Understanding capital gains taxes is crucial for any investor, business owner, or even someone who has sold a significant asset. These taxes represent a portion of the profit realized from the sale of an asset that was acquired for less than its selling price. The “percentage” aspect of capital gains taxes isn’t a single, fixed number; rather, it’s a variable that depends on a number of factors, primarily the holding period of the asset and your overall taxable income. This article will delve into the intricacies of capital gains tax rates, explaining how they are determined and how they can impact your investment decisions.

Understanding the Fundamentals of Capital Gains

Before dissecting the percentages, it’s essential to grasp what constitutes a capital gain. A capital gain occurs when you sell a capital asset – which can include stocks, bonds, real estate, collectibles, and even cryptocurrency – for more than you paid for it. The difference between the selling price and your “cost basis” (typically the original purchase price plus any associated costs like commissions or improvements) is your capital gain. Conversely, if you sell an asset for less than your cost basis, you incur a capital loss, which can sometimes be used to offset capital gains or even ordinary income.

The Concept of Capital Assets

The IRS defines a capital asset broadly. For most individuals, common capital assets include:

- Stocks and Bonds: These are perhaps the most frequently discussed assets in the context of capital gains.

- Real Estate: This encompasses your primary residence (though there are exclusions for gains on primary homes), investment properties, and land.

- Cryptocurrencies: Digital assets like Bitcoin and Ethereum are also treated as capital assets.

- Collectibles: This category includes items like art, antiques, stamps, and coins.

- Business Assets (Non-Inventory): Certain assets used in a business, such as equipment or property, can also generate capital gains.

It’s important to note that certain assets are explicitly excluded from being capital assets, such as inventory held for sale in the ordinary course of business, depreciable property used in a trade or business (which is taxed differently), and certain U.S. government publications.

Cost Basis: The Foundation of Your Gain

Your cost basis is the bedrock upon which your capital gain or loss is calculated. For purchased assets, it’s generally the purchase price. However, it can be more complex:

- Inherited Property: The cost basis for inherited property is typically its fair market value on the date of the decedent’s death, or on the alternate valuation date if elected by the executor. This is known as a “step-up in basis.”

- Gifts: If you receive an asset as a gift, your cost basis is usually the donor’s cost basis. However, if the fair market value at the time of the gift is less than the donor’s basis, you may have a different basis for calculating a loss.

- Stock Splits and Dividends: If you own stock that undergoes a stock split or you receive stock dividends, your cost basis per share is adjusted accordingly.

- Improvements to Real Estate: Significant improvements made to a property (e.g., a new roof, a renovated kitchen) can be added to your cost basis, thereby reducing your potential capital gain upon sale.

Accurately tracking your cost basis is paramount for proper tax reporting and minimizing your tax liability.

Long-Term vs. Short-Term Capital Gains

The most significant differentiator in determining the “percentage” of capital gains tax you’ll pay lies in how long you held the asset. The IRS distinguishes between short-term and long-term capital gains, with vastly different tax treatments.

Short-Term Capital Gains

Short-term capital gains are profits from the sale of assets held for one year or less. These gains are taxed at your ordinary income tax rates. This means if your top marginal income tax bracket is 22%, then any short-term capital gains you realize will be taxed at that 22% rate. This can be a significant consideration for active traders or those who frequently buy and sell assets within short timeframes.

Taxed at Ordinary Income Rates: The rationale behind this is that frequent trading is often viewed more as a business activity than a long-term investment strategy. Therefore, the profits are subject to the same progressive tax rates that apply to your wages, salary, or other forms of earned income.

Impact on Overall Taxable Income: Since short-term capital gains are added to your other taxable income, they can push you into a higher tax bracket, further increasing your overall tax burden.

Long-Term Capital Gains

Long-term capital gains are profits from the sale of assets held for more than one year. These gains are subject to more favorable tax rates, which are generally lower than ordinary income tax rates. These preferential rates were introduced to encourage long-term investment and to avoid penalizing individuals for the natural appreciation of assets over time.

Preferential Tax Rates: The IRS has established three tiers for long-term capital gains tax rates: 0%, 15%, and 20%. These rates are determined by your taxable income.

Encouraging Long-Term Investment: The lower tax rates on long-term capital gains incentivize investors to hold onto their assets for longer periods, fostering stability in financial markets and promoting a more patient approach to wealth building.

Determining Your Capital Gains Tax Percentage

As mentioned, the percentage you pay on your capital gains depends on a combination of whether the gain is short-term or long-term, and your overall taxable income.

