In an increasingly sophisticated financial world, the concept of “cash back” has evolved from a niche perk to a mainstream expectation for savvy consumers. It represents a potent financial tool, offering a tangible return on everyday spending and presenting a clear pathway to optimizing personal finance. Whether it’s a percentage off your credit card statement, points convertible to cash, or direct rebates from online purchases, understanding where and how to effectively leverage cash back can significantly impact your budget and savings goals. This guide delves into the mechanisms, opportunities, and strategies for maximizing cash back, empowering you to turn ordinary transactions into extraordinary savings.

Understanding the Core Mechanics of Cash Back Programs

At its heart, cash back is a simple yet powerful incentive system designed to reward consumers for their purchasing habits. It’s a fundamental aspect of modern personal finance, offering a small percentage of your money back on eligible purchases. Yet, beneath this simplicity lies a sophisticated ecosystem driven by financial institutions, retailers, and third-party platforms.

How Cash Back Works

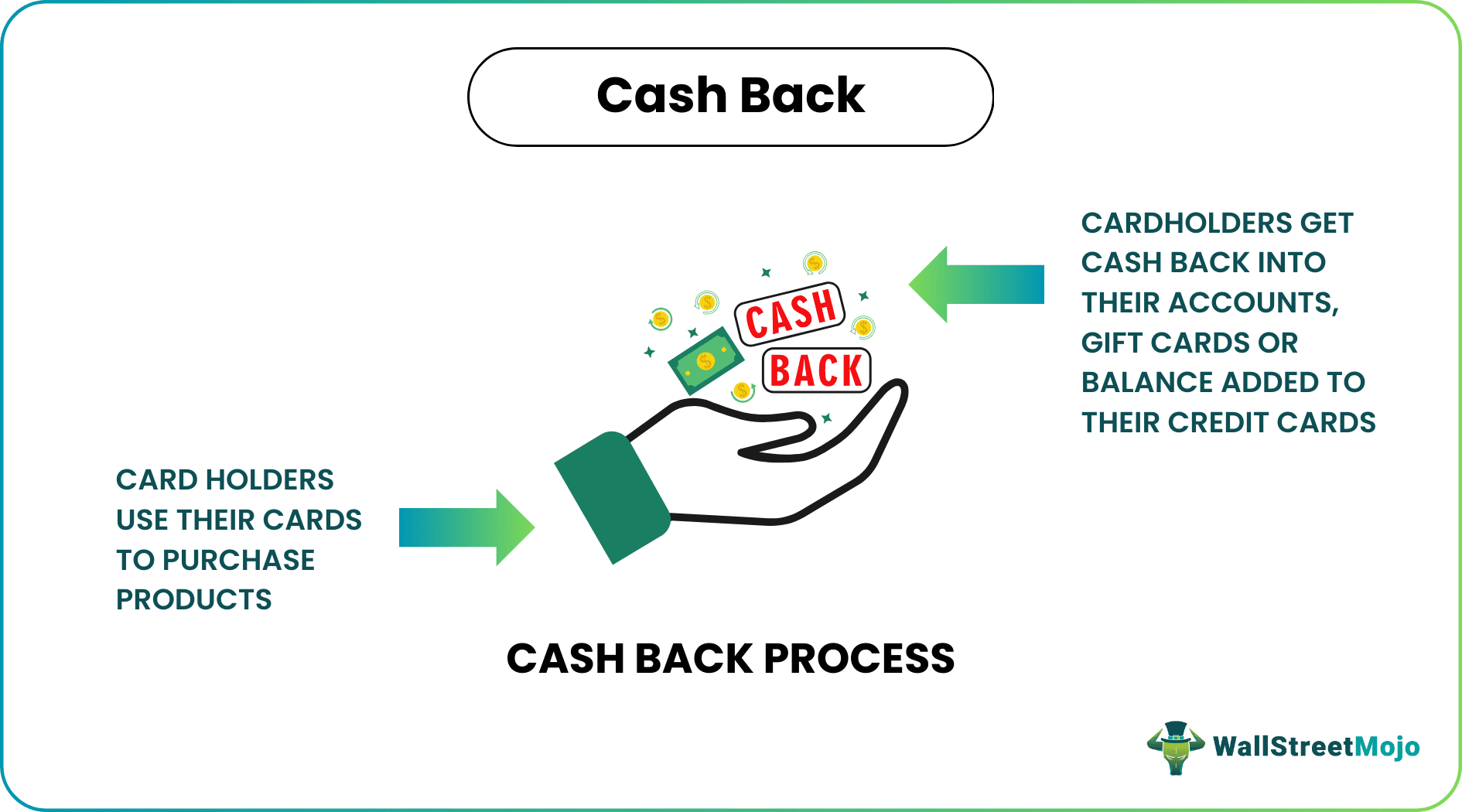

The basic principle of cash back is straightforward: you spend money, and a portion of that spending is returned to you. The “who” and “how” of this return can vary significantly. Typically, cash back is funded either by the financial institution issuing your credit card, the merchant selling the product, or an affiliate marketing platform that facilitates the transaction.

When you use a cash back credit card, for instance, the bank earns a small interchange fee from the merchant with every swipe. A portion of this fee is then passed back to you as cash back. For online shopping portals, the portal earns an affiliate commission for referring you to a retailer; they then share a portion of that commission with you.

Payout methods are diverse:

- Statement Credit: The most common form, where your earned cash back is applied directly to reduce your credit card balance.

- Direct Deposit: Funds are transferred electronically to your bank account, offering liquid cash.

- Gift Cards: Some programs offer enhanced value when redeeming for gift cards from specific retailers.

- Check: Less common now, but some programs still mail a physical check.

Understanding these underlying mechanisms is crucial for discerning the true value and flexibility of various cash back offers.

The Strategic Value for Consumers

For individuals focused on personal finance, cash back is not merely “found money” but a strategic component of a holistic financial plan. It serves multiple critical functions:

- Reducing Overall Spending: By effectively lowering the net cost of purchases, cash back helps stretch your budget further. A 2% cash back on all expenses is akin to a 2% discount on everything you buy, significantly impacting annual spending.

- Maximizing Budget Efficiency: It allows for more efficient allocation of funds. Money earned back can be saved, invested, or used to cover other necessary expenses, freeing up capital that would otherwise be spent.

