The question of “what percent of us is unemployed” is more than just a statistic; it’s a crucial indicator of the economic health of a nation and has profound implications for individuals, businesses, and the broader financial landscape. While the headline itself points to a purely statistical query, its impact reverberates through personal finance, investment strategies, and the overall flow of money within an economy. Therefore, understanding unemployment figures necessitates a deep dive into the financial ramifications they carry.

The Mechanics of Measuring Unemployment: Beyond a Simple Percentage

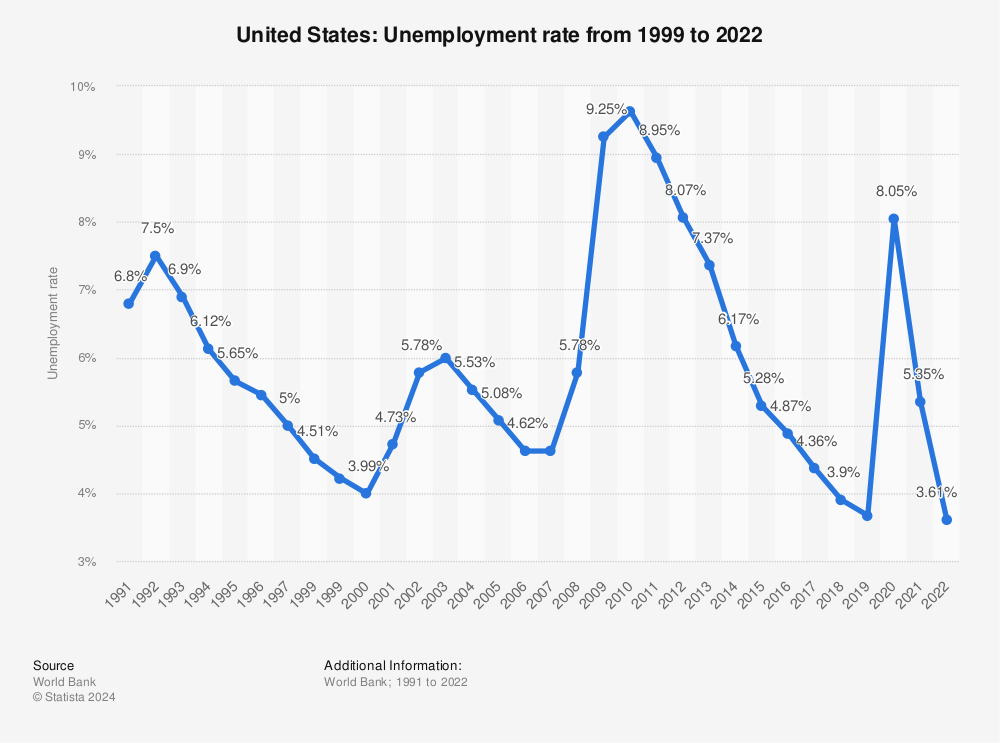

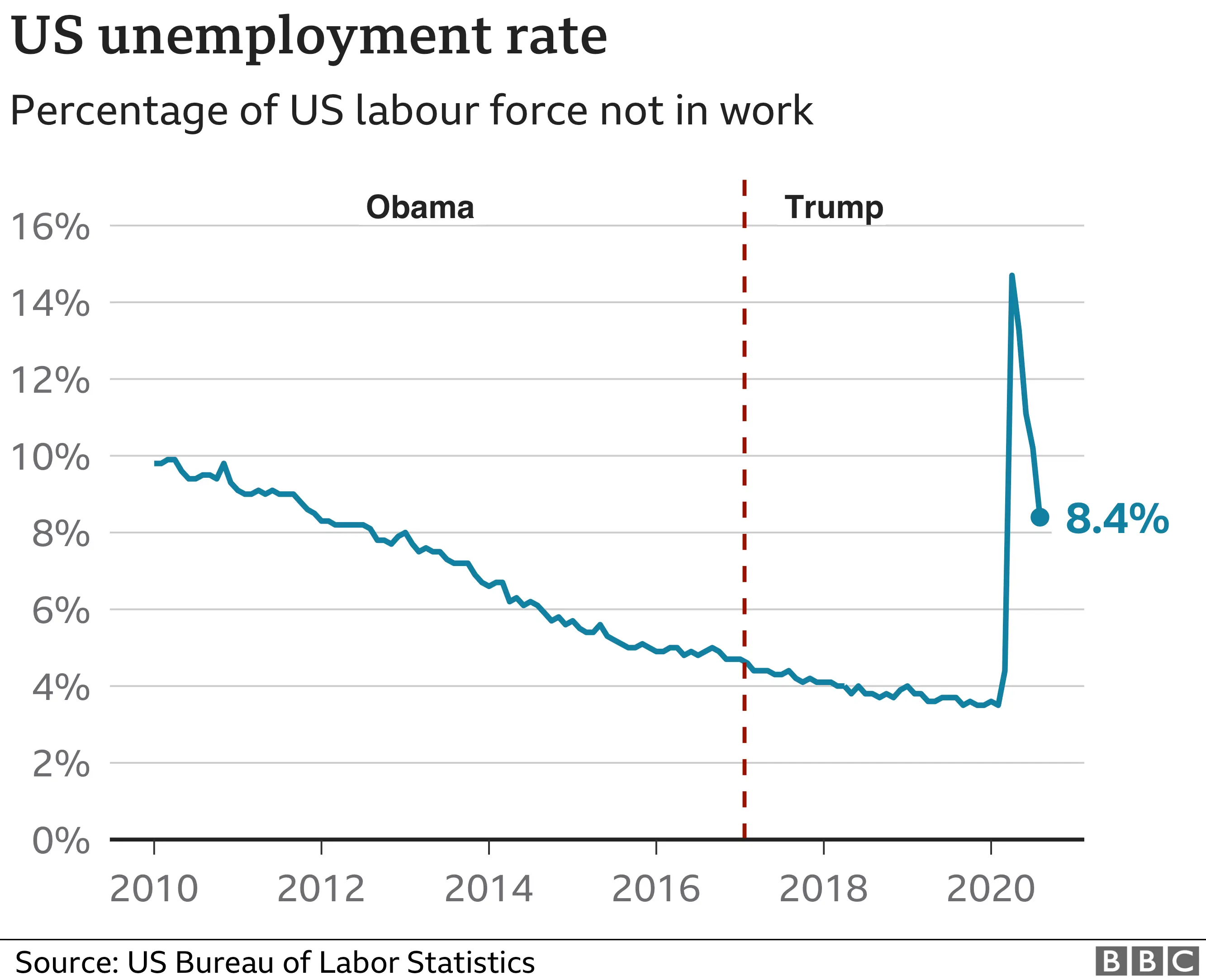

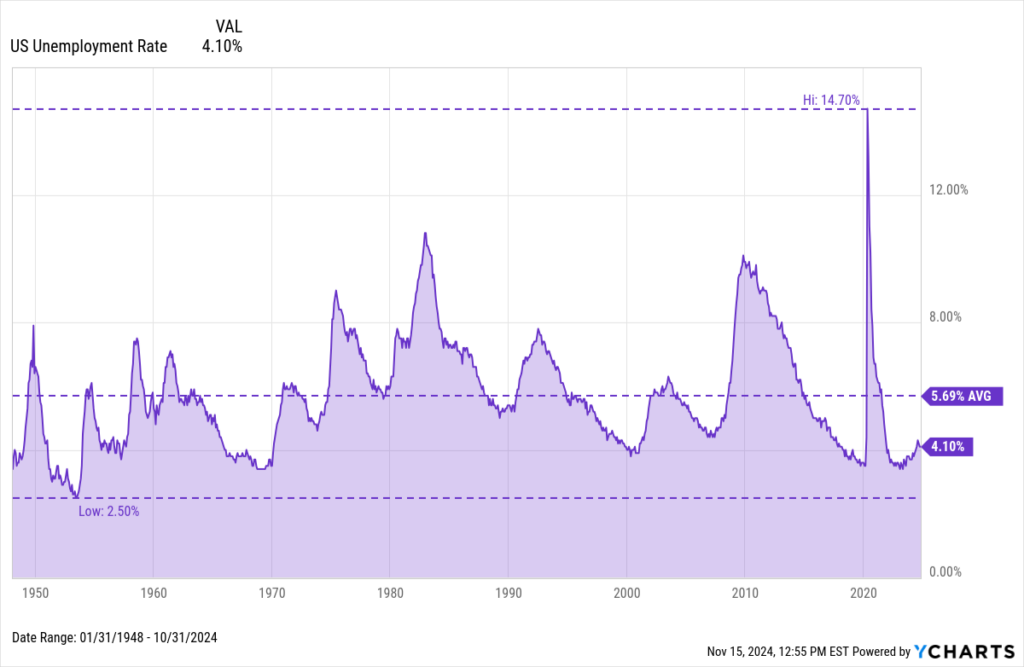

The commonly cited unemployment rate, often referred to as the U-3 rate, is a specific measurement calculated by government agencies. However, to truly grasp the financial implications, it’s essential to understand what goes into this number and what it doesn’t capture.

Defining Unemployment: Who is Counted and Who Isn’t?

The Bureau of Labor Statistics (BLS) in the United States, for instance, defines an unemployed person as someone who is jobless, actively seeking employment, and available to take a job. This definition is critical because it immediately excludes several significant groups of people who, while not earning a traditional wage, are not officially counted as unemployed.

The Labor Force: The Foundation of the Calculation

