The question of “what to invest in” is perhaps the most critical financial inquiry an individual can make. In an era defined by fluctuating inflation, rapid technological advancement, and shifting global demographics, the traditional methods of saving money are no longer sufficient. To build true wealth, one must transition from a saver to an investor. Investing is the process of allocating resources—usually capital—with the expectation of generating an income or profit.

However, the modern investment landscape is vast. From the stock market and real estate to digital assets and personal skill sets, the options can be overwhelming. This guide explores the most effective vehicles for wealth creation, categorized by their risk profiles, liquidity, and long-term potential, providing a strategic roadmap for both novice and seasoned investors.

1. Traditional Asset Classes: The Bedrock of a Portfolio

Traditional investments remain the most reliable way to build long-term wealth. These assets have decades, if not centuries, of historical data supporting their ability to outpace inflation and compound value over time.

The Power of Equities and Index Funds

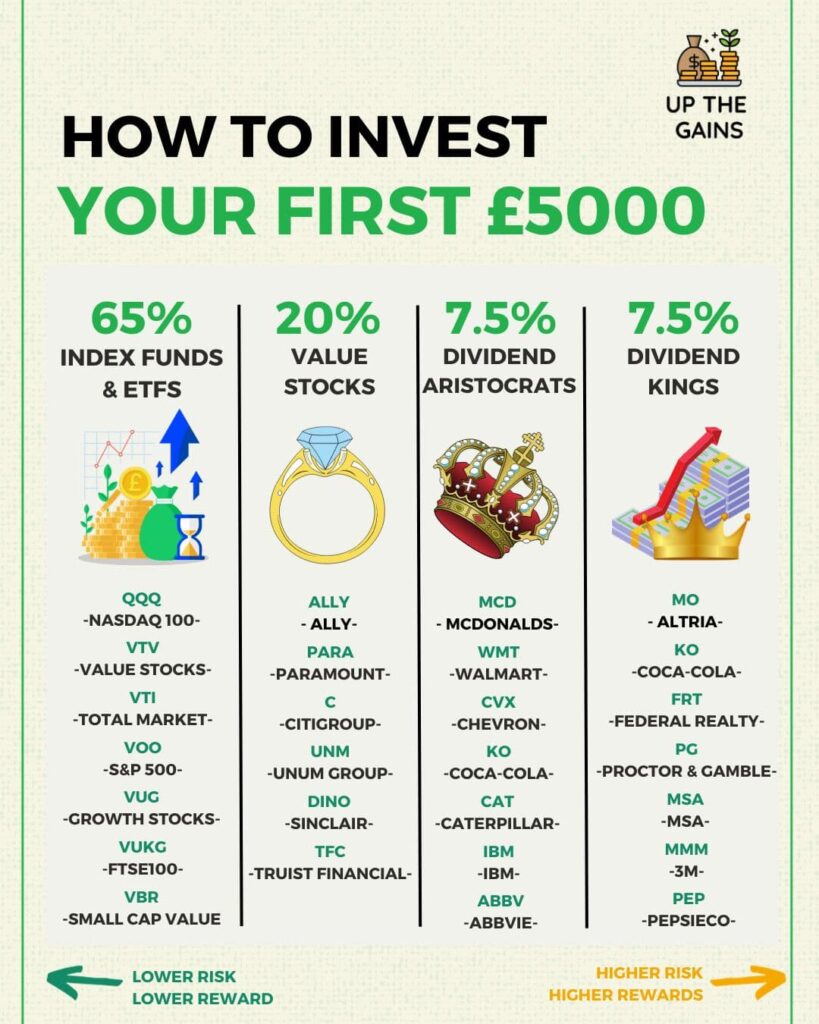

For the majority of investors, the stock market represents the primary engine of growth. Rather than attempting to pick individual “winner” stocks—a practice that often leads to underperformance—many financial experts recommend low-cost index funds or Exchange-Traded Funds (ETFs). By investing in an index like the S&P 500, you are essentially betting on the continued growth of the largest corporations in the world. This approach provides instant diversification, reducing the risk associated with any single company’s failure.

Fixed Income and Bonds

Bonds act as a stabilizer for a portfolio. When you buy a bond, you are essentially lending money to a government or corporation in exchange for regular interest payments and the return of the principal at maturity. While the returns on bonds are generally lower than those of stocks, they provide a safety net during market volatility. In high-interest-rate environments, government bonds (like U.S. Treasuries) become particularly attractive as “risk-free” yields increase.