- A “Free Money” Aspect (When Used Wisely): When coupled with responsible spending habits—only buying what you would have purchased anyway and paying off balances in full to avoid interest—cash back genuinely feels like extra income without extra effort. It rewards financial discipline.

The strategic value extends beyond immediate savings, fostering a mindset of mindful spending and continuous optimization of financial resources.

The Business Perspective: Why Merchants Offer Cash Back

It’s natural to wonder why businesses would give money back. The answer lies in powerful economic incentives that benefit both the seller and the consumer:

- Customer Acquisition and Retention: Cash back acts as a powerful lure for new customers and a strong incentive for existing ones to remain loyal. In a competitive market, a compelling cash back offer can differentiate a product or service.

- Increased Transaction Volume: By making purchases more attractive, cash back programs can encourage consumers to spend more frequently or to make larger individual purchases.

- Data Collection and Marketing Insights: Many loyalty programs tied to cash back collect valuable data on consumer spending habits. This data allows businesses to tailor future marketing efforts, personalize offers, and improve product development, ultimately leading to more effective sales strategies.

From credit card companies vying for market share to retailers competing for foot traffic and online sales, cash back is a proven marketing and loyalty tool that drives consumer engagement and generates economic activity.

Diverse Avenues for Earning Cash Back

The opportunities to earn cash back are vast and varied, spanning across different financial products and shopping environments. To maximize your returns, it’s essential to understand the different types of programs available and how they can be combined.

Credit Card Cash Back Programs

Credit cards remain the cornerstone of many cash back strategies. They offer a reliable and often lucrative way to earn rewards on almost every purchase.

- Fixed-Rate Cards: These cards offer a consistent cash back percentage on all purchases, typically ranging from 1.5% to 2%. They are ideal for simplicity and for those whose spending doesn’t align with rotating categories.

- Rotating Category Cards: Cards like the Chase Freedom Flex or Discover it Cash Back offer higher percentages (often 5%) on specific spending categories that change quarterly (e.g., gas stations, grocery stores, Amazon.com). These require active management but can yield significant returns for targeted spending.

- Bonus Categories for Specific Merchants: Some cards offer elevated cash back at specific retailers or for particular spending types (e.g., 3% on dining, 4% on travel). These are excellent for those with predictable spending patterns in these areas.

- Sign-Up Bonuses: Many cash back cards entice new customers with substantial sign-up bonuses (e.g., “Earn $200 after spending $500 in the first three months”). These provide an immediate boost to your cash back earnings and can be a strategic way to get a quick return on planned large purchases.

