Deciding what percentage of your salary to contribute to your 401k can feel like navigating a dense financial jungle. It’s a question that resonates with employees across all career stages, from fresh graduates to seasoned professionals nearing retirement. While there’s no single “magic number” that applies to everyone, understanding the principles behind 401k contributions and tailoring them to your personal circumstances is a cornerstone of sound financial planning. This guide will demystify the process, helping you formulate a robust strategy for securing your financial future.

Understanding the 401k Basics and Its Unmatched Power

Before diving into percentages, it’s crucial to grasp the fundamental nature of a 401k and why it’s often hailed as one of the most powerful retirement savings vehicles available. It’s more than just a savings account; it’s a tax-advantaged investment tool designed to help you build wealth over decades.

What is a 401k and How Does It Work?

A 401k is an employer-sponsored retirement plan that allows employees to save and invest a portion of their pre-tax or after-tax (Roth) salary. Contributions are automatically deducted from your paycheck, making it a convenient and disciplined way to save. The money is then invested in a range of funds, typically chosen from a menu provided by your plan administrator. Over time, these investments grow, ideally leading to a substantial nest egg by the time you retire. The “401k” designation comes from the section of the Internal Revenue Code that governs these plans.

The Power of Tax Advantages

One of the most compelling features of a 401k lies in its tax benefits. With a traditional 401k, your contributions are made with pre-tax dollars, meaning they reduce your taxable income in the year they are made. This effectively lowers your current tax bill. The investments then grow tax-deferred, meaning you don’t pay taxes on the capital gains, dividends, or interest until you withdraw the money in retirement. This deferral allows your money to compound more aggressively. For Roth 401k contributions, the money is contributed after-tax, but qualified withdrawals in retirement are entirely tax-free. This offers incredible flexibility and a hedge against future tax rate increases.

The Magic of Compounding Returns

Compounding is often called the “eighth wonder of the world,” and nowhere is its effect more evident than in long-term retirement savings. When your investments earn returns, and those returns themselves start earning returns, your money grows exponentially. The earlier you start contributing, the more time your money has to compound, leading to significantly larger sums down the road, even with smaller initial contributions. Every percentage point you contribute, especially early in your career, has a magnified impact over time.

The “Ideal” Contribution Percentage: A Starting Point

While personal situations vary, financial experts often provide general guidelines to help you determine a good starting point for your 401k contributions. These rules of thumb are designed to set you on a path toward a comfortable retirement.

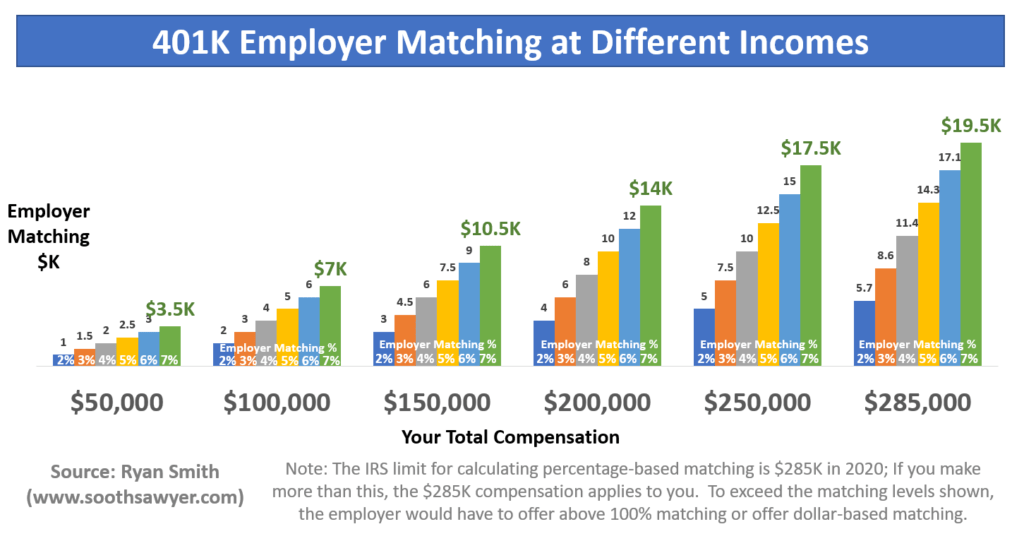

Don’t Leave Free Money on the Table: The Company Match

This is perhaps the most crucial piece of advice for any 401k participant: always contribute at least enough to get your full employer match. Many companies offer to match a certain percentage of your contributions, essentially giving you free money. For example, a company might match 50 cents on the dollar for the first 6% of your salary you contribute. If you contribute less than 6%, you’re leaving a guaranteed 50% return on the table, which is an invaluable boost to your retirement savings. Failing to take advantage of the match is one of the biggest financial mistakes an employee can make.