Short-Term Capital Gains Tax Rates

For short-term capital gains, the tax rate is simply your marginal income tax rate. As of the tax year 2023 (filed in 2024), the federal income tax brackets are:

- 10%: For individuals with taxable income up to $11,000

- 12%: For taxable income between $11,001 and $44,725

- 22%: For taxable income between $44,726 and $95,375

- 24%: For taxable income between $95,376 and $182,100

- 32%: For taxable income between $182,101 and $231,250

- 35%: For taxable income between $231,251 and $578,125

- 37%: For taxable income over $578,125

Note: These brackets are for single filers. Married couples filing jointly and heads of household have different bracket thresholds. It’s crucial to refer to the most current IRS figures for accurate tax planning.

Therefore, if you have $50,000 in short-term capital gains and your ordinary income tax rate is 24%, you will pay $12,000 in federal taxes on those gains (24% of $50,000).

Long-Term Capital Gains Tax Rates

The long-term capital gains tax rates are significantly more favorable. For the tax year 2023 (filed in 2024), these rates are tied to your taxable income as follows:

- 0%: For taxable income up to $44,625 for single filers, or $89,250 for married couples filing jointly.

- 15%: For taxable income between $44,626 and $492,300 for single filers, or between $89,251 and $553,850 for married couples filing jointly.

- 20%: For taxable income above $492,300 for single filers, or above $553,850 for married couples filing jointly.

Again, these thresholds are subject to change and vary based on filing status. Always consult the latest IRS publications.

Let’s illustrate with an example. If you have $50,000 in long-term capital gains and your total taxable income places you in the 15% long-term capital gains bracket, you would owe $7,500 in federal taxes on those gains (15% of $50,000). This is a substantial saving compared to the $12,000 you would have paid on short-term gains in the same scenario.

Additional Taxes to Consider

It’s important to remember that federal capital gains taxes are not the only potential tax liability.

