The intersection of migration and social safety nets is a cornerstone of modern economic discourse. For investors, policymakers, and taxpayers, understanding the financial mechanics of the Social Security system—specifically how it interacts with foreign-born populations—is essential for accurate financial forecasting and personal retirement planning. One of the most frequent questions in the realm of public finance is: what percentage of migrants are actually drawing social security benefits?

To answer this, we must look beyond political rhetoric and examine the data provided by the Social Security Administration (SSA), the Congressional Budget Office (CBO), and various economic research institutions. The reality is a complex tapestry of legal eligibility, work history requirements, and significant net contributions to the trust funds that often go unrecognized in general financial reporting.

The Legal Framework: Eligibility Criteria for Non-Citizens

Before discussing percentages, it is vital to establish the financial “rules of the game.” Social Security is not a universal entitlement; it is a contributory social insurance program. To understand the volume of migrants receiving benefits, one must first understand the high bar set for eligibility.

“Qualified Alien” Status and the 1996 Reform

The Personal Responsibility and Work Opportunity Reconciliation Act (PRWORA) of 1996 fundamentally changed how non-citizens interact with federal benefits. Under current law, only “qualified aliens”—a category that includes lawful permanent residents (Green Card holders), refugees, and asylees—are potentially eligible for Social Security benefits.

Crucially, unauthorized or undocumented migrants are legally barred from receiving Social Security benefits, regardless of whether they have paid into the system using a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN). From a financial management perspective, this creates a one-way flow of capital for this specific demographic: they contribute to the system’s solvency without the ability to draw from it.

The 40 Quarters (10-Year) Work Requirement

Even for legal migrants, the path to drawing benefits is long. Like U.S.-born citizens, migrants must generally accumulate 40 “credits” to qualify for retirement benefits. Since a maximum of four credits can be earned per year, this necessitates at least ten years of covered employment.

For many migrants who arrive later in life, achieving this threshold is a significant hurdle. This requirement ensures that those drawing from the fund have made a decade-long financial commitment to the American economy. When analyzing the percentage of migrants drawing benefits, we find a natural “lag” compared to native-born citizens who have a 40-to-45-year window to accumulate these credits.

