The term “progressive” carries a rich and often debated history, particularly when viewed through the lens of economic and financial principles. Historically, a progressive, in the context of economic thought and policy, was an individual or movement advocating for reforms aimed at addressing systemic inequalities, market failures, and the concentration of wealth and power that arose during periods of rapid industrialization and unchecked capitalism. Their core belief was that government intervention was necessary to correct these imbalances, protect public welfare, and ensure a more equitable distribution of economic opportunity and resources. This contrasted sharply with proponents of pure laissez-faire capitalism, who believed in minimal government involvement in the economy.

The Roots of Progressive Economic Thought

The economic ideas underpinning progressivism emerged most prominently in the late 19th and early 20th centuries, a period often referred to as the Progressive Era in the United States, but with parallels in other industrialized nations. This era was characterized by unprecedented economic growth, technological innovation, and the rise of massive industrial corporations. However, it also brought profound social and economic challenges that fueled progressive critiques.

Challenging Laissez-Faire Capitalism

Progressives fundamentally questioned the premise that an unregulated free market would naturally lead to optimal economic outcomes for all. They observed firsthand the negative externalities of industrialization: hazardous working conditions, child labor, urban poverty, and environmental degradation, all alongside the immense accumulation of wealth by a few powerful industrialists, often dubbed “robber barons.” They argued that the “invisible hand” of the market was failing to address these issues and, in many cases, actively exacerbating them.

Progressive economists posited that while competition was beneficial, unchecked competition and the pursuit of profit could lead to monopolies and trusts that stifled innovation, exploited workers, and manipulated prices. They believed that the government had a crucial role in safeguarding economic fairness and stability, not just allowing market forces to operate freely. This shift in thinking laid the groundwork for modern concepts of economic regulation and social safety nets.