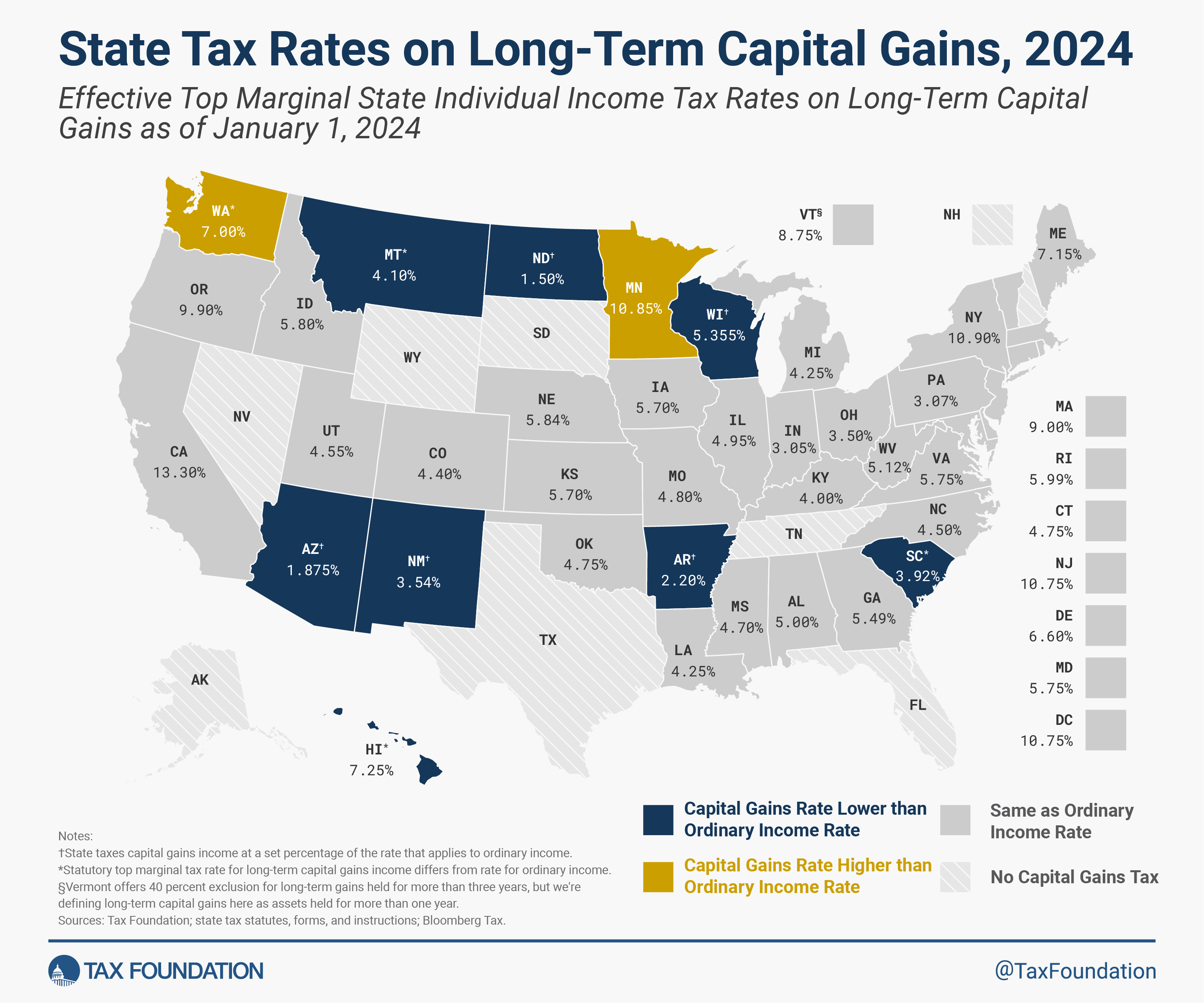

- State Capital Gains Taxes: Many states also impose their own capital gains taxes. These rates vary widely by state, and some states have no capital gains tax at all. For example, California has a progressive capital gains tax system that can reach up to 13.3% in addition to federal taxes. Other states, like Florida and Texas, do not have a state income or capital gains tax.

- Net Investment Income Tax (NIIT): For individuals with higher incomes, the Net Investment Income Tax (NIIT) may apply. This is an additional 3.8% tax on the lesser of your net investment income (which includes capital gains) or the amount by which your modified adjusted gross income (MAGI) exceeds certain thresholds ($200,000 for single filers, $250,000 for married couples filing jointly). This means your total capital gains tax could be 18.8% or 23.8% in certain circumstances.

- Depreciation Recapture: When you sell depreciable real estate or certain business assets, you may have to “recapture” the depreciation deductions you’ve taken over the years. This recaptured amount is taxed at a special rate, typically up to 25%, rather than the lower long-term capital gains rates.

Strategic Implications of Capital Gains Tax Rates

Understanding the nuances of capital gains taxes empowers you to make more informed investment and financial planning decisions.

Holding Period Strategy

The distinction between short-term and long-term capital gains heavily influences the optimal holding period for your investments. If maximizing after-tax returns is a primary goal, holding an asset for over a year to qualify for lower long-term capital gains rates is often a financially advantageous strategy. This is especially true for significant gains.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy where investors intentionally sell assets that have declined in value to realize capital losses. These losses can then be used to offset capital gains realized from the sale of other assets. If your capital losses exceed your capital gains for the year, you can deduct up to $3,000 of those excess losses against your ordinary income. Any remaining losses can be carried forward to future tax years. This strategy can effectively reduce your overall tax liability.

Asset Location

The concept of “asset location” refers to where you hold different types of investments within your portfolio – specifically, whether you hold them in taxable accounts (like a regular brokerage account) or tax-advantaged accounts (like a 401(k) or IRA). Generally, it’s advisable to hold investments that generate a lot of taxable income or frequent capital gains in tax-advantaged accounts to defer or avoid taxation. Conversely, investments that are expected to have slower growth or are less tax-efficient might be better suited for taxable accounts where you can benefit from long-term capital gains rates.

Understanding the Impact of Inflation

While not directly a capital gains tax rate, it’s worth noting that inflation can erode the purchasing power of your gains. When you sell an asset after a long period of appreciation, part of that “gain” might simply be keeping pace with inflation rather than representing true economic growth. The preferential long-term capital gains rates can help offset some of this impact, but it’s a factor to consider in long-term financial planning.

Conclusion

The “percentage” of capital gains taxes is not a static figure but a dynamic calculation influenced by holding periods, income levels, and various other tax provisions. Short-term capital gains are taxed at ordinary income rates, which can be substantial, while long-term capital gains benefit from significantly lower, preferential rates. For investors aiming to optimize their after-tax returns, a thorough understanding of these rates, coupled with strategic planning around holding periods, tax-loss harvesting, and asset location, is indispensable. Staying informed about current tax laws and consulting with a qualified tax professional can ensure you are making the most of your investment journey while minimizing your tax obligations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.