General Guidelines: The 10-15% Rule

Beyond the company match, a widely recommended guideline for retirement savings is to contribute between 10% and 15% of your gross income, including your employer’s contribution. For instance, if your employer matches 3% and you contribute 7%, you’ve hit the 10% mark. Aiming for the higher end of this range, or even more, positions you better for a more comfortable retirement, especially if you start saving later in life or aspire to an early retirement. This percentage is often considered the sweet spot for balancing present-day expenses with future financial security for most income levels.

The Long-Term Impact of Early Contributions

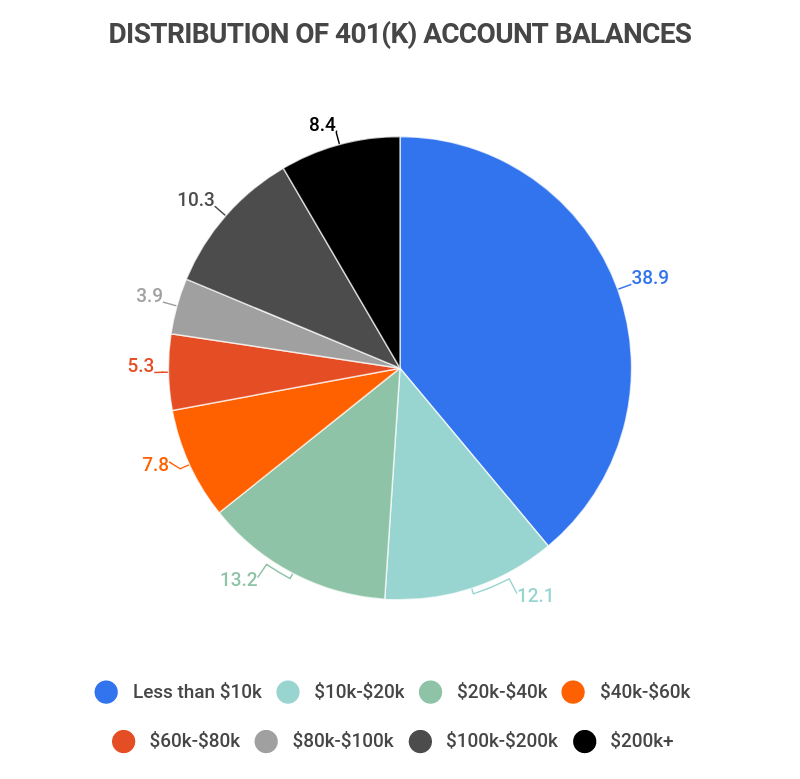

The impact of starting early, even with modest contributions, cannot be overstated. A person who starts contributing 10% at age 25 will likely accumulate significantly more wealth than someone who starts contributing 15% at age 35, simply due to the extended period of compounding. Time in the market is far more important than timing the market. Every year you delay is a year of lost potential growth that can never be fully recovered.

Factors Influencing Your Personalized Contribution Strategy

While general guidelines provide a good starting point, your optimal 401k contribution percentage should ultimately be a personalized strategy. Several key factors related to your individual financial situation and life stage should influence your decision.

Your Age and Retirement Horizon

Your age plays a significant role. If you’re in your 20s or 30s, you have a long runway for your investments to grow, so consistently hitting the 10-15% target can lead to substantial wealth. If you’re in your 40s or 50s and haven’t saved much, you might need to accelerate your contributions, perhaps aiming for 15-20% or even more, to catch up. The closer you are to retirement, the more aggressive your savings rate may need to be to meet your goals.

Current Income and Household Budget

Your current income and expenses are practical constraints. While the ideal is to save more, your budget must allow for it. Start by analyzing your cash flow. Can you comfortably afford to contribute 10-15%? If not, start with what you can – at least the company match – and incrementally increase your contributions by 1% or 2% each time you get a raise until you reach your target. Even small, consistent increases can make a big difference over time without severely impacting your immediate lifestyle.

Debt Management: Balancing Retirement and Repayment

High-interest debt, such as credit card balances or personal loans, can erode your financial progress. While it’s crucial to contribute enough to get the company match, it’s often wise to prioritize aggressively paying down high-interest debt before significantly increasing your 401k contributions beyond that point. The guaranteed return from eliminating high-interest debt often outweighs the potential, but not guaranteed, returns from additional 401k contributions. Once high-interest debt is gone, you can redirect those payments toward your retirement savings. Student loans and mortgages, which typically have lower interest rates, can often be managed concurrently with robust 401k contributions.

