The concept of “trickle-down economics” remains one of the most polarizing and debated frameworks in the history of modern finance and economic policy. Often associated with the Reagan administration of the 1980s, the theory posits that tax breaks and financial benefits provided to corporations and the wealthy will eventually “trickle down” to the rest of the economy. By stimulating investment and production at the top, the theory argues, the entire economic ecosystem grows, ultimately creating jobs, increasing wages, and improving the standard of living for all citizens. However, understanding what the theory actually entailed—and why it continues to occupy such a contentious space in business finance—requires a deep dive into its mechanics, its historical application, and the resulting economic reality.

The Philosophical and Economic Foundations

At its core, the trickle-down theory is rooted in supply-side economics. While the term “trickle-down” is often used pejoratively by critics, its proponents preferred the term “supply-side,” emphasizing the role of production as the primary driver of prosperity.

The Logic of Capital Allocation

The primary argument for the theory centers on the efficient allocation of capital. Economists supporting this view suggest that when corporations and high-net-worth individuals retain more of their earnings—rather than paying them in taxes—they are incentivized to reinvest that capital into business expansion. This expansion takes many forms: building new factories, investing in research and development, upgrading technology, and hiring additional workforce personnel. In this framework, the wealthy act as the “engine” of the economy. When the engine is fueled with lower taxes and deregulation, it pulls the rest of the economic train forward.

Marginal Tax Rates and Investment Incentives

A secondary pillar of the theory is the belief that high marginal tax rates stifle ambition. If the government captures a significant portion of an entrepreneur’s profits, the incentive to take risks—such as launching a new startup or expanding into a volatile market—diminishes. By lowering these rates, the theory argues that the government effectively lowers the cost of business investment. Theoretically, this leads to a more robust business cycle where capital is constantly moving, creating wealth that eventually reaches the middle and lower classes through increased demand for labor and services.

Historical Context: Reaganomics and Beyond

While the idea of supply-side economic policy existed in academic circles long before the 1980s, it reached its zenith during the presidency of Ronald Reagan. The policy package, which came to be known as “Reaganomics,” serves as the definitive case study for the trickle-down experiment.

Tax Reform as a Catalyst

The Economic Recovery Tax Act of 1981 was the centerpiece of this era. It slashed the top marginal income tax rate and significantly lowered corporate tax burdens. The intention was to catalyze a “supply-side boom.” During this period, proponents pointed to the massive expansion of the stock market and the creation of new technology sectors as evidence that the policy was working. The argument was that the deregulation of industries combined with tax relief allowed businesses to compete more effectively on a global scale, thereby generating the “trickle” that would elevate the entire country’s GDP.

The Transition to Globalization

In the decades following the 1980s, the trickle-down narrative evolved as it merged with the broader movements of globalization and financialization. As companies became multinational, the argument shifted slightly: the focus moved from merely domestic investment to global competitiveness. Policymakers argued that keeping corporate tax rates low was essential to prevent capital flight, where businesses would move their headquarters and operations to countries with more favorable tax environments. In this context, the “trickle-down” was intended to keep the domestic economy attractive for global capital, which would theoretically sustain long-term employment levels.

Critical Analysis: Where the Theory Met Reality

Decades after the initial implementation of these policies, economists and financial analysts have subjected the trickle-down theory to rigorous scrutiny. The results, according to much of the data, have been far from the idealized version of the theory presented in the early days.

