Understanding what $50 an hour translates to in terms of an annual salary is a fundamental step in personal financial planning. While an hourly rate provides a clear picture of immediate earnings, converting it into a yearly figure allows for comprehensive budgeting, tax estimation, and long-term financial goal setting. For many, $50 an hour represents a significant income milestone, opening doors to greater financial stability and investment opportunities.

Calculating the Annual Equivalent of $50 an Hour

The direct conversion of an hourly wage to an annual salary is straightforward, assuming a standard full-time work schedule. However, it’s crucial to differentiate between gross and net income, as taxes and other deductions significantly impact the actual take-home pay.

Hourly to Weekly, Monthly, and Annual Breakdown

Let’s start with the basic calculation:

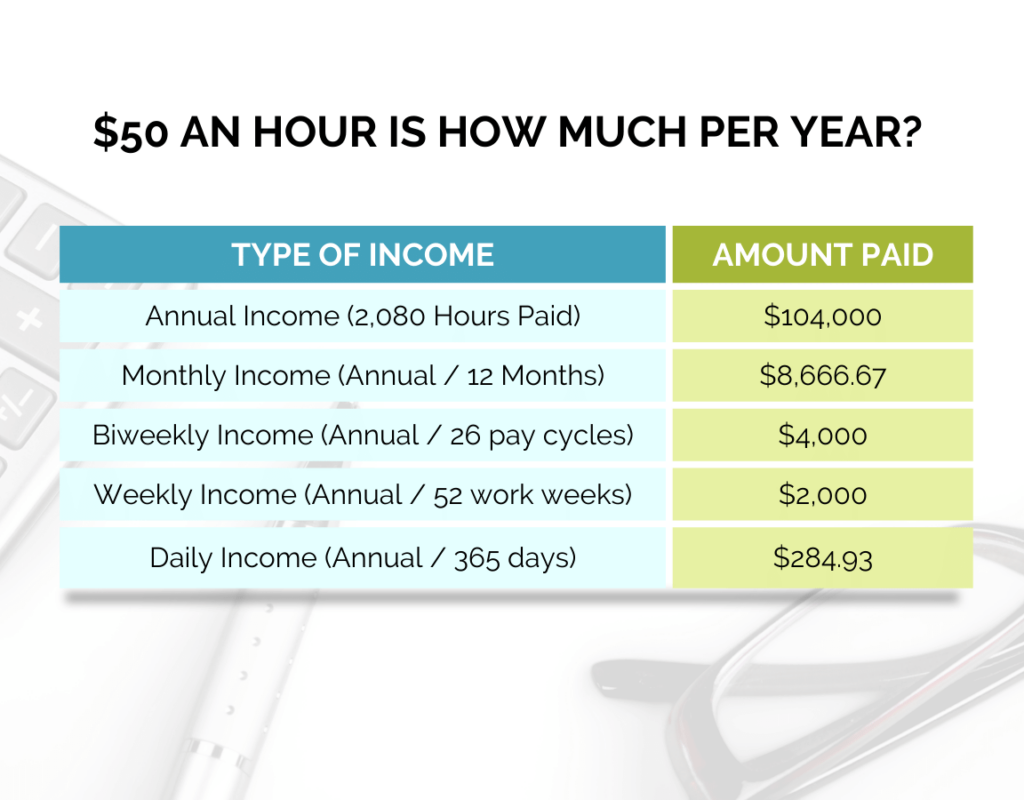

A standard full-time work week typically consists of 40 hours.

- Weekly Income: $50/hour * 40 hours/week = $2,000 per week

- Monthly Income: To estimate monthly income, we can multiply the weekly income by 4.33 (average weeks in a month) or divide the annual income by 12. Using the latter for precision after annual calculation:

- Approximate Monthly: $2,000/week * 4.33 weeks/month = $8,660 per month

- Annual Income (Gross): Assuming a full 52 weeks of work in a year:

- $2,000/week * 52 weeks/year = $104,000 per year

Therefore, a consistent income of $50 per hour translates to a gross annual salary of $104,000. This figure represents your earnings before any deductions are made.

Gross vs. Net Income: The Critical Distinction

While $104,000 sounds substantial, it’s vital to understand that this is your gross income. Your net income, or take-home pay, will be considerably less due to various mandatory and elective deductions. These typically include:

- Federal Income Tax: The amount varies based on your filing status (single, married, head of household) and the number of dependents.

- State and Local Income Tax: Many states and some localities impose their own income taxes, which can range from zero to over 10%.

