In the world of business finance and retail operations, few metrics are as frustrating or as closely watched as “shrink.” Shrinkage, the difference between the inventory recorded on the balance sheet and the actual physical inventory on hand, represents a direct hit to a company’s bottom line. While many business owners and investors immediately picture masked shoplifters or organized retail crime when they hear the term, a significant portion of these losses comes from within. Understanding what percentage of shrink is caused by employees is not just an exercise in statistics; it is a critical component of financial management and protecting profit margins.

Decoding Retail Shrinkage: A Financial Perspective

To understand the weight of internal theft, one must first view shrinkage through a purely financial lens. In corporate finance, inventory is an asset. When that asset disappears without a corresponding revenue entry, it is a “leak” in the financial bucket that cannot be easily patched with marketing or sales volume.

Defining Shrinkage in the Modern Business Landscape

Shrinkage is an umbrella term that encompasses several types of loss: shoplifting (external theft), employee theft (internal theft), administrative errors, and vendor fraud. From a financial reporting standpoint, shrink is often discovered during annual or quarterly audits and physical inventory counts. When the numbers don’t align, the business must write off the value of the missing goods, which directly reduces the Net Income and lowers the valuation of the company’s current assets.

Why Every Basis Point Matters for Profitability

For high-volume, low-margin businesses like grocery stores or discount retailers, a shrinkage rate of even 2% can be devastating. Consider a retail chain with a 5% net profit margin. If that store loses $10,000 to internal theft, it doesn’t just lose $10,000 in “cost of goods.” To recoup that $10,000 loss and return to the same financial standing, the store must generate an additional $200,000 in sales. This is why financial officers prioritize loss prevention as a key strategy for increasing EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization).

What Percentage of Shrink is Caused by Employees?

The data regarding internal theft is often surprising to those outside the retail finance sector. While shoplifting often receives the most media attention, employee theft is frequently more systemic, harder to detect, and more costly per incident.