Other Financial Goals: Homeownership, Education, Emergency Fund

Retirement isn’t your only financial goal. You might be saving for a down payment on a house, your children’s education, or building a robust emergency fund. It’s essential to strike a balance. Financial advisors typically recommend having an emergency fund covering 3-6 months of living expenses before focusing entirely on maximizing retirement contributions. Once your emergency fund is solid, you can allocate funds to other goals while maintaining consistent 401k contributions. Your budget might need to allocate funds across multiple buckets simultaneously.

Optimizing Your 401k Contributions for Maximum Impact

Once you’ve established your foundational contribution strategy, there are further steps you can take to optimize your 401k and ensure it’s working as hard as possible for your financial future.

Aiming for the Maximum: Contribution Limits

The IRS sets annual limits on how much you can contribute to your 401k. For 2024, the employee contribution limit is $23,000 (this figure typically adjusts annually for inflation). If you have the financial capacity to “max out” your 401k, it’s an excellent strategy, particularly for high-income earners. This maximizes your tax-advantaged growth and accelerates your path to retirement. Be aware that the total contribution limit (employee + employer contributions) is much higher, also adjusting annually.

Traditional vs. Roth 401k: Which is Right for You?

Many employers offer both traditional and Roth 401k options. The choice depends on your current tax situation and your expectations for future tax rates.

- Traditional 401k: Contributions are pre-tax, reducing your current taxable income. You pay taxes on withdrawals in retirement. This is generally preferred if you expect to be in a lower tax bracket in retirement than you are now.

- Roth 401k: Contributions are after-tax. Qualified withdrawals in retirement are tax-free. This is generally preferred if you expect to be in a higher tax bracket in retirement, or if you want to diversify your tax exposure in retirement.

For many, a mix of both types of accounts can offer the most flexibility.

Catch-Up Contributions for Older Workers

If you are age 50 or older, the IRS allows you to make additional “catch-up” contributions to your 401k beyond the standard limit. For 2024, this catch-up contribution is an additional $7,500, bringing the total employee contribution limit to $30,500. This is a powerful tool for those who started saving late or want to supercharge their savings in the years leading up to retirement.

Diversifying Your Retirement Portfolio Beyond the 401k

While the 401k is a fantastic tool, it shouldn’t necessarily be your only retirement savings vehicle. Consider diversifying with other accounts like an Individual Retirement Account (IRA) – either traditional or Roth – especially if your employer’s 401k investment options are limited or have high fees. Health Savings Accounts (HSAs), if available through your health plan, can also serve as a triple-tax-advantaged retirement savings tool (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses).

Reviewing and Adjusting Your Contributions Over Time

Financial planning is not a “set it and forget it” endeavor. Your life, income, and financial goals will evolve, and your 401k contribution strategy should adapt accordingly.

Annual Financial Check-ups

Make it a habit to review your 401k contributions and overall financial plan at least once a year. This is an opportune time to:

- Increase your contribution percentage: Especially after a raise or bonus. Even a 1% increase can significantly impact your long-term wealth.

- Rebalance your investment portfolio: Ensure your asset allocation still aligns with your risk tolerance and time horizon.

- Check fee structures: Be aware of any administrative or fund management fees that might be eating into your returns.

Responding to Life Changes

Major life events should trigger a review of your 401k strategy:

- Marriage or divorce: Could impact household income, expenses, and beneficiary designations.

- Birth of a child: May necessitate saving for college in addition to retirement.

- New job: Always assess the new employer’s 401k plan, including the match, investment options, and vesting schedule.

- Large inheritance or windfall: An opportunity to significantly boost your retirement savings.

The Importance of Professional Guidance

While this guide provides a comprehensive overview, personal finance can be complex. Consulting with a qualified financial advisor can provide invaluable personalized advice. An advisor can help you:

- Create a holistic financial plan that integrates your 401k with other goals.

- Optimize your investment choices within your 401k.

- Navigate complex tax implications and estate planning.

- Stay disciplined and on track with your long-term objectives.

In conclusion, the question “what percentage to 401k” is deeply personal, yet universally important. By understanding the core benefits of a 401k, leveraging employer matching, adhering to general savings guidelines, and continuously adapting your strategy to your evolving life circumstances, you can confidently build a robust foundation for a secure and comfortable retirement. Start today, stay consistent, and watch the power of compounding transform your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.