When a business owner walks into a bank to apply for a line of credit or a commercial loan, they often focus on their credit score, their annual revenue, and their time in business. While these are critical factors, there is a silent gatekeeper that often determines the fate of an application before a human loan officer even sees it: the SIC code.

Standard Industrial Classification (SIC) codes are four-digit numerical codes assigned by the U.S. government to identify the primary business activity of an establishment. In the world of business finance, these codes are much more than administrative labels; they are risk-assessment tools. Banks and alternative lenders use these codes to categorize businesses into risk tiers. Understanding which SIC codes banks “like” can be the difference between a seamless approval and an automated rejection.

Understanding the Role of SIC Codes in Business Finance

The financial industry operates on the principle of risk mitigation. Banks are not just looking at your individual business’s performance; they are looking at the historical performance of your entire industry. SIC codes allow banks to automate this process, filtering out industries that have historically high failure rates or regulatory complexities.

How Underwriting Algorithms Use Industry Data

In modern banking, the initial phase of underwriting is almost entirely automated. When you submit your business’s legal name and tax ID, the system pulls your business credit report, which prominently features your SIC code. If that code is flagged as “High Risk” or “Restricted,” the algorithm may immediately decrease your borrowing limit or trigger a manual review that requires significantly more documentation. Banks prefer codes that represent stability, low overhead, and predictable cash flow.

The Link Between SIC Codes and Interest Rates

Your industry classification doesn’t just affect whether you get approved; it affects how much the capital will cost you. A business classified under a “favored” SIC code is perceived as a lower risk, which often translates to lower interest rates and more favorable repayment terms. Conversely, “high-risk” industries are often forced into high-interest products, such as Merchant Cash Advances (MCAs), because traditional banks view them as too volatile for standard term loans.

SIC vs. NAICS: What You Need to Know

While the SIC system was officially replaced by the North American Industry Classification System (NAICS) in 1997 for statistical purposes, many legacy banking systems and business credit bureaus (like Dun & Bradstreet) still rely heavily on SIC codes. For a business owner, it is vital to ensure that both your SIC and NAICS codes are aligned and accurately reflect a lender-friendly profile.

Top Low-Risk SIC Codes That Banks Prefer

Banks “like” industries that are “asset-light” or have professional barriers to entry. These businesses are seen as more professional, better managed, and less susceptible to the sudden market swings that plague retail or construction.

Professional and Administrative Services

One of the most lender-friendly categories is professional services. Banks favor these because they typically have low overhead and high margins.

- 7389 (Business Services, Not Elsewhere Classified): This is a broad, catch-all code often used for various consulting and administrative roles.

- 8742 (Management Consulting Services): This is perhaps the most “bank-friendly” code in existence. It implies that the business provides expert advice to other businesses, suggesting a high level of professional competence and low physical risk.

- 8748 (Business Consulting Services, Not Elsewhere Classified): Similar to 8742, this code suggests a professional service model that banks find highly attractive.

Technology and Information Services

In the digital economy, technology companies are viewed as highly scalable and generally safe bets, provided they aren’t in high-risk niches like crypto-mining.

- 7371 (Computer Programming Services): Companies that write and modify software are viewed favorably due to the high demand for their services.

- 7374 (Computer Processing and Data Preparation): This covers SaaS (Software as a Service) models, which banks love because of the recurring revenue streams.

- 7372 (Prepackaged Software): This is another “gold star” code for lenders looking for stable, scalable business models.

Healthcare and Medical Practices

Medical professionals are historically the most sought-after borrowers for banks. The high barrier to entry (schooling and licensing) and the constant demand for services make these codes extremely low-risk.

- 8011 (Offices and Clinics of Doctors of Medicine): This is considered a premier code for financing.

- 8021 (Offices and Clinics of Dentists): Dentists are often eligible for specialized “Professional Loan” programs with the lowest interest rates available.

