In the world of personal finance, raw numbers often tell only half the story. While a salary of $100,000 might seem substantial, its true value is dictated by the percentages surrounding it: what percent goes to taxes, what percent is consumed by housing, and what percent is redirected into wealth-building assets. Understanding “what percent” is the fundamental key to moving beyond mere survival and toward true financial independence.

Percentages provide a universal language for financial health, allowing individuals at any income level to benchmark their progress and optimize their cash flow. Whether you are a young professional starting your first “real” job or an experienced investor refining a portfolio, the following percentage-based frameworks serve as a roadmap for sustainable wealth.

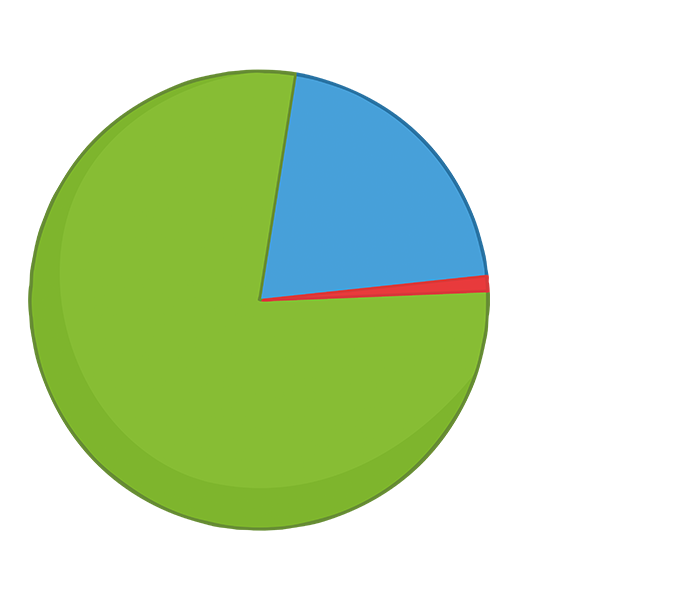

The Core Framework: The 50/30/20 Rule of Budgeting

Budgeting is often viewed as a restrictive exercise in deprivation, but when viewed through the lens of percentages, it becomes a strategic tool for empowerment. The 50/30/20 rule is perhaps the most famous financial guideline, popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi. It provides a simple yet effective way to allocate post-tax income.

Identifying Your Needs (50%)

The first half of your income—exactly 50%—should be dedicated to “needs.” These are the non-negotiable expenses that keep your life functioning. This includes housing (rent or mortgage), utilities, groceries, transportation, insurance, and minimum debt payments.

The challenge many face in modern economies is “lifestyle creep,” where needs are conflated with luxuries. To master this percentage, one must be rigorous in their definitions. A safe place to live is a need; a luxury apartment in the most expensive zip code is a choice. If your needs exceed 50%, it is a signal that your fixed costs are too high, leaving you vulnerable to financial shocks.

Balancing Your Wants (30%)

The 30% category is dedicated to “wants”—the items and experiences that enhance your quality of life but are not essential for survival. This includes dining out, streaming subscriptions, travel, hobbies, and that morning latte.

By capping this at 30%, you create a “guilt-free” spending zone. As long as your needs are met and your savings are prioritized, you can spend this portion of your income without the anxiety that often accompanies discretionary spending. This balance is crucial for long-term psychological sustainability; a budget that allows for zero fun is a budget that will eventually be abandoned.

Prioritizing Savings and Debt Repayment (20%)

The final 20% is the most important for your future self. This portion of your income should be directed toward savings, investments, and debt repayment beyond the minimum requirements. This includes building an emergency fund, contributing to a 401(k) or IRA, and paying down high-interest credit card debt.

This 20% is your wealth-building engine. If you can consistently hit this mark, you are statistically likely to achieve financial security. However, for those aiming for early retirement, this percentage often needs to be significantly higher—a concept we will explore in the context of the “Savings Rate.”

Wealth Accumulation: What Percent Should You Invest?

Once your budget is structured, the question shifts from “how do I survive?” to “how do I grow?” The percentage of your income that you invest is the single greatest predictor of your future net worth—more so than your specific stock picks or your timing of the market.

The 15% Retirement Benchmark

In the financial planning industry, 15% is often cited as the “Golden Percentage” for retirement contributions. If an individual begins investing 15% of their gross income in their mid-20s and places it into a diversified portfolio (such as a low-cost S&P 500 index fund), they are almost guaranteed to retire comfortably by their mid-60s.

This 15% takes advantage of the most powerful force in finance: compound interest. By consistently allocating this percentage, you ensure that you are buying into the market during both highs and lows (dollar-cost averaging), allowing the math of exponential growth to do the heavy lifting over several decades.