The Statistics of Internal Dishonesty

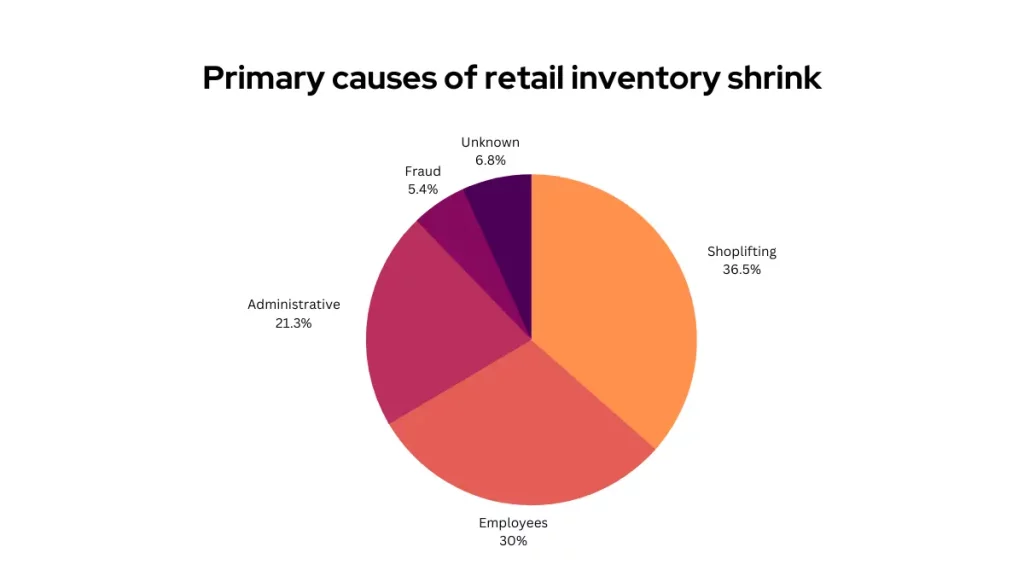

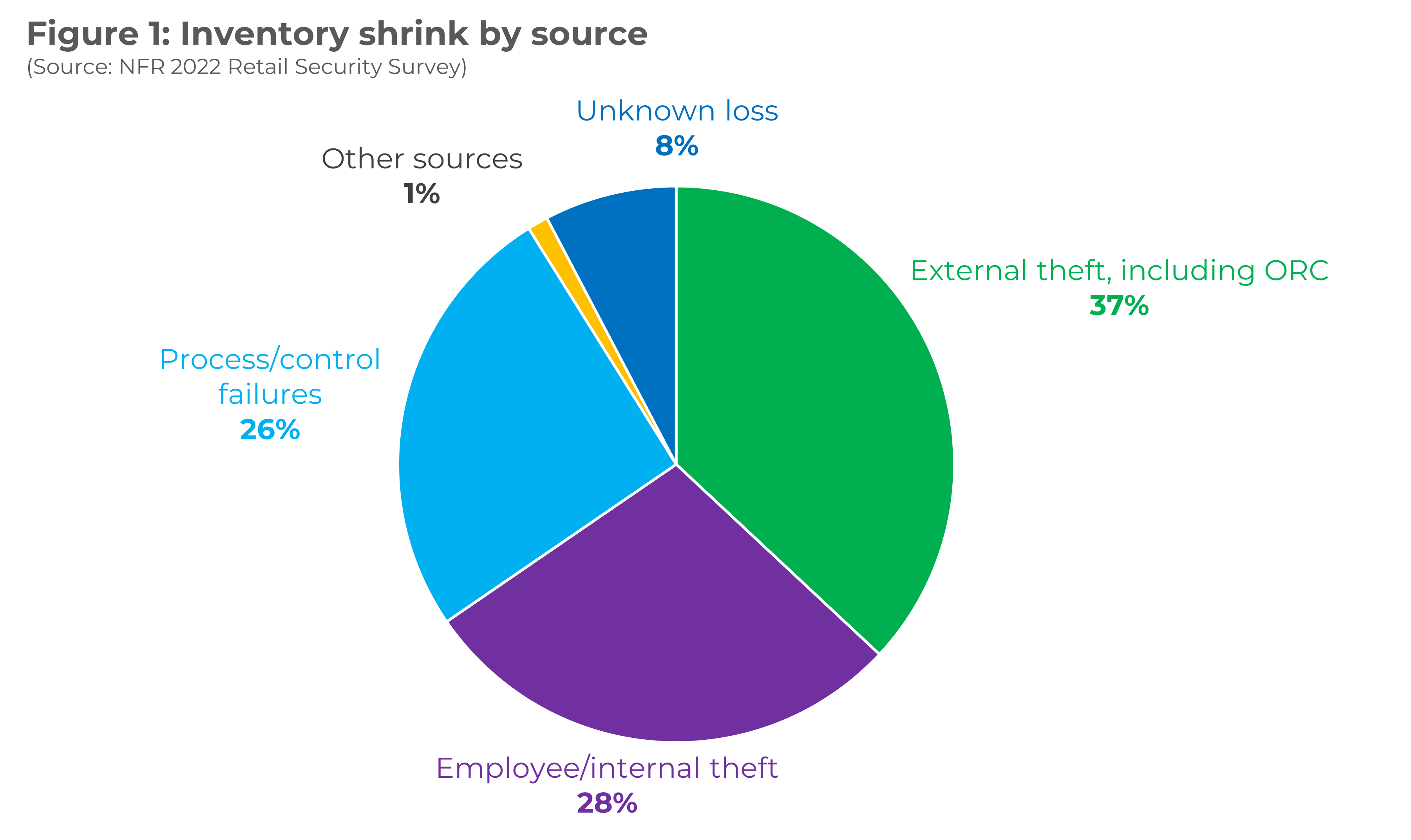

According to long-term studies by the National Retail Federation (NRF) and various retail security surveys, internal theft consistently accounts for a massive portion of total shrinkage. Historically, the percentage of shrink caused by employees typically hovers between 28% and 33%.

In some years, particularly during economic downturns or shifts in labor market dynamics, this number has been known to climb even higher. While external theft (shoplifting) often accounts for a slightly larger slice of the pie (around 36-38%), the average value of a single internal theft incident is significantly higher than that of an external one. A shoplifter might take one item; a dishonest employee with access to the POS system or the warehouse can siphon off thousands of dollars over months or even years.

Comparing Employee Theft vs. Shoplifting vs. Administrative Errors

To understand the financial risk, we must break down the “Big Three” of shrinkage:

- External Theft (approx. 37%): Driven by shoplifters and organized retail crime. It is high-frequency but often low-value per incident.