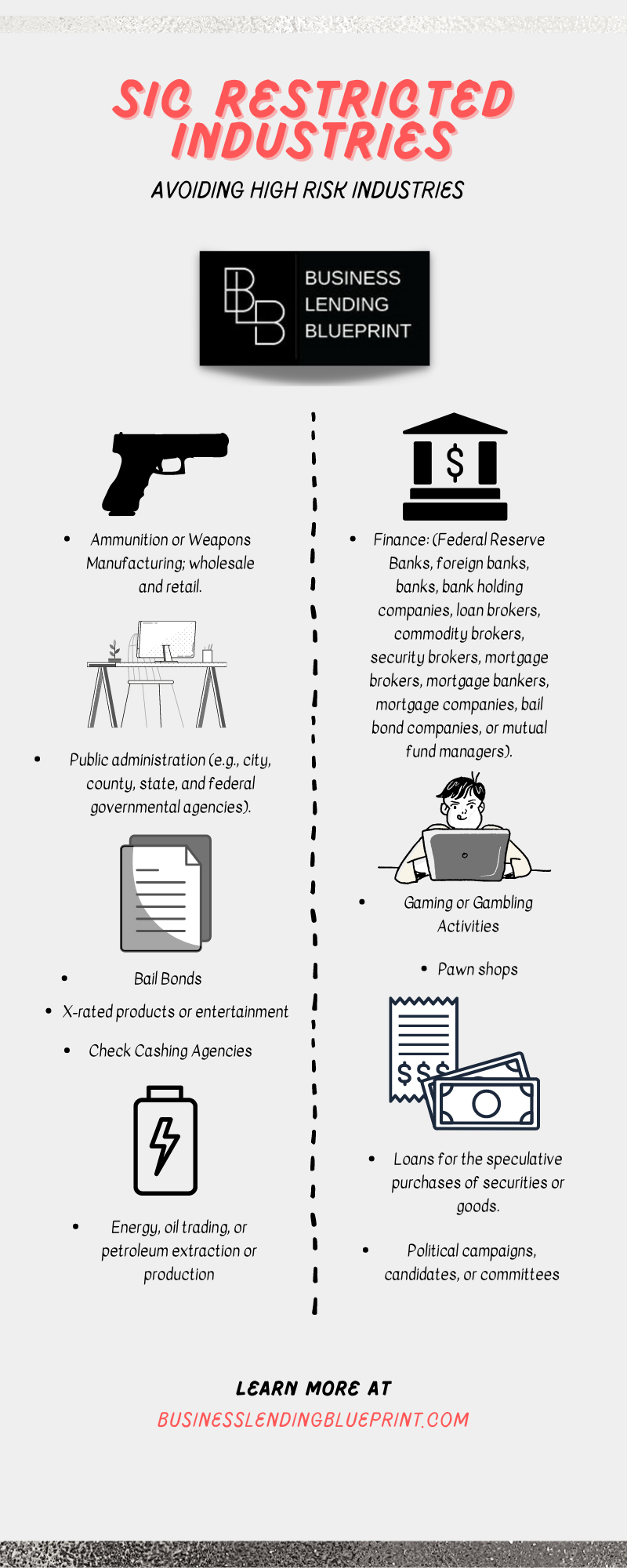

Navigating High-Risk Categories: Why Banks Hesitate

To understand what banks like, you must understand what they avoid. High-risk codes often lead to “Automatic Declines.” These industries are flagged not necessarily because your specific business is failing, but because the industry as a whole is prone to litigation, bankruptcy, or regulatory scrutiny.

Real Estate and Construction

While many people make fortunes in real estate, banks view the industry as highly speculative and cyclical.

- 6531 (Real Estate Agents and Managers): This is often flagged as high-risk because income is commission-based and fluctuates wildly with the economy.

- 1521 (General Contractors – Single-Family Houses): Construction is viewed as high-risk due to the frequency of workplace injuries, the potential for litigation, and the “boom and bust” nature of the housing market.

Transportation and Long-Haul Trucking

The logistics industry is the backbone of the economy, but for a bank, it represents a liability nightmare.

- 4213 (Trucking, Except Local): Long-haul trucking is often restricted because of high fuel costs, expensive equipment maintenance, and significant insurance liabilities. Many banks have a strict “No Trucking” policy for unsecured lines of credit.

High-Volatility Retail and Entertainment

Any industry that deals with “vice” or high-cash volumes is usually avoided due to Anti-Money Laundering (AML) regulations.

- 5813 (Drinking Places – Alcoholic Beverages): Bars and taverns have high failure rates and are subject to intense regulatory oversight.

- 7999 (Amusement and Recreation Services): This is a catch-all for various entertainment venues which banks view as discretionary spending—the first thing to go in a recession.

Strategic Selection: How to Choose a Lender-Friendly SIC Code

If you are in the process of incorporating or updating your business profile, you have the opportunity to be strategic. You should never lie about your business activities (which constitutes bank fraud), but you can choose the code that most accurately describes your least risky activity.

Identifying Your Primary Business Activity

Many businesses do multiple things. A marketing firm might also sell promotional products (Retail). If they classify themselves under a retail SIC code, they may face harder lending requirements. However, if they classify themselves as a “Marketing Consulting” firm (Professional Services), their path to financing becomes much smoother. You should always select the code that represents the “administrative” or “consulting” side of your business if that is a legitimate part of your operations.

How to Check Your Current Classification

Many business owners have no idea what their SIC code is. You can find yours by searching the OSHA SIC Manual or the U.S. Census Bureau website. More importantly, you should check your business credit reports with Dun & Bradstreet (D&B), Experian Business, and Equifax Business. If these bureaus have the wrong code listed, you must file a dispute to correct it, as lenders will pull this data automatically.

Consistency Across All Platforms

A major reason for loan denials is “Information Mismatch.” If your tax return says you are a “Contractor” but your bank application says you are a “Consultant,” the bank’s fraud detection software will flag the application. Before applying for money, ensure your SIC code is consistent across:

- Articles of Incorporation (Secretary of State).

- Your EIN application (IRS).

- Your Business Credit Profiles.

- Your business website and social media.

Maintaining Financial Credibility and Compliance

Selecting a lender-friendly SIC code is only the first step. To maintain a “bankable” status, you must ensure that your financial behavior aligns with the professional image your SIC code projects.

The Importance of a Professional Business Address

Banks look for “stability markers.” If you have a high-end “Management Consulting” SIC code but your business address is a residential house or a P.O. Box, it creates a “cognitive dissonance” in the underwriting system. Using a virtual office or a physical commercial space reinforces the legitimacy of your professional SIC classification.

Building a Strong Business Credit Profile

A favorable SIC code opens the door, but your credit history walks through it. To truly leverage a “preferred” code, you must build a robust business credit score (such as the D&B PAYDEX score). This involves opening trade lines with vendors who report to the bureaus and ensuring every payment is made on time. When a low-risk SIC code is paired with a 80+ PAYDEX score, banks will often compete for your business, offering you pre-approved lines of credit with no collateral required.

Regular Audits of Your Business Data

As your business evolves, so should your SIC code. If you started as a “General Laborer” (High Risk) but have evolved into a “Project Management and Consulting” firm (Low Risk), failing to update your SIC code is costing you money in the form of higher interest rates or denied opportunities. Perform an annual audit of your business filings to ensure you are still classified in the most advantageous, yet honest, category possible.

By understanding the “language” of SIC codes, business owners can position themselves as ideal borrowers. In the world of money, perception is reality. Choosing a lender-friendly SIC code ensures that when a bank looks at your business, they don’t see a risk—they see a partner worth investing in.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.