Understanding Your Savings Rate as a Wealth Accelerator

While 15% is a solid baseline, the “FIRE” (Financial Independence, Retire Early) movement has popularized the idea of a much higher savings rate. Your savings rate—the percentage of your take-home pay that you keep—dictates your “time to freedom.”

If you save 10% of your income, it takes about nine years of work to save for one year of living expenses. If you save 50% of your income, you save one year of living expenses for every year you work. When the percent of your income saved climbs toward 50% or 60%, the timeline for retirement collapses from 40 years to 10 or 15 years. This highlights why focusing on the percentage is more impactful than focusing on the dollar amount.

Risk Management: Asset Allocation Percentages

How you divide your “investment pie” is just as important as how much you put into it. Asset allocation is the process of deciding what percent of your portfolio should be in different types of investments, such as stocks (equities), bonds (fixed income), and cash.

The “100 Minus Age” Rule

A classic rule of thumb for asset allocation is subtracting your age from 100 to determine what percent of your portfolio should be in stocks. For example, a 30-year-old would hold 70% in stocks and 30% in bonds.

In a modern environment with longer life expectancies and lower bond yields, many advisors have updated this to “110 or 120 minus age.” Regardless of the specific number, the principle remains: your percentage of aggressive assets (stocks) should be higher when you are young to capture growth, and your percentage of conservative assets (bonds) should increase as you approach retirement to protect your capital.

Diversification Across Asset Classes

Beyond the stock/bond split, sophisticated investors look at percentages within their equity holdings. What percent is in domestic vs. international markets? What percent is in large-cap vs. small-cap companies?

A common mistake is “home country bias,” where investors put nearly 100% of their money into their local stock market. Professional portfolio theory suggests that a well-diversified investor should look at global market caps, often resulting in a 60/40 or 70/30 split between domestic and international equities. Maintaining these percentages prevents a single economic downturn in one country from wiping out your entire net worth.

The Exit Strategy: The 4% Rule and Financial Independence

The ultimate goal of tracking percentages is to reach a point where you no longer need to trade your time for money. This is where the “4% Rule” becomes the most important percentage in your life.

Calculating Your Target Portfolio

Derived from the Trinity Study, the 4% Rule suggests that you can safely withdraw 4% of your initial investment portfolio in the first year of retirement (adjusted for inflation thereafter) with a very high probability that your money will last at least 30 years.

This rule allows you to reverse-engineer your “Freedom Number.” If you know your annual expenses, you can multiply them by 25 (the inverse of 4%) to find your target. If you need $50,000 a year to live, you need a portfolio of $1.25 million. By focusing on this percentage, you transform a vague goal of “being rich” into a concrete mathematical objective.

Adjusting for Inflation and Market Volatility

While the 4% Rule is a powerful benchmark, it is not a law of nature. Successful retirees often use a “variable percentage” strategy. If the market is down, they might withdraw only 3%; if the market is up, they might stick to 4% or slightly more. Being flexible with your withdrawal percentage provides a safety buffer that protects against “sequence of returns risk”—the danger of the market crashing right as you begin your retirement.

Debt and Housing: Managing Your Liability Percentages

Finally, we must look at the percentages that represent our liabilities. Debt is often the primary obstacle to wealth, and managing it requires strict adherence to specific ratios.

The 28/36 Rule for Mortgages

Lenders often use the 28/36 rule to determine how much debt a household can safely carry. According to this guideline, your mortgage payment (including principal, interest, taxes, and insurance) should not exceed 28% of your gross monthly income. Furthermore, your total debt-to-income (DTI) ratio—including car loans, student loans, and credit cards—should not exceed 36%.

Exceeding these percentages often leads to being “house poor,” where so much of your income is tied up in a physical asset that you lack the liquidity to invest or handle emergencies.

Credit Utilization: The 30% Ceiling

In the realm of credit scores, the most influential percentage is your credit utilization ratio. This is the percent of your available credit limits that you are actually using. To maintain a high credit score, financial experts recommend keeping this below 30%.

For example, if you have a credit card with a $10,000 limit, carrying a balance of more than $3,000—even if you pay it off in full every month—can negatively impact your score. Mastering this percentage is essential for securing the best interest rates on future loans, which in turn saves you thousands of dollars over a lifetime.

Conclusion

Mastering the “what percent” of your financial life is about more than just math; it is about control. By adhering to the 50/30/20 budget, striving for a 15% investment rate, balancing asset allocation, and respecting debt-to-income ratios, you create a fortress of financial stability. Percentages remove the emotion from money management, providing a clear, objective lens through which to view your progress. Whether you are calculating your withdrawal rate for retirement or your utilization rate for a credit card, these ratios are the compass that will lead you to financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.