- FICA Taxes: This includes Social Security (6.2%) and Medicare (1.45%), totaling 7.65% on earnings up to a certain threshold for Social Security, and on all earnings for Medicare. These are withheld from your paycheck.

- Health Insurance Premiums: If provided by your employer, your share of health, dental, and vision insurance premiums is typically deducted pre-tax.

- Retirement Contributions: Contributions to 401(k)s, 403(b)s, or other employer-sponsored retirement plans are usually pre-tax, reducing your taxable income.

- Other Deductions: This could include life insurance, disability insurance, flexible spending accounts (FSAs), health savings accounts (HSAs), or union dues.

After all these deductions, your actual bi-weekly or monthly paycheck will be significantly lower than the gross figures. For instance, in many states, an individual earning $104,000 might see their net pay hover around $6,000-$7,500 per month, depending heavily on the specific tax rates and deduction elections.

The Real Value of $50 an Hour: Beyond the Number

The purchasing power of a $104,000 annual salary is not uniform across all locations or lifestyles. Several factors influence how far this income can stretch, making the “real value” a highly personal metric.

Cost of Living Considerations (Geographic Impact)

A $104,000 salary offers a comfortable standard of living in many parts of the United States and globally, but its relative value diminishes significantly in high-cost-of-living areas. For example:

- High-Cost Cities: In major metropolitan areas like New York City, San Francisco, or Honolulu, where housing, transportation, and daily expenses are exceptionally high, a $104,000 salary might still require careful budgeting to live comfortably, especially for a family. Rent for a modest apartment could consume a substantial portion of net income.

- Average-Cost Cities/Suburbs: In medium-sized cities or suburban areas with moderate living costs, this income level typically allows for a very comfortable lifestyle, including homeownership, discretionary spending, and robust savings.

- Low-Cost Areas: In rural regions or areas with a lower cost of living, $104,000 per year can provide a luxurious standard of living, enabling significant savings, investments, and a greater capacity for leisure.

It’s crucial to research the cost of living index for your specific location or target location when evaluating the adequacy of a $50/hour income.

Tax Implications and Deductions

The progressive nature of income tax means that a higher salary places you in a higher tax bracket, though only the portion of your income within that bracket is taxed at the higher rate. Beyond federal and state income taxes, understanding potential deductions and credits can significantly impact your net income. Utilizing tax-advantaged accounts like 401(k)s and IRAs, as well as being aware of eligible deductions for student loan interest, mortgage interest, or medical expenses, can reduce your overall tax burden. Financial planning with a tax professional is highly recommended to optimize your tax strategy.

Benefits and Compensation Packages

The value of an hourly wage isn’t solely determined by the numerical rate. A comprehensive benefits package can add substantial value, often equivalent to 20-40% of your base salary. When evaluating a $50/hour job, consider:

- Health Benefits: Employer-sponsored health, dental, and vision insurance can save thousands annually in premiums and out-of-pocket costs.

- Retirement Matching: A company match on 401(k) contributions is essentially free money and a powerful tool for wealth accumulation.

- Paid Time Off (PTO): Vacation days, sick leave, and holidays represent paid time when you are not working, maintaining your income stability.

- Life and Disability Insurance: Employer-provided policies offer financial security.

- Other Perks: Tuition reimbursement, professional development opportunities, gym memberships, and transit subsidies all contribute to the overall compensation value.

A job paying $45/hour with excellent benefits might offer a better overall financial package than a $50/hour job with minimal or no benefits.

Budgeting and Financial Planning with a $50/Hour Income

Earning $104,000 annually provides a strong foundation for robust financial planning. Effective budgeting is key to maximizing this income for both current comfort and future security.

The 50/30/20 Rule Applied

A popular and effective budgeting framework is the 50/30/20 rule:

- 50% for Needs: This portion of your net income goes towards essential expenses like housing (rent/mortgage), utilities, groceries, transportation, and minimum loan payments. For someone with a net monthly income of, say, $6,500, this would be $3,250.

- 30% for Wants: This covers discretionary spending like dining out, entertainment, hobbies, travel, and non-essential shopping. This would equate to $1,950 from our example net income.

- 20% for Savings & Debt Repayment: This crucial portion is dedicated to building an emergency fund, investing for retirement, making extra payments on debt (beyond minimums), and saving for other financial goals. This would be $1,300.

Adhering to this rule, or a similar structured budget, helps prevent lifestyle creep and ensures a significant portion of your income is directed towards wealth building.