The Persistence of Income Inequality

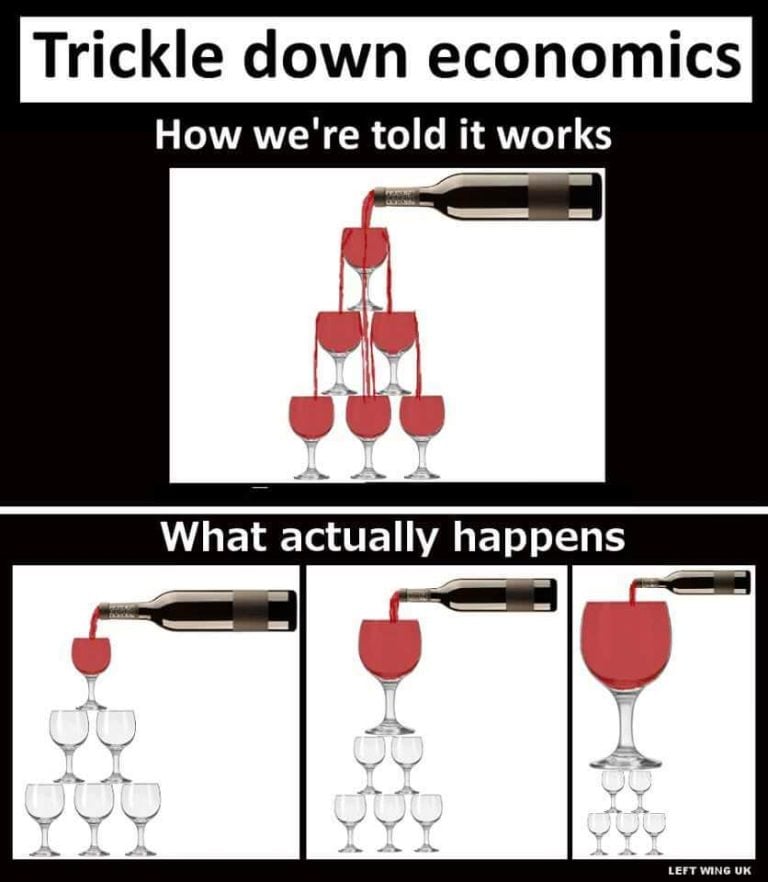

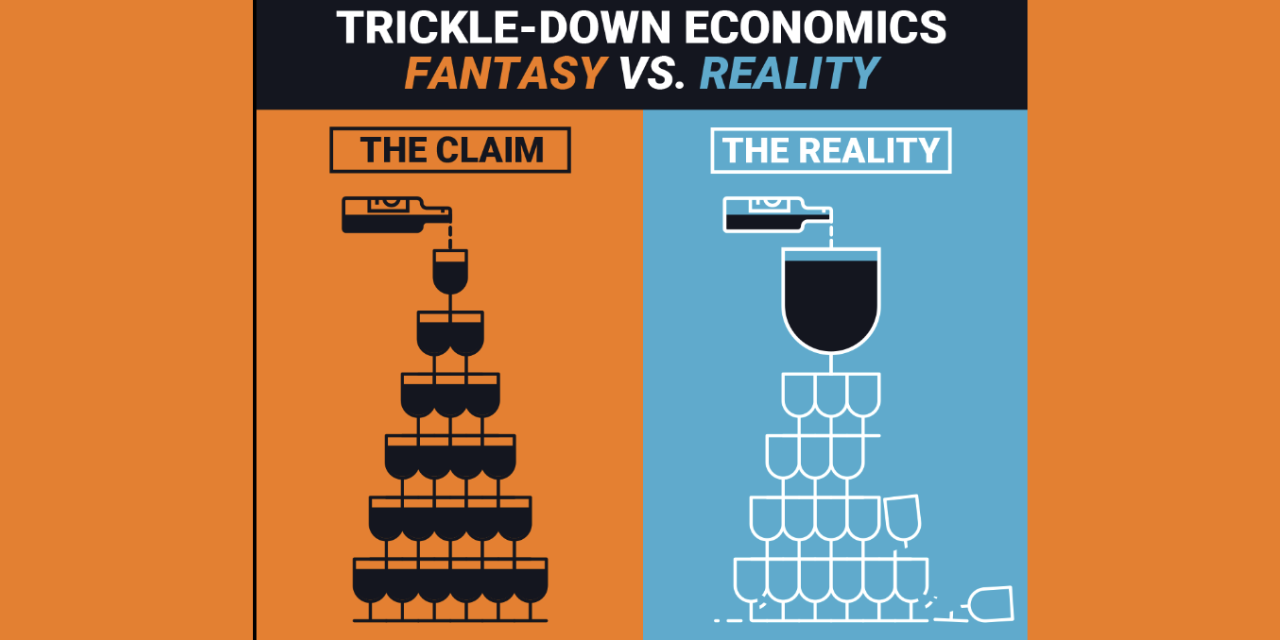

One of the most significant criticisms of the trickle-down theory is the widening gap between the wealthy and the working class. If the theory functioned as designed, the increased wealth at the top should have resulted in a commensurate rise in real wages for the average worker. However, historical data suggests that while productivity has soared over the last forty years, wage growth for middle- and low-income workers has remained stagnant when adjusted for inflation. Critics argue that instead of “trickling down” into salaries or business reinvestment, the excess capital generated by tax cuts often ended up in stock buybacks and dividend payments, which primarily benefit shareholders and executives.

Diminishing Returns on Capital Reinvestment

The assumption that corporate tax savings are automatically recycled into productive assets—like new machinery or staff—has proven to be overly optimistic. In the modern financial era, corporations often prioritize short-term stock price appreciation over long-term capital expenditure. When tax laws allow companies to keep more cash, they frequently utilize it to repurchase their own shares, a maneuver that inflates earnings per share and increases executive compensation, but does little to stimulate the “trickle” toward the broader economy. Consequently, the capital that was meant to lubricate the economic gears often became trapped in the top layer of the wealth pyramid.

The Legacy of Trickle-Down in Modern Business Finance

Today, the term “trickle-down” is rarely used in boardrooms or professional financial settings; instead, it has been replaced by discussions of “pro-growth” tax policies and “competitiveness.” However, the ghost of the theory remains deeply embedded in current debates regarding tax reform and corporate regulation.

Shifting Focus to Human Capital

Modern business finance is beginning to pivot away from the pure supply-side focus on corporate tax cuts and toward the concept of human capital investment. Many analysts now argue that if the goal is to drive long-term economic growth, financial resources are more effectively deployed through education, infrastructure, and technology adoption than through broad-based corporate tax relief. The argument is that the “trickle” is more likely to occur when the labor force is highly skilled and the infrastructure is modern, rather than when corporations are simply afforded larger profit margins.

The Demand-Side Alternative

The critique of trickle-down has bolstered interest in alternative frameworks, often referred to as “middle-out” or “bottom-up” economics. This school of thought argues that the economy is driven by demand—the ability of the middle and lower classes to spend money on goods and services. When workers have more disposable income, businesses are forced to grow to meet that demand, naturally creating a more stable and equitable cycle of prosperity. While the supply-side theory emphasizes the supply of products, the demand-side critique emphasizes the capacity of the consumer to purchase those products.

Ultimately, the trickle-down theory stands as a monumental study in the limitations of pure financial theory when applied to human systems. While the mechanisms of tax incentives and capital allocation are essential components of any functioning business environment, the assumption that wealth naturally cascades downward has been challenged by the realities of shareholder capitalism and wealth concentration. As business finance continues to evolve, the focus is shifting toward a more nuanced understanding of how capital truly translates into economic growth—one that requires balancing the needs of high-performing corporations with the long-term stability and health of the wider workforce.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.