Real Estate: Physical and Synthetic

Real estate has long been a favorite for those seeking tangible assets. Investing in physical property allows for rental income and capital appreciation. However, for those who do not wish to manage properties, Real Estate Investment Trusts (REITs) offer a way to invest in large-scale commercial or residential portfolios through the stock market. REITs are required by law to distribute 90% of their taxable income to shareholders as dividends, making them excellent vehicles for passive income.

2. Alternative Investments and the Modern Frontier

As the global economy evolves, “alternative” investments have moved from the fringes to the mainstream. These assets often have a low correlation with the stock market, meaning they may stay stable or even rise when stocks are falling.

Digital Assets and Cryptocurrency

While volatile, cryptocurrencies like Bitcoin and Ethereum have emerged as a new asset class. Bitcoin is often referred to as “digital gold” due to its fixed supply, serving as a potential hedge against fiat currency devaluation. Ethereum, on the other hand, represents an investment in the underlying infrastructure of decentralized finance (DeFi). For a modern investor, allocating a small percentage (1–5%) of a portfolio to digital assets can provide significant upside, provided they can withstand the price swings.

Commodities and Precious Metals

In times of geopolitical instability or high inflation, commodities such as gold, silver, and oil often perform well. Gold has been a store of value for thousands of years. Unlike paper currency, it cannot be printed, making it a “hard asset.” Modern investors can gain exposure to commodities through physical ownership, futures contracts, or commodity-focused ETFs.

Private Equity and Venture Capital

Previously reserved for institutional investors and the ultra-wealthy, the democratization of finance has made it easier for individual investors to participate in private equity. This involves investing in companies that are not yet publicly traded. While these investments are highly illiquid (meaning you cannot easily sell your stake), the potential for exponential returns during an Initial Public Offering (IPO) or acquisition is substantial.

3. Investing in Yourself: The Highest Return on Investment

While financial markets are vital, the most significant asset any individual possesses is their “human capital”—the ability to earn. Investing in yourself often yields a higher percentage return than any stock or bond ever could.

High-Income Skill Acquisition

The labor market is shifting toward specialized skills. Investing in education, certifications, or intensive training in fields like data science, financial analysis, or digital sales can lead to significant salary increases. If an investment of $5,000 in a specialized course leads to a $20,000 annual salary increase, the Return on Investment (ROI) is 400% in the first year alone—a figure no traditional market can consistently match.

The Solopreneur Revolution and Side Hustles

In the digital age, starting a business has never been more accessible. Investing capital into a “side hustle”—whether it’s an e-commerce store, a consulting practice, or a content platform—allows you to build an asset that you control. Unlike a stock, where you are a passive observer, a business allows you to directly influence the outcome through your effort and strategy. This provides a secondary stream of income that can be reinvested back into traditional assets.

Health and Longevity

Financial wealth is meaningless without the health to enjoy it. Investing in preventative healthcare, nutrition, and fitness is a financial strategy. By maintaining optimal health, you reduce long-term medical costs and extend your “earning years,” allowing the power of compound interest to work over a longer horizon.

4. Strategic Asset Allocation and Risk Management

Knowing what to invest in is only half the battle; knowing how to manage those investments is what separates successful investors from those who lose money.

The Importance of Diversification

The only “free lunch” in investing is diversification. By spreading your capital across different asset classes (stocks, bonds, real estate, and alternatives), you ensure that a downturn in one sector does not wipe out your entire net worth. A well-diversified portfolio is designed to capture gains in bull markets while cushioning the blow during bear markets.

Understanding Risk Tolerance and Time Horizons

Your investment strategy must align with your age and financial goals. A 25-year-old with a 40-year time horizon can afford to be aggressive, focusing heavily on growth stocks and crypto. Conversely, someone five years away from retirement should prioritize capital preservation and income-generating assets like bonds and dividend-paying stocks.

The Role of Inflation and Economic Cycles

Investors must stay cognizant of the macroeconomic environment. In a high-inflation environment, cash is a losing investment because its purchasing power erodes. In such times, “inflation hedges” like real estate, commodities, and certain equities become essential. Understanding where we are in the economic cycle—expansion, peak, recession, or recovery—helps in deciding whether to be defensive or aggressive with your capital.

Conclusion: Building a Resilient Financial Future

Determining what to invest in is not a one-time decision but a continuous process of evaluation and adjustment. A robust investment strategy should be built on a foundation of traditional assets like index funds and real estate, supplemented by a calculated exposure to modern alternatives like digital assets.

Ultimately, the most successful investors are those who view their finances holistically. They balance the passive growth of the markets with the active growth of their own skills and businesses. By maintaining a long-term perspective, staying diversified, and consistently reinvesting profits, you can move beyond financial insecurity and build a legacy of lasting wealth. The best time to start investing was twenty years ago; the second best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.