Statistical Breakdown: Percentage of Migrants Drawing Benefits

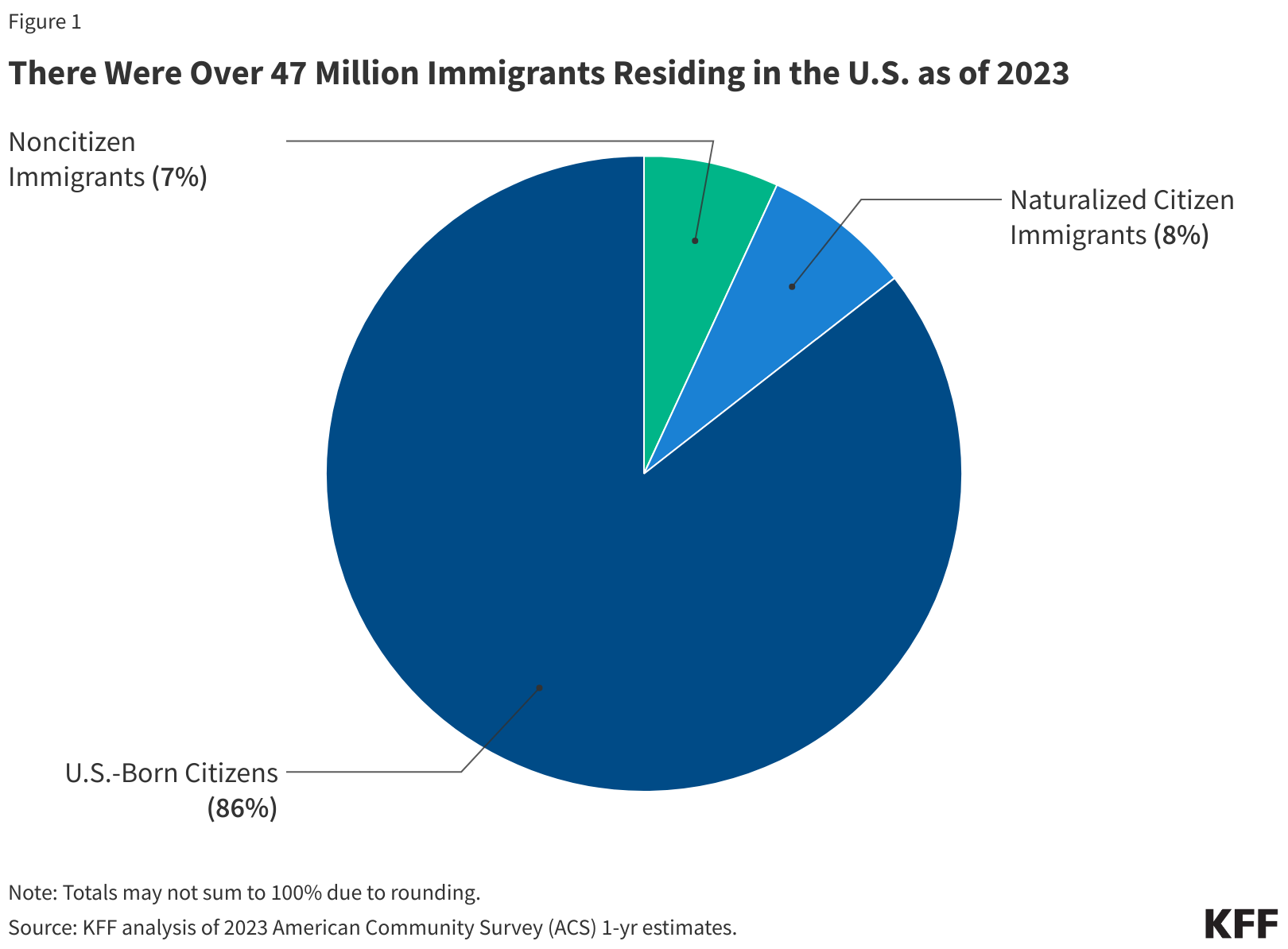

When we look at the raw data, the percentage of migrants receiving benefits is lower than that of the native-born population. According to U.S. Census Bureau and SSA data, while immigrants make up approximately 14% to 15% of the total U.S. population, they do not represent a proportional share of Social Security beneficiaries.

Naturalized Citizens vs. Non-Citizen Residents

To get an accurate financial picture, we must distinguish between naturalized citizens and non-citizen residents. Naturalized citizens draw benefits at rates very similar to native-born citizens because they typically have longer work histories in the U.S. and have fully integrated into the financial system.

However, among non-citizen legal residents, the percentage drawing benefits is remarkably low. Data suggests that only about 3% to 5% of non-citizens receive Social Security benefits at any given time. This is largely because the migrant population in the U.S. is skewed toward “working-age” individuals. Economically speaking, migrants are often in their peak earning years, meaning they are currently in the “accumulation phase” of the financial lifecycle rather than the “distribution phase.”

Why the Numbers Are Often Lower Than Public Perception

Public perception often misses the demographic reality of migration. Migration is frequently a self-selecting process of the young and able-bodied. Consequently, the “dependency ratio” (the number of retirees compared to the number of workers) is actually improved by the presence of migrants.

In a traditional financial model, a healthy Social Security system requires a large base of workers to support a smaller group of retirees. Because the percentage of migrants who are elderly is significantly lower than the percentage of native-born Americans who are elderly, migrants as a group act as a net “creditor” to the Social Security Trust Fund during their primary years in the country.

The Paradox of the Undocumented: Paying In Without Taking Out

From a purely fiscal and business finance perspective, the role of undocumented migrants in the Social Security system is one of the most interesting anomalies in modern economics.