The unemployment rate is calculated as a percentage of the labor force. The labor force consists of individuals who are either employed or unemployed (as defined above). This means that those who have stopped looking for work, often due to discouragement or other reasons, are considered “out of the labor force” and are therefore not included in the unemployment calculation. This distinction is vital when considering the broader economic picture. For example, if a significant portion of the population becomes discouraged and exits the labor force, the official unemployment rate might appear lower than the reality of economic hardship.

Discouraged Workers and Underemployment: A Deeper Financial Picture

Beyond the official U-3 rate, economists often look at broader measures of labor underutilization. The U-6 rate, for example, includes individuals who are marginally attached to the labor force (those who want to work but have stopped looking) and those who are working part-time for economic reasons but would prefer full-time employment. These individuals, while not technically unemployed, are facing financial insecurity. They might be earning less than they need, struggling to meet financial obligations, or delaying major financial decisions like buying a home or investing. Understanding these broader measures provides a more nuanced picture of the financial strain on households and the potential impact on consumer spending, a major driver of economic growth.

Financial Ramifications of the Unemployment Rate: From Personal Budgets to Market Stability

The unemployment rate is a potent barometer for individual financial well-being and has a direct correlation with various aspects of the financial markets.

Personal Finance: The Immediate Impact on Households

For individuals, unemployment represents a sudden and often drastic disruption to their financial lives. The most immediate consequence is the loss of income, which can trigger a cascade of financial challenges.

Income Loss and Budgetary Strain

The primary financial impact is the cessation of regular wages. This immediately strains household budgets, forcing difficult decisions about essential versus non-essential spending. Rent or mortgage payments, utility bills, groceries, and healthcare costs become immediate priorities. Savings accounts are often depleted to cover these basic needs, jeopardizing long-term financial goals like retirement or education. The ability to service existing debt, such as car loans or credit card balances, is severely compromised, leading to potential defaults and damage to credit scores.

Impact on Savings and Investment Goals

Beyond immediate survival, unemployment halts progress towards future financial security. Contributions to retirement accounts like 401(k)s or IRAs cease, and any investments may be liquidated to generate cash, often at unfavorable market prices. This can set back retirement planning by years, if not decades. The psychological stress of unemployment can also lead to impulsive financial decisions, further exacerbating difficulties. Furthermore, the inability to meet financial obligations can lead to increased debt, higher interest payments, and a prolonged period of financial recovery even after re-employment.