The Rise of Industrial Monopolies and Wealth Inequality

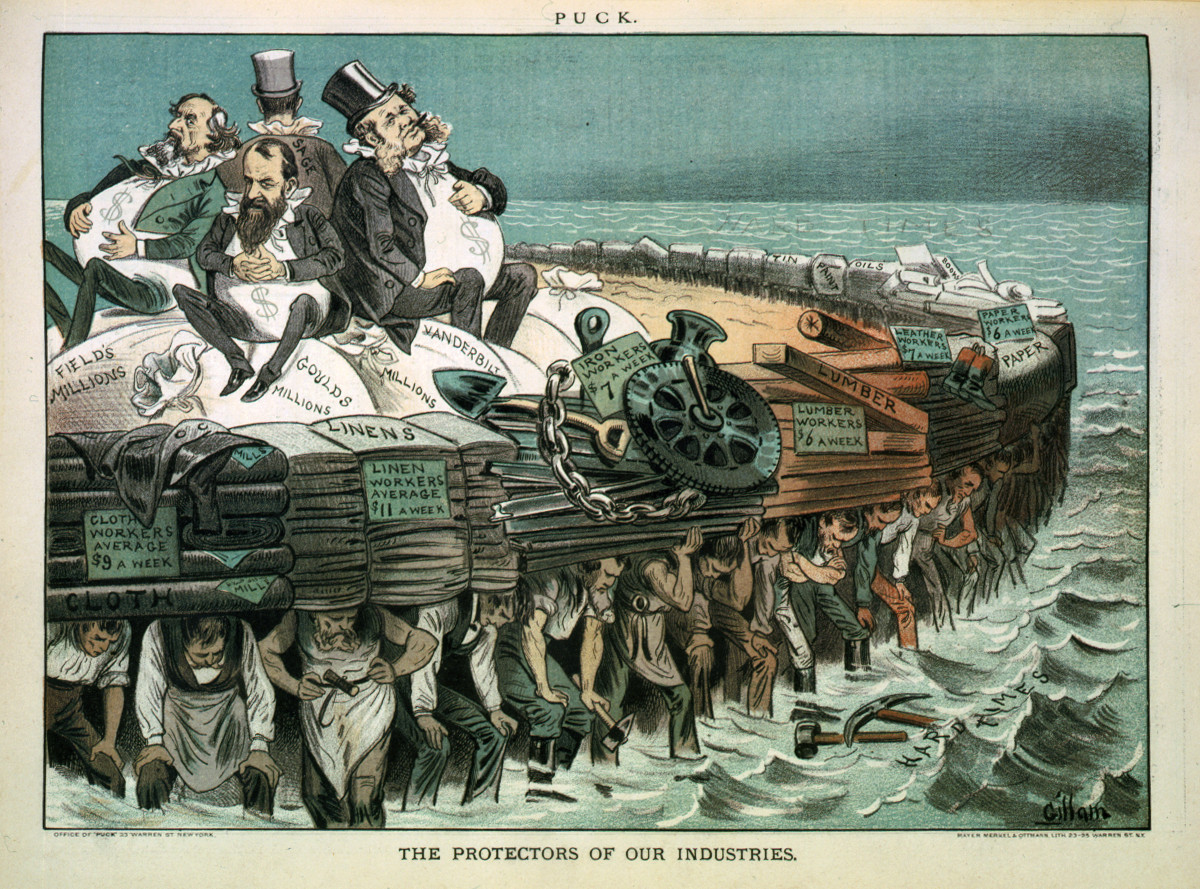

A significant driver of progressive economic thought was the alarming rise of monopolies and trusts that dominated key industries like railroads, oil, steel, and banking. Companies such as Standard Oil, U.S. Steel, and the railroad empires wielded immense economic power, often at the expense of small businesses, farmers, and consumers. They engaged in predatory pricing, controlled supply chains, and exerted undue influence over political processes.

The resulting wealth inequality was stark. While industrial titans amassed fortunes unimaginable before, a large segment of the population, particularly factory workers and recent immigrants, lived in poverty, enduring long hours, low wages, and precarious employment. Progressives saw this vast disparity not merely as an unfortunate byproduct of economic development, but as a direct consequence of an unfair and unregulated economic system. They advocated for policies to break up these monopolies and to rebalance economic power.

Key Financial and Economic Policies of Progressivism

Progressives championed a range of economic and financial policies designed to curb corporate power, promote fair competition, protect workers, and fund public services. These policies reshaped the economic landscape and laid the foundation for much of modern financial regulation.

Anti-Trust Legislation and Market Regulation

Central to the progressive economic agenda was the belief that monopolies harmed market efficiency and consumer welfare. The Sherman Antitrust Act of 1890, though initially weakly enforced, provided a legal framework that progressives later leveraged to break up trusts and regulate large corporations. Theodore Roosevelt’s “trust-busting” efforts and Woodrow Wilson’s Clayton Antitrust Act of 1914 strengthened these regulations, prohibiting practices like price discrimination and interlocking directorates, and granting more power to agencies like the Federal Trade Commission (FTC) to oversee fair competition. These measures aimed to restore competitive markets and prevent the excessive concentration of economic power.

Progressive Taxation and Wealth Redistribution

Progressives were strong advocates for a more equitable tax system. Prior to the Progressive Era, government revenue largely came from tariffs and excise taxes, which disproportionately burdened lower-income individuals. Progressives argued for the implementation of a federal income tax, believing that those with greater wealth should contribute a larger percentage of their income to support public services. This culminated in the 16th Amendment, ratified in 1913, which established the constitutional authority for a federal income tax.

The concept of “progressive taxation”—where tax rates increase with income—was a cornerstone of their financial philosophy. They also pushed for inheritance taxes to curb the perpetuation of dynastic wealth, aiming to mitigate extreme wealth concentration and provide funds for government programs that benefited the broader public, from infrastructure to education.

Labor Rights, Wages, and Financial Security

Recognizing the immense power imbalance between industrial employers and individual workers, progressives fought for legislation to improve workers’ financial security and working conditions. This included advocating for minimum wage laws, maximum hour legislation (e.g., the eight-hour day), and the abolition of child labor. They supported the right of workers to organize into unions, seeing collective bargaining as a necessary counterweight to corporate power in determining wages and benefits. The goal was to ensure that labor received a fairer share of the wealth it created and to reduce the economic precarity faced by the working class, thereby stimulating broader economic demand.