Contributions to the Social Security Trust Fund

Every year, the SSA’s Office of the Chief Actuary calculates the impact of “unauthorized workers” on the Social Security Trust Funds. Because many undocumented workers use SSNs that do not match their identities—often for the purpose of tax compliance and employment—their payroll taxes are diverted into the “Earnings Suspense File” (ESF).

The financial impact is staggering. It is estimated that undocumented workers contribute roughly $12 billion to $15 billion annually to the Social Security system. Because these individuals are ineligible to draw benefits, these funds remain in the system, effectively subsidizing the retirement of legal residents and citizens. For a system facing long-term solvency challenges, this infusion of “non-claimable” capital is a critical, if controversial, financial cushion.

Use of ITINs and Synthetic Identities

While some may assume that lack of legal status means a lack of participation in the financial system, the use of Individual Taxpayer Identification Numbers (ITINs) allows for significant tax compliance. While ITINs do not grant Social Security eligibility, they facilitate the payment of payroll taxes. This reinforces the “Money” niche reality: a high percentage of the migrant population is paying into the benefit pool, while a relatively small percentage is drawing from it.

Financial Impact on the Social Security Administration (SSA)

To understand the macro-financial health of the SSA, one must look at “Totalization Agreements” and the long-term actuarial projections that account for migration patterns.

Totalization Agreements with Foreign Nations

The U.S. has entered into “Totalization Agreements” with nearly 30 countries, including Canada, Mexico, and much of Western Europe. These are essentially bilateral financial treaties designed to prevent double taxation. They allow workers who split their careers between two countries to “totalize” their work credits so they can qualify for a partial benefit in one or both countries.

For a migrant from a totalization-partner country, the percentage drawing a benefit might be higher, but the amount of the benefit is often pro-rated based on their specific U.S. earnings. This ensures that the financial drain on the U.S. Treasury is minimized while honoring the international labor market’s fluidity.

Long-term Solvency Projections

In the world of personal finance and retirement planning, the “Solvency Date” of Social Security (currently projected in the mid-2030s) is a major concern. Actuaries consistently note that net migration is a net positive for the fund’s longevity. Migrants tend to have higher fertility rates and enter the workforce immediately, providing the immediate cash flow needed to pay out the “Baby Boomer” generation’s benefits. Without the current level of migrant participation in the labor force, the “percentage” of people drawing benefits compared to those paying in would reach a crisis point much sooner.

Strategic Financial Planning for Migrant Families

For migrants who are legally eligible to draw benefits, or for those planning their family’s financial future, navigating the Social Security system requires strategic foresight.

Navigating Retirement Planning for Multi-National Workers

If you are a migrant worker, it is essential to track your “Earnings Record” through the SSA. Errors in reporting can lead to a lower “Primary Insurance Amount” (PIA) upon retirement. Furthermore, understanding the “Windfall Elimination Provision” (WEP) is crucial. If a migrant receives a pension from a job in their home country where they did not pay U.S. Social Security taxes, their U.S. benefit may be reduced. This is a vital piece of financial planning that many overlook until they reach age 62.

Tax Implications and Compliance

For high-net-worth migrants or those with side hustles, tax compliance is the gatekeeper to future benefits. Ensuring that all income is reported correctly ensures that the 40-quarter requirement is met efficiently. From a business finance perspective, employers of migrant workers must also remain diligent. Proper withholding not only ensures legal compliance but also supports the macro-economic stability of the national insurance pool.

Conclusion: A Net Financial Contribution

The question “what percentage of migrants are drawing social security benefits” often arises from a concern about fiscal sustainability. However, the financial data reveals a counter-intuitive reality: the migrant population, as a whole, is a massive net contributor to the Social Security system.

Due to strict eligibility laws, a younger demographic profile, and the billions of dollars contributed by those ineligible for payouts, migrants actually help stabilize the financial foundation of the system. While a small percentage of legal, long-term residents and naturalized citizens do draw benefits—as is their right after years of contribution—they do so at rates that are mathematically sustainable within the broader context of the American economy. For the savvy investor or the cautious retiree, understanding these nuances is key to a realistic view of the nation’s financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.