- Internal Theft (approx. 29%): Driven by employees. It is lower frequency than shoplifting but involves higher-value items or cash, and it is much harder to catch because the perpetrator knows the “blind spots” in the system.

- Administrative/Paperwork Errors (approx. 21%): This is the “hidden” shrink. It isn’t theft, but rather poor financial record-keeping, pricing errors, or shipping mistakes that manifest as missing value on the balance sheet.

The Hidden Costs of Internal Shrinkage

The financial damage caused by employee theft extends far beyond the price tag of the stolen item. For a business to remain financially healthy, it must account for the secondary and tertiary costs associated with internal leakage.

Beyond the Direct Loss: Operational Inefficiencies

When an employee steals inventory, it creates a ripple effect in the supply chain. The automated inventory management system believes the item is still in stock, so it doesn’t trigger a reorder. When a customer comes in to buy that item and finds the shelf empty, the business loses a sale—and potentially a long-term customer. This “out-of-stock” cost is a ghost that haunts retail financial statements, leading to inaccurate forecasting and wasted labor hours spent looking for “phantom inventory.”

Impact on Capital Allocation and Growth

Every dollar lost to internal shrink is a dollar that cannot be reinvested into the business. For a growing startup or a scaling brand, high shrinkage rates can scare off investors or lead to higher interest rates from lenders who view the business as “high risk” due to poor internal controls. In the world of business finance, shrink is viewed as a sign of operational weakness. Reducing internal theft by just 10% can free up enough capital to fund a new marketing campaign or upgrade a digital storefront.

Identifying the Vulnerabilities in Business Finance Systems

To mitigate the percentage of shrink caused by employees, financial managers must identify where the money is actually leaking. Most internal theft occurs at the intersection of inventory and cash handling.

Point of Sale (POS) Discrepancies and “Sweethearting”

The POS system is the most common site for internal financial fraud. “Sweethearting” is a common practice where an employee rings up a friend or accomplice but fails to scan all the items or applies unauthorized discounts. Financially, this looks like a legitimate transaction on the surface, but it results in a slow bleed of inventory. Other methods include “voiding” transactions after the customer has paid in cash and pocketing the difference, or issuing fraudulent returns to a personal gift card.

Inventory Management and Back-of-House Leakage

The warehouse and receiving dock are high-risk areas for bulk theft. Employees may intentionally miscount incoming shipments or “accidentally” damage items to justify throwing them away, only to retrieve them from the dumpster later. From a financial auditing perspective, these losses are often categorized as “damages,” masking the reality of the theft and making it difficult for the finance team to identify the true cause of the margin erosion.

Strategic Financial Controls to Mitigate Employee Theft

Lowering the percentage of internal shrink requires more than just security cameras; it requires robust financial systems and a culture of transparency.

Implementing Robust Auditing Processes

Regular, unannounced financial audits are the most effective deterrent to internal theft. When employees know that the books are being scrutinized and that physical inventory counts are reconciled against POS data weekly rather than annually, the “opportunity” component of the fraud triangle (Pressure, Opportunity, Rationalization) is significantly reduced. Modern AI-driven financial tools can now flag “exceptions” in POS data—such as a specific employee performing an unusually high number of “no-sale” drawer openings—allowing management to intervene before the financial loss scales.

Cultivating a Culture of Accountability

From a brand and corporate identity perspective, how a company treats its employees significantly impacts the “Rationalization” part of the theft equation. Employees who feel underpaid, undervalued, or see their supervisors cutting corners are more likely to justify stealing from the company.

Financially, investing in competitive wages and employee profit-sharing programs can actually save money by reducing shrink. When an employee feels like a stakeholder in the business, they are less likely to steal from it and more likely to report others who do. This “peer-to-peer” accountability is a powerful, low-cost financial control that protects the bottom line.

Conclusion: The Bottom Line on Internal Shrink

While the headline-grabbing stories often focus on brazen shoplifting raids, the data is clear: nearly 30% of retail shrinkage is an inside job. For anyone managing business finances, this is a call to action. Internal theft is a controllable variable. By implementing tighter POS controls, conducting regular inventory audits, and fostering a healthy corporate culture, businesses can significantly reduce their shrinkage rates.

In an era of tightening margins and economic volatility, protecting your assets from internal “leaks” is one of the most direct ways to ensure long-term financial stability and profitability. Shrink is not just an operational nuisance; it is a financial challenge that requires a strategic, data-driven response.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.