Central Banking and Monetary Policy

The financial panics that plagued the late 19th and early 20th centuries highlighted the instability of the existing banking system. Progressives, alongside other reformers, pushed for the creation of a centralized banking system to stabilize the economy, control the money supply, and act as a lender of last resort. This led to the establishment of the Federal Reserve System in 1913. The Fed was designed to provide a more elastic currency, supervise banking, and act as a fiscal agent for the U.S. government, thereby fostering greater financial stability and preventing economic collapses that disproportionately harmed ordinary citizens and small businesses.

Progressive Impact on Business and Corporate Finance

The progressive movement profoundly altered the environment for businesses and reshaped corporate finance practices. No longer could corporations operate with complete autonomy, free from government oversight.

Shifting Corporate Responsibility and Governance

Progressive reforms introduced the idea that corporations had responsibilities beyond merely maximizing shareholder profit. Legislation related to worker safety, consumer protection, and environmental standards (though nascent at the time) began to establish a broader framework of corporate accountability. The very structure of corporate governance began to face scrutiny, with demands for greater transparency and checks on executive power. This was a nascent step towards what would later evolve into concepts of corporate social responsibility (CSR) and stakeholder capitalism.

Investor Protection and Financial Transparency

Prior to progressive reforms, financial markets were often opaque and susceptible to manipulation. Progressively-minded regulators and lawmakers sought to bring greater transparency and fairness to financial dealings. While comprehensive investor protection laws (like those that emerged after the Great Depression) were still some decades away, the progressive emphasis on curbing monopolies and promoting fair business practices laid the groundwork for future regulations aimed at preventing market abuses and ensuring that investors had access to reliable information. This early push for transparency was crucial for building trust in financial institutions.

The Enduring Legacy: Modern Applications of Progressive Economic Principles

While the original Progressive Era concluded over a century ago, many of the economic principles championed by progressives continue to resonate and inform contemporary financial and economic debates.

Addressing Contemporary Wealth Gaps

The concern over wealth and income inequality remains a central theme in modern economic discourse. Progressive thought continues to inspire arguments for higher marginal tax rates on the wealthy, increased inheritance taxes, and expanded social safety nets to address the growing disparities. Policies like universal basic income, expanded access to affordable healthcare, and investments in public education are often framed within a progressive economic paradigm, aiming to provide greater economic security and opportunity for a broader segment of the population.

Financial Regulation in the 21st Century

The progressive commitment to financial stability and consumer protection is evident in modern regulatory frameworks. Following financial crises, such as the Great Recession of 2008, there have been renewed calls for stronger financial regulations, including reforms to banking practices, oversight of investment firms, and consumer protection agencies. Laws like the Dodd-Frank Act in the U.S. reflect a continuation of the progressive ideal that unchecked financial markets pose systemic risks that require governmental oversight to protect the broader economy and individual investors.

The Debate Over Social Spending and Economic Equity

Today, “progressives” often advocate for increased government spending on social programs, infrastructure, and renewable energy, believing these investments not only address social needs but also stimulate economic growth and create jobs. Debates around student loan debt relief, affordable housing, and universal healthcare are direct descendants of progressive ideals about ensuring economic equity and shared prosperity. The core progressive conviction that economic systems should serve the well-being of all citizens, not just a privileged few, continues to shape policy proposals concerning resource allocation, public finance, and the role of the state in mitigating economic hardship.

In essence, a progressive, in economic terms, was and often remains an advocate for governmental and societal mechanisms that ensure economic fairness, mitigate market failures, regulate powerful financial interests, and strive for a more equitable distribution of wealth and opportunity. Their historical impact fundamentally reshaped how economies function, moving from a purely laissez-faire approach to one where government plays a critical role in shaping market outcomes for the common good.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.