-contribution plans like 401(k)s, placing more responsibility for retirement savings directly onto the individual.

The Rise of the Dual-Income Household and its Financial Implications

The latter half of the 20th century witnessed a significant increase in women entering the workforce. For Gen X, this often meant growing up in or becoming part of dual-income households. While this provided greater financial resources and opportunities, it also introduced new complexities. Managing household finances became a shared endeavor, often requiring more sophisticated budgeting and financial planning. The pressure to balance careers, family responsibilities, and financial goals intensified.

This era also saw the increasing cost of higher education and healthcare, placing a growing burden on families. Gen Xers, therefore, often found themselves grappling with student loan debt for themselves or their children, and facing rising healthcare premiums and out-of-pocket expenses. The financial scaffolding that supported previous generations began to feel less robust, demanding a more disciplined and strategic approach to financial management.

Gen X’s Investment Strategies: Prudence, Diversification, and the Long Game

As Gen Xers have progressed through their careers and entered their peak earning years, their investment strategies have evolved. Shaped by their experiences with economic downturns and a growing awareness of the need for personal financial responsibility, their approach often reflects a blend of caution and a commitment to long-term growth.

The 401(k) Generation and the Burden of Retirement Planning

As previously mentioned, Gen X is largely the generation that has embraced the 401(k) and similar employer-sponsored retirement savings plans. This shift from defined-benefit pensions, which guaranteed a certain income in retirement, to defined-contribution plans places the onus on the individual to contribute consistently and make sound investment decisions. This has led to a heightened awareness of the importance of early and consistent saving.

For many Gen Xers, retirement planning has become a continuous process, often involving a diversified portfolio of stocks, bonds, and mutual funds. They have witnessed firsthand the impact of market volatility, leading many to adopt a balanced approach that seeks growth while mitigating risk. This often involves a longer-term perspective, understanding that market fluctuations are a natural part of investing and that staying invested through various economic cycles is key to long-term wealth accumulation. The increasing availability of online investment platforms and financial advisory services has also empowered Gen Xers to take a more active role in managing their retirement portfolios.

The “Sandwich Generation” and the Dual Financial Pressures

A significant challenge for many Gen Xers is their position as the “sandwich generation.” They are often simultaneously responsible for supporting their aging parents and raising their own children. This dual financial responsibility can create immense pressure, impacting their ability to save for retirement or pursue other financial goals.

This often necessitates a careful balancing act. Gen Xers may need to allocate funds towards elder care, healthcare expenses for aging parents, and, concurrently, save for their children’s education and their own retirement. This can lead to increased reliance on financial advisors or the exploration of various financial tools and strategies to optimize cash flow and investment allocation. Strategies such as maximizing contributions to tax-advantaged retirement accounts, exploring estate planning options for their parents, and seeking opportunities for income enhancement through side hustles or career advancement become paramount.

Future Financial Outlook for Gen X: Adapting to a Shifting Landscape

As Gen Xers continue to navigate their financial lives, several key trends and considerations will shape their future outlook. Their adaptability, forged through years of economic change, will be a significant asset.

The Evolving Retirement Landscape and Longevity Risk

With increasing life expectancies, the traditional retirement age of 65 is becoming less of a definitive endpoint. Gen Xers, therefore, may need to plan for longer retirement periods, which in turn requires larger nest eggs. This necessitates a continued focus on savings and smart investing. The rising costs of healthcare in retirement also remain a significant concern, prompting many to explore options like long-term care insurance or dedicated health savings accounts.

Furthermore, the rise of the gig economy and the potential for continued career longevity means that Gen X may not necessarily retire completely but rather transition to less demanding roles or entrepreneurial ventures. This flexibility can offer new avenues for income generation in their later years, providing a valuable buffer against potential financial shortfalls. The ability to leverage their accumulated skills and experience will be a key determinant of their financial success in this evolving landscape.

The Importance of Financial Literacy and Continuous Learning

Given the complexities of the modern financial world, continuous learning and a strong foundation in financial literacy are more critical than ever for Gen X. Understanding investment vehicles, tax laws, and estate planning principles is crucial for making informed decisions. The digital age has made information readily available, but discerning reliable sources and applying that knowledge effectively remains a challenge.

Gen Xers who actively engage in financial education, seek advice from trusted professionals, and regularly review and adjust their financial plans are best positioned to achieve their long-term goals. This proactive approach, coupled with their inherent resilience and adaptability, will be instrumental in ensuring a secure and prosperous financial future as they move towards and into retirement. The generation that learned to adapt to technological shifts and economic uncertainties is well-equipped to tackle the financial challenges and opportunities that lie ahead.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.