When choosing a credit card, always consider the annual fee, interest rates (if you carry a balance), and how well its reward structure aligns with your spending habits.

Retailer-Specific Loyalty Programs

Beyond credit cards, many individual retailers offer their own cash back or points-based loyalty programs. These are often designed to foster direct relationships with customers.

- In-Store Loyalty Cards: Supermarkets, drugstores, and department stores often have membership programs that offer cash back equivalents, exclusive discounts, or points that convert to store credit. Examples include Walgreens Balance Rewards or Target Circle.

- Online Retailer Programs: Major online players like Amazon (with its Prime Rewards Visa Signature Card offering 5% back on Amazon purchases) and specific brand websites (e.g., Sephora’s Beauty Insider) have robust loyalty ecosystems. These programs often stack with other cash back methods.

These programs are excellent for frequent shoppers at particular stores, providing deeper savings within those specific retail environments.

Online Shopping Portals and Apps

The digital age has ushered in a new era of cash back through online shopping portals and mobile apps. These platforms leverage affiliate marketing to provide you with rebates.

- Explanation of Affiliate Model: When you click through a shopping portal (like Rakuten or TopCashback) to a retailer’s website, the portal tracks your purchase. The retailer pays the portal a commission, and the portal shares a portion of that commission with you as cash back.

- Popular Platforms:

- Rakuten (formerly Ebates): One of the largest, offering cash back at thousands of online stores.

- TopCashback: Known for often offering higher percentages and no minimum payout.

- Ibotta: Primarily focused on groceries and in-store offers, requiring users to scan receipts or link loyalty cards.

- Honey: A browser extension that automatically finds and applies coupon codes and also offers its own “Honey Gold” cash back.

- Browser Extensions: Many portals offer browser extensions that automatically notify you when cash back is available on a site you’re visiting, making it seamless to activate.

- Stacking Opportunities: One of the most powerful strategies is to combine a cash back credit card with an online shopping portal. For example, using a credit card that gives 2% cash back on online purchases through a portal offering an additional 5% back results in a total of 7% back.

These digital tools are indispensable for online shoppers looking to maximize their savings with minimal effort.

Debit Card and Bank Account Rewards

While less common and typically less lucrative than credit card offers, some debit cards and bank accounts do offer cash back rewards.

- Specific Spending Patterns: These programs might offer a small percentage back on certain categories (e.g., gas, groceries) or require linking your card to specific merchant offers.

- Direct Deposit Requirements: Some checking accounts offer rewards for maintaining a certain balance or setting up direct deposit, occasionally including cash back incentives.

- Local Bank Offers: Smaller regional banks or credit unions sometimes have unique local merchant offers tied to their debit cards.

These options can complement a broader cash back strategy, especially for those who prefer using a debit card for everyday spending or want to capitalize on specific local deals.

Maximizing Your Cash Back Earnings: A Financial Strategy

Earning cash back is one thing; optimizing it to significantly impact your financial health is another. It requires a strategic approach, a keen eye for detail, and a commitment to responsible spending.

Stacking Rewards Effectively

The key to supercharging your cash back earnings lies in understanding how to combine different programs. This “stacking” approach can turn a modest return into substantial savings.

- Combining Credit Card Rewards with Shopping Portals: As mentioned, this is often the most lucrative stack. Always check a shopping portal (like Rakuten or TopCashback) before making an online purchase, and then pay with your highest-earning cash back credit card for that purchase.

- Utilizing Merchant-Specific Offers with General Cash Back Cards: Keep an eye out for targeted offers from your credit card company (e.g., “Spend $100 at Target, get $10 back”). These can often be combined with Target’s own loyalty programs or a general cash back card, amplifying your savings.

- Example Scenarios of Optimized Spending: Imagine buying groceries. You might use a credit card offering 5% cash back on groceries this quarter. Then, you scan your store loyalty card for additional discounts or points. Finally, you might check Ibotta for specific item rebates. This layered approach maximizes your return on a single shopping trip.

Avoiding Common Pitfalls

While cash back is a powerful tool, it comes with potential traps that can undermine its benefits if not managed carefully.

- Overspending to Earn Rewards: The most significant pitfall is spending more than you otherwise would, solely for the sake of earning cash back. The 2% you get back is meaningless if you spent 10% more than your budget allowed. Always prioritize needs over rewards.