Building an Emergency Fund

With a $50/hour income, building a robust emergency fund should be a top priority. This fund, typically held in a high-yield savings account, should cover 3-6 months of essential living expenses. Given a comfortable income, aiming for 6-12 months of expenses provides even greater security against unexpected job loss, medical emergencies, or large unforeseen expenditures.

Debt Management Strategies

While a $104,000 salary makes minimum debt payments manageable, it also provides the bandwidth to accelerate debt repayment, particularly high-interest debts like credit card balances or personal loans. Strategies include:

- Debt Snowball: Pay off the smallest debt first to gain psychological momentum.

- Debt Avalanche: Focus on paying off debts with the highest interest rates first to minimize total interest paid.

- Refinancing: Consider refinancing student loans or personal loans for lower interest rates if eligible.

Eliminating consumer debt frees up substantial cash flow for saving and investing, dramatically improving your financial position.

Leveraging a $50/Hour Income for Wealth Building

A $50/hour income places you in a strong position to build significant wealth over time through strategic saving and investing.

Retirement Savings (401k, IRA)

Maximizing contributions to retirement accounts is paramount.

- 401(k)/403(b): If your employer offers a matching contribution, contribute at least enough to get the full match – it’s a 100% return on your investment. Aim to contribute the maximum allowable amount ($23,000 for 2024, plus catch-up contributions for those 50 and over) if feasible. These contributions are pre-tax, reducing your current taxable income.

- Individual Retirement Accounts (IRAs): Consider contributing to a Traditional or Roth IRA. Roth IRAs are particularly attractive for those who expect to be in a higher tax bracket in retirement, as contributions are post-tax, but qualified withdrawals are tax-free.

- Health Savings Accounts (HSAs): If you have a high-deductible health plan, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. It can also function as an additional retirement investment vehicle.

Diversified Investment Strategies

Beyond retirement accounts, consider investing in a diversified portfolio to grow your wealth.

- Brokerage Accounts: Open a taxable brokerage account to invest in a mix of exchange-traded funds (ETFs), mutual funds, and individual stocks. Diversification across different asset classes (stocks, bonds, real estate) and geographies is crucial to mitigate risk.

- Robo-Advisors: For those new to investing or preferring a hands-off approach, robo-advisors can build and manage a diversified portfolio tailored to your risk tolerance.

- Real Estate: With a stable income, exploring real estate investments, whether through direct property ownership, real estate investment trusts (REITs), or crowdfunding platforms, can be a powerful way to build equity and generate passive income.

Regular, consistent investing, even modest amounts, benefits greatly from the power of compound interest over time.

Financial Planning for Future Goals

Beyond retirement, a $50/hour salary enables you to plan for other significant life goals:

- Homeownership: Saving for a down payment becomes much more achievable.

- Children’s Education: Funding 529 plans for college savings.

- Large Purchases: Saving for cars, major home renovations, or dream vacations.

- Philanthropy: Contributing to causes you care about.

Regularly reviewing and adjusting your financial plan with a certified financial planner can help ensure you stay on track to achieve these aspirations.

Achieving and Maintaining a $50/Hour Income

While the initial question focused on the financial implications of earning $50 an hour, it’s also worth briefly considering the path to achieving and maintaining such an income. This income level typically requires a combination of specialized skills, education, experience, and strategic career management.

In-Demand Skills and Industries

Roles commanding $50/hour or more often exist in industries with high demand for specific expertise. This includes:

- Technology: Software development, data science, cybersecurity, cloud architecture, IT project management.

- Healthcare: Experienced nurses (especially in specialized fields), physician assistants, medical technologists, certain therapists.

- Engineering: Electrical, mechanical, civil, and software engineers with experience.

- Finance: Financial analysts, accountants (CPA), investment managers.

- Consulting: Management consultants, IT consultants.

- Specialized Trades: Highly skilled and experienced electricians, plumbers, welders, often working as independent contractors.

Continuous learning and skill development are crucial to remain competitive and increase earning potential in these fields.

Negotiation and Salary Growth

Achieving a $50/hour rate often involves effective salary negotiation, both when accepting a new role and during annual reviews. Researching market rates for your specific role and location, articulating your value proposition, and being prepared to advocate for yourself are vital. Regularly updating your resume, networking, and potentially exploring new opportunities can also contribute to sustained income growth and ensure your earnings keep pace with your skills and the market.

In conclusion, $50 an hour translates to a significant gross annual salary of $104,000. While impressive, its true financial impact is shaped by net income after taxes and deductions, local cost of living, and the benefits package. With diligent budgeting, strategic debt management, and proactive investment, this income level provides a powerful platform for achieving robust financial security and long-term wealth accumulation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.