Broader Economic Impact: Influencing Business and Investment

The unemployment rate is not just a concern for individuals; it’s a critical data point for businesses and investors, influencing a wide array of financial decisions and market dynamics.

Consumer Spending and Business Revenue

A higher unemployment rate generally translates to lower consumer spending. When more people are out of work, they have less disposable income, leading to reduced demand for goods and services. This directly impacts business revenues, particularly for industries reliant on consumer discretionary spending, such as retail, hospitality, and entertainment. Businesses may respond by cutting production, delaying expansion plans, or even resorting to layoffs themselves, creating a negative feedback loop that can exacerbate economic downturns. Conversely, a low unemployment rate signifies robust consumer confidence and spending power, creating a favorable environment for business growth and investment.

Investment Markets and Economic Outlook

The stock market, bond market, and real estate sector are all sensitive to unemployment figures. A rising unemployment rate often signals economic weakness, which can lead to a decline in stock prices as investors anticipate lower corporate profits. Bond yields may rise as investors seek safer havens for their capital. Real estate markets can cool as demand falters due to job insecurity and reduced purchasing power. Central banks also closely monitor unemployment data when setting monetary policy. For example, a persistently high unemployment rate might prompt interest rate cuts to stimulate economic activity, while a rapidly falling rate could signal inflationary pressures that warrant interest rate hikes.

Navigating the Financial Landscape in an Uncertain Job Market

Understanding the unemployment rate is the first step; knowing how to navigate the financial implications is paramount for individual financial resilience.

Strategies for Financial Resilience During Unemployment

When faced with job loss, proactive financial management is crucial to mitigate the immediate and long-term impacts.

Emergency Funds and Budgetary Adjustments

The cornerstone of financial resilience is an emergency fund. Ideally, this fund should cover 3-6 months of essential living expenses. If one is unemployed, tapping into this fund is its primary purpose. Alongside this, a rigorous review and adjustment of the household budget are essential. Non-essential expenses must be cut, and a strict adherence to a revised budget is critical. This might involve renegotiating bills, seeking out cheaper alternatives for goods and services, and pausing discretionary spending entirely.

Unemployment Benefits and Financial Aid

Understanding and accessing available unemployment benefits is a vital immediate step. These benefits provide a crucial safety net, offering a temporary income stream to help cover essential expenses. Beyond unemployment insurance, individuals should research other forms of financial aid, such as government assistance programs for food, housing, or healthcare, if eligible. Exploring options for temporary debt forbearance or repayment plans with creditors can also prevent further financial distress and damage to credit.

Long-Term Financial Planning in the Face of Economic Volatility

Even when employed, an awareness of economic indicators like the unemployment rate should inform long-term financial planning.

Diversification of Income and Skill Development

Relying on a single source of income can be risky. Developing multiple income streams, whether through a side hustle, freelance work, or passive income investments, can provide a buffer against job loss. Continuous skill development is also crucial. Acquiring new skills or enhancing existing ones makes individuals more adaptable and marketable in a dynamic job market, reducing the likelihood and duration of unemployment.

Investment Strategies for Economic Uncertainty

Economic uncertainty, often signaled by fluctuating unemployment rates, requires a thoughtful approach to investing. For long-term goals, maintaining a diversified investment portfolio that includes a mix of asset classes can help mitigate risk. During periods of economic downturn, the opportunity to invest in quality assets at lower prices may arise for those with the financial capacity. However, it’s crucial to approach such decisions with careful research and consider professional financial advice. Understanding one’s risk tolerance and adjusting investment strategies accordingly is paramount.

In conclusion, the question “what percent of us is unemployed” is a gateway to a complex web of financial considerations. From the immediate budgetary crises faced by individuals to the broader market reactions and policy decisions, unemployment figures are a fundamental measure of economic well-being. By understanding the nuances of its measurement and its far-reaching financial implications, individuals and institutions can better prepare, adapt, and build greater financial resilience in an ever-changing economic landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.