- Chasing Too Many Cards or Programs: Managing multiple rotating categories, different redemption thresholds, and various loyalty accounts can become overwhelming and lead to missed opportunities or confusion. Focus on a few key programs that align with your natural spending.

- Ignoring Annual Fees or High Interest Rates: A credit card with a high annual fee might only be worthwhile if the rewards significantly outweigh that fee. Similarly, carrying a balance on a rewards card negates any cash back earned, as interest charges will far exceed your returns. Always pay your statement balance in full.

- Understanding Expiration Dates or Minimum Payout Thresholds: Some cash back programs have minimum payout requirements (e.g., $5 for Rakuten, $20 for Ibotta) or points that expire after a certain period. Keep track of these to ensure you don’t lose out on earned rewards.

Tracking and Redeeming Smartly

Effective management of your cash back earnings is crucial to realize their full financial potential.

- Importance of Monitoring Earnings: Regularly check your cash back balances across all platforms. Many credit card apps and shopping portals provide real-time updates.

- Setting Reminders for Rotating Categories: If you use rotating category cards, set calendar reminders for when categories change so you can adjust your spending strategy accordingly.

- Choosing the Best Redemption Option: Consider your financial goals. A statement credit immediately reduces your debt, which is often the most financially sound choice. Direct deposit gives you liquid cash for other needs or investments. Gift cards can offer more value but lock you into specific retailers.

- Integrating Cash Back into a Broader Budget: View cash back as a supplemental income stream or a reduction in expenses. Incorporate anticipated cash back into your budgeting process to get a more accurate picture of your net spending.

The Future of Cash Back and Consumer Finance

The landscape of cash back is continuously evolving, driven by technological advancements and shifting consumer expectations. The future promises even more sophisticated and integrated ways to save.

Emerging Trends

Innovation is constant in the financial tech space, and cash back is no exception.

- AI-Driven Personalized Offers: Artificial intelligence can analyze your spending patterns to offer highly personalized cash back deals that are genuinely relevant to you, maximizing the chances of engagement.

- Blockchain-Based Loyalty Programs: Decentralized ledger technology could offer more secure, transparent, and transferable reward points, potentially allowing for easier exchange or consolidation of rewards across different brands.

- Integration with Budgeting Apps and Financial Planning Tools: Expect seamless integration of cash back earnings directly into your personal finance management apps, providing a clearer, real-time view of your net financial position.

- Hyper-Local Cash Back Initiatives: Geolocation technology could enable more precise, real-time cash back offers from local businesses as you move through your community, fostering local economic activity.

Cash Back in a Digital Economy

The accelerating shift towards a digital-first economy is inherently changing how cash back operates.

- Growth of Mobile Payment Integrations: As mobile wallets become more prevalent, cash back will likely be integrated directly into payment apps, making activation and redemption even smoother.

- Seamless Digital Redemption: The friction of redeeming cash back will continue to decrease, with instant transfers and automated application of credits becoming standard.

- The Role of Data Privacy and Security: As personalization increases, so does the importance of data privacy. Future cash back programs will need to balance personalized offers with robust data protection measures and transparency.

Educating Consumers for Smarter Choices

As the complexity and number of cash back options grow, so does the need for ongoing financial literacy.

- The Ongoing Need for Financial Literacy: Consumers need to understand not just how to earn cash back, but how to do so responsibly, avoiding debt and making informed choices about the best programs for their lifestyle.

- Empowering Individuals to Make Informed Decisions: Financial education empowers individuals to critically evaluate cash back offers, understand terms and conditions, and integrate these tools effectively into their long-term financial planning.

Conclusion

The question “what shop does cash back” opens up a fascinating and financially rewarding world for consumers. From the broad strokes of credit card rewards to the granular detail of online shopping portals and retailer loyalty programs, the opportunities to save money on everyday spending are ubiquitous. Cash back, when approached strategically and responsibly, transcends mere discounts; it becomes a powerful component of a robust personal finance strategy.

By understanding how these programs work, exploring the diverse avenues for earning, and adopting smart maximization techniques, you can transform your spending habits into a consistent source of savings. Remember, the true value of cash back is realized not in the accumulation of points, but in their thoughtful application towards your financial goals. Even small percentages, diligently earned and wisely managed, can accumulate into significant sums over time, contributing meaningfully to your financial well-being. Embrace the landscape of cash back, and let your money work harder for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.